1996 or 1999? Walsh's First Test is 'How to View AI'

"1996 or 1999? Wall's First Big Test Is 'How to View AI'"

Federal Reserve Chairman Wall's initial challenge is not whether to raise or cut rates, but a more fundamental judgment: what kind of boom is the current AI boom? This will determine the Fed's policy path and define his legacy.

Economics is split between two opposing views, according to reporter Nick Timiraos. One sees imminent productivity gains that will increase supply and cool inflation, allowing the Fed to hold steady. The other argues that while productivity benefits are distant, demand shocks are here now, and waiting for data confirmation risks missing the intervention window, forcing sharper rate hikes later.

Wall has signaled a leaning toward the first view, echoing 1996-era Alan Greenspan, who embraced strong, productivity-driven growth without fear of inflation. However, Wall faces a different macro environment than Greenspan did, with tariff pressures, expanding fiscal deficits, and diminishing globalization benefits, which could force more significant inflation pressures even if AI benefits materialize.

Wall's logic, expressed before taking office, is that AI-driven productivity gains won't show in official data for years. If the Fed waits for confirmation, it might mistakenly tighten policy and choke off the very growth that could suppress inflation. This argues for using forward-looking narratives over lagging data.

Chicago Fed President Austan Goolsbee presents a key counter-argument. He distinguishes between expected and unexpected productivity booms. A widely anticipated boom, like the current AI wave, can cause people to spend future wealth gains in advance, overheating the economy before productivity actually rises, thus requiring preemptive rate hikes. He cites rising costs for AI data centers as evidence of such overheating.

Fed Governor Christopher Waller offers a rebuttal to Goolsbee, noting the "expected spending" mechanism only works if people can borrow against future income, which many households cannot do due to borrowing constraints.

Wall also faces a paradox related to his desire to reduce the Fed's use of "forward guidance" (pre-announcing policy moves). This practice was established in 1999 when Greenspan began signaling hikes to avoid market shocks. If the economy follows a less optimistic path, Wall may be forced to choose between using the guidance he wants to abolish or risking market volatility by staying silent.

The ultimate question defining Wall's first major test remains: Is this 1996 or 1999?

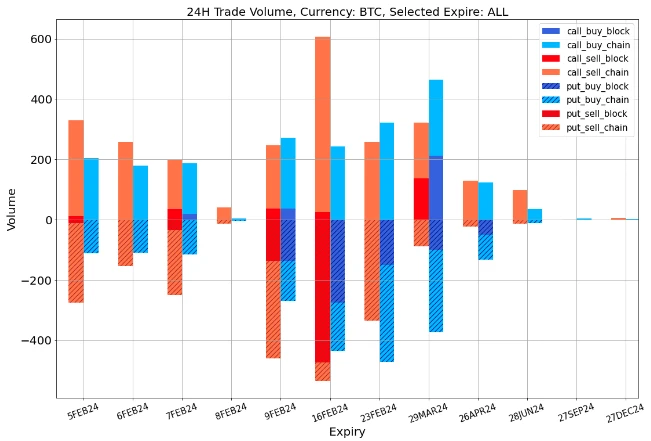

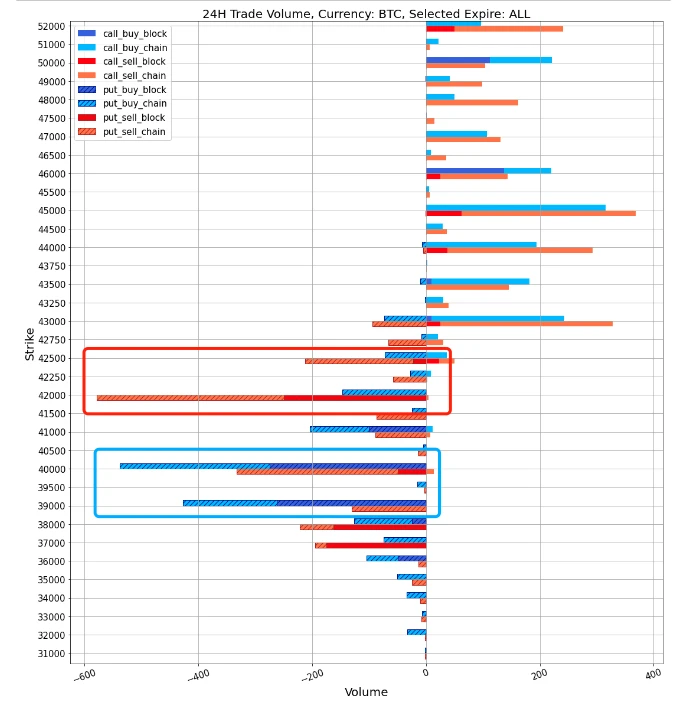

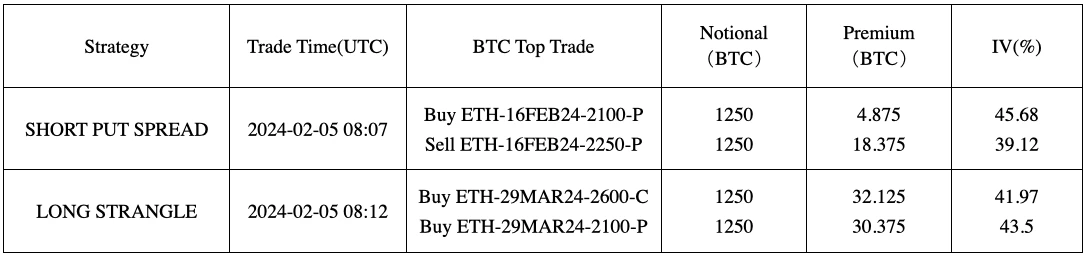

marsbit14h ago