昨日(18 JAN)美联储博斯蒂克向市场做出表态,他表示,如果通胀进展放缓,最好在更长时间保持较高利率,如果通胀率更快下降,可能会提前降息。在这之后,美国公布当周初请失业金人数录得 18.7 万人(低于预期的 20.7 万),是去年九月底以后的新低,凸显了劳动力市场依旧稳健的现状,并再次打压了市场对美联储降息的预期,美债收益率应声走高,当前两年期和十年期分别为 4.346% /4.150% 。美国三大股指高开高收,道指/标普/纳指分别上涨 0.54% /0.88% /1.35% 。

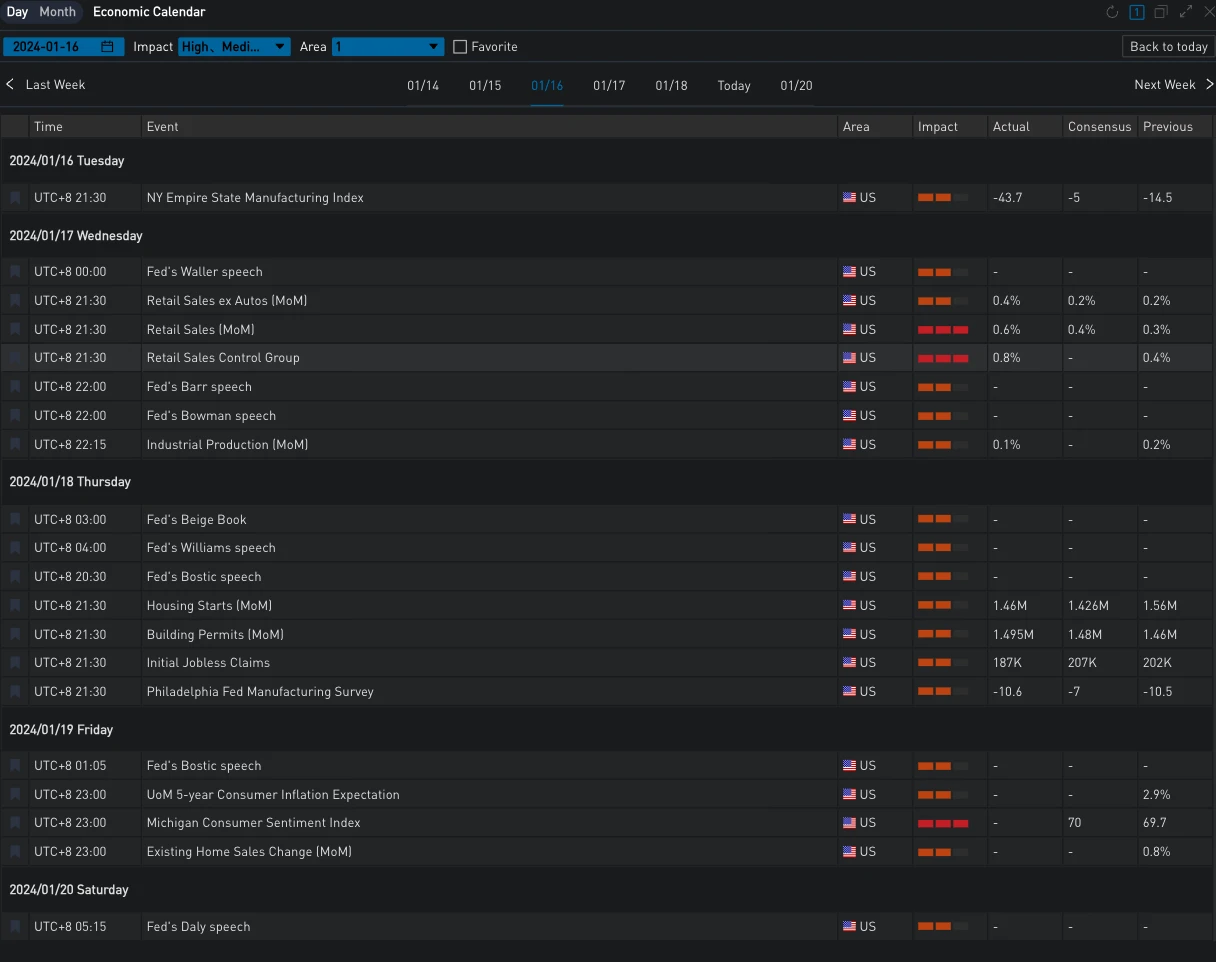

Source: SignalPlus, Economic Calendar

数字货币方面,在接近一周的横盘行情过后,BTC 于昨日短线下挫约 5% ,一度挑战 41000 关口并受到支撑,创下 ETF 批准后的新低点。市场密切关注与 ETF 相关的资金流向,不少分析都将近期 BTC 的下行归咎于灰度 BTC 的抛压,其中,摩根大通指出了流动性和市场深度的重要性,表示如果 GBTC 失去流动性优势,可能会有更多的资本退出,金额将达到 50 亿至 100 亿美元;同时也提到,在机构投资者陆续退出 GBTC 的同时,“来自散户投资者的比特币钱包最近几天有所缩减”,他们似乎正从交易所转向更便宜的现货 BTC ETF。

Source: Binance & TradingView

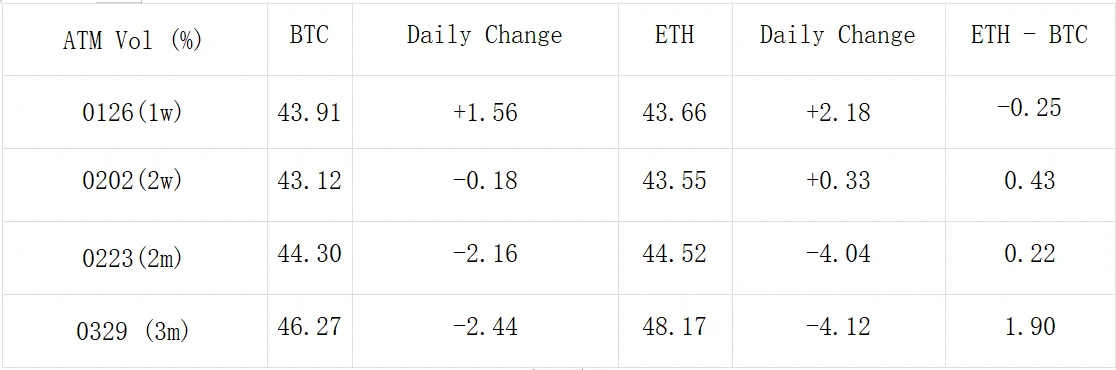

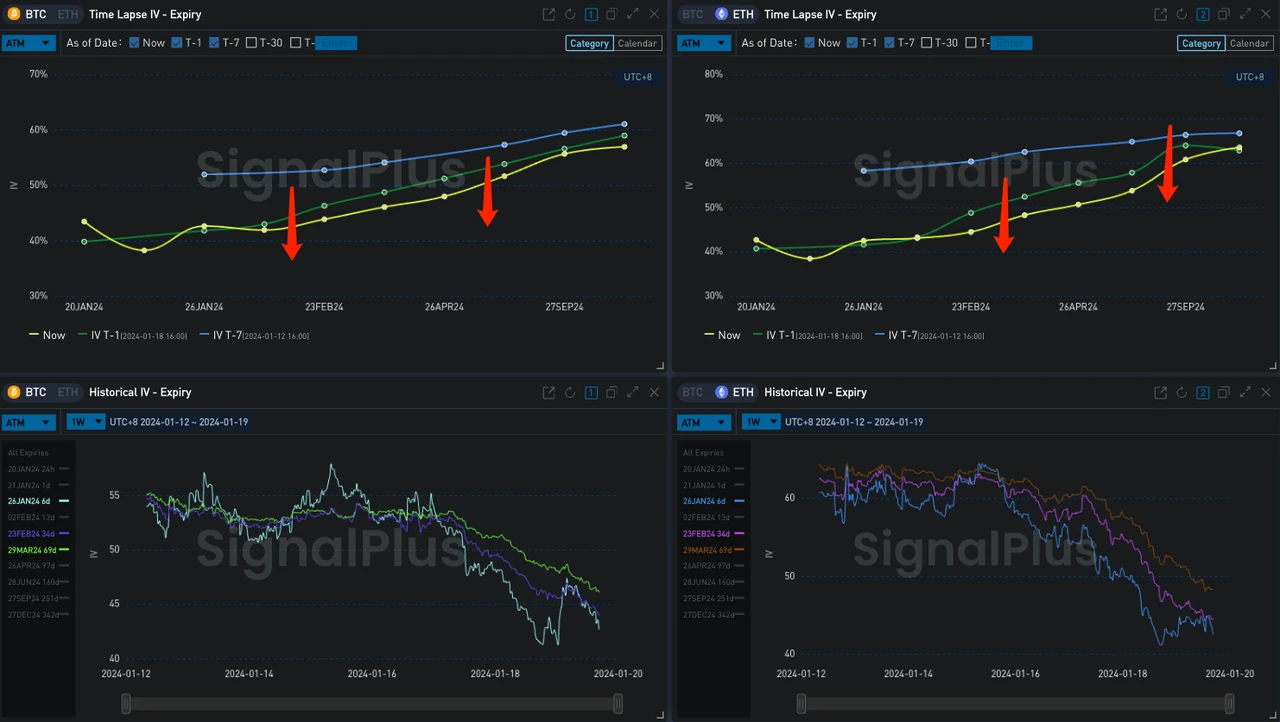

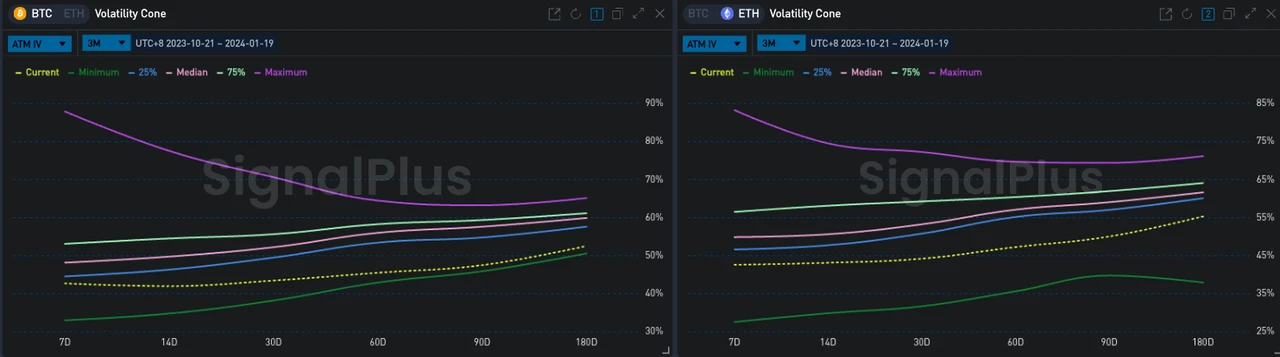

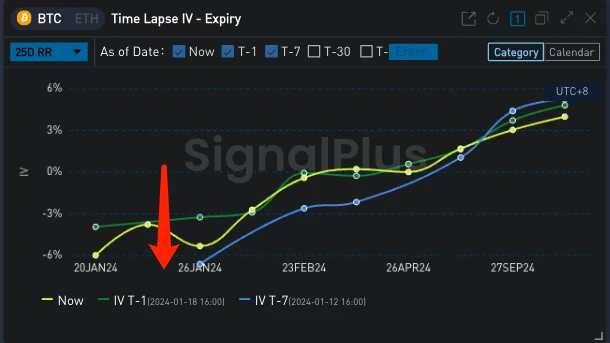

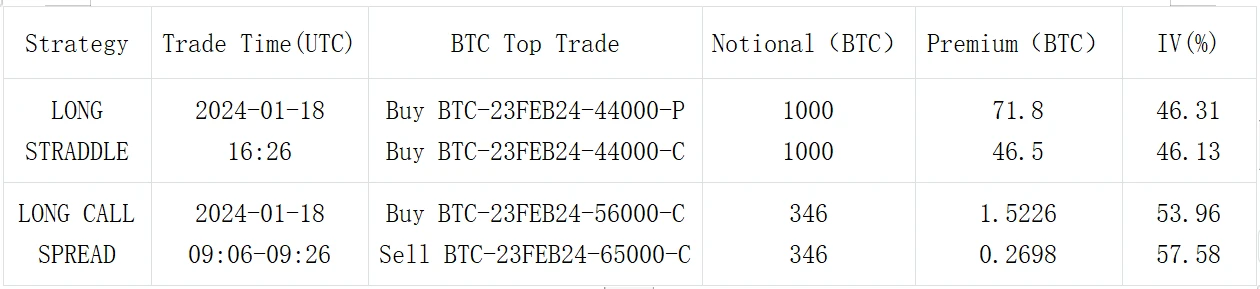

期权方面,过去 24 小时 BTC/ETH 中远端 IV 再度降低了 2% /4% 左右,BTC 整体水平几乎已经贴近过去三个月以来的最低点,同时在交易商,ETH 一月和六月底分别出现了数笔看跌波动率的 Short Strangle,但 BTC 上则相反,交易员选择了在过去三个月以来低点时刻逢低买入 23 Feb 44000 Straddle 看涨波动率,此处也接近该期限曲面的最低点。另外,一月底交易最为活跃,市场上明显出现了买 put 卖 Call 的倾向,使得该到期日 25 dRR 下行大约 2% 至 Vol Skew 曲线低点。

Source: Deribit (截至 18 JAN 16: 00 UTC+ 8)

Source: SignalPlus

Source: SignalPlus

Source: SignalPlus, BTC 一月底 25 dRR 下降 2% 至 Vol Skew 曲线低点

Source: Deribit Block Trade

Source: Deribit Block Trade

您可在 ChatGPT 4.0 的 Plugin Store 搜索 SignalPlus ,获取实时加密资讯。如果想即时收到我们的更新,欢迎关注我们的推特账号@SignalPlus_Web3 ,或者加入我们的微信群(添加小助手微信:xdengalin)、Telegram 群以及 Discord 社群,和更多朋友一起交流互动。

SignalPlus Official Website:https://www.signalplus.com