原创 | Odaily星球日报

作者 | Loopy Lu

今日,加密市场的走势再次大幅上扬,Odaily星球日报于今早发布《BTC 再度逼近 38000 美元,小牛结局还是大牛伊始?》一文报对行情进行了解读。

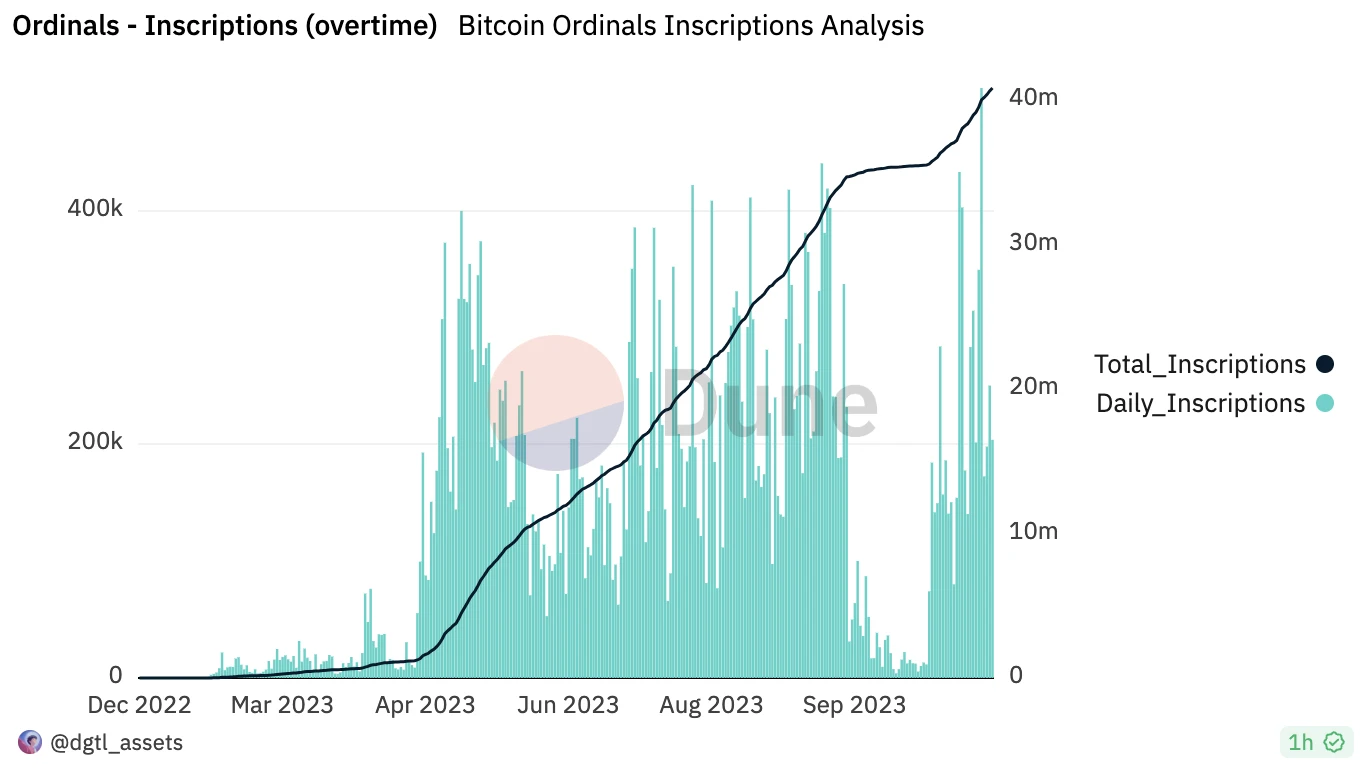

而在大盘亮眼的表现中,BRC-20 板块的狂飙突进最为引起投资者关注。比特币铭文市场已经迎来了“狂暴大牛”,铸造的比特币序数铭文总数已攀升至新纪录。

Dune 数据显示,过去一天,单日铸造的比特币序数铭文数量激增至 50.5 万个,创下历史新高。而截至目前,全网铸造的铭文总数已经超过4083 万枚,为了完成这些铭文的铸造,已经消耗了约2564 枚 BTC,约合9614 万美元。

投资者不仅对铭文的铸造热情高涨,BRC-20 的市场也一样极度繁荣,多种 BRC-20 代币在今日快速上涨。

Odaily星球日报统计了多个市值较大、近日热度较高、且快速上涨的 BRC-20 代币,具体情况如下:

近一周以来,多款铭文代币获得了数倍的涨幅。例如,rats 或许是今日话题最高的 BRC-20 代币,这一代币近日的高额获利让社区热议其或许是下一个 meme。而一些小市值代币则更容易在短时间内快速拉升,例如,mfsq、jpeg 均在今日一日之间获得了超过三倍的涨幅。

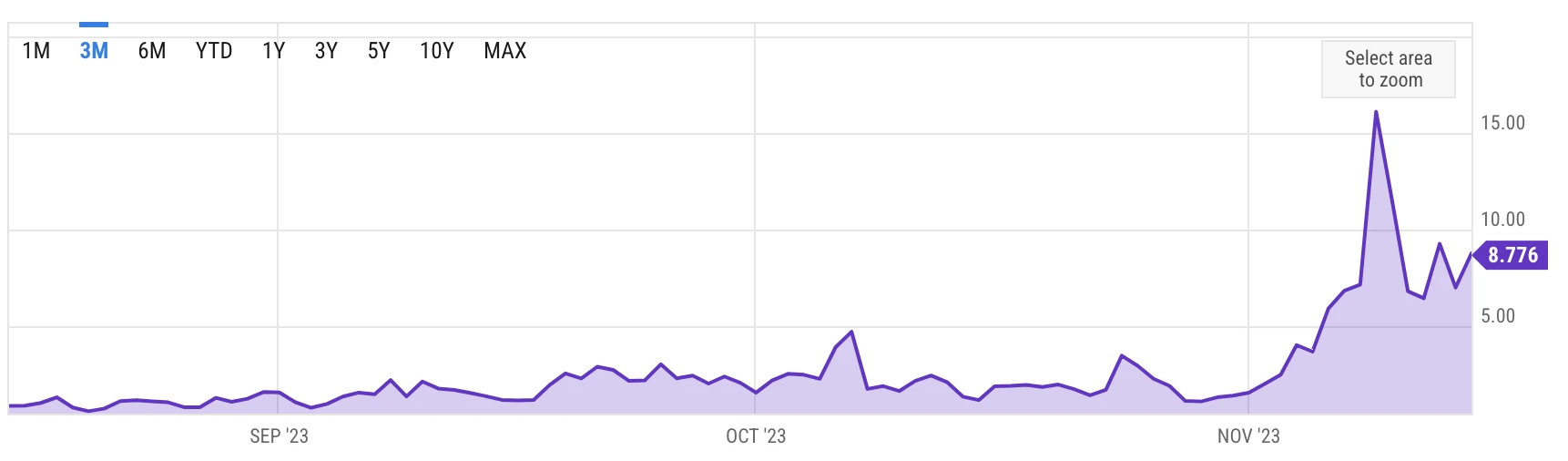

BRC-20 市场的火热,也引发了链上手续费的飙升。

Ycharts 数据显示,本周稍早时,比特币的平均费用一度飙升至 15.86 美元,目前仍在接近 10 美元的高位区间。

本轮 BRC 牛市,矿工无疑成为了最大的获益方之一。目前,减半距离我们并不遥远。明年减半之后,比特币区块奖励将从 6.25 BTC 减少到 3.125 BTC,而手续费的快速攀升无疑为矿工提供了更为丰富的收入来源。

而作为 BRC-20 生态的“龙头”代币,ORDI 的涨幅虽然(与其他 meme 相比)并不瞩目,但这一代币已经成为了庞然大物。

欧易 OKX 行情显示,ORDI 价格今日一度达到 27.8 美元,创下历史新高。目前 ORDI 市值约为 5.3 亿美元,coingecko 数据显示,这一市值表现已经进入加密世界的前 100 位排名,目前为市值第 96 大的代币。对于一款新生的 meme 币来说,这一表现颇为亮眼。

今日,除“传统”的比特币铭文市场外,Polygon 铭文也一度引发链上 gas 飞涨。

目前,铭文市场全面“起飞”,其价值早已外溢至不止 BTC 一条链。而从社区的立场出发,我们可将其解读为投资者对这一新兴市场的看好。但若从“刻舟求剑”的角度解读,meme 的“漫天飞舞”,是否又是一场“闪崩”的前奏呢?Odaily星球日报将保持关注。