“Why would anyone buy a token? How is this internet funny-money supposed to be valuable? It’s all just a big ponzi where everyone is trying to find a greater fool to buy their bags, isn’t it?”. These are important questions that can help us clarify our thinking. Skeptical voices tend to increase in volume during market downturns, so this may be a good time to go back to basics and join skeptics in asking “Why are tokens valuable?”.

First things first, tokens that are live and tradable have a clearly defined value in form of their market price. The market price at any time is a function of supply and demand. When it comes to the supply side, different tokens have widely different numbers for their total supply, so comparing their prices would be comparing apples to oranges. What is more, some tokens also increase their supply over time. For that reason, the best metric to compare the value between tokens is the fully diluted market capitalization, to account for the differences in token supply. But where does the demand, the other side of the equation, come from?

Tokens are valuable for different reasons. The framework of “super asset classes” provides an answer to the question of demand, and therefore value, for different types of crypto assets. In this article, we first quickly introduce the framework of super asset classes. We then apply it to today’s landscape of tokens. Finally, we outline the different drivers of demand for each of the super asset classes.

Applying super asset classes to tokens

“Super asset classes” is a theoretical framework to categorize different asset classes published by Robert J. Greer in 1997, and popularized by Chris Burniske, who attempted to classify Bitcoin in 2016. The conclusion was that Bitcoin could not be classified into any of the existing super asset classes since it exhibits properties of several ones. The 2016 ARKInvest whitepaper argued that Bitcoin should be considered as its own, novel super asset class. Since then, a lot has happened in crypto so it makes sense to apply the framework beyond Bitcoin to different types of tokens and crypto assets.

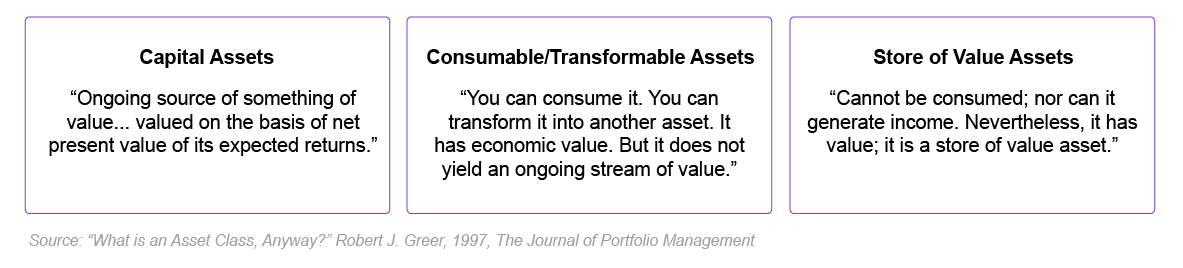

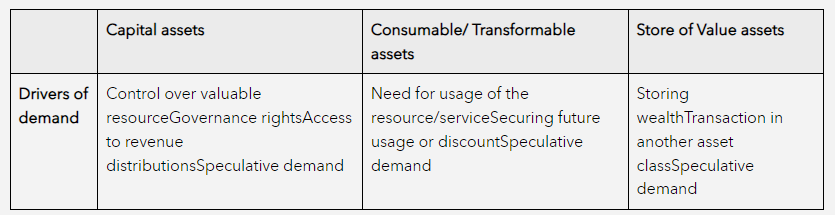

The three super asset classes are “Capital Assets”, “Consumable/Transformable Assets”, and “Store of Value Assets”.

The image above shows the definitions for each asset class, as provided by Robert J. Greer.

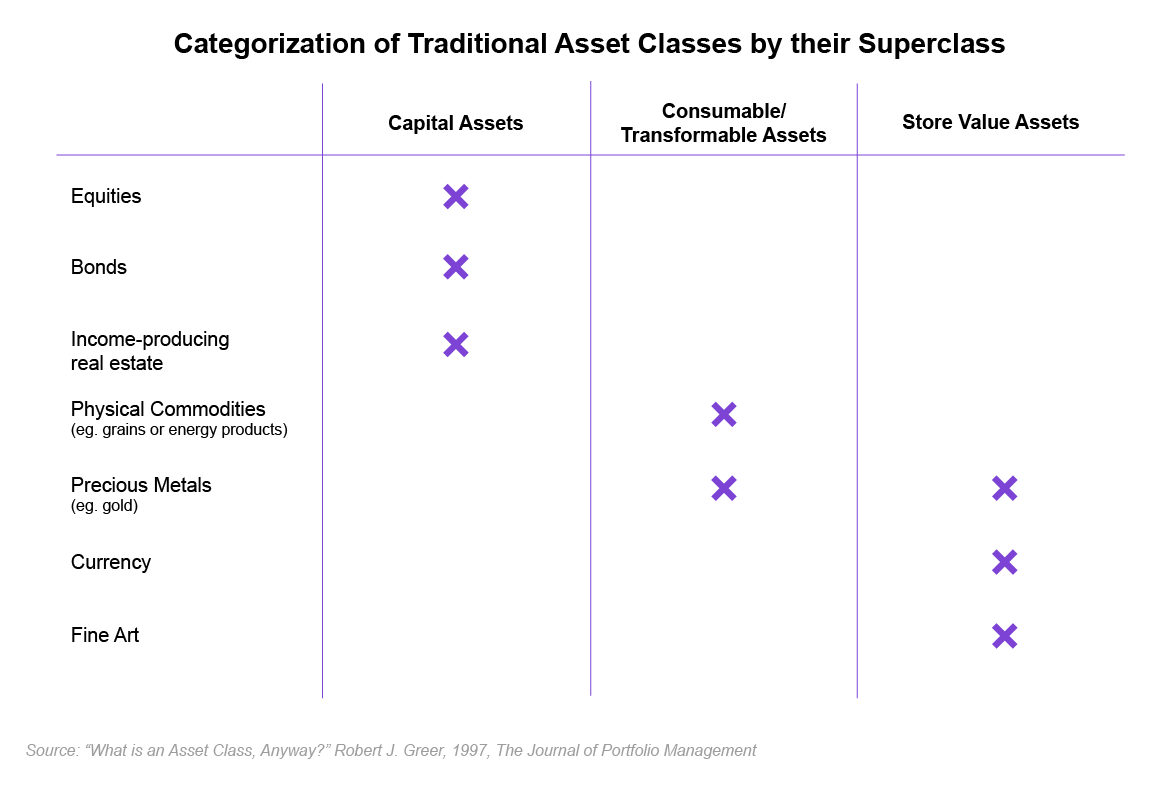

The table above shows the application of super asset classes to traditional financial asset classes. Crypto assets exhibit similar properties as traditional assets, so it makes sense to apply the framework to tokens. Since tokens are programmable money, they may fit in several super asset classes at the same time.

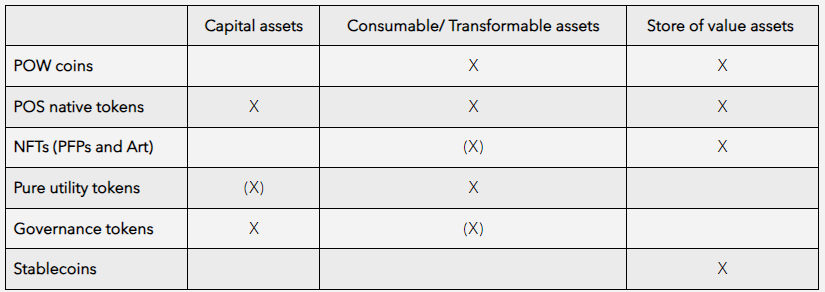

The table above proposes an updated classification of crypto assets and classes of tokens into the super asset class framework. The “X” in brackets designate cases where a type of crypto asset is starting to enter an additional super asset class.

Note that Proof-of-Work coins like Bitcoin and Proof-of-Stake native tokens like Ethereum fall squarely between traditional super asset classes. Bitcoin clearly has properties of both Consumable/Transformable assets (since it’s needed to pay for transaction fees) as well as Store-of-Value Assets (since it commands a monetary premium and has politico-economical implications). Ethereum, in addition, also has properties of a Capital asset since it gives a recurring yield to its holders through staking rewards. For that reason, ETH has been described as a “triple-point asset” by Bankless. Since both of these classes of crypto assets fall between traditional super asset classes, one could argue that they create novel super asset classes, like the ARKInvest paper originally argued. Alternatively, we can continue using the original three super asset classes and allow layer one assets to fall between the asset classes. This approach seems reasonable due to the programmability of tokens which renders the boundaries between the super asset classes much softer.

Most NFTs that exist today can be described as a Store-of-Value asset, analogous to fine art in traditional asset classes. Profile Picture collections and Art NFTs especially fit that bill in general. However, there has been increasing focus on utility for NFTs, so they are starting to fit the Consumable/Transformable class better. As new types of NFTs start getting traction, it might make more sense to classify them on an individual basis. For instance, real-estate NFTs would look more like Capital assets and not Store of Value assets like PFPs and Art NFTs.

The class of Pure Utility tokens is what most closely fits into the super asset class of Consumable/Transformable. Within Web3, there are many decentralized resource networks that include tokens to coordinate supply and demand. Examples include assets tied to file storage networks like FIL (IPFS) and Arweave (AR), compute networks (RNDR or GLM) or even data connectivity like Uplink. Since some of these include mechanisms like staking that provide a yield in terms of the token, they sometimes exhibit properties of capital assets too.

Discount functionality for a given product or service is another typical example of pure utility. The addition of “Pure” to “Utility Tokens” is to differentiate from the legal use of the term “Utility token”, e.g. as defined by the Swiss regulator FINMA.

Governance tokens, whether for DeFi protocols like COMP (Compound) or MKR (MakerDAO), or different DAOs like investment DAOs, clearly fall into the Capital assets category. The protocols or DAOs that they govern produce an “ongoing source of value”, whether through fees generated, investment returns, or other flows of value. As a result, control over those valuable assets can be considered Capital, whether or not there are regular flows of value paid to token holders (as is the case with some governance tokens, e.g. GMX). Chris Burniske has also argued for governance tokens as a Capital asset. However, governance tokens frequently have other utility functions on top of the governance capabilities, such as a discount functionality. In those cases, governance tokens could also be considered as Consumable/Transformable.

Finally, Stablecoins are a clear case of Store of Value asset, since their sole purpose is to be used as currencies. Often, they are even pegged to existing fiat currencies such as the US Dollar.

Different drivers of value per crypto asset super asset class

Now that we have categorized different classes of tokens into the framework of super asset classes, let’s have a look at what drives demand for each of them.

People want to buy or hold Capital assets like governance tokens for the control rights that they hold. Whether they have a special interest in the valuable protocol or assets being governed, or whether they are interested from an investment point of view, the interest is always specific to the protocol in question. It’s not that they want just any governance token, but the governance token of a specific protocol they are interested in, for example Uniswap. There are different reasons for somebody to have an interest in Uniswap governance, whether as a user, a builder, or a liquidity provider, just to name a few. The investment motivation becomes more pronounced if there are recurring distributions to token holders. As the perceived value of the governance token increases, so does demand for it and therefore its market value.

The primary reason to buy Consumable/Transformable assets like Pure Utility tokens is the resource network it grants usage of. For example, someone might want to store files on IPFS, whether as an individual or as a developer of an application making use of the protocol. We can distinguish between the desire to use a resource network now or in the future. In the latter case, one might want to buy the corresponding tokens earlier than they are needed to secure access at a given market price. As a resource network becomes used more heavily, its corresponding token is demanded in larger quantities, leading to an increase in its value.

When it comes to Store of Value crypto assets, the primary motivations to buy them are either to preserve value into the future or to use them as a medium of exchange for another asset. Depending on the risk profile, one might choose a Stablecoin or Bitcoin/Ethereum. PFP and Art NFTs add aesthetic, expression, and identity dimensions to the purely financial considerations, so reasons to buy those are more similar to acquiring fine art.

In all of the different cases, speculative demand is another reason for buying any token. It is important to note that the classification of tokens into super asset classes does not say anything about the legal status of tokens, which needs to be determined case-by-case and will differ across jurisdictions.

Qualitative and quantitative indicators for demand

We saw how tokens are valuable for different reasons and how the framework of super asset classes provides a great starting point to differentiate between different drivers of demand. Crypto assets are still novel and therefore, speculative demand is arguably a significant factor across the different super asset classes. So a large part of the demand is actually a bet on future demand of different kinds.

Having laid the groundwork for the value of tokens in this piece, we will expand on it in forthcoming articles. We will look at different indicators, both qualitative and quantitative, that can be used to compare tokens of the same class with one another. We will especially look at the “Capital Assets” super asset class, where valuation methods and ratios from traditional finance can best be applied. Asking the question “Why is this token valuable” and attempting to answer it in a principled way is crucial to separate signal from noise in Web3.