DeFi 领域正在酝酿一个热门的新叙事——“真实收益”(Real Yield),协议根据其创造的收入向用户支付收益。

🧵本文就要聊聊这个新叙事,其为什么能够成为下一周期的支柱以及具有代表性的项目。👇

真实收益归类为“真实”收入产生的收益,而并非发行代币产生的收入。真实收益运作方式很直接:更多的收入 = 支付给用户更多的收益,反之亦然。

因此,押注一个真实收益项目其实就是在赌它 a)积累新用户以及 b)增加创收以奖励代币持有者的能力。

在我讲一些具有代表性的项目之前,了解这个叙事的来源是很重要的。

让我们回到 2021 年。当时吸引用户最常见的方式就是以高昂的 APR 为诱惑,从而吸引更多的 TVL(不惜一切代价)。

这些 DeFi 协议都是通过发行/稀释代币来进行激励的例子。

$TIME

$SUNNY

$AXS

$ANC

事实是,2021 年几乎所有 DeFi 协议都采用了激进的代币发行模型以达到快速吸引流动性的目的。

为什么会这样呢?因为这是一场比赛。用户的兴趣和贪婪达到了空前的高度。项目方感受到了这种 FOMO,而且不想错过。

问题在于,这种模式是不可持续的。在被迫转向可持续的模式之前,项目方只能在有限的时间内提供人造收益。没有这些人造收益来激励用户存钱和质押,很多 DeFi 协议都会面临可预见的崩溃。

这就导致很多投资者在 $LUNA 和 $UST 上蒙受了重大的损失。PTSD(创伤后应激障碍)和 DeFi 随之而来的崩溃导致的用户流失突显了当前 DeFi 领域的致命缺陷:

A) 通过激励流动性来发行代币人为扩充了 TVL。一旦失效,很多链的“真实”价值就暴露了。

B) 很多协议都不具备精心设计的底层价值增值机制。

结果是什么呢?随着市场偏向避险,就会出现从“虚假”到“真实”收益协议的急剧转变。这种转变体现在近期永续 DEX 的增长以及在合并(The Merge)预期下以太坊生态的反弹。

以下是我最喜欢的真实收益项目,他们都是通过实际的收入来产出收益的。我会简单说说他们的情况,如何产生收入以及他们的潜力所在。

第一类属于“去中心化永续交易所”范畴。

他们提供高流动性和低费率的杠杆交易,同时拥有所有 DEX 和 CEX 具备的正面优势:

没有 KYC

没有交易对手风险

安全

独立自主

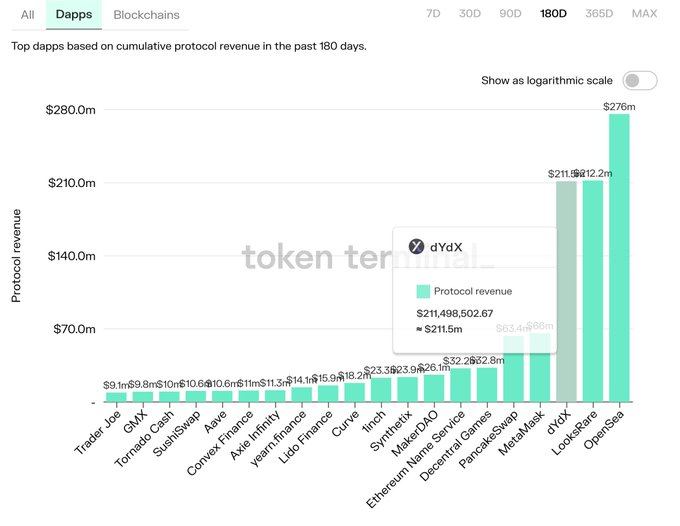

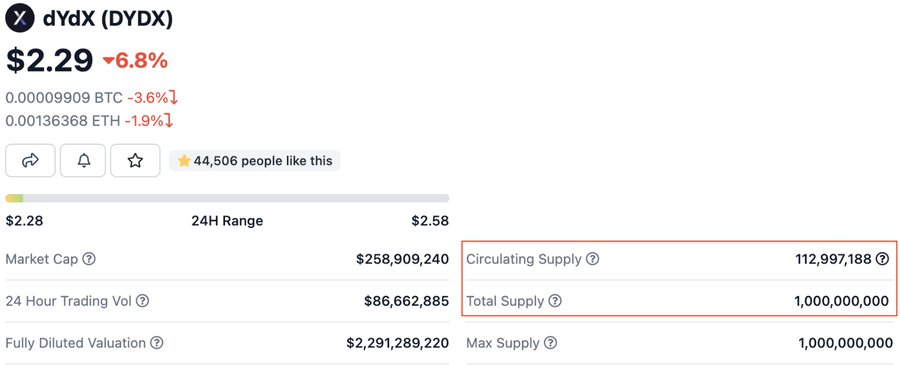

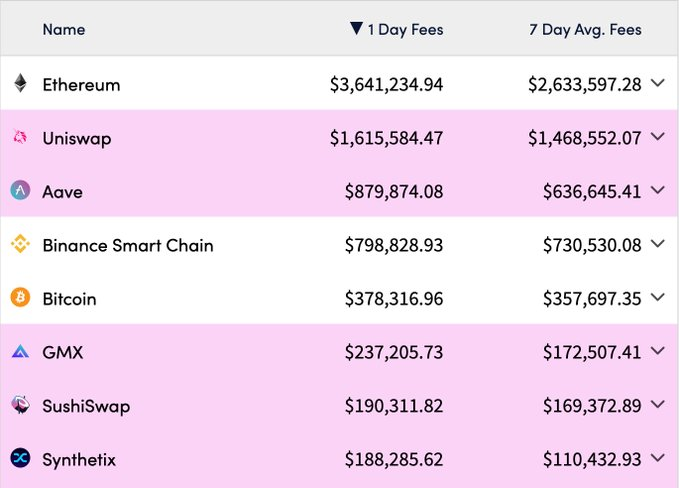

首先是 $DYDX。据 Token Terminal 的数据,dYdX 是最大的且使用永续交易最多的 DEX,每年产生超过 3.21 亿美元的协议收入,在 dAPP 协议收入中排名前三。

现阶段 $DYDX 的收益仍是中心化的(并未直接支付给代币持有者),但他们计划在今年年底的 V4 更新中改进这一模式。

$DYDX 还将面临大量稀释。因此,就目前而言,其在众多竞争对手中并不配备最好的代币经济学,然而……

我认为 dYdX 最大的利好在于其即将在 Cosmos 上推出自己的链。与其他 DEX 相比,dYdX 的灵活性为他们提供了得天独厚的优势,这也是我长期看好这个项目的原因之一。

其次是 $GMX,Arbitrum 上最大的项目(TVL 2.5 亿美元),在 $AVAX 上排名第 7(9000 万美元)。

GMX 以独特的多资产池为基础,赚取 LP 费用,可实现现货资产 30 倍的杠杆交易,且滑点很低。

可以说 GMX 在所有永续 DEX 中拥有最好的代币经济学。质押 GMX 代币可以获得 30% 的平台费用,以 ETH 支付。另外还有一个 esGMX 模型来激励流动性的“粘性”。

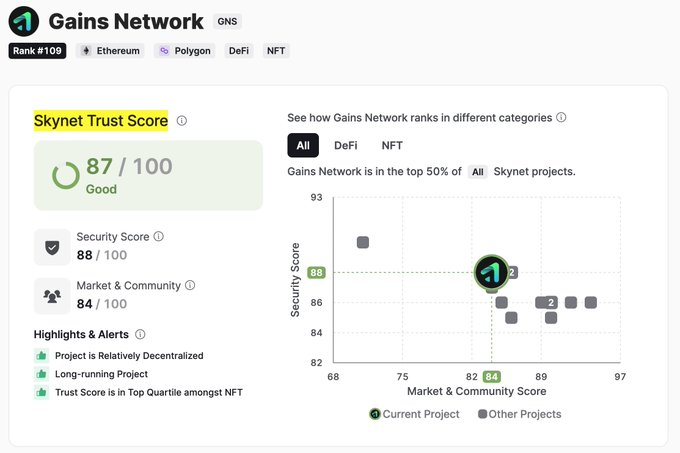

然后是 $GNS。Gains Network 基于 Matic,其首发产品 gTrade 近期的交易量超过了 150 亿美元。它拥有时尚的用户界面、出色的代币经济学,与同类产品相比,其市值“适中”,为 6000 万美元。

CertiK 给 $GNS 的安全评分很高,信任评分为 87,社区评分为 84(总分 100)。

(鉴于近期的 DeFi 攻击事件,在投资一个项目之前了解它是否值得信赖还是很有必要的。)

上述三个 DEX 都是不错的选择。有关这几个永续 DEX 的对比,更多的信息可以参见 @gnsGoblin 以及这篇文章。

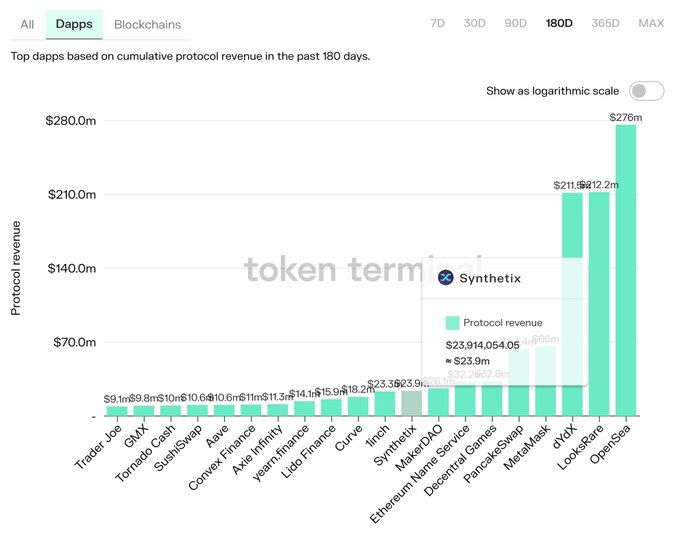

$SNX:基于以太坊和 OP 的去中心化合成资产协议。也就是说,你可以互相交易虚拟和现实世界资产,如黄金、白银、加密货币、欧元、石油和股票。

你可以质押 $SNX 来赚取 $sUSD 和 $SNX。他们通过协议费用(由铸造/销毁合成资产产生的费用)产出收益。

据 Token Terminal,$SNX 目前每年产生 1 亿美元的协议收入,在收入排名中位居第九。

可以看到 $SNX 和 $GMX 产生的费用都排名前十,超过了整个加密货币领域 7 天 1 亿美元的平均值。

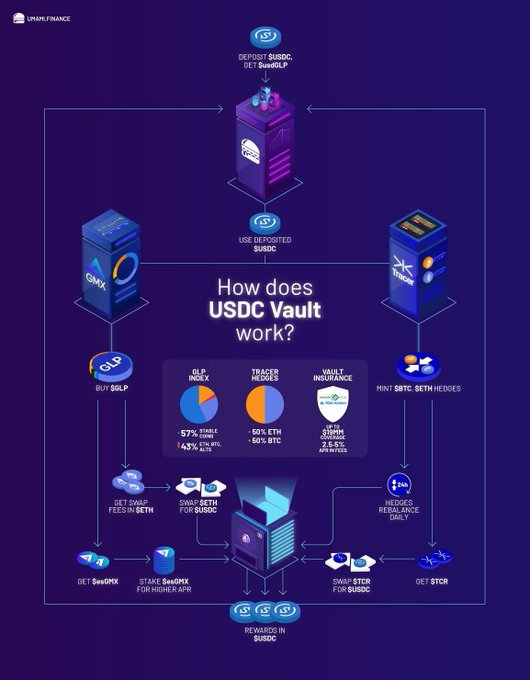

$UMAMI:它最大的创新就是 USDC Vault。与 Anchor 不同,它支付了 20% 的可持续收益,由铸造 GLP 和收取交易费用产生。他们还将推出 ETH 和 BTC Vault。

还有很多其他项目都符合真实收益这一新叙事,包括:

$RBN

$BTRFLY

$DPX

$LOOKS

$FXS、$CVX、$CRV

一些补充信息:

我认为,真实收益从客观上说一定更好,这是一种误解。

发行代币也有自己的目的。很多协议都通过发行代币提高了 APR,从而成功获取了很多新用户,并且建立了很好的社区。

很多一开始采取了激进的发行计划的代币都开始逐渐向费用生成模式转变。最终,只有能够产出真实收益的协议才能成功。炒作和通胀都只能体现在短期的价格表现上。

尽管会有很多 DeFi 协议转向这个模式,但有些会失败,因为脆弱的代币经济学;有些会成功,因为成功适应了新的架构。

无论如何,真实收益越来越趋近于 DeFi 的未来。只有成功部署可以同时驱动普及和收入生成的项目,才能在未来几年蓬勃发展。

随着这一领域的成熟,投资者将倾向于选择能够产生真实和可持续收入的协议,尤其是在市场动荡的情况下。

对于机构 DeFi 而言,寿命和风险调整后的增长潜力也将成为关键考虑因素。