撰文:mikey,1kx 分析师

编译:Luffy,Foresight News

预测市场出现了许多新的建设者,因此有必要对这个垂直领域进行一次全面的概述。本文将简要总结预测市场类别、GTM(进入市场)策略、产品更新、机制以及当前的发展方向。

GTM

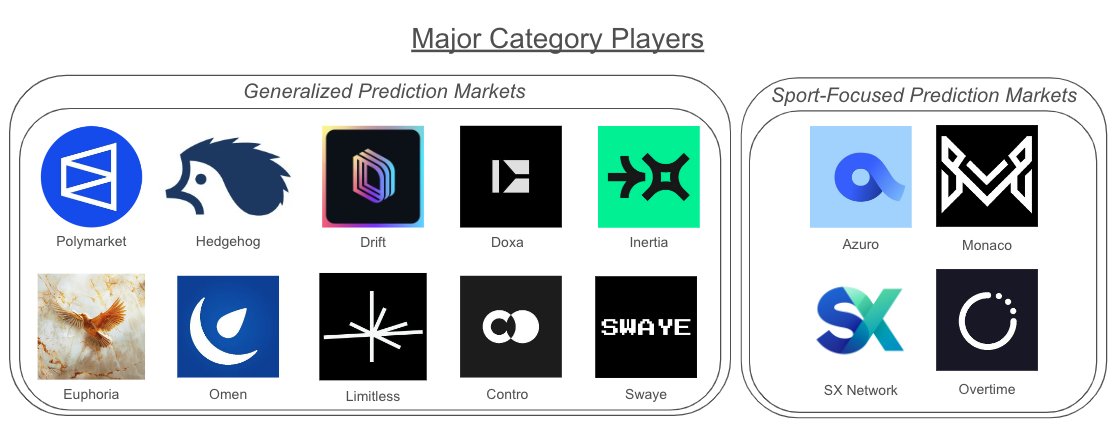

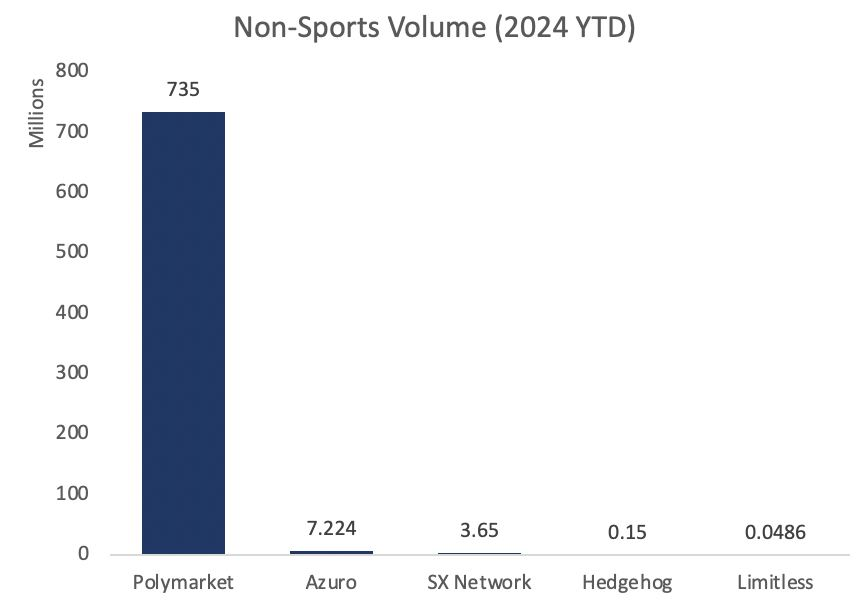

预测市场 GTM 大致有两种方法:非体育和体育。前者是一个相对未开发的领域,包括几个目标领域:加密货币、政治、文化活动。Polymarket 显然是非体育领域的领导者,其 GTM 主要关注政治事件。

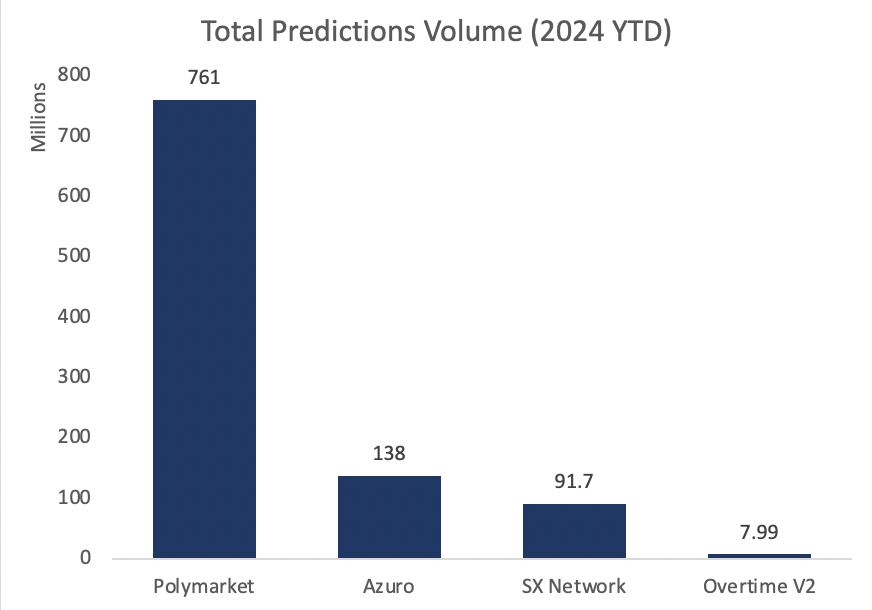

如果比较专注体育赛事的预测市场今年以来的交易量,你会发现 Azuro 和 SX Network 与 Polymarket 的差距更大。

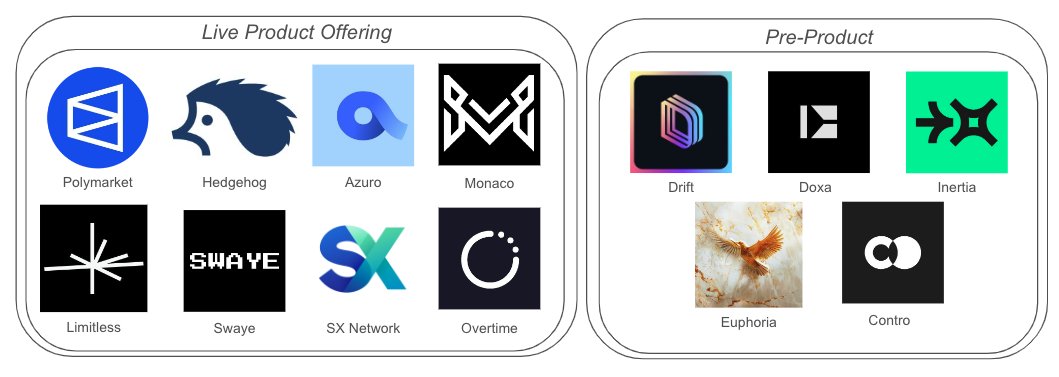

新上线的竞争者包括 EVM 上的 Limitless (其中一些市场支持 ETH 交易),以及 Solana 上的 Hedgehog。此外还有竞争者产品尚未上线,包括:Drift Exchange、xMarkets、Inertia Social、Doxa 和 Contro。

新玩家们普遍聚焦于两个共同主题:

-

无需许可的市场:开放市场创建和激励层

-

解决方案:依靠人工智能进行市场结算,或创建更高效的系统

这正是 Polymarket 用户一直期盼的。

鉴于体育类预测市场受欢迎程度和赛事规律性,它们在 Web2 中具有明显的吸引力。很难让用户转移到 Web3,因为大多数用户看重品牌和用户体验。此外,Web2 体育博彩在营销资金上具有优势,至少有 5 家体育博彩公司每年花费 1 亿美元以上。

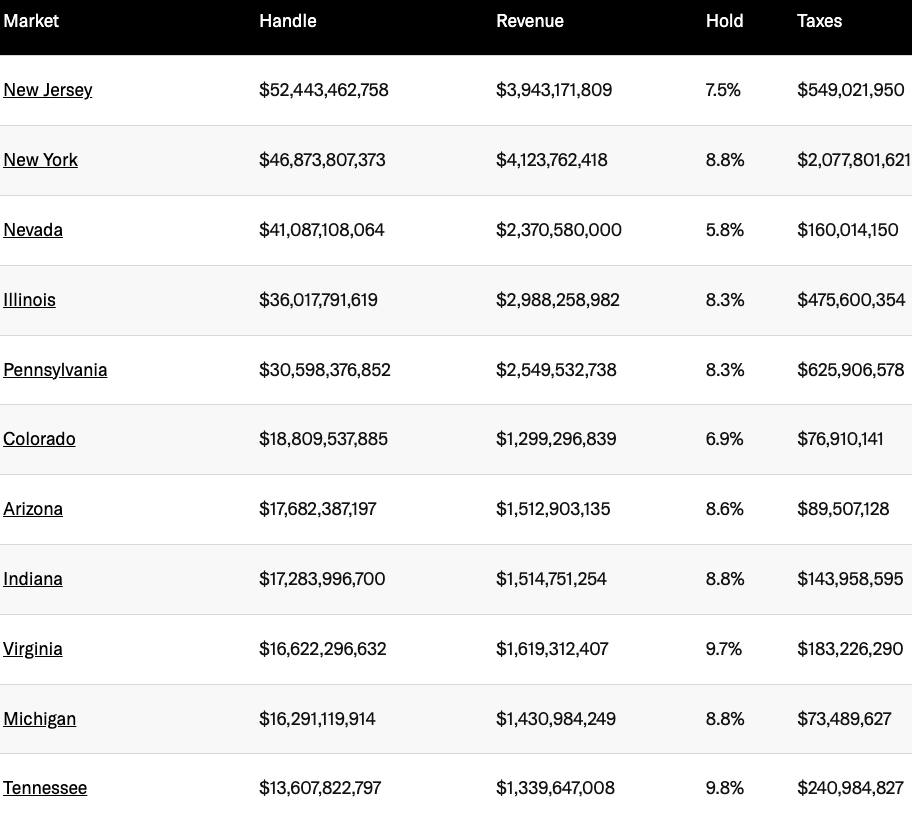

美国人在单场超级碗上的投注金额(约 230 亿美元)是加密货币预测市场总投注额(约 20 亿美元)的 10 倍。甚至单个州的投注金额就远远超过了 20 亿美元。

链上资金越多 = 链上体育博彩越多,就像互联网博彩公司被手机设备统治一样。预测市场的限制因素之一是缺乏资金。在非体育方面,LogX 将支持 TRUMP 永续产品,类似于 2020 年的 FTX。Doxa 也在研究 lev。这两个项目的交易对手都是流动性池。清算和坏账是潜在的问题。

我希望 Polymarket 更多地探索复式投注模式。从技术上讲,「特朗普和拜登赢得提名」市场是一种杠杆投注,因为它需要猜测两个不同的事件。

我很想看到诸如「a、b、c 和 d 会发生吗」这样的市场,我不认为初始流动性会成为问题,LP 不会错过这样的机会。

在体育预测市场方面,已有多个协议允许通过所谓的 parlays 进行杠杆操作,只有当用户正确猜出多个不相关事件时才会赢得奖金。SX Bet、Azuro 和 Overtime 已经支持这种功能。

机制

预测市场的工作机制大致有两种类型:Web2.5 和 Web3。Web2.5 模式通常将加密货币用作支付渠道,例如 Stake/Rollbit。用户可以使用加密货币下注,但交易对手是应用程序背后的团队,并且产品在链上交互。

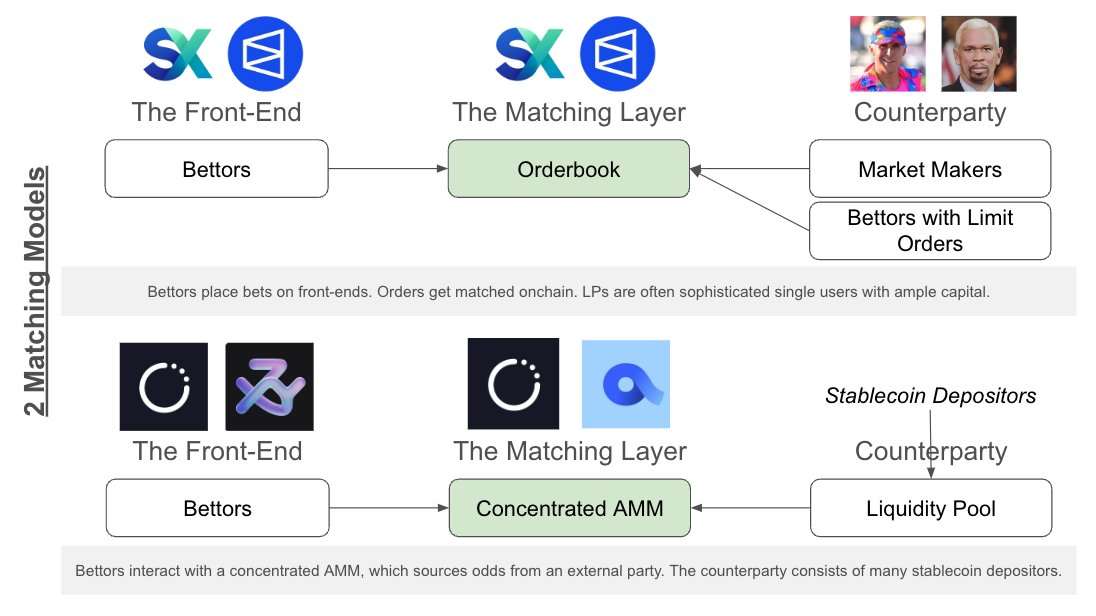

Web3 模式的部分产品逻辑会放在链上,无论是 NFT 头寸,还是通过智能合约执行的赌注。通常有两种方式来匹配链上赌注,要么是依赖被动 LP 的 AMM,要么是平台充当交易所的订单簿。

在 Web3 中,Memecoins 本身已经成为预测市,$TRUMP 和 $BODEN 就是典型的代表,持有者可以从两方面获利:1)方向正确;2)吸引注意力。Memecoins 允许你推测其他人的投机行为,无论你是对是错。

一个新的协议叫做 Swaye,尝试结合预测市场和 Memecoins 的优势,早期进入市场的用户不仅押注特定结果,而且有动力吸引注意力,因为任何一方的投注活动都有助于增加 P 损益。

盈利模式

预测市场协议如何盈利呢?有几种方法:

-

交易费

-

交易者收益的一部分(Web2 模型遵循这条路径)

-

交易对手的损益(Web2 喜欢服务亏损的客户)

大多数协议要么采用方法 1,要么采用方法 3。Polymarket 目前不收取任何费用。

下一步

下一步是什么?人工智能代理是预测市场的下一个大机遇,因为它们可以对新闻做出快速反应。它们能够管理订单和下注,它们还可以计算结果的预期值并承担计算出的风险。有几个团队正在研究这一领域。

在未来几年,至少会有 1 个协议与 Polymarket 的交易量正面竞争。考虑到 Polymarket 目前对其市场的激励程度,竞争者可能需要大量使用积分、代币或 USDC 等激励措施。

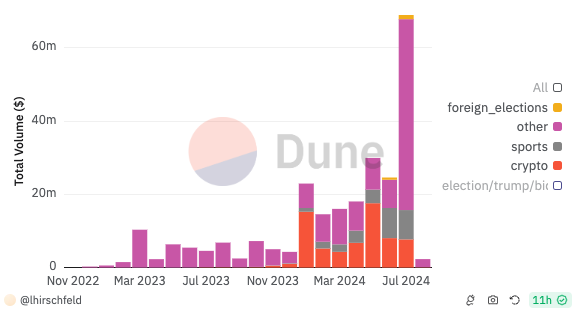

每个人都在问美国大选后交易量能否持续,到目前为止,Polymarket 上的非选举交易量自今年年初以来一直保持稳定。