In-Depth Research Report on Prediction Markets: The Liquidity Paradigm, Industry Leap, and the New Primitives Revolution

I. Historical Evolution & Industry Landscape of Prediction Markets

Prediction markets are mechanisms for pricing future events and have evolved from academic experiments and gray betting exchanges to independently recognized asset-class markets combining informational value, liquidity scale, and financial attributes in the past more than three decades. Their core structure is “price as probability" — using real money to reflect the aggregate judgment of market participants about the likelihood of a given event. A binary contract settled by 1 U.S. dollar or 0 U.S. dollar, traded between 0 and 1 U.S. dollar, directly reflects the market consensus. For example, a contract priced at 0.62 U.S. dollar implies the market estimates roughly a 62% chance the event will occur. Such markets — which aggregate the views of decentralized participants using real money — effectively create a quantifiable, verifiable, and real-time public information good. Unlike purely recreational gambling or house-structured binary options, they serve as hybrid information financial infrastructure, combining market efficiency, collective intelligence, and dynamic trading capabilities. Rather than a zero-sum gambling game, prediction markets generate “positive-sum information output”: Platforms typically collect only small fees while the core value comes from the aggregated probability signal produced by the market. That signal can be referenced by media, used by research institutions, leveraged by enterprises for risk management, or directly embedded in other financial derivatives or Web3 protocols as pricing nodes, giving it strong externalities and societal value.

The roots of modern prediction markets trace back to the Iowa Electronic Markets (IEM), launched in 1988 at the University of Iowa. This was an early experiment led by academic institutions, allowing participants to trade small-stake contracts that represented a candidate’s winning probability or vote-share, with a clear aim to enhance the accuracy of prediction. Numerous studies show that between 1988 and 2004, the Iowa Electronic Markets (IEM) outperformed most conventional polls in predicting U.S. presidential elections, with its probability signals often showing real trends earlier.

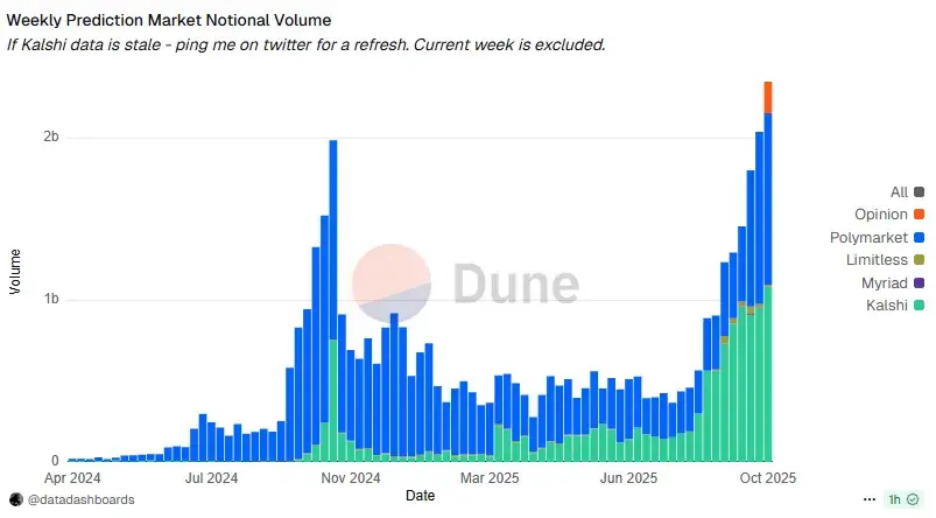

The real industrial-scale leap for prediction markets was driven by a new generation of platforms emerging under the maturity of Layer-2, stablecoins, and cross-chain infrastructure after 2020, epitomized by the “duopoly structure” formed by Polymarket and Kalshi in 2024–2025. Polymarket marks the full maturity of the decentralized route: Built on Polygon and multi-chain expansions, it adopts an order-book (CLOB) model, enables low-friction deposits, gas-free trades, and uses UMA-style optimistic oracles to deliver a user experience that is both seamless and censorship-resistant. During the 2024 U.S. Presidential Election, its monthly trading volume reportedly reached as high as $2.6 billion, and yearly aggregate trades surpassed tens of billions of dollars. Its viral impact across media and social-network channels created a flywheel featuring “opinion → position → dissemination”, making Polymarket the go-to platform for Web3 users entering prediction markets. Even after regulatory pressure from the CFTC, Polymarket repositioned itself for the U.S. market by acquiring the licensed exchange QCEX, further underscoring that compliance has become a core direction for the sector. In parallel, Kalshi represents a completely different path: a compliance-first approach, regulatory certainty, and deep penetration into mainstream finance channels. In 2021, Kalshi was designated as a Designated Contract Market (DCM) by the Commodity Futures Trading Commission (CFTC), and subsequently secured a Derivatives Clearing Organization (DCO) license, thus becoming an event-contract exchange fully compliant under U.S. federal regulation. Its centralized matching structure resembles that of traditional exchanges: It supports USD and USDC deposits and offers event contracts directly on mainstream investor interfaces through partnerships with brokers like Robinhood. After the 2025 surge in sports and macroeconomic event contracts, Kalshi’s weekly trading volume reportedly climbed to $800-900 million, with market share reaching 55–60%, cementing its role as the de facto domestic infrastructure for U.S. prediction markets. Unlike Polymarket's on-chain openness, Kalshi's strength lies in compliance certainty, which attracts institutional participation, builds brand trust, and enables distribution via traditional channels. However, Polymarket and Kalshi together form an orthogonal dual core of "on-chain composability‘’ and ”compliant usability”.

Beyond the duopoly, a wave of new platforms and vertical-market experiments has rapidly emerged, further expanding the market boundaries. For instance, leveraging BSC-ecosystem traffic and airdrop incentives, Opinion reportedly reached hundreds of millions of dollars in volume within its first week of launch; Limitless (on Base chain) uses short-cycle price-prediction markets to meet the demand of crypto traders for volatility exposure; in the Solana ecosystem, PMX Trade tokenizes Yes/No contracts, exploring a deep integration between prediction markets and DEX liquidity. Vertical-specific platforms with sports-oriented networks like SX Network, BetDEX and Frontrunner, have become major niches thanks to high frequency and high user stickiness; and “creator-economy prediction markets” represetned by Kash, Melee and XO Market are turning influencers’ opinions directly into tradeable assets. Meanwhile, TG bots and aggregation tools represented by Flipr, Polycule, and okbet are emerging as another fast-growing frontier. They compress complex prediction-market interactions into chat interfaces and provide cross-platform price tracking, arbitrage, and fund-flow monitoring, forming a “1inch + Meme-Bot”–style new ecosystem for prediction.

Overall, over thirty years of evolution, prediction markets have completed three major leaps: from academic experiments to commercial betting exchanges, and from on-chain experiments to a dual-core structure combining regulatory compliance and scale, and ultimately to a richly diversified ecosystem across vertical scenarios such as sports, crypto markets, creator economy. The window of opportunity for general-purpose platforms is narrowing, while the real incremental growth is more likely to come from deep verticalization, data & tooling layers around the ecosystem, and the extent to which prediction-market signals integrate with other financial systems. In short, prediction markets are rapidly moving from a “gray toy market” toward becoming “key infrastructure for global information and finance systems".

II. Structural Challenges Facing Prediction Markets

After more than three decades of iterations, prediction markets have evolved from experimental products into financial-grade infrastructure gradually adopted by global users and institutions. Yet their development to date still confronts three structural bottlenecks that cannot be bypassed: regulation, liquidity, and oracle governance. These three factors are not independent; instead, they interact with, and constrain each other. Together they determine whether prediction markets can evolve from “gray innovation” into a “compliant, transparent global information and derivatives system". Regulatory uncertainty limits institutional capital entry; insufficient liquidity undermines the validity of probability signals; and if oracle governance cannot provide reliable and credible resolution mechanisms, the entire system risks descending into manipulation and disputed outcomes, failing to become a trusted external source of information.

Regulation represents the foremost bottleneck — particularly pronounced in the United States. Prediction markets may be classified variously as commodity derivatives, gambling, or security-style investment contracts. Each classification triggers a distinct regulatory pathway. If deemed commodities/derivatives, such platforms fall under the supervision of the CFTC and must obtain DCM (Designated Contract Market) and DCO (Derivatives Clearing Organization) licenses — a high-bar, costly process, but passing this regulatory hurdle affords them legitimate federal status, as exemplified by Kalshi. If treated as gambling, platforms must secure licenses in each of the 50 states, raising compliance costs exponentially and effectively blocking the possibility of becoming a nationwide platform. If regarded as securities, they trigger stringent regulation by the securities regulator, posing severe legal risks for DeFi prediction protocols that integrate token designs or yield promises. The fragmented and overlapping regulatory framework in the U.S. leaves prediction markets trapped in a recurring gray area of debate. For example, the litigation between Kalshi and the the New York State Gaming Commission hinges on whether CFTC has exclusive regulatory authority over event contracts. The ruling decides whether Kalshi can operate smoothly across U.S. and the regulation path for U.S. prediction markets over the next decade. Moreover, the enforcement against Polymarket and the classification of event-contracts on Crypto.com’s sports markets by CFTC demonstrate that regardless of whether a platform’s front end appears decentralized, as long as it offers access to U.S. users and facilitates trades, it will be considered unregistered derivatives or binary-options activity, and be subject to legal liability under U.S. regulations.

Outside the U.S., most jurisdictions continue to apply a “binary framework” where prediction markets are either regulated under gambling laws or under financial derivatives legislation. But very few have enacted laws specifically tailored to prediction markets. In countries such as the U.K. and France, online event betting may be permitted under gambling regulation, but regulatory tools such as geo-blocking, payment restrictions and ISP filtering make it difficult for unauthorized platforms to reach mainstream users. For entrepreneurs, claiming “technical neutrality” no longer suffices to evade regulation. Besides, offshore companies, DAOs, or decentralized front ends cannot guarantee immunity from regulatory oversight either. Consequently, the long-term survival strategies are limited: either (1) secure licensing like Kalshi; or (2) remain entirely offshore, fully open-source, decentralized and accept the tradeoff of being excluded from mainstream markets; or (3) pivot to providing techinical services such as KYC, risk control, prediction-data APIs to licensed institutions. The prevailing regulatory uncertainty constrains institutional capital inflows, limits connections with traditional finance, and impedes the true scaling of prediction markets globally.

III. Value Innovation and Future Opportunities of Prediction Markets

After multiple rounds of reshuffling under the constraints of regulation, liquidity, and oracle governance, the truly valuable innovation in prediction markets is now shifting from “competition among individual platforms” toward the “primitive layer” and the “infrastructure layer". In simple terms, over the past decade, the industry focused on “building new prediction-market websites”. However, over the next decade, incremental value is likely to come from “abstracting event contracts into informational derivatives, and embedding them into the broader DeFi and financial system", turning prediction markets from a standalone application into modular, composable “DeFi-Lego blocks". The binary event contracts are only the beginning. Once such contracts become standardized, composable, and collateralizable asset units, an entire layer of derivatives, including perpetuals, options, indices, structured products, lending and leverage, can naturally emerge around the prediciton markets. The “event-markets” explored by D8X, Aura and even parts of dYdX v4 essentially project “whether an event occurs” into a 0–1 price space, and allow high-leverage trading, enabling traders to not only bet on event direction, but also trade volatility and sentiment. Gondor-style protocols go further. By allowing users to collateralize YES/NO shares from Polymarket to borrow stablecoins, they transform previously static long-term event positions into reusable collateral assets; the protocols then dynamically adjust LTV and liquidation logic based on market probabilities, thereby financializing “opinions” into reusable capital instruments. On top of that, index or structured-product mechanisms like PolyIndex bundle a basket of events into an ERC-20 index token. Users can thereby obtain a comprehensive exposure to a themed set of events with one click such as a “U.S. Macro-Policy Uncertainty Index” or a “Basket of AI Regulation and Subsidy Implementation Events". In an asset-management context, prediction markets thus evolve from isolated individual markets into a new asset class that can be incorporated into portfolios.

From a medium-to-long-term value perspective, the most promising “pickaxe-style opportunities” concentrate across four layers: 1) Truth & Rule Layer — Oracles and Arbitration Protocols. How to avoid a recurrence of controversies like those of UMA in terms of economic incentives and governance structure, and how to provide standardized, modular tools that allow common users to create “event markets with clear rules and arbitrable outcomes”, will directly determine the extent to which prediction markets earn acceptance and trust from institutions and public-sector entities. 2) Liquidity & Capital-Efficiency Layer: Custom AMMs for prediction markets, unified liquidity pools, collateralized lending and yield-aggregation protocols could turn dormant event positions into reusable collateral assets, bringing a new asset into DeFi and offering platforms stronger economic moats. 3) Distribution & Interaction Layer: Future paths such as social-embedded SDKs/APIs, media-plug-in components, professional terminals and strategy tools determine the “on-ramp form” for prediction markets, and decide who could capture continuous fees and technology-service revenues at the intersection of information flow and trading flow. 4) Compliance Tech & Security Layer: Fine-grained geo-fencing, KYC/AML, risk-monitoring and multi-jurisdiction automated reporting could enable licensed institutions to safely integrate prediction-market data within regulatory boundaries, so that event prices can genuinely feed into asset management, investment research and risk-management workflows. Finally, the rise of AI may provide a new feedback loop binding prediction markets with capital markets. On one hand, AI models could act as “super traders", using superior information processing and pattern recognition to trade on prediction markets, thereby improving market pricing efficiency. On the other hand, prediction markets can serve as a “real-world scoring ground” for AI capabilities. By evaluating AI performance in terms of actual P&L and long-term calibration accuracy, they can provide external, hard-constraint metrics for “AI research reports, AI advisory services and AI strategies". For investors, projects that understand the design of derivatives, can safely operate within regulatory boundaries, and successfully bridge AI with traditional finance are likely to become key infrastructure assets for the next cycle of the “informational derivatives” sector.

IV. Conclusion

From betting pools of pope elections in the 16th century, to president-predicting bets on the Wall Street in the 20th century, to early academic experiments like Iowa Electronic Markets (IEM), betting exchanges like Betfair, and now to modern platforms such as Polymarket and Kalshi — the evolution of prediction markets is, in essence, a human attempt to approximate “true probabilities” more closely via institutions and incentives. Today, as the trustworthiness of mainstream media declines and social-platform signals become more noisy, prediction markets concretize the “cost of wrong remarks”: They compress dispersed global information and judgments into a quantifiable, verifiable probability curve. The curve is not a perfect “truth machine”, but it provides a public signal that is more verifiable than slogans or emotions. Looking ahead, the ultimate outcome of prediction markets may not be the emergence of a single platform larger than Polymarket, but rather their evolution into an “information and opinion interaction layer” embedded across social media, news websites, financial terminals, games, and creator tools — as ubiquitous as the “like” button — where every opinion can naturally correspond to a tradable probability. In a world where both humans and AI participate, prediction markets could continuously produce incentivized, constrained “collective forecasts”, feeding back into decision-making and governance. To reach that stage, the sector must first cross three thresholds: regulation, liquidity, and oracle governance. It is those thresholds that serve the stage for next-generation infrastructure and emerging primitives. For entrepreneurs and investors, the prediction market is by no means a “completed market". On the contrary, it has just finished its first phase evolving from a concept to an early industrial prototype. Whether it becomes a “Web3-level information infrastructure” depends on the next 5–10 years of continued innovation and institutional adaptation in rules, liquidity designs, and oracle mechanisms. In this multibillion-dollar information war, winners will often not be those who shout the loudest, but those who quietly build the “pickaxes” and pave the “roads” most solidly.