Author: Zhou Hang

SpaceX may be overvalued by $1.25 trillion around its IPO.

This is not to deny SpaceX's greatness. On the contrary, anyone seriously discussing SpaceX must first acknowledge: it is likely one of the greatest industrial companies of the past 50 years.

But the greatness of a company and whether a stock is worth buying at any price are two completely different things.

SpaceX can simultaneously be "the greatest industrial entity of the 21st century" and also a "severely overvalued investment target." These two things are not mutually exclusive.

■ First, Acknowledge Its True Greatness

Any honest discussion about SpaceX's valuation must start with this statement: It is the most successful industrial company of the past 25 years, bar none—even more successful than Tesla. This is not mere praise; it is a fact of engineering economics.

Tesla disrupted a 150-year-old mature industry—automobiles. Its rivals are Mercedes-Benz, Ford, Toyota. These opponents are certainly not weak, but they are commercial companies, not backed by national interests, lacking political barriers; competition is essentially about product, brand, supply chain.

SpaceX disrupted a 60-year-old state-monopolized industry—space. Its rivals are NASA, Roscosmos, ESA, CNSA. This is an entirely different level of difficulty: higher engineering barriers, greater capital density, more complex regulation, deeper entanglement with national interests. When Musk founded SpaceX in 2002, the entire space industry was essentially an extension of national missions; commercial companies were not believed capable of building rockets, let alone rockets cheaper than national ones.

Over 20 years later, SpaceX slashed launch costs from $54,500/kg in the Space Shuttle era to $1,500/kg—a 36-fold reduction. It now launches 165 times a year, one company exceeding the total launch count of all other nations and all commercial players combined. It built humanity's first truly reusable rocket, a single Falcon 9 first stage flying 32 times, with a success rate exceeding 99%. It established the world's first global satellite internet—covering over a billion users, becoming a decisive strategic asset on the first day of the Ukraine war.

Tesla in 2025 still faces fierce competition from Chinese EVs; SpaceX's share in the global commercial launch market, is nearing monopoly.

SpaceX is a great company, perhaps the greatest industrial company on Earth in the past 50 years. Any critique of its valuation must first acknowledge this fact.

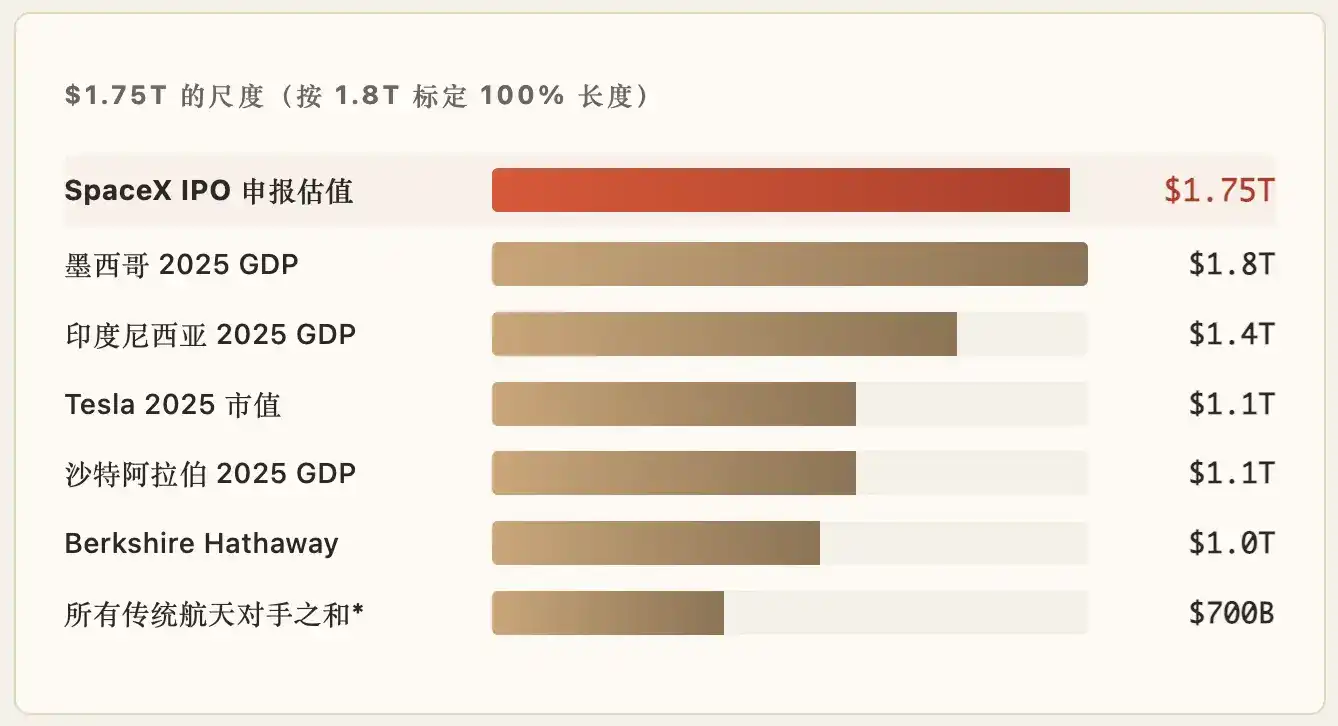

■ What Does $1.75 Trillion Mean?

Let's understand through a set of comparisons:

* Combined market cap of Boeing + Lockheed + Northrop + RTX + GD. SpaceX alone is valued at 2.5 times the sum of these 5.

In other words, the valuation of SpaceX alone will exceed Mexico's annual GDP, exceed either Tesla or Berkshire, and is 2.5 times the total market cap of all traditional space rivals.

This itself is not the issue—great companies deserve great valuations. But the 2.5x ratio means the market is not pricing it as a "space company," nor as an "industrial company." The market is pricing it using a hybrid paradigm closer to "sovereign asset + AI-era infrastructure + narrative premium."

Is this pricing reasonable?

List SpaceX's current businesses and seriously calculate how much revenue it can generate by 2030, assuming a reasonably optimistic scenario for each line:

If SpaceX achieves revenue of $50-80B in 2030, corresponding EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization, roughly understood as the operating cash profitability of the company's main business) would be approximately $20-35B (assuming a 40% margin, already a very optimistic estimate).

Using the standard SaaS/diversified EV/EBITDA multiple of 25-35x—which is already a premium valuation for tech companies—SpaceX's "reasonable valuation" range in 2030 is between $500B and $1.2T.

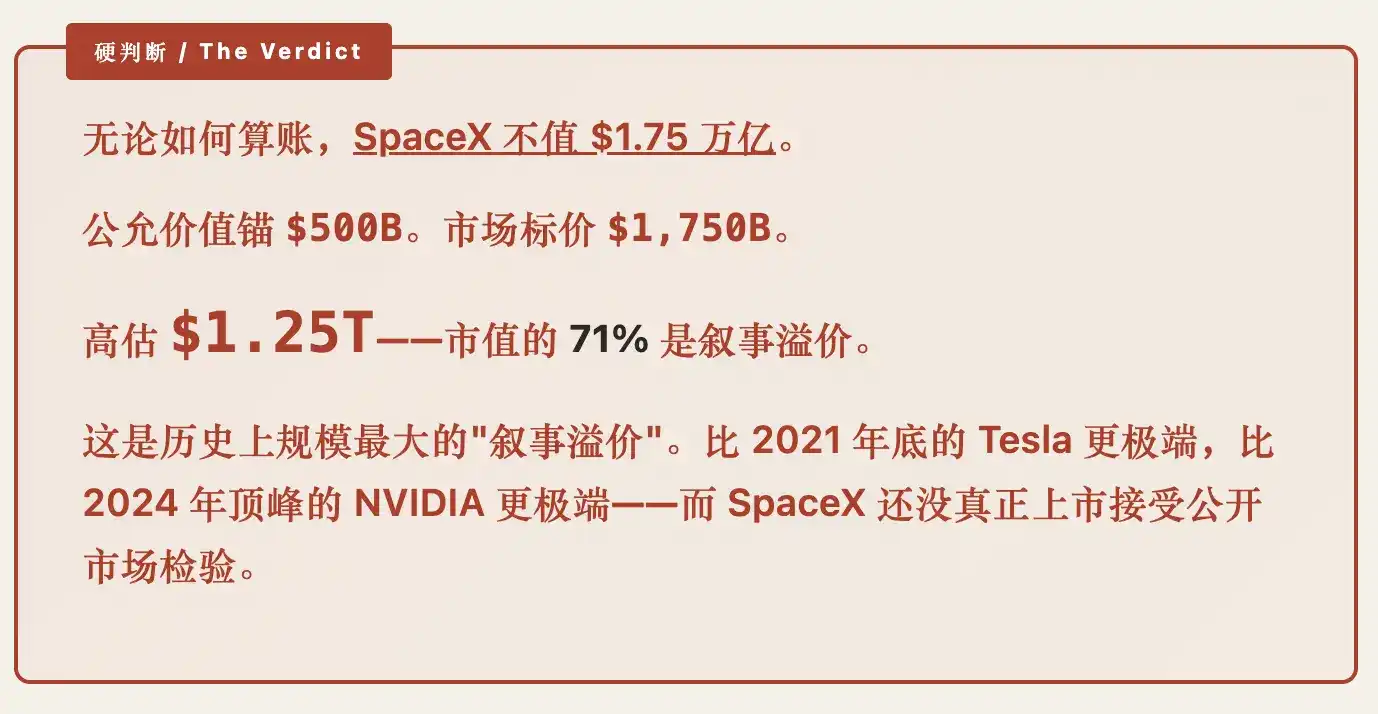

Take the conservative anchor point of $500B (i.e., valuing all 2030 businesses reasonably, not wildly) versus the market price of $1.75T.

Difference: $1.25T.

This difference cannot be explained by any standard financial model. It is not the result of DCF (Discounted Cash Flow), not derived from P/S multiples, nor from comparable company analysis—none of these methods yield $1.75T.

This difference does not appear out of thin air. It has three real sources:

First Source: Long-Term Vision Premium. If Starship operates stably in 2027-2030, launch costs could drop to $200/kg or lower. Capacity increases 30-fold—enough to support new businesses (in-orbit data centers, lunar commerce, deep-space robotics). Anthropic has publicly expressed interest in "being willing to pay for GW-scale space computing." If this narrative materializes, SpaceX plus new businesses could address a total market of $200-500B/year by 2040. This upper limit is indeed massive—so it's rational for the market to leave room for "vision premium."

Second Source: Sovereign Asset + Strategic Position Premium. SpaceX is no longer just a commercial company; it is a U.S. national strategic asset. $22B in government contracts, HLS lunar lander, NRO reconnaissance constellation, Golden Dome missile tracking—these integrate SpaceX into the U.S. national security system. With international communication order fracturing (China bloc / U.S. bloc / third parties), Starlink automatically gains "soft sovereignty" in all markets it can serve. The monetization of this status may take 10+ years to fully manifest, but the premium is real.

Third Source: Retail Investors' Desire for Heroic Narratives + Musk Personal Cult. This is the hardest to quantify, but anyone familiar with capital markets knows its power. Musk has 200 million followers on platform X; his persona is a valuation variable. SpaceX's story—a private company sending humans to Mars, building a global internet, making humanity multi-planetary—is the most heroic commercial story of the past 50 years.

Retail investors are not buying EBITDA; they are buying a ticket to participate in history.

The first two premiums are "real, but slow"; the third premium is "large, but fragile." The current $1.75T valuation bets that all three will hold true and encounter no problems. This is a difficult combination to sustain.

What Happens After IPO?

Assuming SpaceX completes its IPO in the second half of 2026, the next 3-5 years will likely look like this:

Scenario A: Valuation Solidifies (Probability ~25%). Starship V3 successfully launches in 2027, enters stable operation in 2028, the first GW-scale space computing contract lands in 2028. Lunar commerce progresses per NASA schedule. While Starlink growth slows, the Aviation + Maritime + D2C segments offset residential market deceleration. In this scenario, $1.75T "starts to look cheap"—the market would revalue it to $2-3T.

Scenario B: Flat Volatile Valuation (Probability ~50%). Starship materializes slower than expected—5/25 = 20% flight test success in 2025. If this realization rate continues in 2026-2027, V3 may not mature until 2029-2030. Starlink growth slows to +20%/year, the xAI-Anthropic agreement brings real cash flow but no major follow-up contracts. The market realizes "narrative is ahead of reality," and valuation oscillates between $1.2T - $1.8T for 3-5 years. This is the most probable scenario.

Scenario C: Valuation Reckoning (Probability ~25%). Persistent Starship delays, xAI falling significantly behind in AI competition, a Musk personal risk event (health, reputation, politics) triggers. Sentiment premium rapidly contracts. The market reprices using financial models—valuation falls back to the $800B-$1.2T range, equivalent to "the reasonable valuation an excellent industrial company deserves." This scenario is actually good for long-term holders—but means a 30-50% paper loss for retail investors who buy post-IPO.

Probability-weighted = 0.25 × Upside + 0.50 × Flat + 0.25 × Downside ≈ Expected Value $1.3-1.5T, lower than the IPO filing price of $1.75T.

Weighting the three probabilities, the expected central range for SpaceX's valuation over the next 3-5 years is approximately $1.3-1.5T—lower than the current IPO filing price.

In plain language: buying at $1.75T on IPO day yields negative expected returns over 5 years. This is the inevitable conclusion after weighting the three scenarios by probability: you get no return in the highest-probability scenario; you lose 30-50% in the worst scenario; only in 1/4 of cases do you make money.

As Charlie Munger would say: this is not a bet with favorable odds.

■ To Those Planning to Buy on IPO Day

SpaceX is a great company, but a great company does not equal a stock you should buy at any price. These are two different things.

Tesla at the end of 2021 was also considered by many as "should buy at any price"—its market cap was $1.2T then. Over the next two years, Tesla fell 70%, from $1.2T to $400B. Not because Tesla became a bad company—it remains an excellent EV company. It's because price got too far ahead of fundamentals.

SpaceX's current situation is highly similar to Tesla's at the end of 2021—possibly more dangerous, because SpaceX's "vision premium" is a larger component, the story is grander, and retail participation may be deeper.

If you truly believe in SpaceX's long-term vision and are willing to hold for over 10 years without selling, then buying at the IPO price may be fine—the company will likely be worth more in 10 years. But if you expect to "double your money in 1-3 years after buying," the math is not on your side.

A more rational strategy is:

- Do not chase the high on IPO day.

Premium is typically highest on the first day of any mega IPO. - Wait for at least one of three things to happen.

Starship V3 stable operation, the first GW-scale space computing contract, or the stock price falling below $1T. - If you must buy now, limit your position.

Don't treat it as a "sure bet"—it is not. It is a "meaningful long-term +/- 30% uncertainty."

■ A Great Company Can Also Be an Expensive Stock

A company's greatness is fact; whether a stock's price is reasonable is math. Facts don't change, math changes daily. In SpaceX's current valuation structure, financial models can only explain half; the other half is market sentiment + sovereign status + personal cult—this part is not non-existent, but it is fragile.

After IPO, one thing will happen: retail investors start measuring the company with quarterly earnings. The first quarterly report, the second, the third—each will force the market to reconcile "story" with "reality." This reconciliation process is typically unfriendly to short-term valuation.

If you're buying the company—the great industrial entity, the post-Starship human infrastructure, the sovereign asset—then the IPO price is just a point in a 20-year marathon, no need to obsess.

If you're buying the story—participating in history, following a hero, contributing to us becoming a multi-planetary species—then admit this is consumption, not investment. Consumption can be expensive, but you need to know what you're doing.

The company can be world-class, the stock can simultaneously be overvalued by $1.25 trillion. Both are facts, but they must be viewed separately. Distinguish whether you're buying the company, or the story.