On December 15th, the domestic futures market witnessed a remarkable rally. The main platinum futures contract listed on the Guangzhou Futures Exchange surged robustly during the trading session, firmly hitting the limit-up in the afternoon with an intraday gain of 7%, closing at 482.4 yuan per gram.

Notably, this marks the first limit-up since the listing of this contract, with trading volume also surging to 41,800 lots on the same day, indicating strong participation and enthusiasm from market funds.

In a similar vein, the main palladium futures contract, also a platinum group metal, showed strong performance, with intraday gains once exceeding 5%, closing up 4.73% at 407.6 yuan per gram. This synchronized surge signals that platinum and palladium, these relatively "low-profile" precious metals, are officially capturing the attention of more investors. Shifting the focus to the global market, platinum's strong momentum had already been evident.

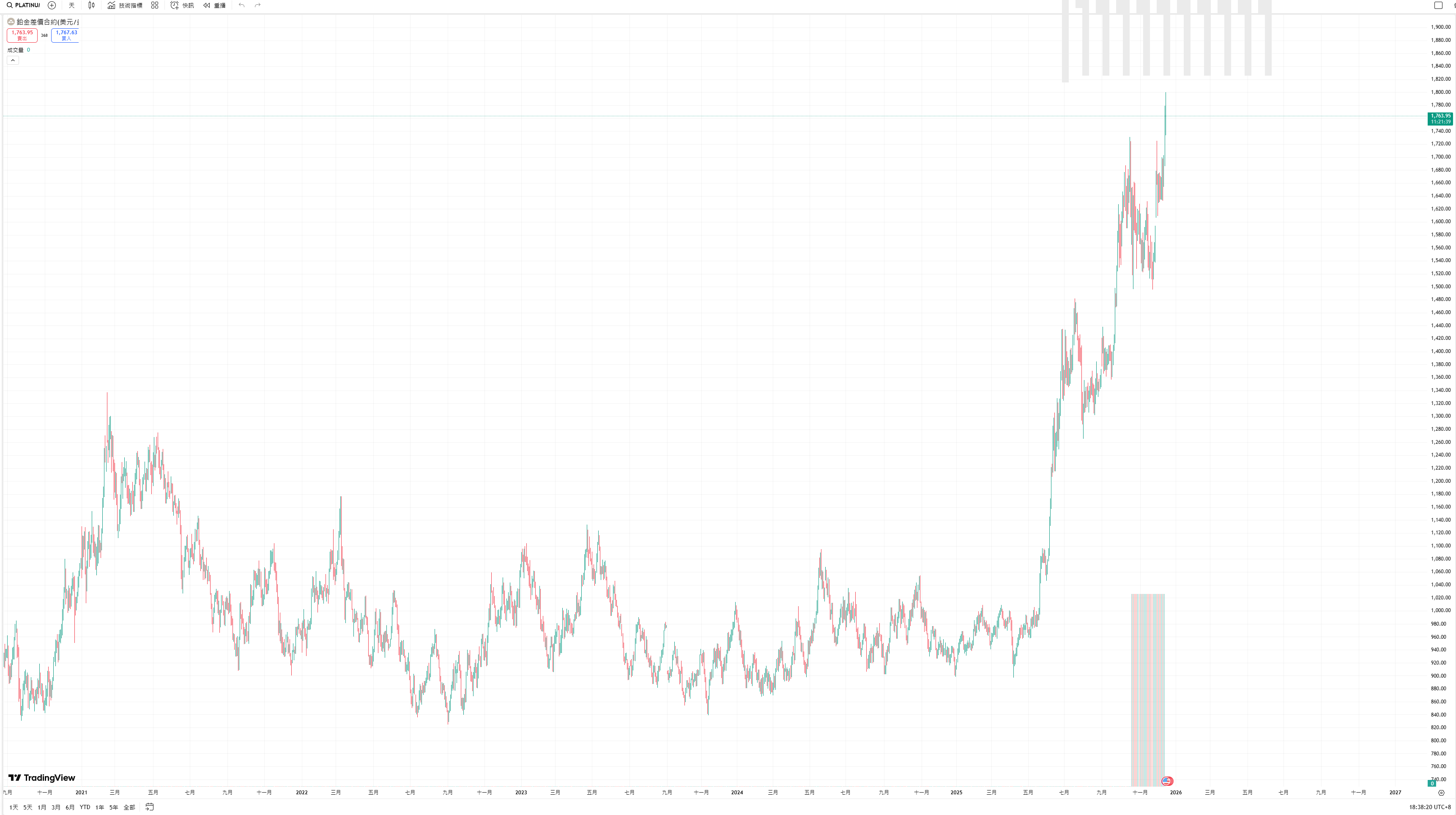

Since the beginning of this year, international platinum prices have soared, with a cumulative increase reaching a staggering 93%, completely breaking the multi-year downtrend and becoming one of the most dazzling performers among commodities this year. This interconnected rise, both domestically and internationally, is not an isolated event; it is driven by profound and lasting changes in fundamental supply and demand dynamics.

II. Analysis of the Rally Drivers: Structural Shortage and New Demand Narratives

Market analysis generally agrees that the core driver of this platinum and palladium rally stems from long-accumulated supply-demand contradictions, rather than short-term speculative sentiment. Muhammad Umair, a financial analyst at FXEmpire, pointed out that the main forces pushing platinum prices higher come from the dual squeeze of growing industrial demand and an increasingly tight supply structure.

From the supply side, a long-term contraction trend is significant.

Global platinum supply has been in a tight state for several consecutive years. According to data from the World Platinum Investment Council (WPIC), global total platinum supply in 2024 is forecast at 227.4 tons, showing a noticeable decline from 258.4 tons in 2021 and remaining at the lower end of the historical supply range.

Platinum supply primarily consists of mine production (over 75%) and recycling.

Currently, the South African mines, which account for over 70% of global production, continue to be plagued by multiple challenges including unstable power supply, aging mine infrastructure, and rising operational costs, severely constraining output from the mining side. Simultaneously, a long-term lack of capital expenditure has created bottlenecks for mine capacity expansion.

Analysis from Xinhu Futures indicates that the platinum market has been in a physical deficit for many consecutive years, and this structural supply gap is the fundamental reason supporting the steady upward shift in its price center. The supply situation for palladium is equally concerning. Although global total palladium supply in 2024 is expected to increase slightly by 3.6% year-on-year to 292.84 tons, inventory levels have fallen to multi-year lows, leaving the market with extremely weak buffering capacity.

More importantly, Russia supplies over 40% of the world's mined palladium, and any potential risks in geopolitics or trade could impact the already fragile supply chain, exacerbating market volatility.

From the demand side, traditional support remains solid, and new bright spots are emerging.

While supply remains constrained, the demand side demonstrates strong resilience and new growth potential.

WPIC data shows that global total platinum demand in 2024 is forecast at 258.25 tons, far exceeding the同期 supply, clearly indicating a supply-demand deficit.

The automotive sector remains the largest source of platinum demand currently, accounting for about 37.4% in 2024, primarily used in manufacturing catalytic converters for vehicle exhaust. Although the global auto industry is transitioning towards electrification, demand for platinum from traditional internal combustion engine vehicles, particularly some diesel vehicles facing stricter emission standards, remains stable. Furthermore, due to price factors, the ongoing substitution of platinum for palladium in some catalytic applications provides additional support for platinum demand. Industrial demand is another stable pillar, accounting for about 30%, widely used in high-end manufacturing sectors such as chemicals, glass, electronics, and medical applications.

However, what most excites the market is the vast potential brought by the hydrogen energy industry. Platinum is an indispensable catalyst material in Proton Exchange Membrane Fuel Cells (PEMFC) and is also a crucial electrode material in electrolyzers for water splitting (a key technology for green hydrogen production). As countries worldwide actively advance the energy transition, the rapid development of the hydrogen energy industry chain is expected to open a long-term and potentially huge new growth avenue for platinum demand. Cong Shanshan, an analyst at Huishang Futures, pointed out that hydrogen energy is becoming a new core growth driver for platinum demand.

Additionally, the recovery in investment demand should not be overlooked. Against a backdrop of increased global macroeconomic uncertainty and expectations for a potential shift in monetary policy by major central banks, platinum, which possesses both precious metal financial attributes and strong industrial properties, has attracted inflows from funds seeking diversification and safe-haven assets. The sustained increase in holdings of palladium ETFs this year also reflects warming investment sentiment.

III. Market Outlook: Value Reassessment Coexists with Potential Risks

Regarding the future market, while specific price point predictions vary among analysis institutions, the view of a bullish medium-to-long-term trend predominates.

Muhammad Umair holds a relatively aggressive view, believing the current rally is not over. He forecasts that platinum prices could climb to the range of $2170-$2300 per ounce by 2026. This expectation is significantly higher than the median forecast of $1550-$1670 per ounce for next year by most Wall Street institutions.

Cong Shanshan, an analyst at Huishang Futures, stated that the prospect of a shift in the Federal Reserve's monetary policy expectations (such as interest rate cuts) and the resulting looser liquidity outlook are macro-level positives for precious metal prices including platinum and palladium.

Concurrently, the strength in gold and silver prices also supports platinum and palladium through precious metal sector correlation.

She emphasized that, from a medium-to-long-term perspective, against a backdrop of loose liquidity, if investors continue to view platinum as an alternative investment to gold, its price will receive solid support. Xinhu Futures also believes that the "structural gap in the platinum and palladium markets will persist, driving prices steadily higher". However, market participants also need to be wary of potential risks. Firstly, the overall platinum and palladium markets are much smaller than gold, inherently leading to higher price volatility; rapid short-term gains could accumulate correction pressure. Secondly, high prices may prompt some industrial users to seek alternative materials or process improvements, thereby dampening long-term demand. Finally, the global macroeconomic situation, particularly the industrial activity sentiment in major economies, will continue to directly impact the industrial demand for platinum and palladium.

IV. Conclusion: Precious Metal Opportunities in the New Cycle

In summary, the recent price explosion in platinum and palladium is the result of the combined effect of a long-term reversal in fundamental supply and demand, empowerment from new application scenarios, and changes in the macro-financial environment. South Africa's supply woes, geopolitical risks associated with Russia, and the grand narrative of the hydrogen economy together form a solid foundation for this value reassessment.

The listing of domestic platinum and palladium futures provides investors with more convenient participation tools, expected to further enhance market attention and liquidity for these two metals. In a broader asset allocation perspective, it's not just niche precious metals like platinum and palladium that are shining; the entire commodities market is showing signs of活跃 (activity).

From energy to metals, prices of various basic assets are rotating, seemingly heralding a new cycle of volatility and opportunity. As traditionally defined commodities纷纷启动 (start rallying across the board), Bitcoin, representing the innovation of value storage in the digital age, is also being increasingly discussed and its属性 (attribute) as "digital gold" is gaining more attention. If commodities are all rallying, can Bitcoin, as digital gold, be far behind?