Author:Wintermute

Compiled by: Deep Tide TechFlow

Deep Tide Guide:This article is written by a Wintermute OTC trader, providing an in-depth analysis of the root causes behind the current outflow of retail capital from the crypto market. Historically, crypto bull markets have often been driven by retail speculation, but the latest data indicates that retail investors are flooding into US stocks at a record pace, causing the crypto market and US stocks to shift from "rising and falling together" to a "seesaw" relationship. As crypto market volatility declines, the barriers to entry and exit lower, and AI grants retail investors an analytical edge in US stocks, cryptocurrency is no longer the preferred choice for retail speculation. Understanding this logic of capital rotation can help us readjust our multi-asset investment framework.

Full Text Below:

Retail activity has always driven the crypto market. Through speculation, reflexive buying-the-dip, and flexible capital rotation among various tokens, retail investors have defined every major cycle in crypto history. But the latest data suggests that the relationship between retail and the crypto market is changing.

For some time, we have been warning that the US stock market is capturing retail attention at the expense of altcoin liquidity. The latest data from J.P. Morgan's strategy desk, combined with our proprietary flow data, further indicates that US stocks and cryptocurrencies are becoming substitutable risk assets.

Correlation Reversal

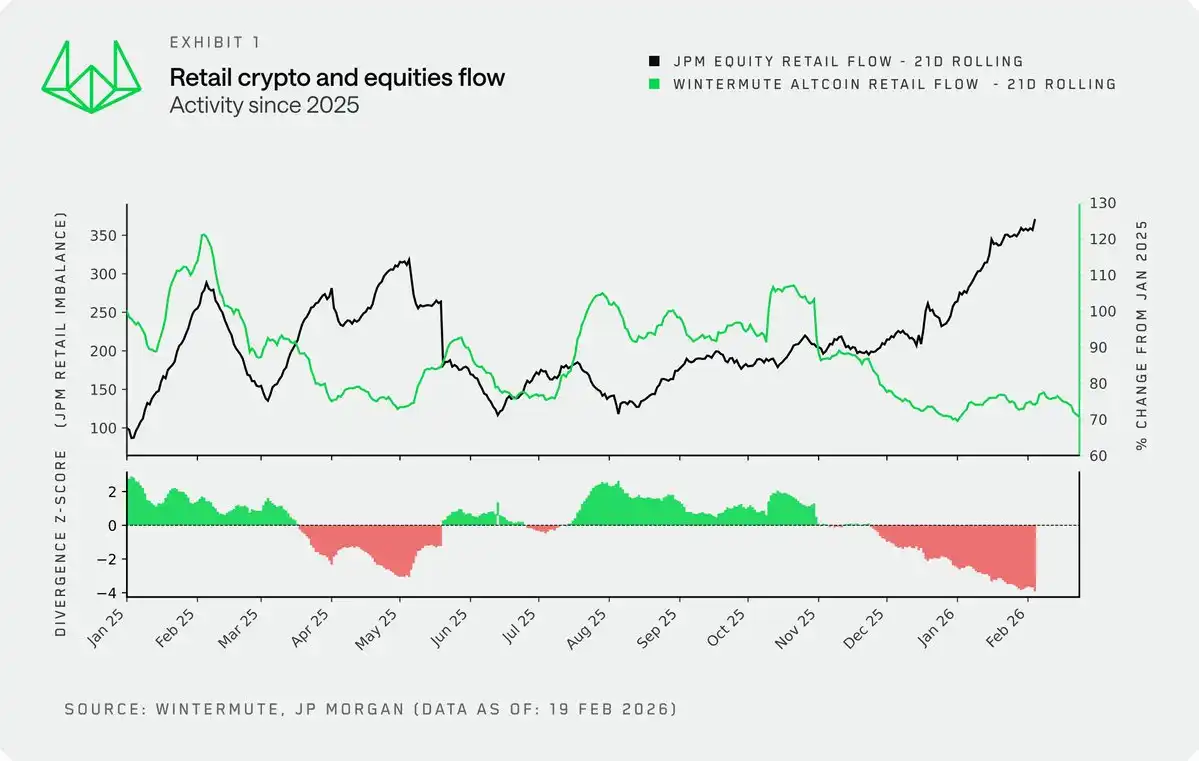

By overlaying Wintermute's proprietary crypto retail flow data with J.P. Morgan's data on retail inflows into US stocks, we gain a new perspective on the relationship between retail activity in US stocks and the crypto market.

Historically, the two have typically moved in sync. Until late 2024, rising risk appetite usually meant buying on both sides, as, to some extent, they were both outlets for excess capital (referencing M2 data) and risk appetite. However, since late 2024, this correlation has broken down. Today we are seeing the most severe divergence in recent history: retail is pouring into US stocks at a record pace while choosing to hold and wait in the crypto market.

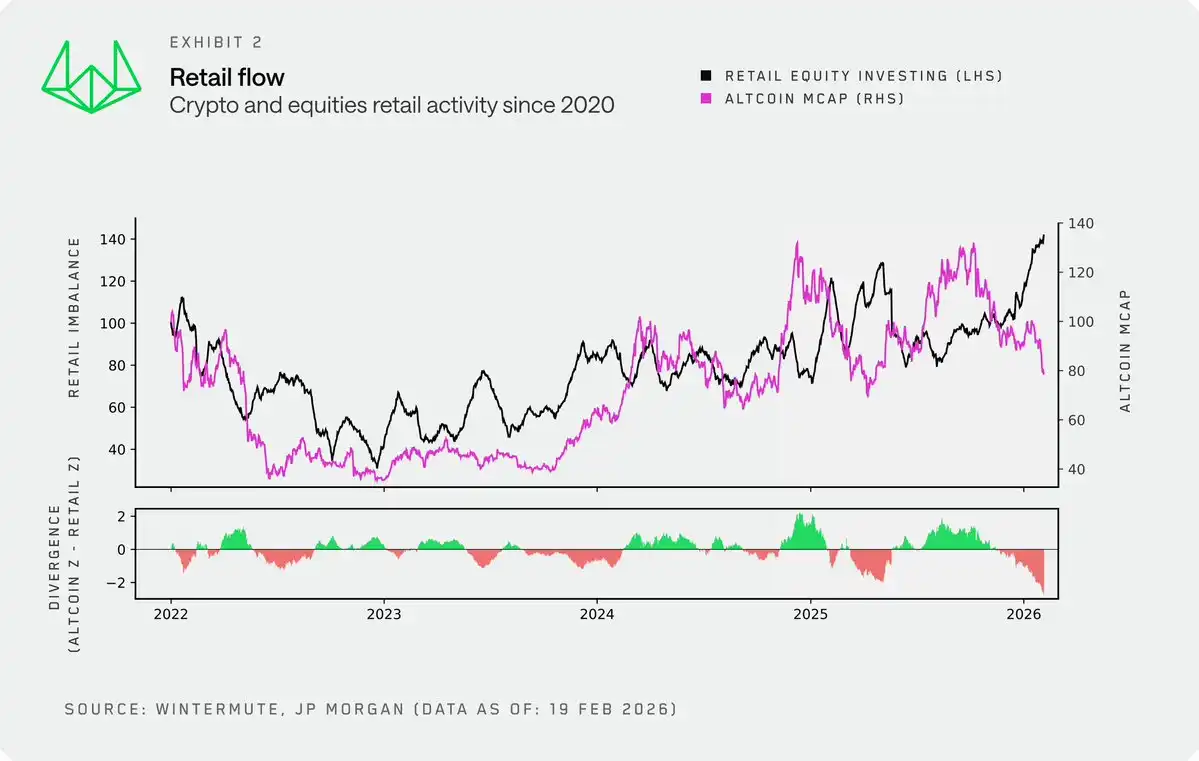

Looking at a longer time frame, we use the total market capitalization of altcoins as a long-term proxy for retail crypto activity. It aligns highly with our retail flow data and has a more objective, longer historical record. From 2022 to late 2024, cryptocurrencies and US stocks largely moved in tandem, with retail viewing both as part of a high-risk portfolio. But this decoupling in late 2024 is particularly pronounced, with retail trading behavior becoming more short-term driven, volatile, and lacking structure.

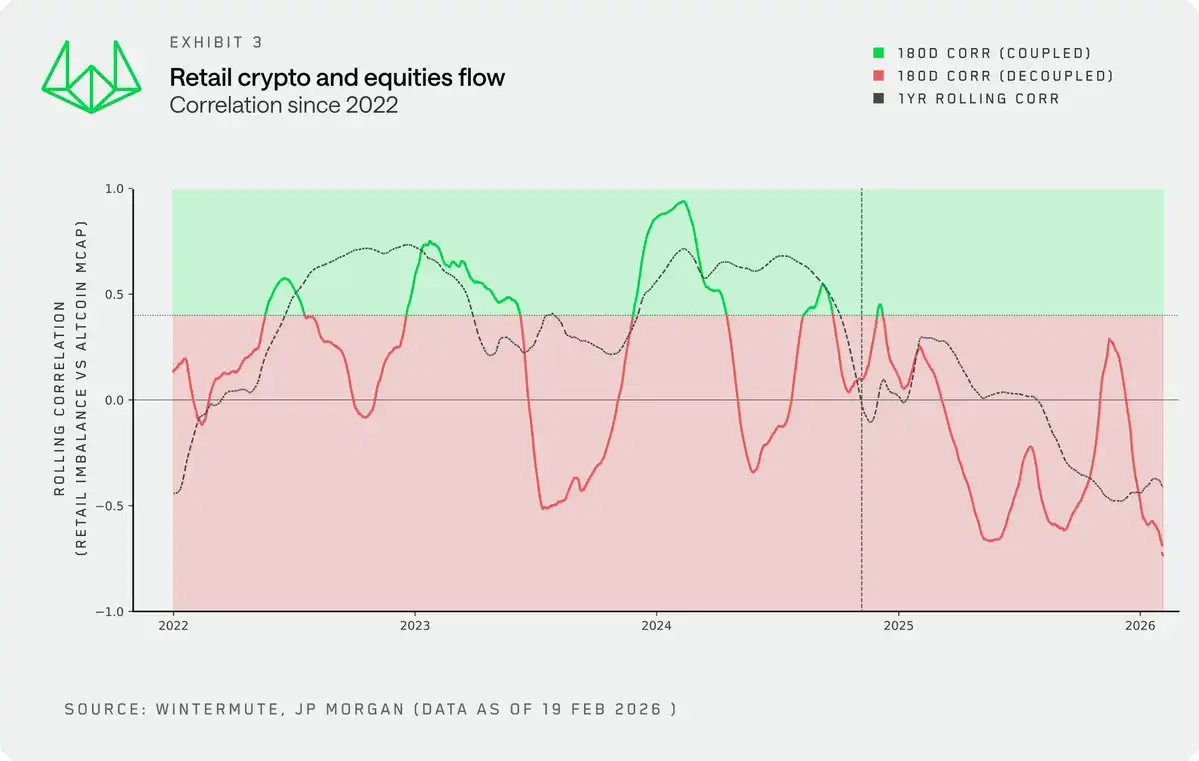

The rolling correlation between retail activity and altcoin market cap confirms this shift. The once volatile but generally positive relationship has now turned negative. Retail is now making an "either-or" capital allocation between these two, rather than buying both simultaneously.

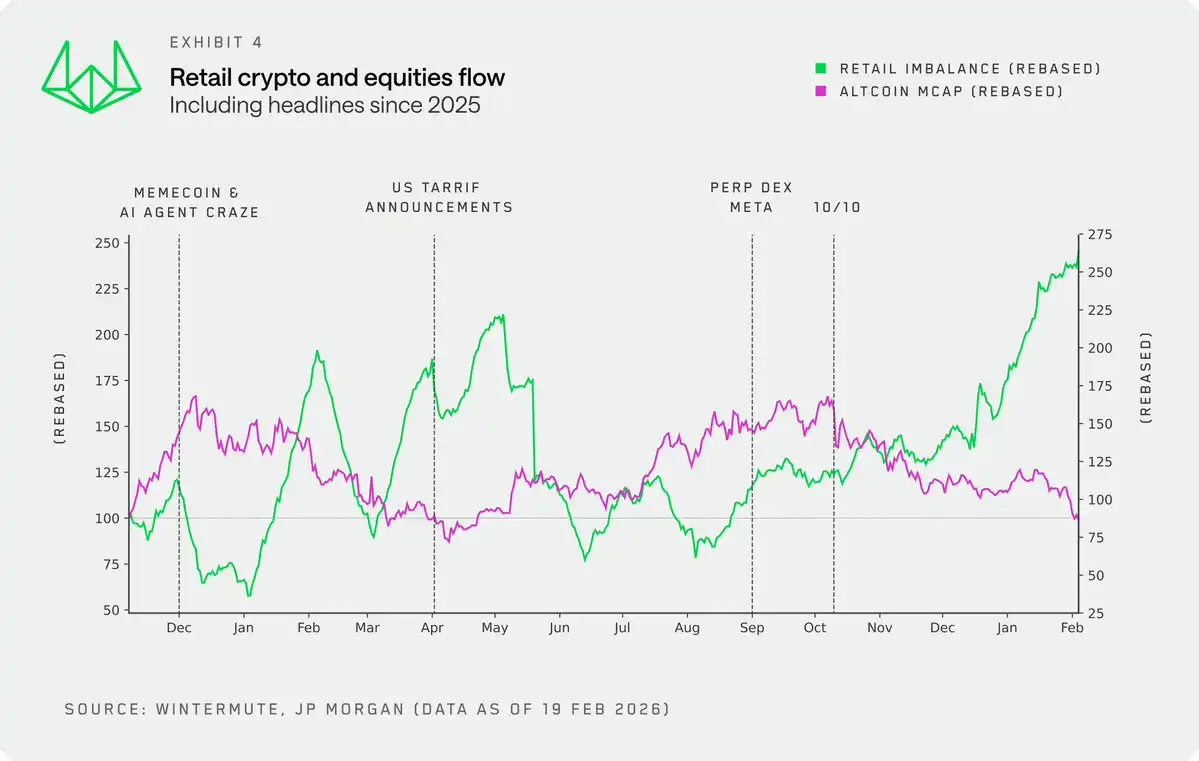

Focusing on 2025, this dynamic becomes clearer when combined with key catalyst events. Several points are very evident:

- When US market activity stalled, Memecoins and AI agents had their moment, as retail shifted speculative demand to these areas.

- Retail continued to aggressively buy the dip in US stocks, both during the tariff policy period announced in April 2025 and more recently.

- After October 10th, capital almost completely shifted to US stocks, and this trend continues to this day.

Causality

One point must be clear: we do not believe the retail cohort in crypto is large enough to pull capital *from* US stocks. Quite the opposite, it is the soaring retail enthusiasm in the US stock market that is draining liquidity *from* the crypto market.

New data also confirms this. US retail activity has become a new variable, and crypto investors should closely monitor this indicator to find windows of opportunity when retail capital can provide sustained buying support for the crypto market.

Volatility is the Product Itself

While there are many reasons, one core reason why retail has been so active in and attracted to the crypto market is the asset's volatility characteristics. Volatility *is* the product itself. This was the core driving force that initially pulled retail into crypto.

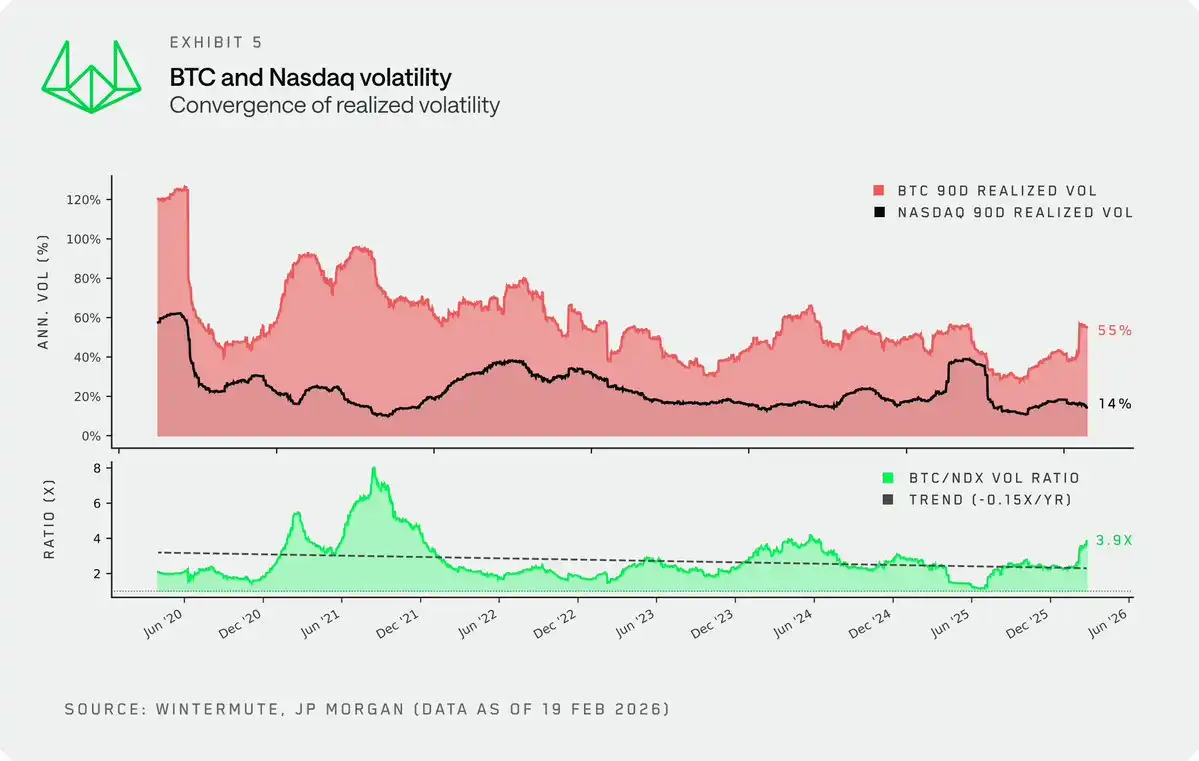

However, although crypto market volatility still far exceeds that of US stocks, its realized volatility has been undergoing structural compression, a trend that is difficult to reverse. The volatility ratio of BTC to the Nasdaq 100 Index (NDX) has been declining, compressed to below two times in the first half of 2025.

Some thoughts on key driving factors:

- Market Maturation. Increasing participation from sophisticated investors, coupled with the emergence of new liquidity tools like ETFs and DATs, suppresses the typical, reflex-driven volatility spikes seen in earlier cycles.

- Market Size. The total crypto market cap now stands at $2.3 trillion. Even with a 40% drawdown from the all-time high (ATH), the amount of capital required to move the market is far greater than it was five years ago.

As volatility compresses, the core selling point that attracted retail to cryptocurrency fades. The dramatic surges and crashes that defined the 21-22 bull cycle and attracted a whole cohort of retail investors are now a thing of the past. For volatility-seeking retail, US stocks are becoming increasingly attractive.

Technology-Driven Factors

Beyond the structural changes in the crypto market itself, technology-driven factors are also accelerating this capital rotation, a point not yet sufficiently discussed in the market.

- Integration of Investment Channels. The integration of crypto trading into fintech and traditional brokerage platforms (or the integration of US stock trading into crypto-native platforms)确实降低了入场门槛,但其更深远的影响体现在「资金撤离」上. In previous cycles, complex deposit and withdrawal processes effectively locked capital inside the crypto ecosystem once it entered, fostering organic rotation among different tokens. Today, equally smooth on/off ramps mean capital can move freely and without friction between cryptocurrencies and US stocks.

- The Edge. Retail seems increasingly drawn to US stocks, partly because they are gaining a new kind of advantage through AI. Large Language Models (LLMs) have significantly enhanced retail analytical capabilities, creating an illusion of a level playing field with institutions.

But this feeling is absent in crypto. While you can also analyze crypto projects based on data, the crypto space lacks a consensus valuation framework and clear token value capture mechanisms, coupled with an ever-expanding universe of investable assets, making it difficult for retail to find that sense of "having an edge" here.

Conclusion

Retail was once the most reliable source of reflexive demand in the crypto market, but now their risk appetite is increasingly being satisfied elsewhere. US stocks offer highly competitive volatility, provide retail with a growing analytical edge, and allow seamless switching between crypto and stocks through the same app on their phones. Cryptocurrency still has a place in retail portfolios, but it is now just one of many gambling tools, no longer the preferred vehicle for speculation.

This shift should also reshape how investors view the market. Some tried-and-true indicators have become ineffective. For crypto investors seeking success, merely looking for leading indicators of risk appetite and combining them with crypto-native frameworks is no longer sufficient. Investors increasingly need to view cryptocurrency through the lens of a multi-asset portfolio, as has long been standard practice in US equity and fixed income markets.