Written by: Eli5DeFi

Compiled by: AididiaoJP, Foresight News

Token launches in 2026 face a brutal reality.

It's not a celebration, nor is it a reward for your hard work building.

It's more like an 'open gladiator arena'—any flaw in your token economic model will be seized upon and publicly exploited by seasoned veterans with better models than yours.

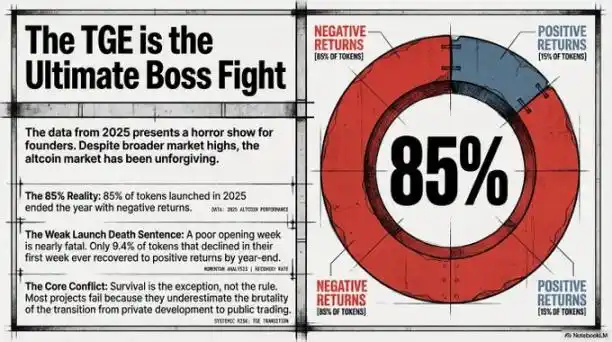

Arrakis Research compiled data from 2025, and the results are unequivocal: 85% of token launch projects ended the year with negative returns.

This can't be blamed on poor market conditions; a bear market doesn't specifically target tokens with poor tokenomics while sparing the well-designed ones.

This number is the market sounding an alarm for founders: most people are heading into a fight but have only prepared for a ribbon-cutting ceremony.

The good news? The surviving 15% aren't just lucky. They are meticulous, and their methods are replicable.

"Poor performance in the first week is basically a death sentence. Data shows that only 9.4% of tokens that fell in their first week managed to recover." — Arrakis Research

This statement is worth pondering.

Summary

- Your token's failure isn't bad luck; it's because you didn't design it to succeed in the first place.

- 85% of tokens launched in 2025 declined over the year. This is a design problem, not a market problem.

- Launching with a Fully Diluted Valuation (FDV) exceeding $1 billion is essentially giving money to people who will never use your product, helping them 'cash out at the top'.

- Staking, governance, and custody are not 'add-on features'; they are the token's immune system. Without them, the token collapses immediately upon launch.

- Only 9.4% of tokens that fell in their first week recovered. The first week's performance essentially determines life or death.

The 'Physical Laws' Behind TGE

Here's a useful mental model, borrowing concepts from physics. Every token launch has two opposing forces:

- Selling Pressure = Gravity. It exists objectively, is patient, and doesn't care about your grand vision.

- Real Demand = Rocket Engine.

The issue isn't whether gravity exists (it always does), but whether your engine is powerful enough to escape it. Unfortunately, most teams build rockets without engines and then blame the planet's gravity.

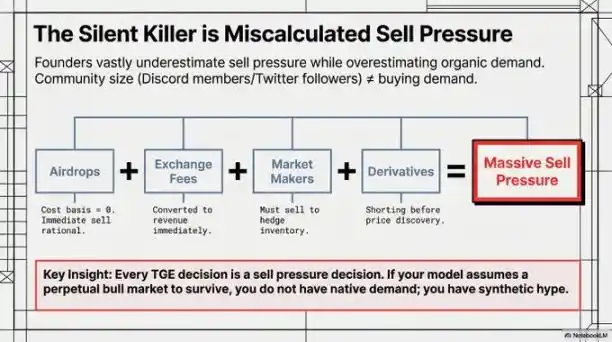

Who Sells on Day One? (It's Not That They're Bad)

Many founders make a big mistake here: seeing selling as betrayal. It's not; it's simple math.

Airdrop users have a cost basis of zero. It's perfectly rational to convert something obtained for free into real money. Data shows that 80% of airdrop users sell their tokens within the first 24 hours of receiving them. This isn't disloyalty; it's human nature.

Centralized exchanges receive tokens as listing fees; this is their revenue. Liquidating their inventory is justified and reasonable.

If market makers are working on a 'loan model' partnership, to hedge risk and prepare stablecoins for quoting, they must also sell a portion of the borrowed tokens. This isn't betrayal either; it's a feature of the model you agreed to, with its inherent math.

Early short sellers act before the price stabilizes. They are veterans, often having been around longer than your project. They are not the problem; your failure to anticipate them is the problem.

Many projects design their tokens assuming the above actors don't exist. But they are real. Either you factor them in, or they will 'teach you a lesson'.

The Valuation Trap (How to Fool Yourself with Math)

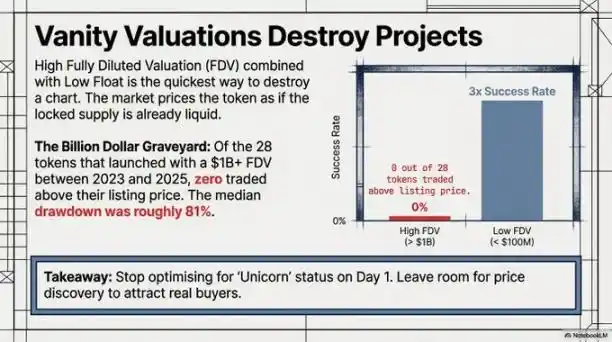

The most expensive vanity item in crypto isn't profile pictures (PFPs); it's an outrageously high Fully Diluted Valuation (FDV).

The common trick: the team releases only 5% of the tokens into circulation ('low float') but publicly claims an FDV of $1 billion.

The market does the math: is the price of the remaining 95% of locked tokens calculated as if they will 'never unlock'? But that's impossible; they will eventually be released. When that day comes, the price plummets like a 'ski jump'.

The data is staggering, and every founder should see it:

FDV at Launch

- Above $1 billion: By year-end, not a single token was above its launch price. Median decline: 81%.

- Below $100 million: The probability of performing well in the first month is 3 times higher than for tokens with an FDV over $500 million.

A 100% failure rate. Not 70%, not 90%, but 100%.

Yet founders keep doing it because '$1 billion FDV' looks great in press releases and makes early investors' paper gains look good before they can actually sell. Essentially, it's a 'pricing illusion' that the market mercilessly bursts.

Obsessing over launch day FDV is like judging a company's success by how pretty its PowerPoint is. It might impress those who don't look long-term. A lower valuation leaves room for genuine price discovery, enabling sustainable growth. Low-key launches often survive; vanity launches mostly die.

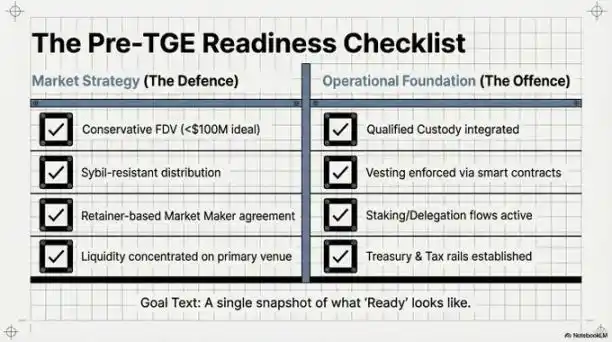

Four Talismans (The Things That Actually Work)

Arrakis summarized four key pillars that distinguish who survives from who just pays tuition. We add our own insights.

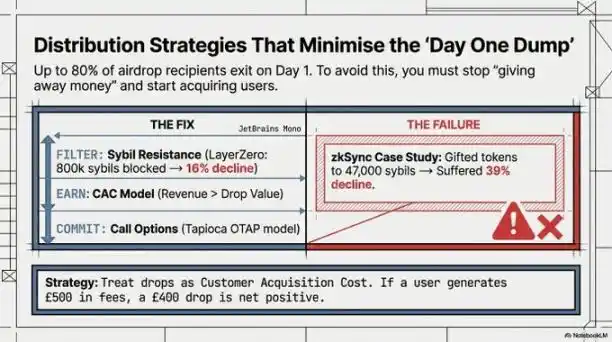

Talisman 1: Sybil — Filter Before Airdrop

A comparison of two cases makes it clear:

- @LayerZero_Core put in the hard work, identifying 800,000 'Sybil addresses' (fake accounts farming the airdrop) before the token launch. These recipients would only sell immediately and never return. Result: only a 16% drop in the first month.

- zkSync did little filtering, resulting in 47,000 Sybil addresses receiving the airdrop. Result: a 39% drop over the same period.

The difference between 16% and 39% is the price of not doing the homework.

Sybil resistance sounds tedious, but think clearly: you are paying for real users, not feeding parasites. Those airdrop farmers don't want your product; they only want your token. Make it costlier for those who don't use your product to get the token.

Talisman 2: Revenue-Based Airdrop — Treat Airdrop as 'Customer Acquisition Cost'

Change your perspective on airdrops: don't see them as 'community rewards', see them as 'customer acquisition cost'.

If a user contributed $500 in fees to your protocol, and you reward them with $400 worth of tokens. Even if they sell all tokens immediately, this 'acquisition' is still a net gain ($100 net profit). Real economic activity has already occurred; the token sell-off is just an entry in the ledger, not a disaster.

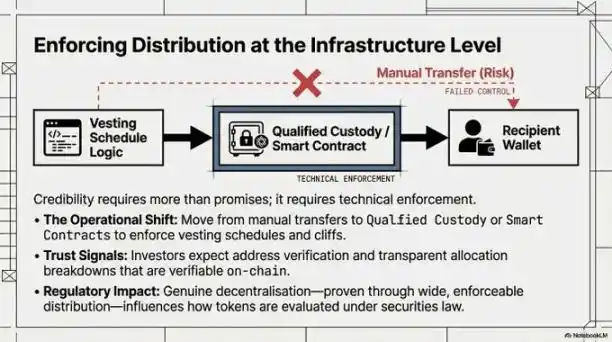

Talisman 3: Infrastructure Readiness — Don't Roll Out a Car Without an Engine

Staking and governance functionalities must be available the moment the token launches. Not 'coming soon', not 'in development', but 'available immediately'.

If not, the result will be:

Early supporters get the token and find they can neither stake it for yield nor participate in voting. Capital sits idle. Idle, non-yielding capital gets sold. This isn't disloyalty; it's basic investment logic.

Additionally, a qualified custody solution must be in place from day one. This is a hard requirement institutional investors will check. If custody is still just a 'multisig' without a compliant framework, large funds simply won't enter. This isn't being difficult; it's their risk management.

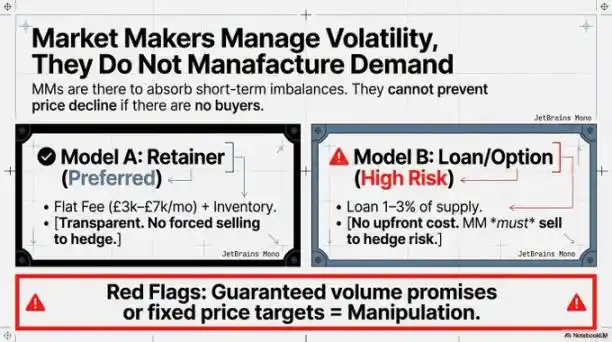

Talisman 4: Choosing the Right Market Maker — Understand the Service You're Buying

Market makers provide 'liquidity' (market depth), not 'demand' (buyers). This is crucial. Some founders hire market makers thinking they're hiring a 'price protection squad'. They only make existing buying and selling smoother; they can't conjure up buyers.

- The 'Engagement Model' is more transparent and better.

- The 'Loan Model' can be useful, but the market maker's own hedging needs inherently conflict with your goal of stabilizing the price.

Danger signs when choosing a market maker:

- Guaranteed volume targets

- Unwilling to accept your terms

- Promising to support the price under heavy selling pressure

These might indicate they plan to use wash trading (fake volume) instead of legitimate market making.

Liquidity should be concentrated. Spreading $1 million across three chains results in shallow 'depth' on each chain, unable to withstand any pressure. It's better to choose one main battlefield and create deep liquidity there. Depth in one place is better than thin coverage in three.

The Ultimate Goal: Decentralization

The infrastructure and distribution mentioned earlier are defensive measures. The real long-term goal is for the protocol to mature truly in four aspects:

- Development Decentralization: Not just the core team can write code; third parties can also participate in development through grant programs.

- Governance Decentralization: Transparent decision-making process, multi-party participation, proposals that are actually implemented.

- Value Distribution Decentralization: Economic design allows more participants to benefit, not just enriching an internal circle.

- Access Decentralization: Global users can participate in staking, voting, etc., through low-barrier, compliant means, not limited to crypto veterans.

The brilliance of the Arrakis framework lies here. A protocol that is only well-prepared at launch but does not advance true decentralization is merely postponing 'centralization risk', not solving it.

Final Thoughts

Arrakis's research is one of the most rigorous analyses of TGE in the first quarter of this year. The core argument is correct: a token launch is about deploying infrastructure, not running a marketing campaign.

Teams that treat it as marketing often produce beautiful 'first-week charts', followed by a 'ski jump' decline. Teams that treat it as infrastructure—meticulously analyzing sell pressure sources, preparing months in advance, not chasing inflated FDV, filtering out airdrop farmers—they often become the surviving 15%.

We want to add one point: real demand for the token must come from the protocol's inherent utility, not from marketing hype. People must genuinely need this token to access the value created by the protocol. If the token's only use is 'governing a protocol no one uses', then even perfect Sybil resistance and compliant custody are useless. Governing something useless has no value.

Before thinking about how to launch, think about how to create real demand first.