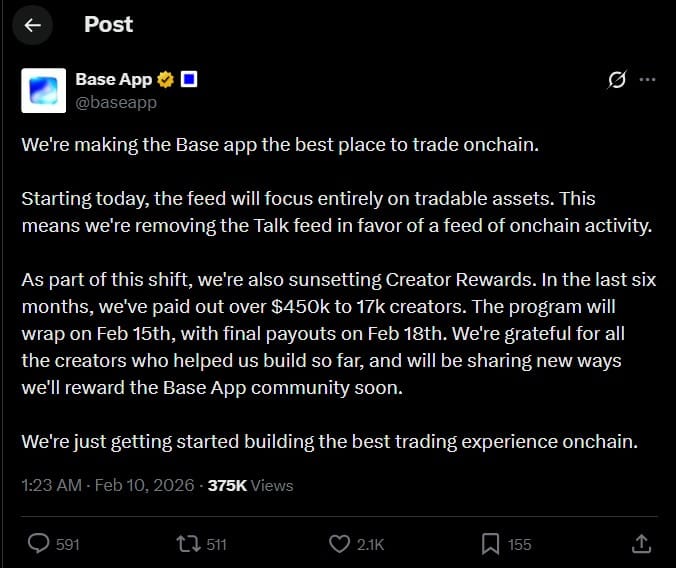

Coinbase is shutting down the app’s Creator Rewards program and its Farcaster-powered social feed, with its focus now on tradable assets. The Creator Rewards initiative, launched in July, was designed to encourage posts and engagement by paying users for activity.

In practice, the payouts were modest. Base says around $450,000 was shared among roughly 17,000 creators over seven months, averaging about $26 per person.

According to creator Jesse Pollak, the decision came down to focus. As the app evolved, the team realized it worked best when it did fewer things well. He stated,

“…as we’ve rolled the app out, we’ve realized we need to do less, better. and by focusing on tradable assets, that’s exactly what we can do.”

The Creator Rewards program will officially end this week, with final payouts scheduled for the 18th of February. Pollak also noted that Base App was never an ideal home for Farcaster’s social feed, and expects most users to return to Farcaster’s native app.

Importantly, the changes do not affect Base’s Creator Coins feature, which remains active.

AMBCrypto previously reported that Coinbase was considering launching a native token called BASE, and that it was likely to happen this year. However, there’s not been much talk on that front since.

Do they really need a native token, though?

For now, it looks like they don’t.

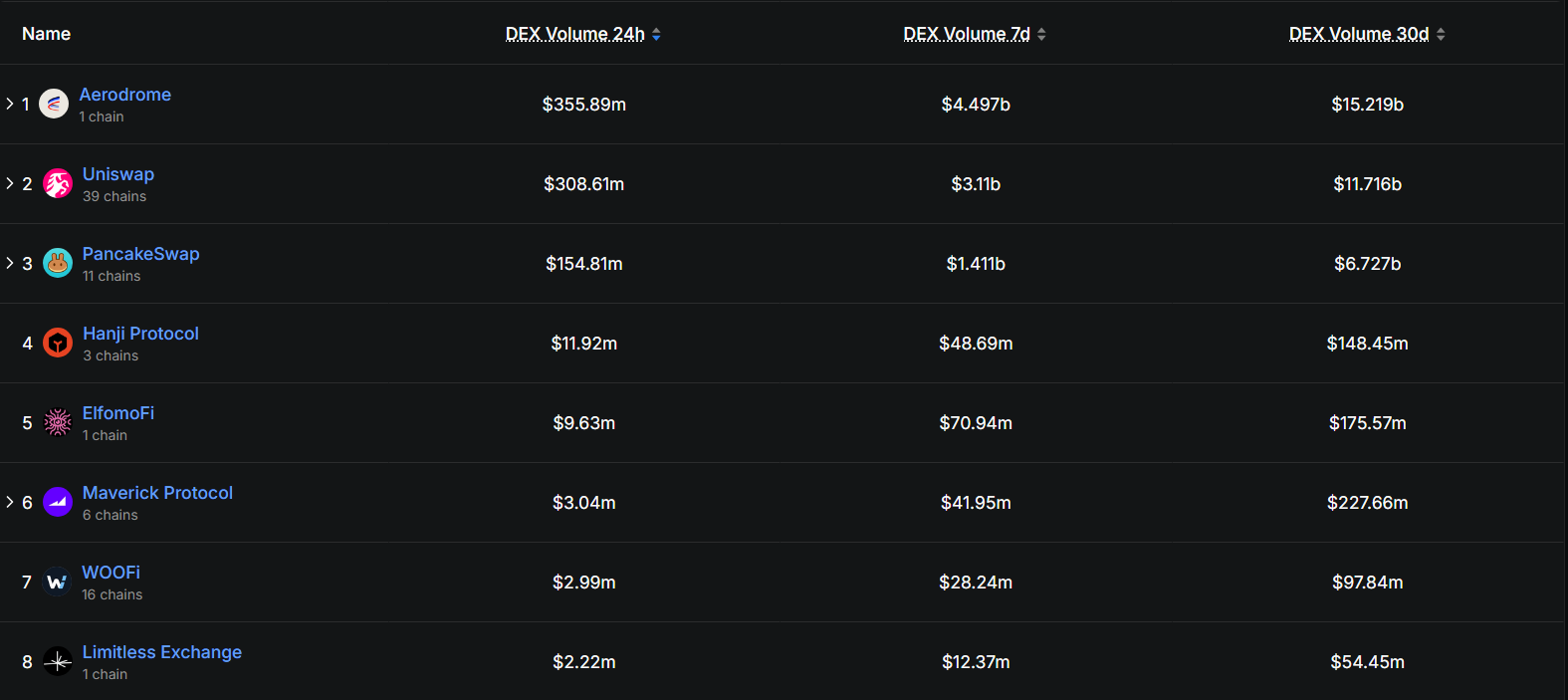

Over the past 30 days, Base-linked DEXs have processed $15.2 billion in trading volume, with Aerodrome Finance [AERO] alone accounting for the bulk of that activity. That puts them ahead of many multi-chain competitors.

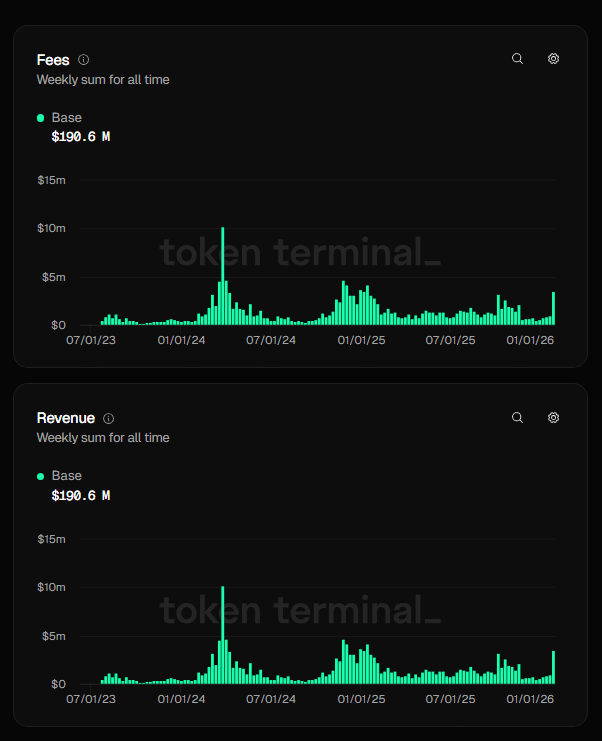

More importantly, the network is generating real money. Data per Token Terminal showed that Base has earned $190.6 million in cumulative fees and revenue to date, with steady weekly inflows.

Instead of relying on a token to bootstrap growth, Base is already monetizing usage directly.

In more recent news, this year’s Super Bowl featured just one major crypto ad, and it was from Coinbase. The streamlining of priorities makes sense as Coinbase seemingly looks to build a bigger brand.

Final Thoughts

- Base is prioritizing trading and revenue, with volume and fees doing the work a token usually would.

- With growth already monetized, a native Base token looks optional rather than necessary.