Altcoins are under pressure, but whales are beginning to circle back in.

Most tokens remain far below their 2025 highs, while many holders have endured four years of pain with almost nothing to show for it. However, this wallet did not chase strength. It targeted battered DeFi-linked names near the floor. So, what exactly did it buy?

Whale pulls $16M in altcoins from Binance

On the 24th of March 2026, whale 0x04d8 pulled $16.06 million from Binance.

The wallet loaded 43.49 million ENA valued at $4.07 million, 32,872 AAVE worth $3.64 million, 249,741 AVAX worth $2.37 million, 595,886 UNI worth $2.13 million, 8.07 million ONDO worth $2.05 million, and 1.49 million PENDLE valued at $1.81 million.

Was that random? No. The wallet leaned hard into DeFi-linked names. Therefore, this looked less like blind gambling and more like early positioning. Someone stepped into weakness while most of the market kept staring at broken charts and broken confidence.

Big bet lands on DeFi-linked names

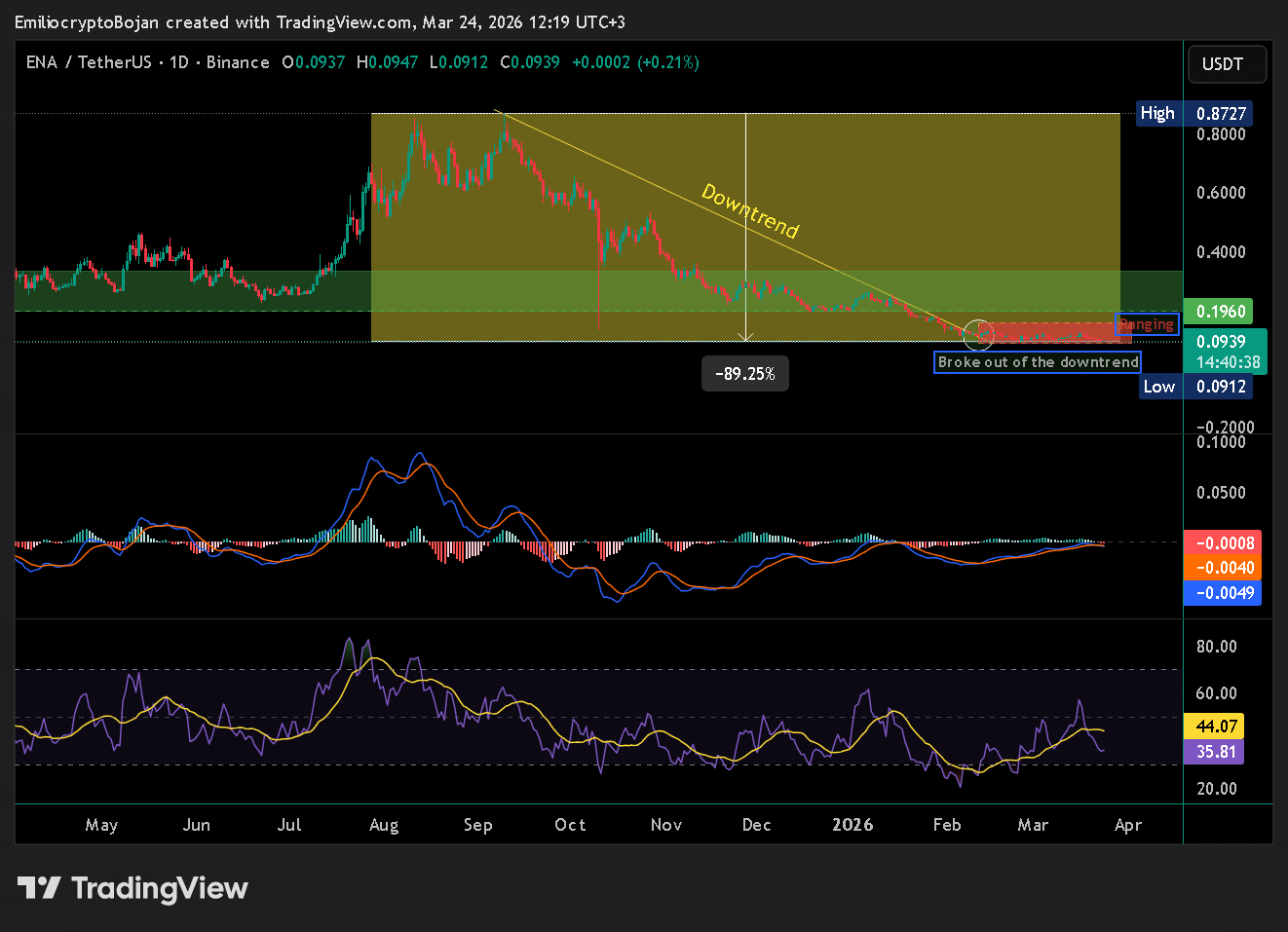

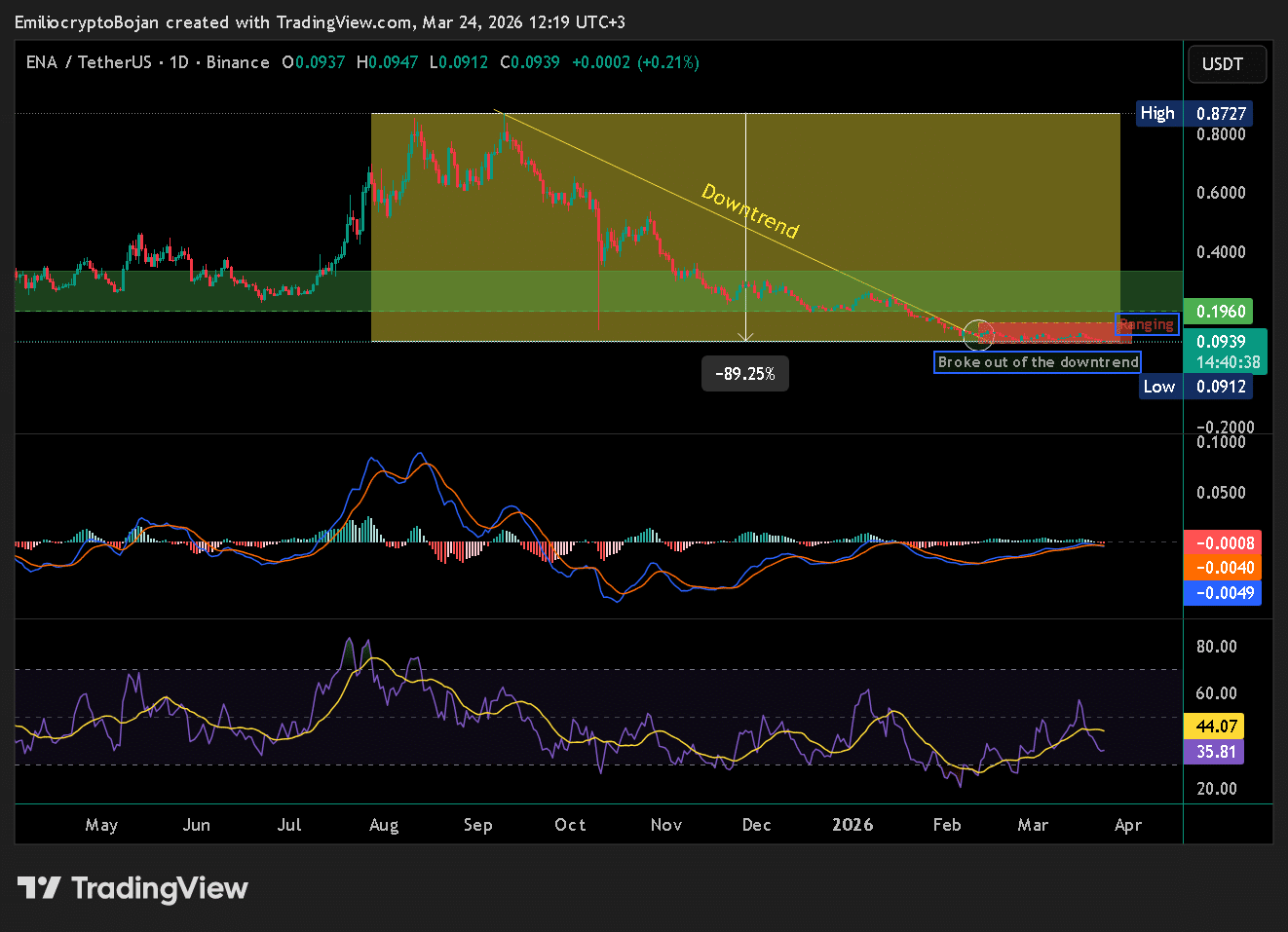

At press time, Ethena [ENA] had broken out of its downtrend after an 89% collapse from its 2025 high near $0.8727, then started ranging sideways near the lows.

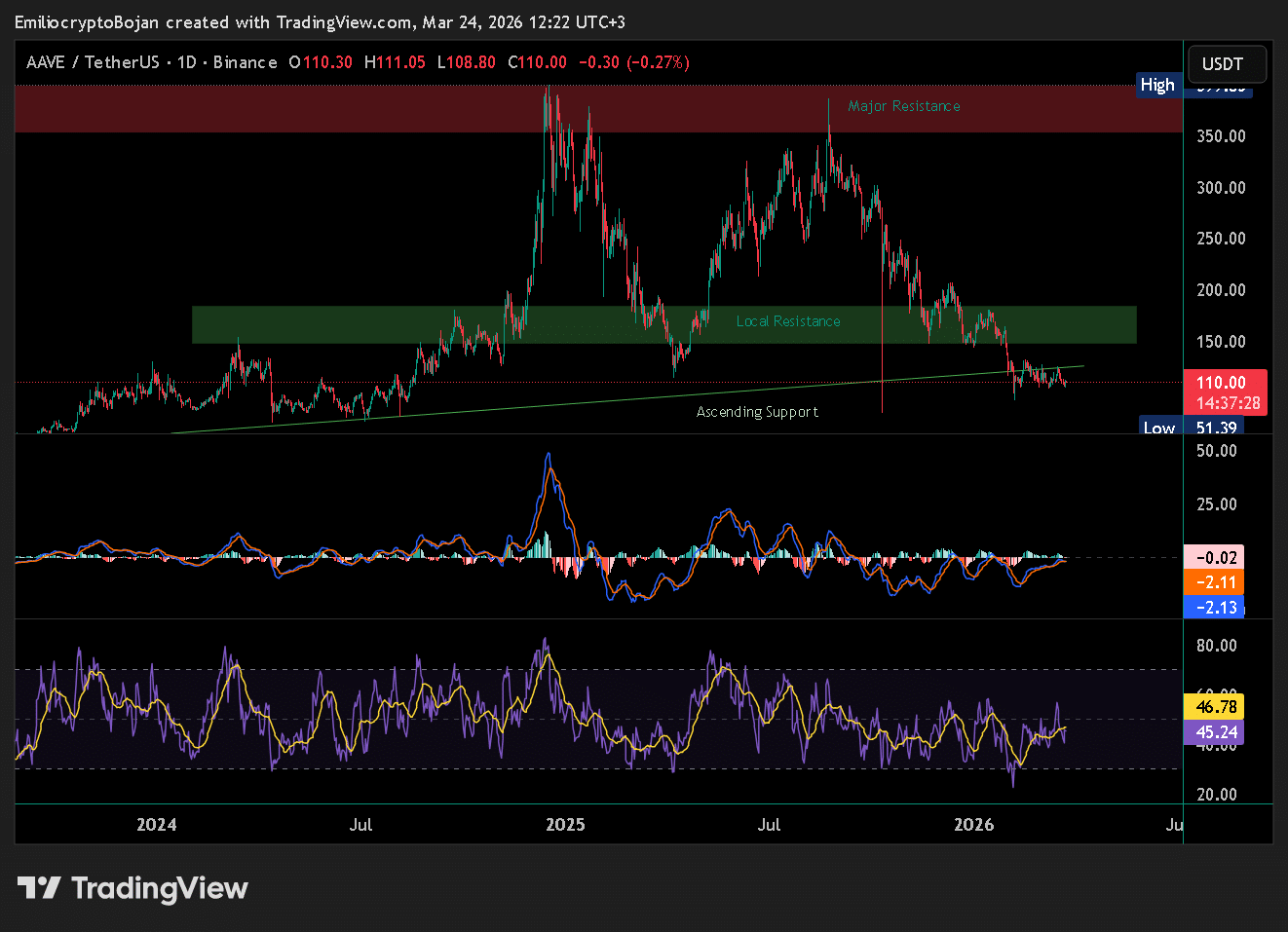

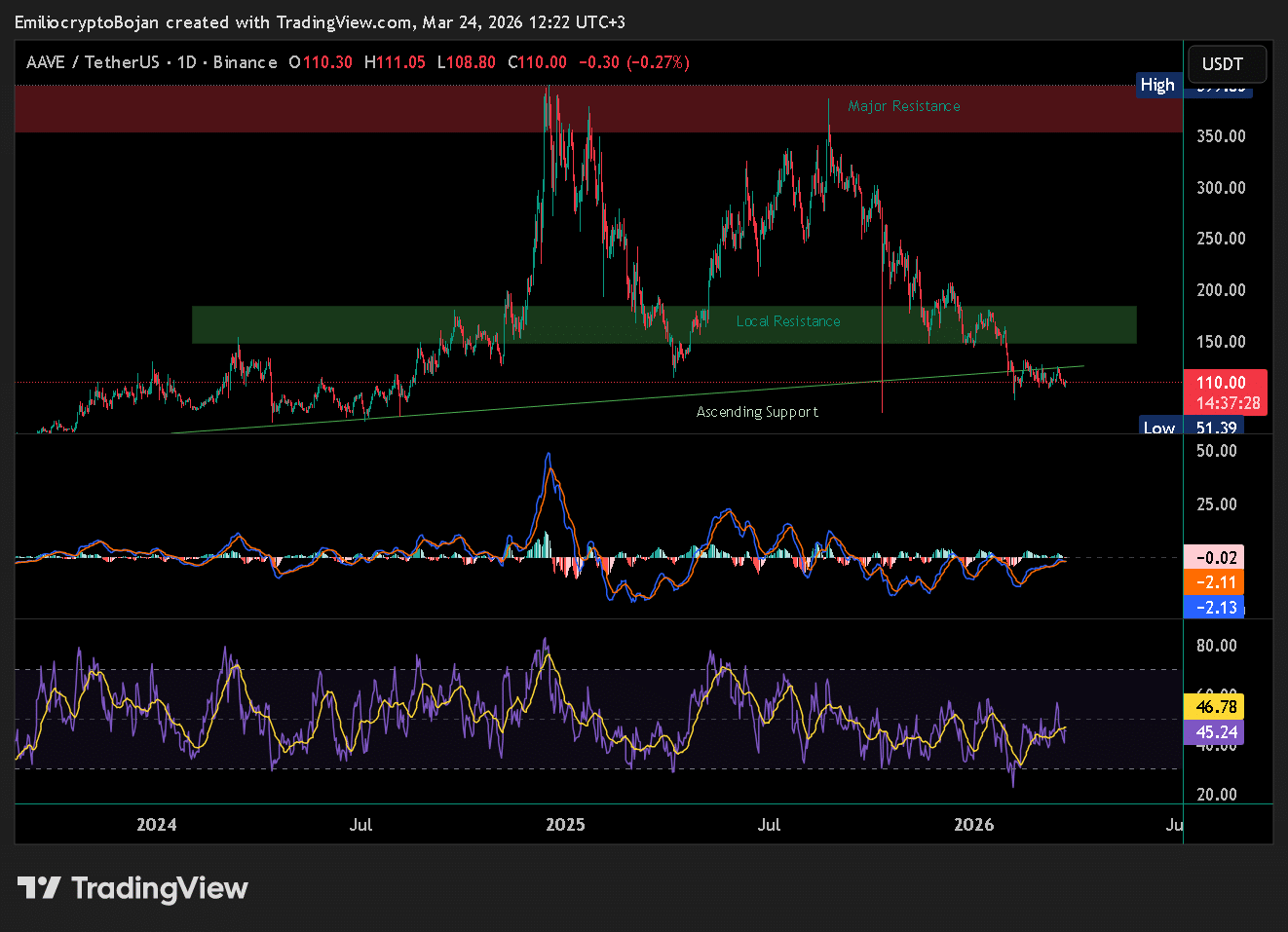

Aave [AAVE] showed signs of weakness. After peaking near 399 in 2024 and 387 later, it completed a double top, dropped hard, and even lost ascending support around 123.

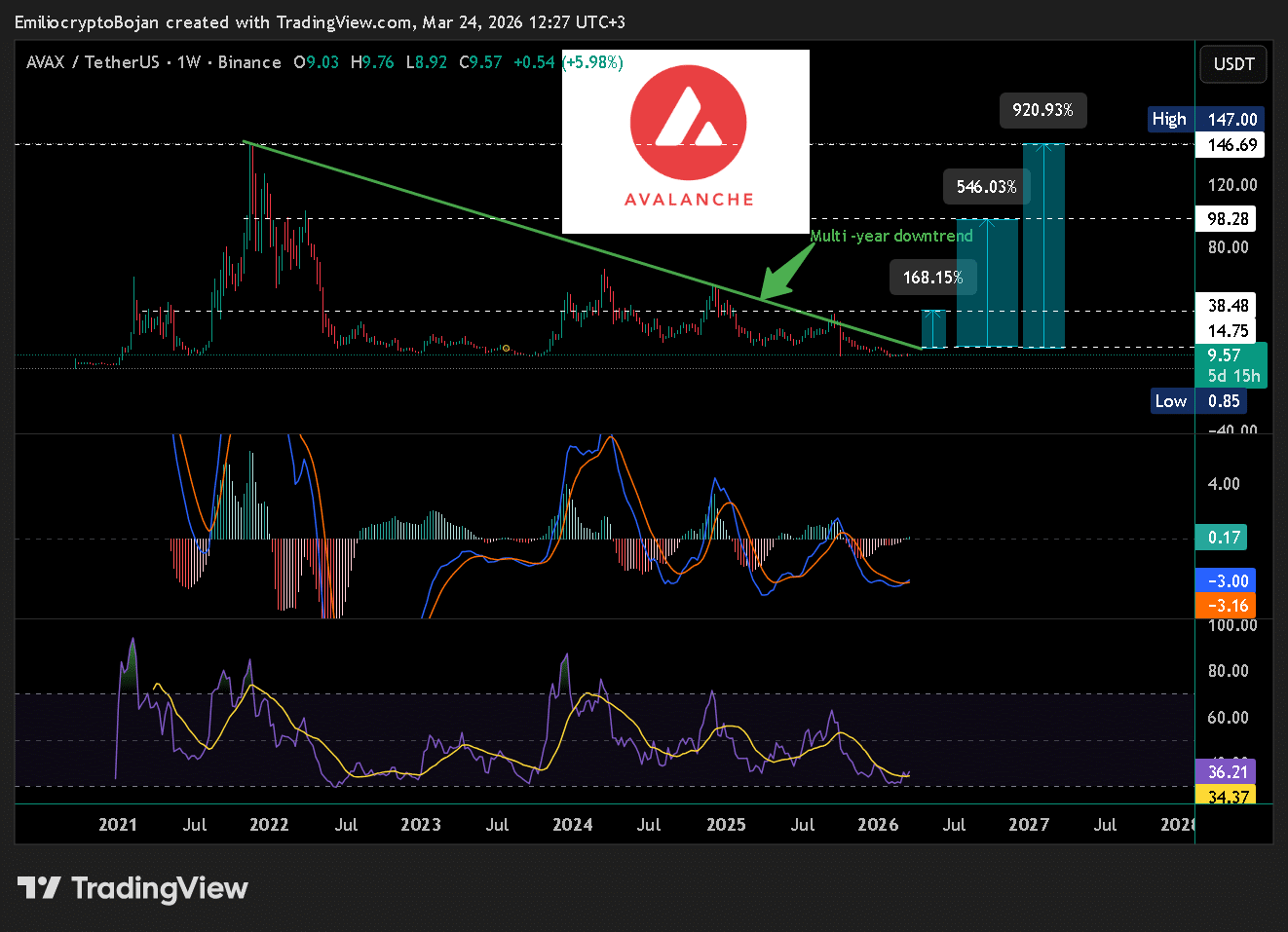

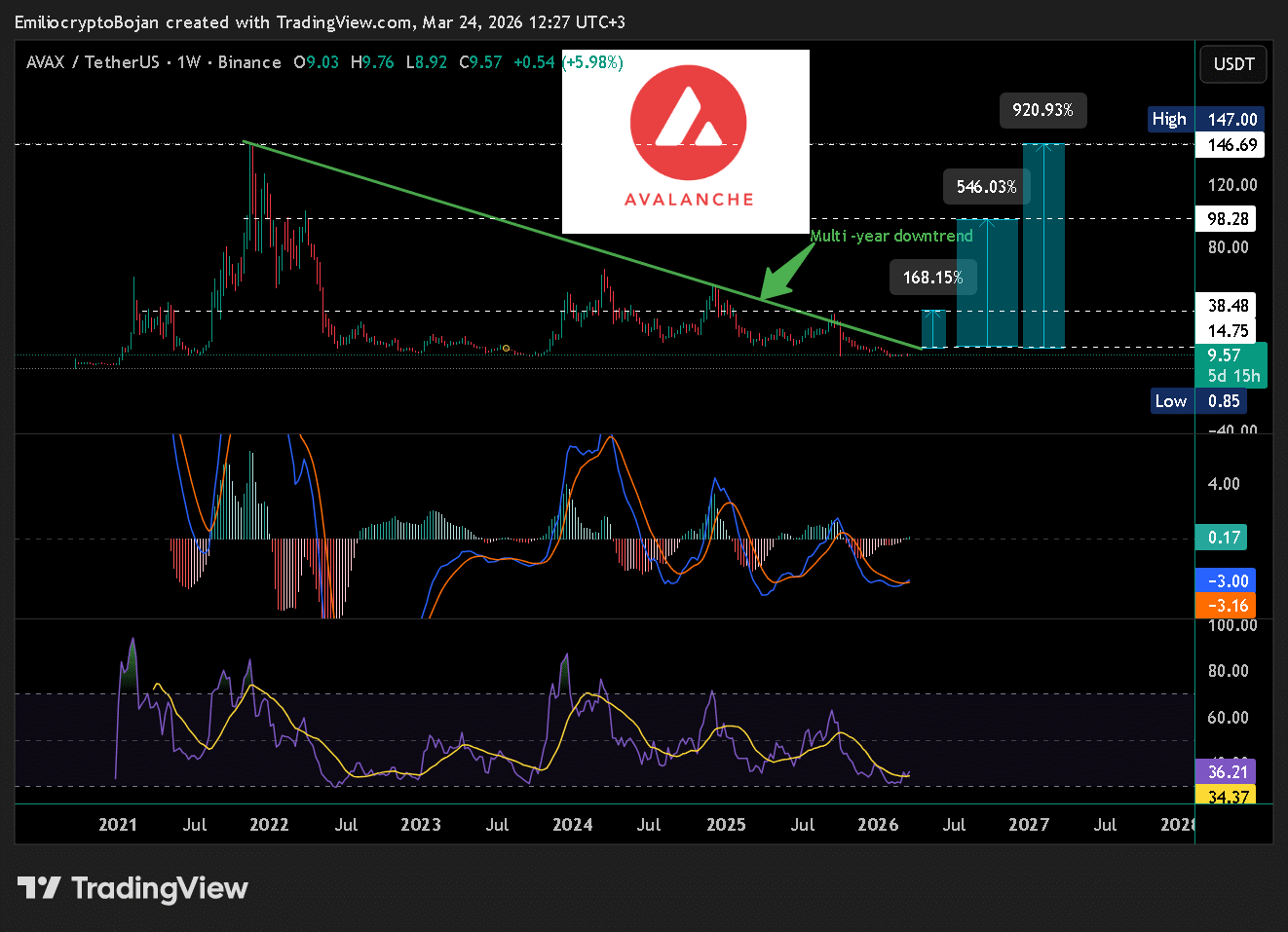

Avalanche [AVAX] looked more constructive. It had flashed a bullish MACD crossover and started pressing against a multiyear downtrend, with $14.75 and $38.48 as early targets if that line broke.

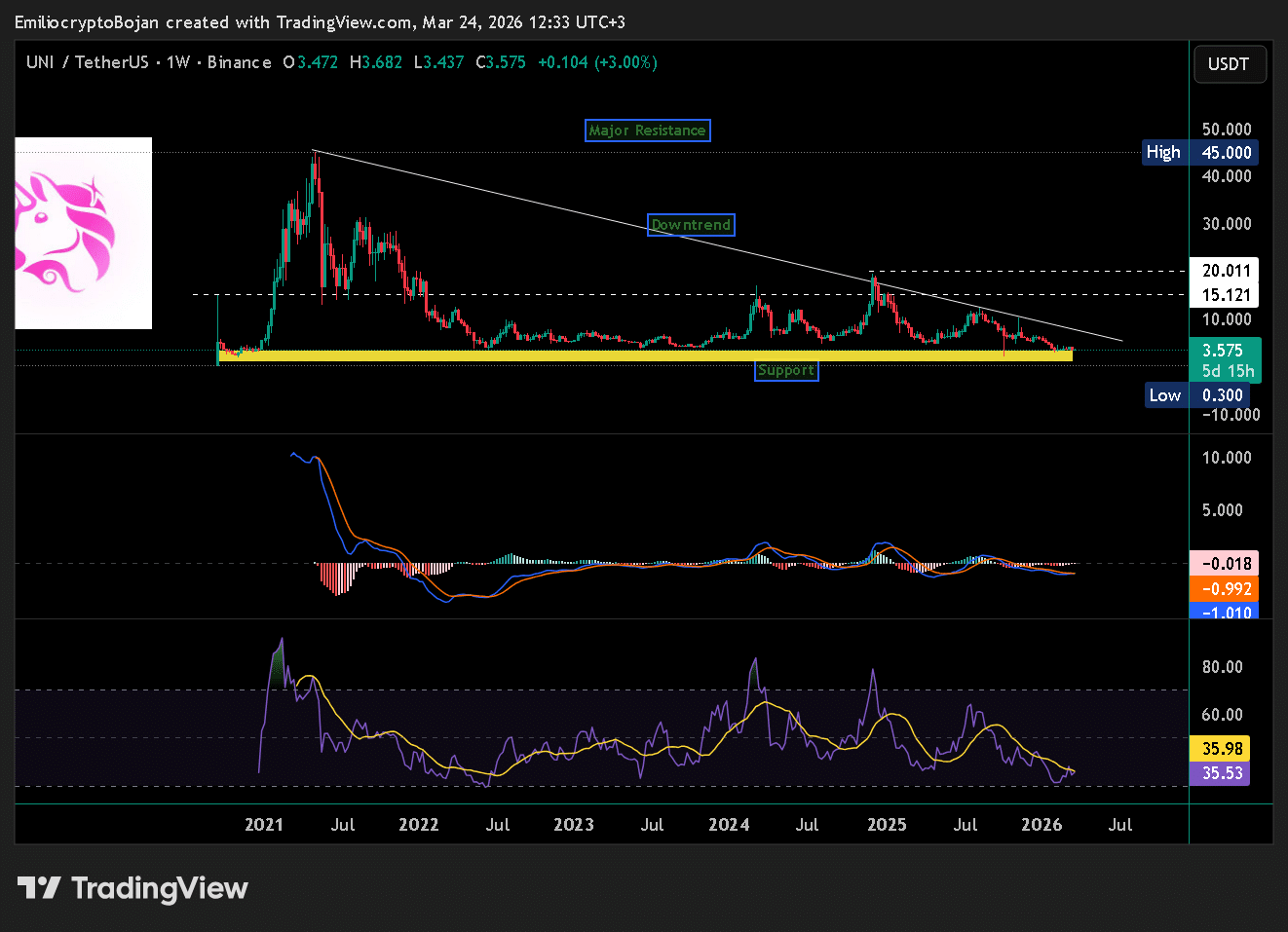

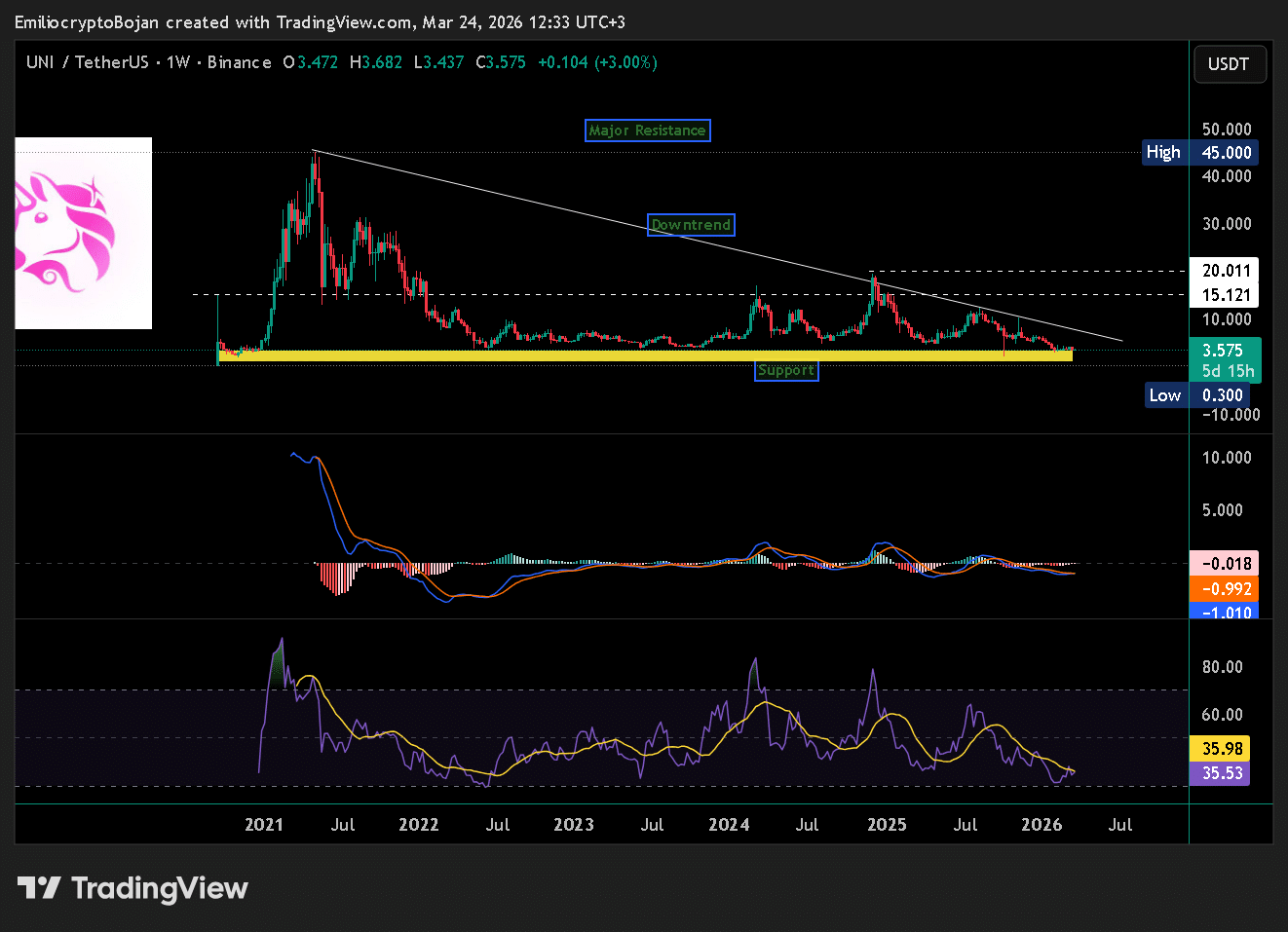

Uniswap [UNI] followed a similar script, still trading near support while leaning toward its own multiyear downtrend, with $15 and $20 standing out before any real test of $45.

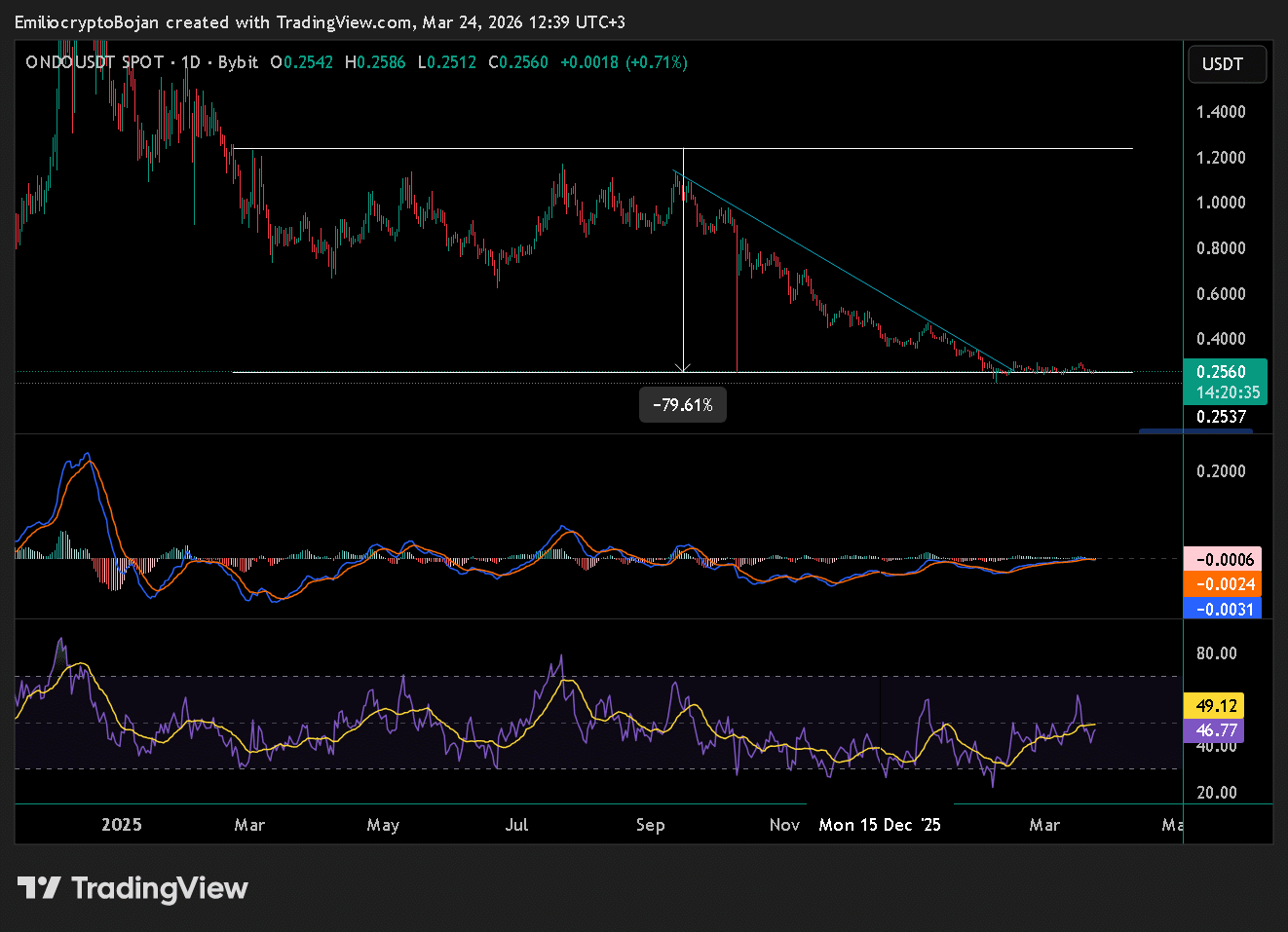

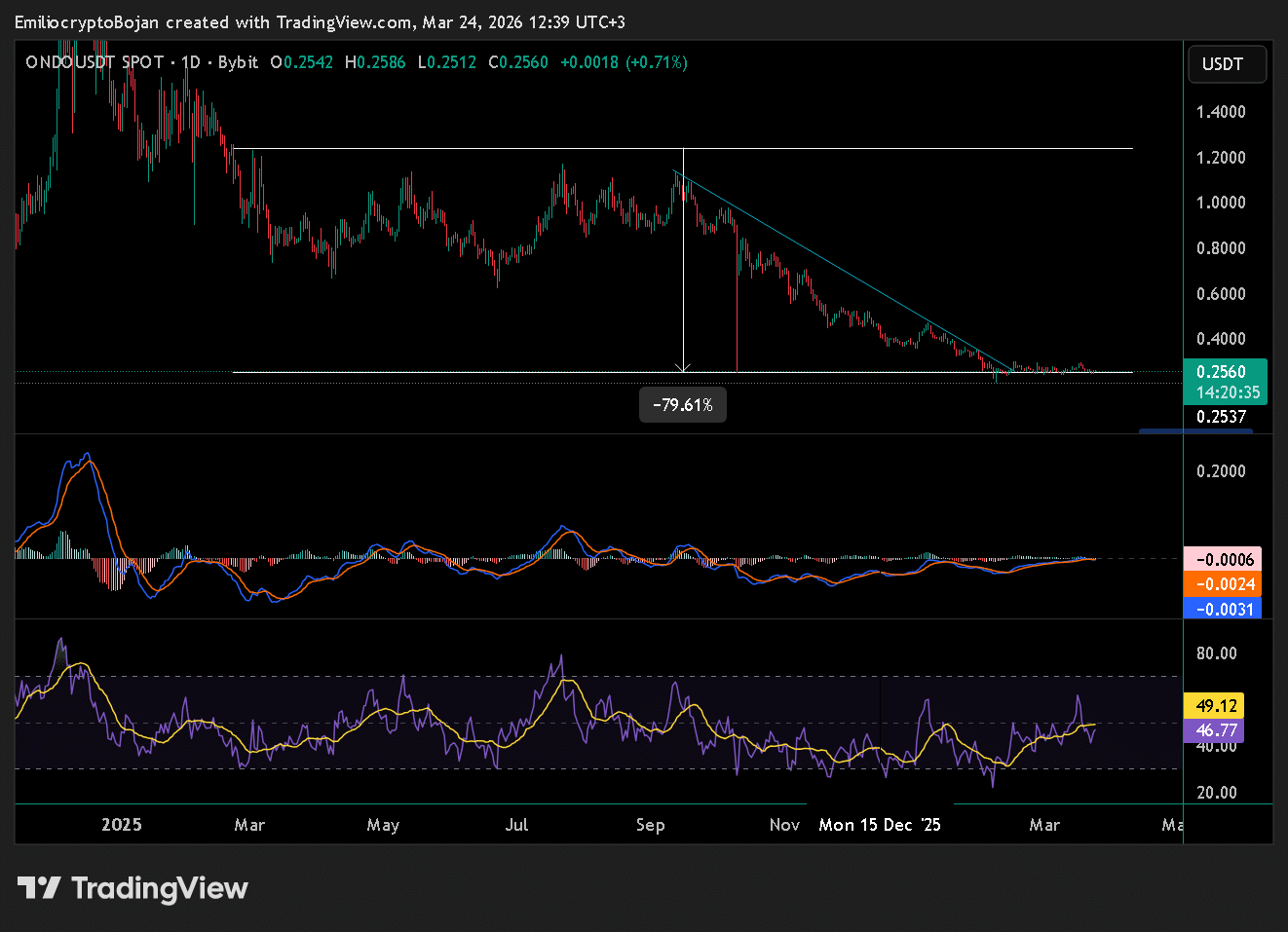

Ondo [ONDO] had already broken out of its downtrend after a 78%+ drawdown from its 2025 high and then moved sideways.

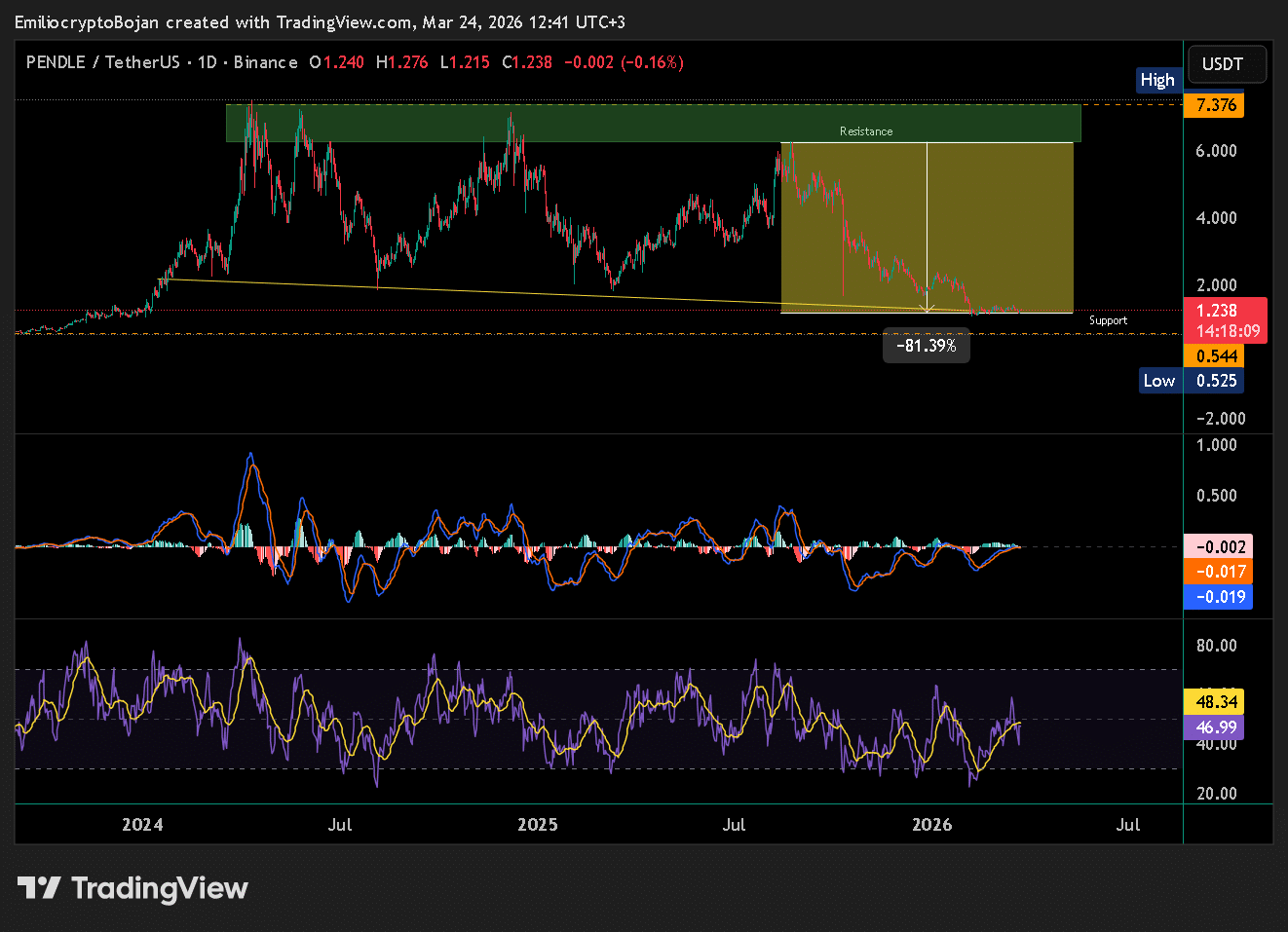

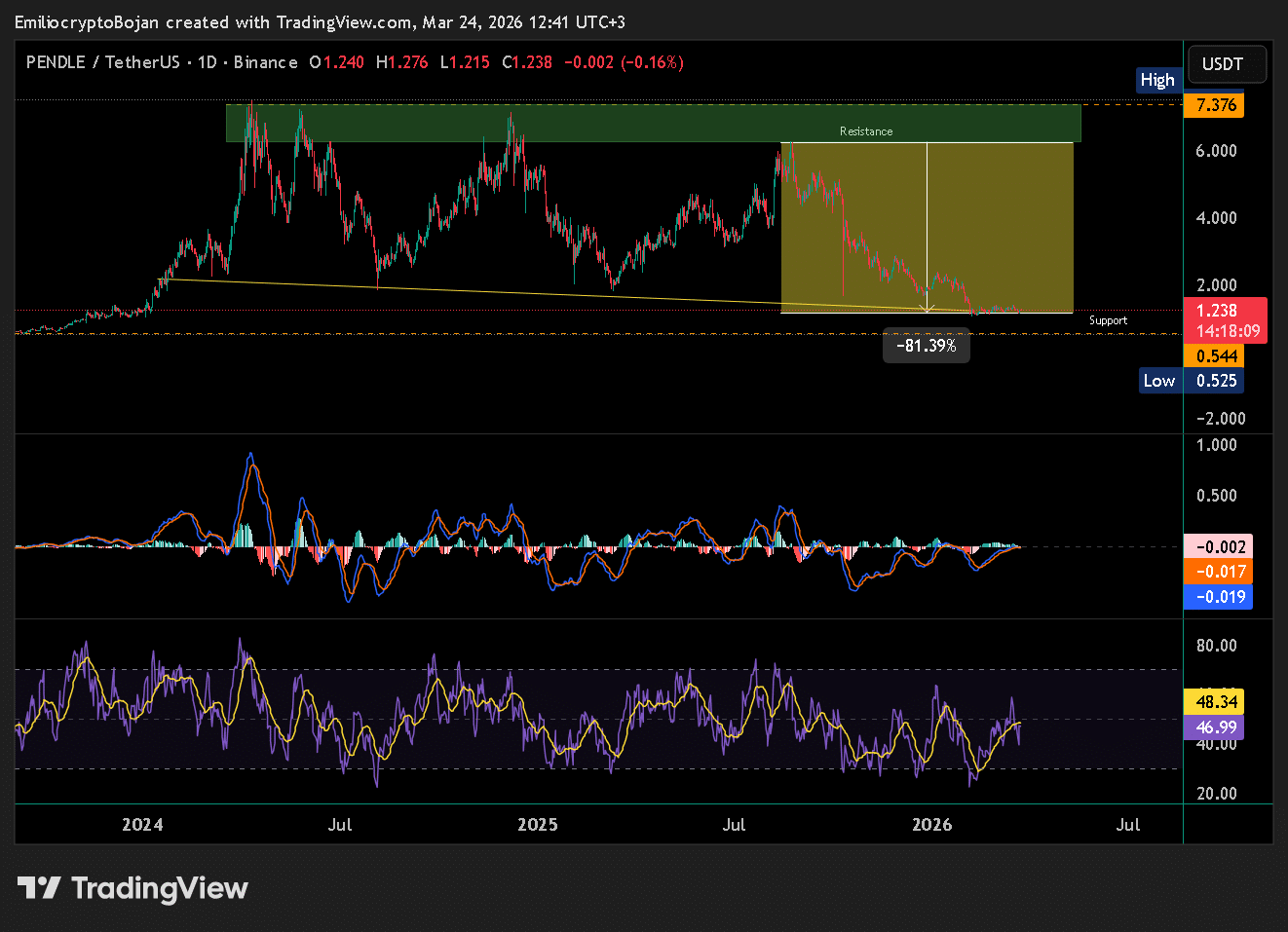

Pendle [PENDLE] stayed above the $1 support zone, while lower-timeframe momentum started picking up.

Even so, most of these names were still trading more than 80% below their 2025 highs.

Is a DeFi rotation about to begin?

Was this the sign of a DeFi rotation? Not yet. One wallet did not repair a market that had punished altcoin holders for years. However, these were the kind of withdrawals whales made near bottoms, not tops.

The real takeaway is that the wallet bought into altcoin weakness. If these assets continue to hold sideways and begin reclaiming structure, talk of a DeFi rotation will quickly stop sounding premature.

Final Summary

- This whale targeted damaged DeFi names at depressed levels, and that made the move serious.

- If structure kept improving across this basket, the market could be witnessing early rotation.