While many are currently concerned about Circle’s stock performance on the NYSE, the company’s partnership with Sasai Fintech, a business of Cassava Technologies, tells an interesting story.

This move isn’t just about expanding into Africa; it’s aimed at tackling a long‐standing challenge: cross‐border payments that remain slow, costly, and inefficient. The plan is to bring USDC into Sasai’s mobile platform, which already supports payments and remittances across multiple African countries.

USDC x Sasai’s partnership: A green flag

Currently, fees can go above 7%, so using a stablecoin like USDC can make transactions faster, cheaper, and more reliable.

By adding USDC into a mobile platform that already supports fast-moving trade, it removes the delays and high costs of traditional systems, where transactions can take days.

Additionally, the partnership is also meant to offer a stable and transparent way to make cross-border payments. This would, in turn, help businesses avoid local currency swings while staying connected to the global market.

Executives weighing in

Remarking on the same, Strive Masiyiwa, Founder and Executive Chairman at Cassava Technologies, said,

Africa’s digital economy is entering a new era, propelled by entrepreneurship, a mobile-first generation, and the acceleration of intra-regional trade.

Adding more to the sentiment, Jeremy Allaire, co-founder and CEO at Circle, noted,

Working with Cassava, we can extend the benefits of USDC and onchain infrastructure into high-growth payment corridors to deliver always-on global connectivity.

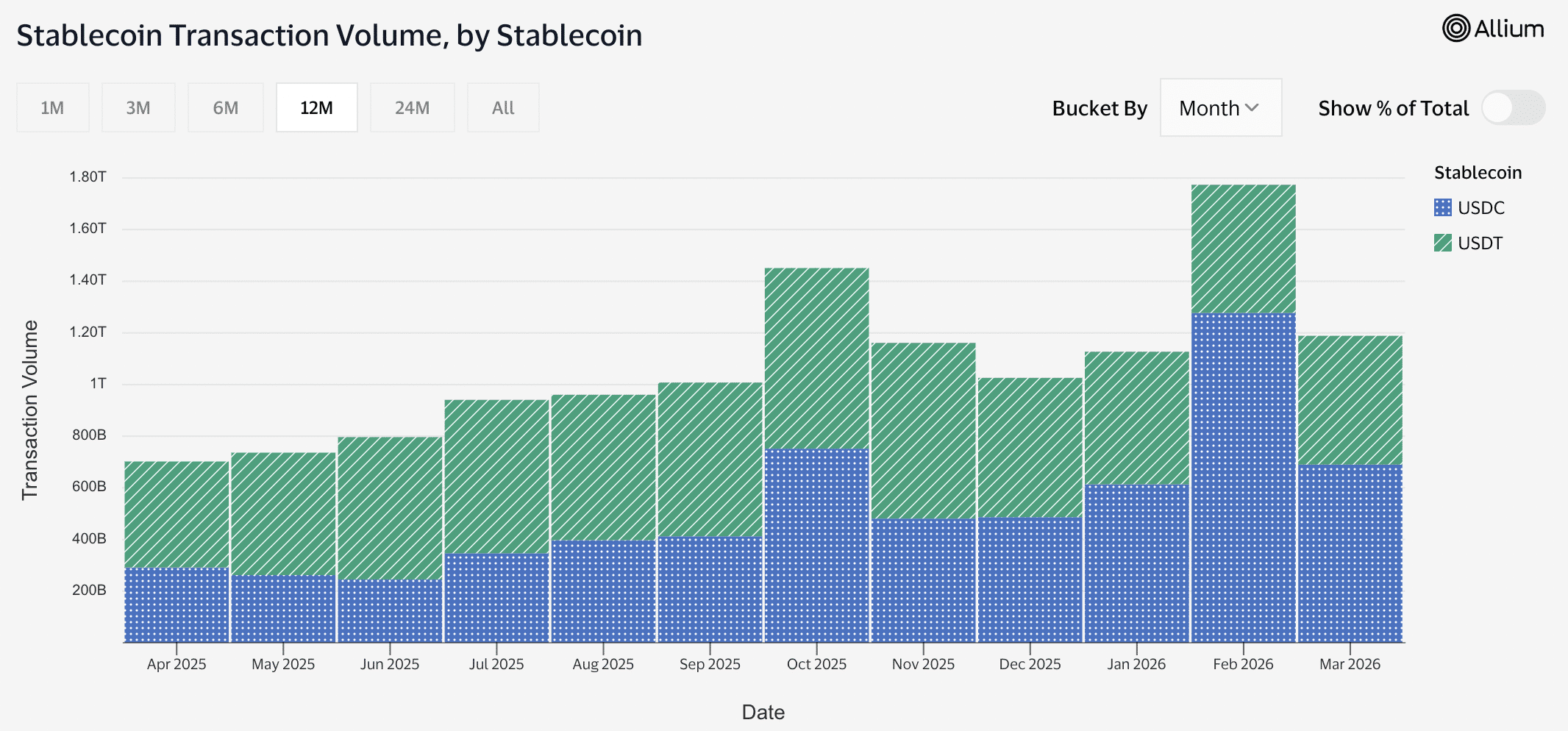

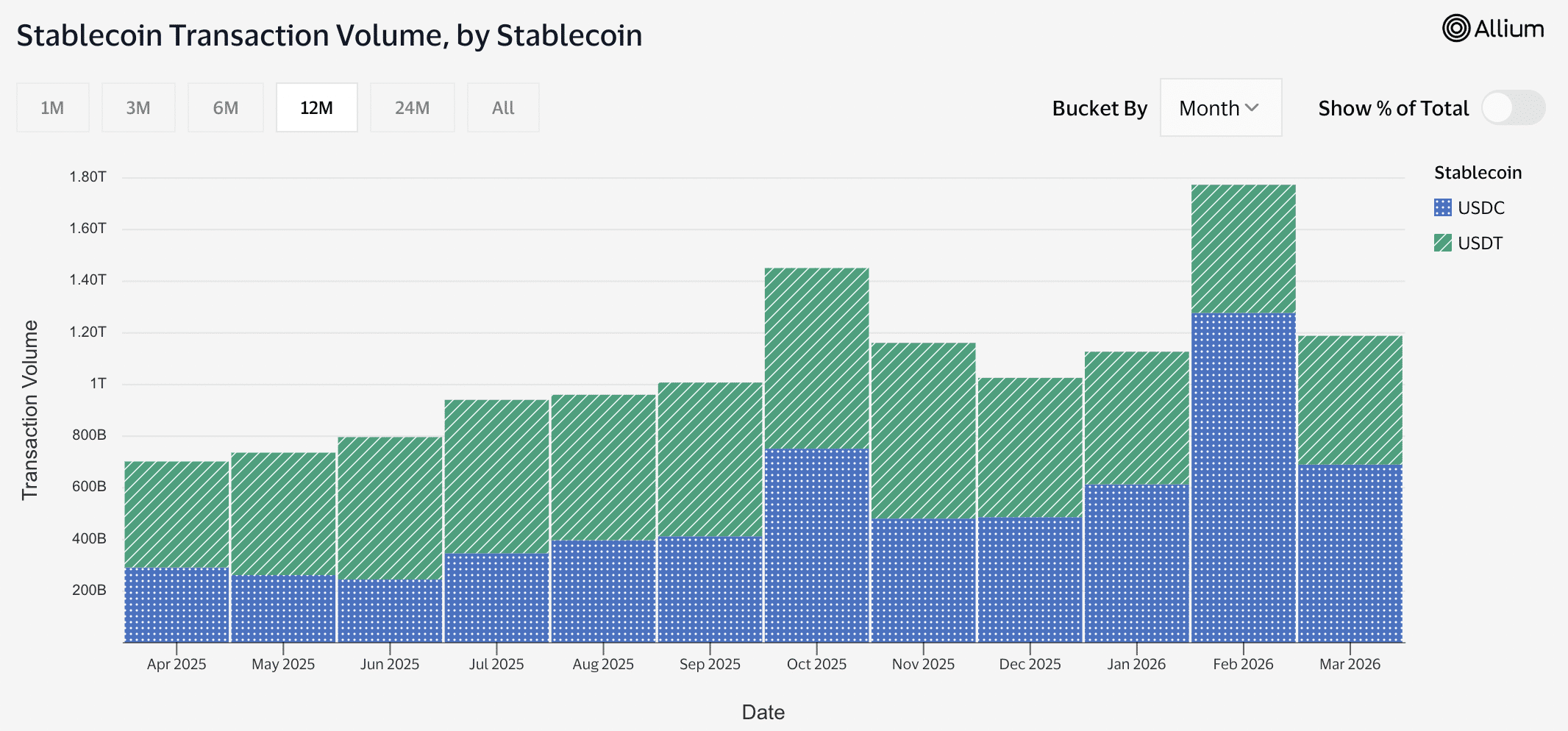

Stablecoin’s market dynamics: USDC vs. USDT

The partnership comes at an important time for stablecoins, which have handled a huge $70.2 trillion in transactions over the past year. While USDT was leading for most of 2025, things started to change in early 2026.

Even though total activity slowed a bit in March after a strong February, USDC has started catching up and even briefly matched USDT’s share.

This rise in USDC signals a shift away from pure speculation toward more reliable systems, something Circle is now bringing to markets like Africa.

Regulatory clarity and more

While Circle expands into Africa, its position in the United States has become shaky due to new regulations.

In 2025, the GENIUS Act gave a positive direction for stablecoins by supporting dollar-backed digital assets. But now, the upcoming CLARITY Act is creating fresh concerns.

This has made investors nervous, as it could directly impact how companies like Circle generate revenue. As a result, Circle’s stock (CRCL) recently saw a sharp drop of nearly 20% on the 24th of March, closing at $101.17.

All this together shows that Circle is at a turning point, dealing with regulatory challenges in the U.S. while building a strong, usage-driven future in markets like Africa.

Final Summary

- Integrating USDC into Sasai’s mobile network could cut remittance costs and speed up settlements.

- The rising competition between USDC and USDT reflects demand for transparency and regulatory alignment.