On April 2, OpenAI and Anthropic each announced an acquisition. OpenAI acquired the tech live show TBPN, while Anthropic spent approximately $400 million in stock to acquire AI biotech startup Coefficient Bio. Both companies are sprinting toward an IPO by the end of 2026, but their shopping lists point to entirely different anxieties.

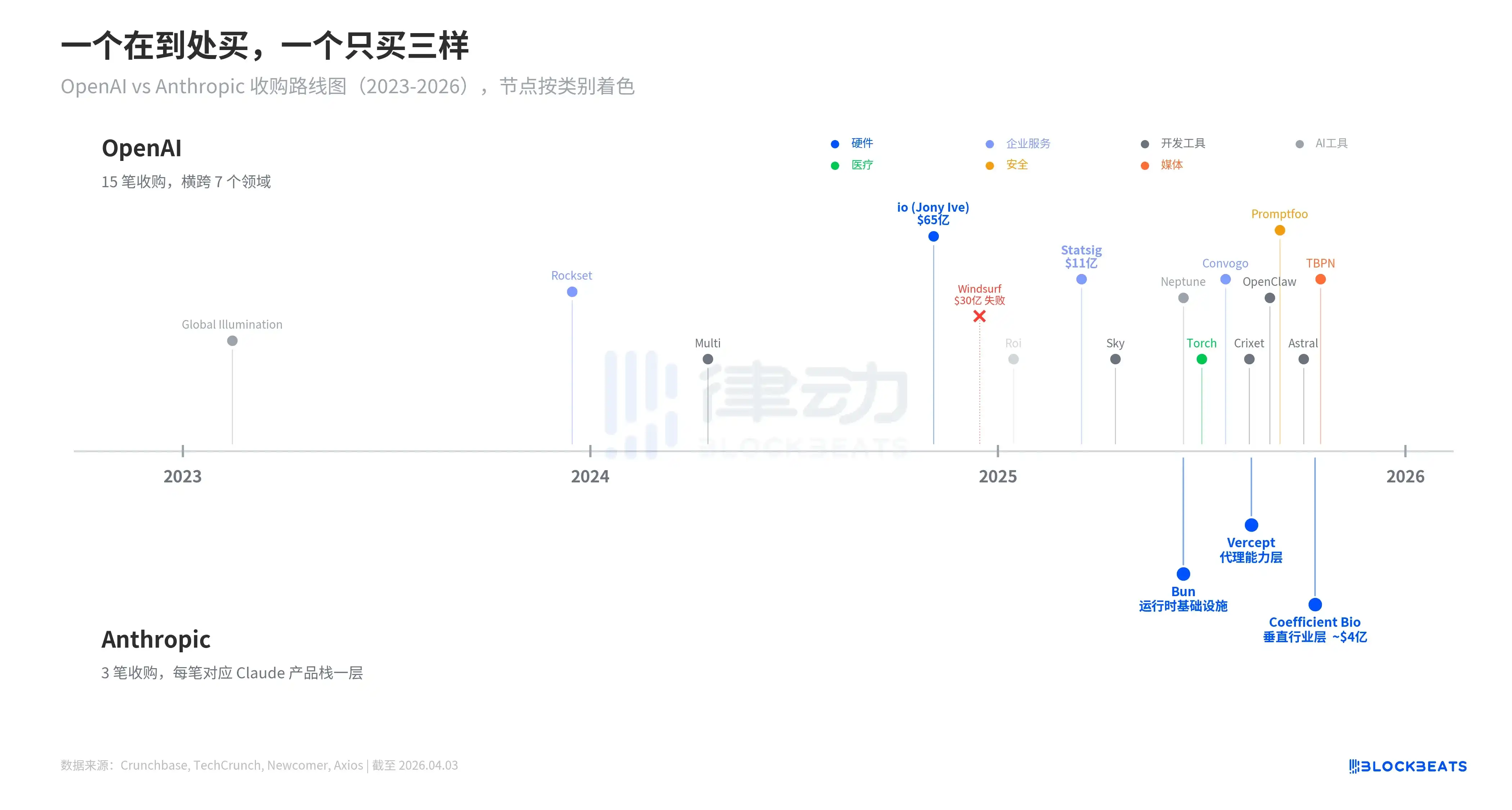

15 vs. 3. This is the number of acquisitions completed by OpenAI and Anthropic, respectively, over the past three years.

According to Crunchbase statistics, OpenAI has completed 15 acquisitions since 2023, spanning seven areas: hardware, enterprise services, developer tools, healthcare, security, media, and consumer. Six were completed in the first three months of 2026 alone. The total disclosed value of these transactions exceeds $7.7 billion, with the largest being the $6.5 billion acquisition of io, an AI hardware company founded by former Apple designer Jony Ive, in May 2025.

Anthropic has only made 3. In December 2025, it acquired the JavaScript runtime Bun to complete the underlying infrastructure for Claude Code. According to an official Anthropic announcement, the acquisition of Bun coincided with the disclosure that Claude Code had reached $1 billion in annualized revenue. In February 2026, it acquired the computer use agent startup Vercept to strengthen Claude's autonomous operation capabilities. On April 2, it acquired Coefficient Bio to enter the life sciences R&D pipeline. Each acquisition precisely corresponds to a technical layer in the Claude product stack.

It is worth noting that OpenAI also had one failed transaction. In May 2025, OpenAI reached a $3 billion acquisition intent with the code editor Windsurf (formerly Codeium). However, according to IT Pro, due to IP clauses in the Microsoft contract, OpenAI could not protect Windsurf's technology from being accessed by Microsoft, and the deal fell through in July. This failure also reflects a structural constraint of OpenAI's "broad procurement" model.

This difference in density is not accidental. It reflects the two companies' vastly different revenue structures and the resulting different anxieties.

Revenue Structure Determines Acquisition Direction

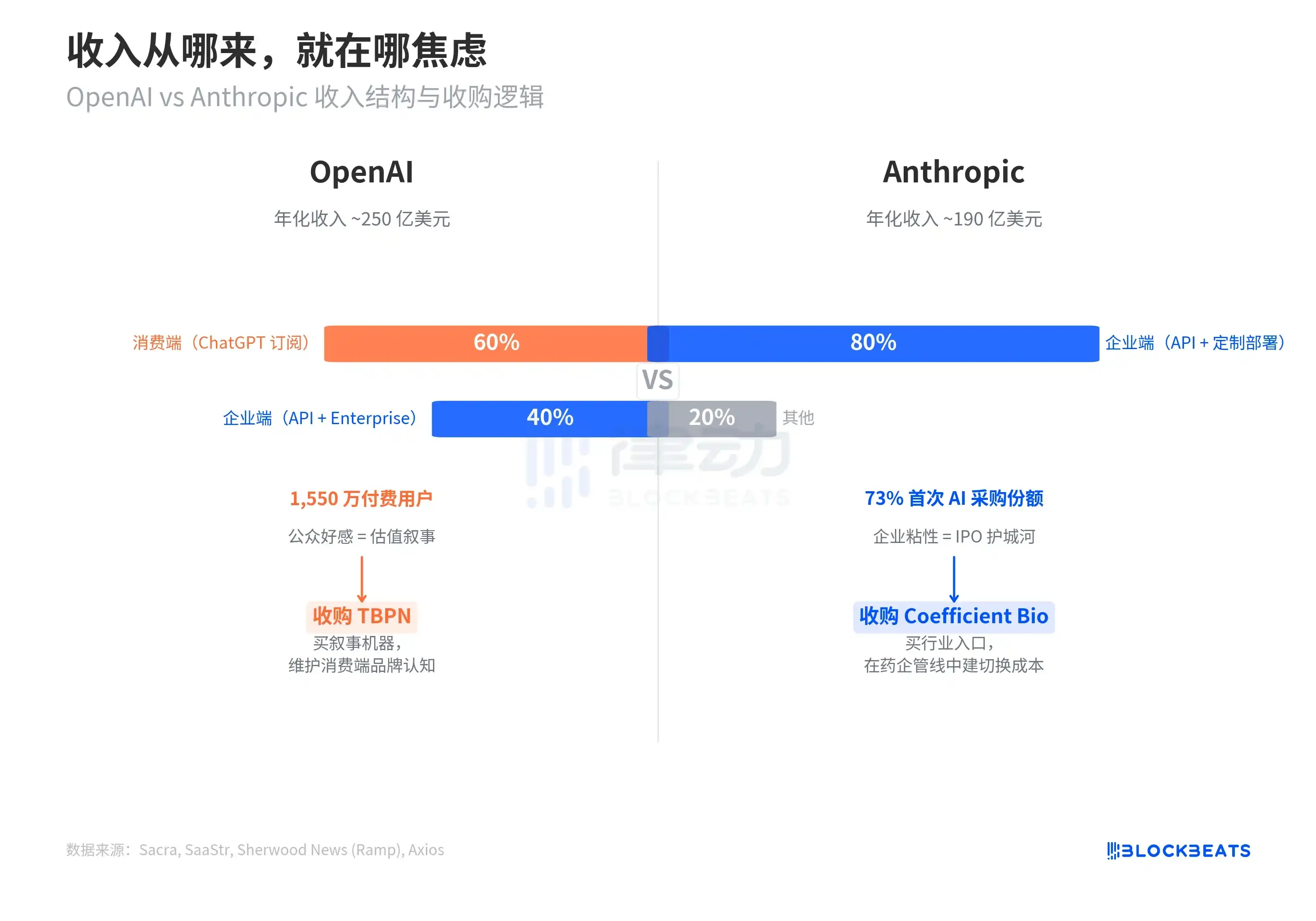

According to Sacra estimates, OpenAI's annualized revenue as of February 2026 was approximately $25 billion, with about 60% coming from the consumer end (ChatGPT subscriptions) and 40% from the enterprise end. 15.5 million paying users are the foundation of OpenAI's income. For a company about to IPO, a high proportion of consumer revenue means public sentiment directly impacts the valuation narrative.

This explains why OpenAI bought TBPN. According to Axios, TBPN is a daily live tech talk show with $5 million in advertising revenue in 2025 and a target of over $30 million for 2026. Post-acquisition, OpenAI will maintain its editorial independence while hiring former Postmates executive Dylan Abruscato to handle advertising monetization. The logic behind buying a tech podcast lies not in its revenue, but in its ability to continuously influence the public discussion framework around AI topics.

Anthropic's anxiety is entirely different. According to Ramp data cited by Sherwood News, Anthropic currently captures 73% of the market share for first-time AI procurement enterprise clients; ten weeks ago, this number was 50%. According to SaaStr, about 80% of Anthropic's revenue comes from the enterprise end. For enterprise customers, choosing an AI supplier is a decision with high switching costs. Anthropic's IPO narrative needs to prove that these enterprise customers will not leave.

Three Moves in Six Months

Coefficient Bio is not an impulsive acquisition. Viewed within the sequence of Anthropic's actions over the past six months, the logic is clear.

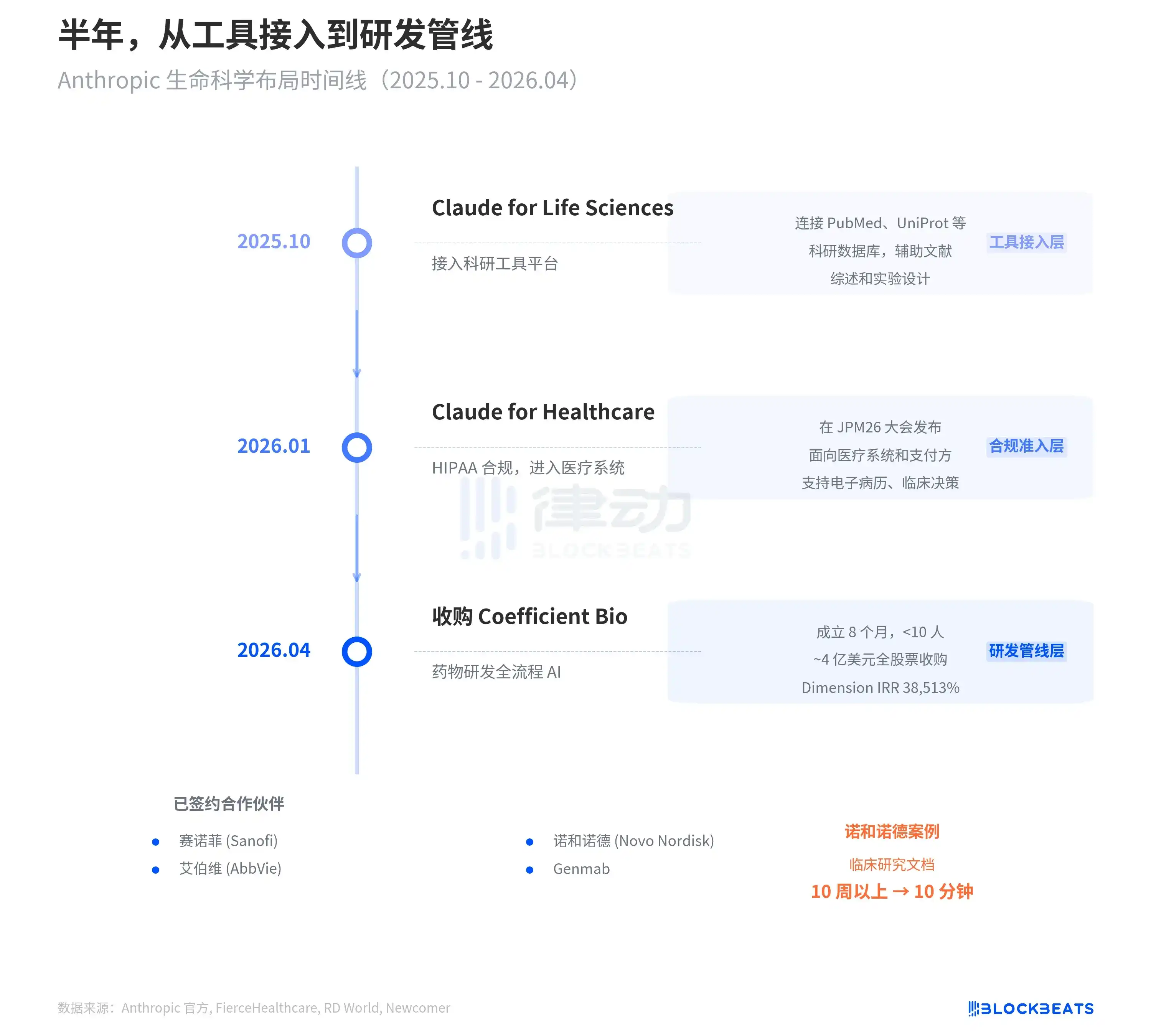

In October 2025, Anthropic launched Claude for Life Sciences, integrating with research databases like PubMed and UniProt, enabling Claude to assist with literature reviews and experimental design. In January 2026, at the JPM26 conference, it launched Claude for Healthcare, obtained HIPAA compliance certification, and formally entered the healthcare system. On April 2, it acquired Coefficient Bio, gaining full-cycle AI capabilities for drug R&D.

In six months, it progressed from the tool integration layer to the compliance access layer, and then to the R&D pipeline layer. According to Newcomer, Coefficient Bio was founded just 8 months ago, has fewer than 10 employees, and is about 50% owned by venture capital firm Dimension. Anthropic completed the acquisition for approximately $400 million in stock. Dimension stated in a letter to LPs that the IRR on this investment reached 38,513%.

This number itself shows that Anthropic is not buying a company's revenue or product, but rather a team plus an industry entry point. According to reports from Anthropic and RD World, pharmaceutical companies like Sanofi, Novo Nordisk, AbbVie, and Genmab are already using Claude's life science tools. The Novo Nordisk case is particularly typical, reducing clinical study document processing time from over 10 weeks to 10 minutes.

Two Balance Sheets, One Countdown

According to WinBuzzer and The Tech Portal, Anthropic has hired Goldman Sachs and J.P. Morgan to lead underwriting, targeting an IPO as early as October 2026 with a financing scale exceeding $60 billion. OpenAI is targeting Q4 2026 or Q1 2027 with a valuation nearing $1 trillion. According to Tom Tunguz's analysis, if OpenAI, Anthropic, and SpaceX all IPO in the same year, these three alone could absorb over $3 trillion in market liquidity.

Both are making final strategic adjustments before their IPOs. According to CNBC, OpenAI CEO Fidji Simo internally announced the cancellation of Sora, the Atlas browser, hardware projects, and instant checkout features, stating the company is "like entering a red alert" and needs to focus on enterprise and agent products. Anthropic's path is to continue deepening into vertical industries like life sciences, using industry switching costs to lock in enterprise customers.

According to FinancialContent, the OpenAI board is concerned that if Anthropic goes public first, it will siphon off the retail investment enthusiasm that has been building up for AI. The valuations of the two companies differ by more than 2 times, but they are competing for the same pool of investors' money. Two acquisitions on the same day: one buying a narrative machine, the other buying an industry entry point.