In the third chapter of the "Part 1" article, we focused on analyzing projects like Synthetix, Gains Network, and Ostium. This article will build upon the previous text, further expanding to other representative case studies.

Three. Representative Projects and Architectural Game Theory: Oracle Pricing + Liquidity Pool (Pool based + Oracle pricing) vs. Order Book (Order book)

3.3 Orderbook Representative: Hyperliquid HIP-3 Ecosystem

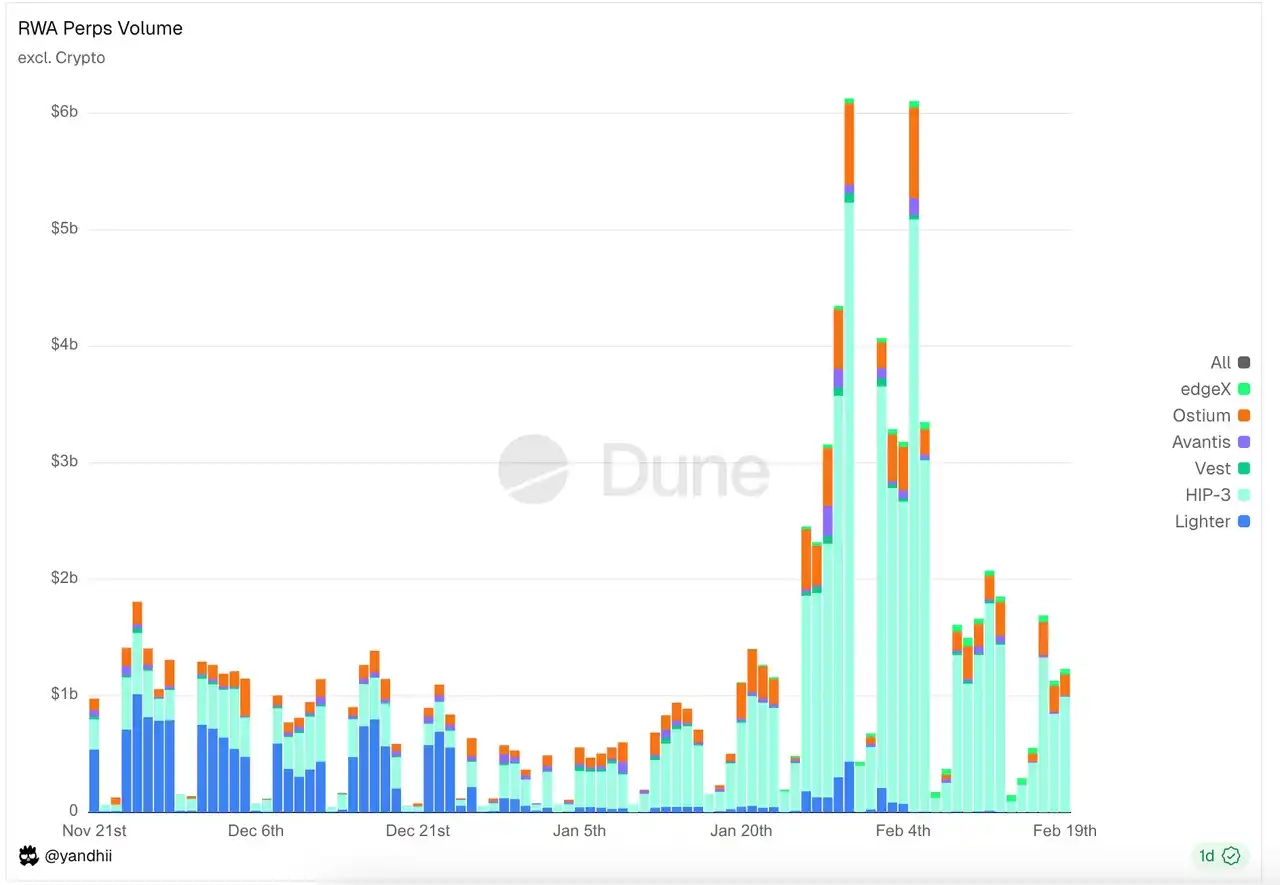

Within the order book (Orderbook) track, the Hyperliquid HIP-3 ecosystem accounts for the vast majority of trading volume and open interest. Outside the Hyperliquid ecosystem, platforms like Lighter and Vest Markets are also launching competition.

Data Source: https://dune.com/yandhii/rwa-perps

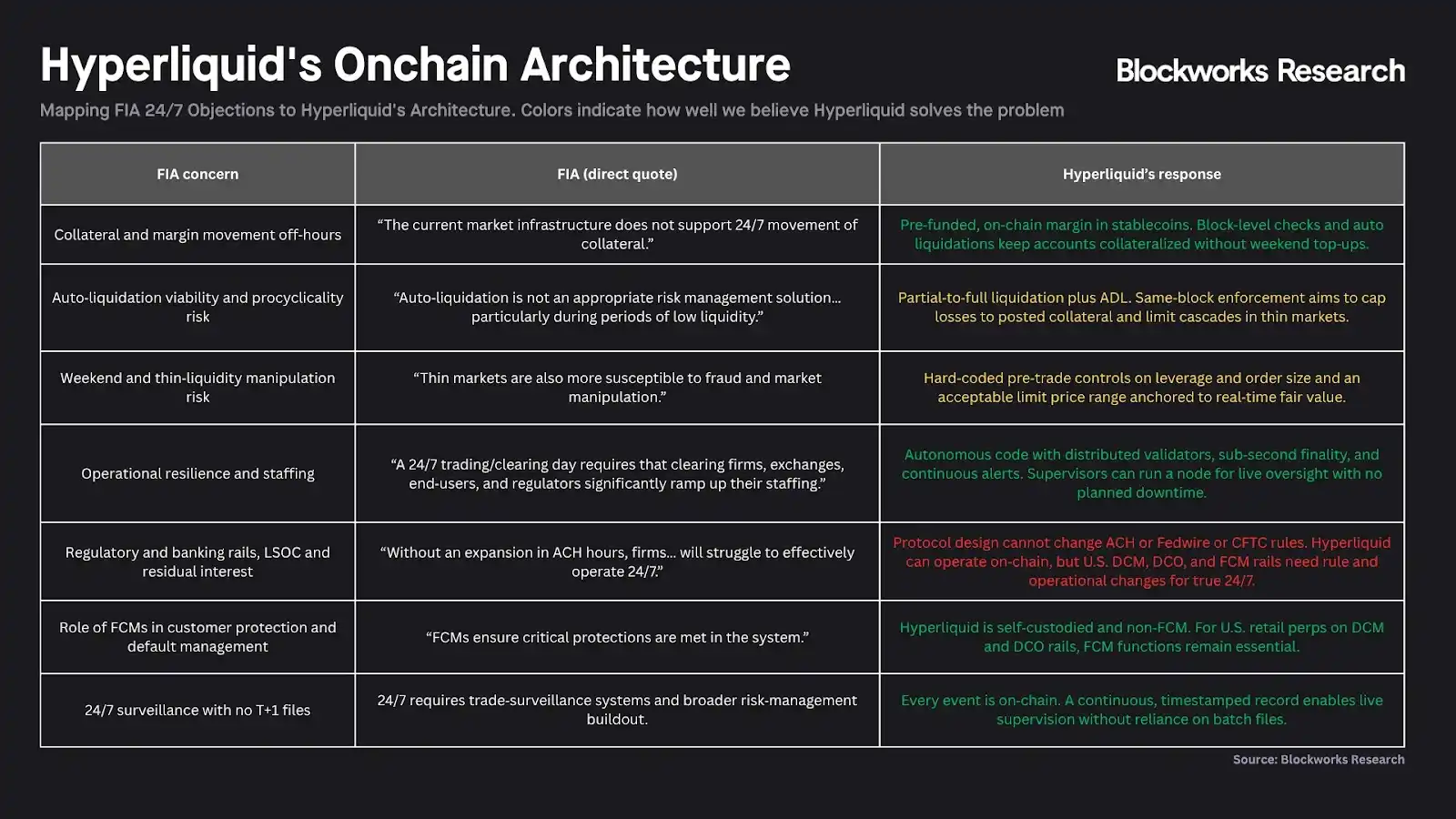

Hyperliquid & HIP-3: Decentralized Nasdaq Infrastructure

Through the HIP-3 upgrade, Hyperliquid has completed its strategic transformation from a single perpetual contract exchange to a "high-performance clearing and matching infrastructure layer." Its core vision is to separate the functions of the DCM (Designated Contract Market) and DCO (Derivatives Clearing Organization) from traditional finance on-chain. In this architecture, the Hyperliquid chain itself plays the role of a unified DCO, providing the underlying matching engine, risk control, and fund settlement; while third-party teams act as "Deployers," taking on the DCM role, responsible for front-end customer acquisition, market operations, and asset listing. This layered design aims to create a "decentralized Nasdaq," carrying perpetual trading of various assets through a unified settlement layer.

Figure: The above diagram summarizes how Hyperliquid hopes to become "a more open, transparent, and efficient financial system" in response to CFTC's skepticism about perpetual contracts and 24/7 trading. For example: Replacing the traditional DCO's reliance on the banking system with a 24/7 automatic clearing protocol, eliminating bloated FCM intermediaries through non-custodial technology, and reconstructing DCM regulatory logic using real-time on-chain data illustrate how blockchain technology can directly leapfrog the physical time differences and efficiency bottlenecks of traditional finance.

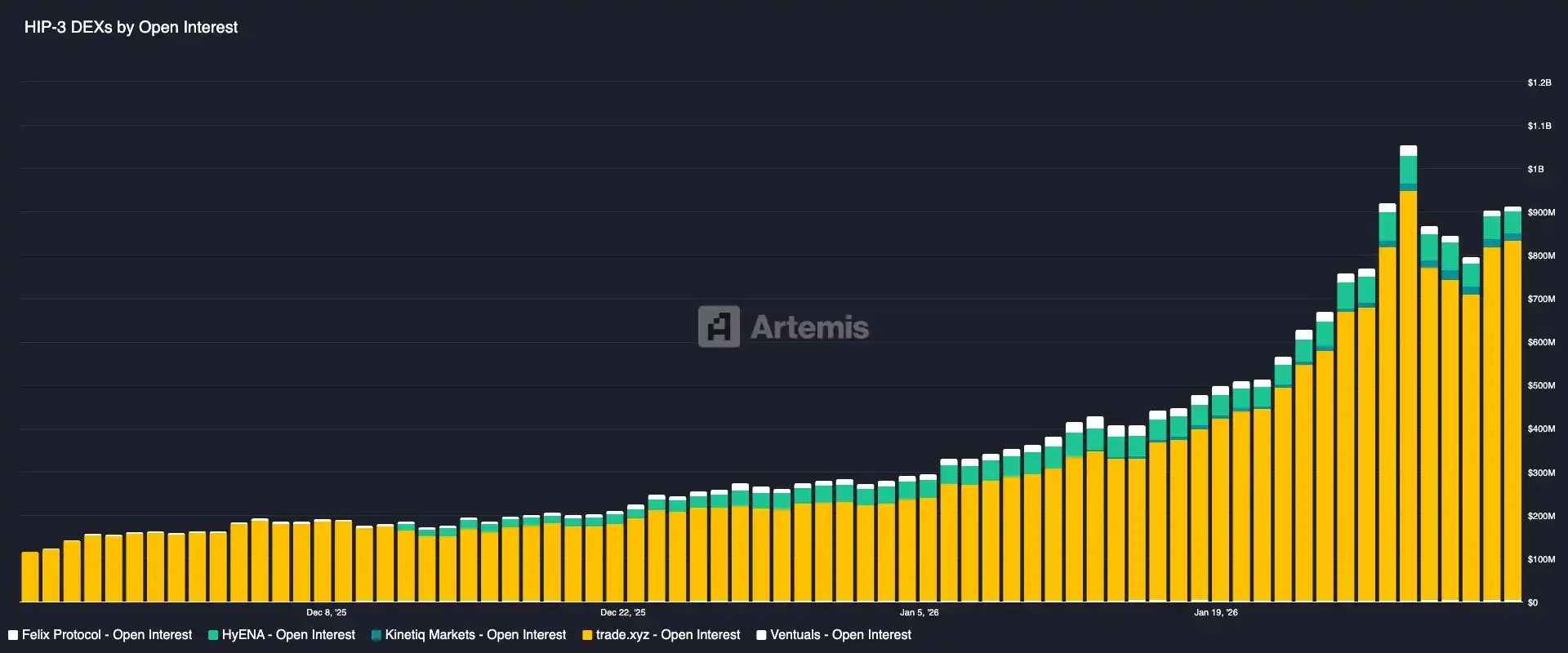

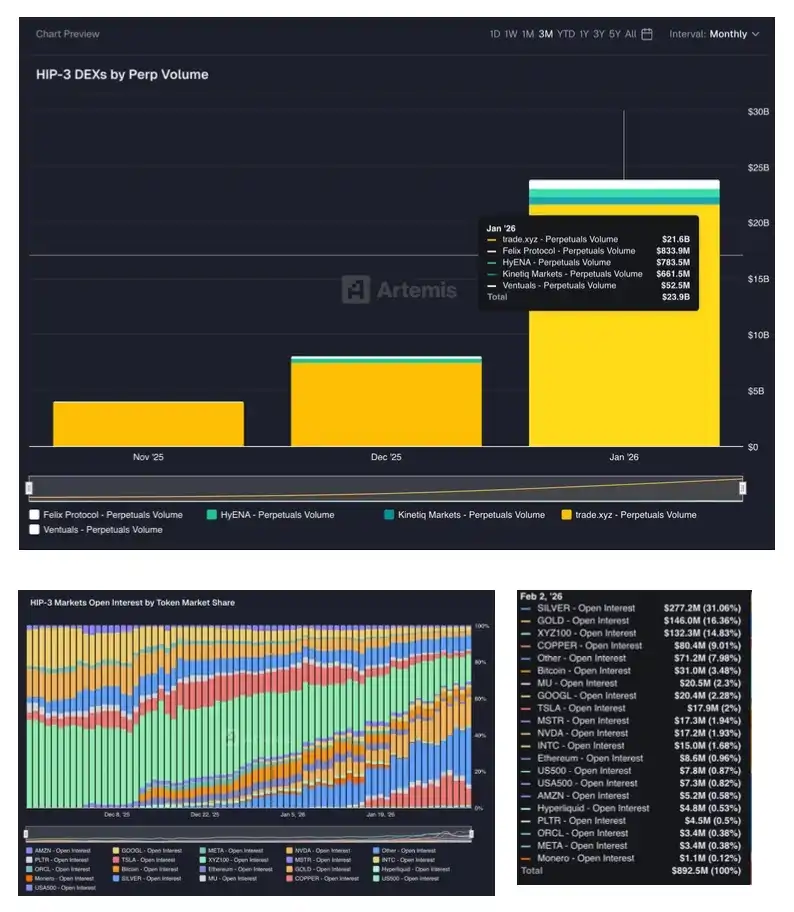

HIP-3 Ecosystem RWA Perps Projects

Project Overview

- Trade.xyz, built by the asset layer team HyperUnit, an official partner of Hyperliquid, was the first to launch the XYZ100 perpetual contract tracking the Nasdaq 100 index and several leading US tech stocks. With rich asset bridging (supporting cross-chain liquidity injection of mainstream assets like BTC, ETH, SOL through HyperUnit), Trade.xyz currently leads in trading volume among all HIP-3 perpetual exchanges, contributing about 90% of the total market volume.

- Markets.xyz is an RWA Perps Dex launched by the team behind Kinetiq, a Liquid Staking project on Hyperliquid. Markets has a slightly different focus from Trade: it concentrates on indices and has launched various index/macro perpetual contracts (covering S&P 500, US tech indices, Euro, US Treasury indices, energy indices, etc.). Another differentiator is its use of USDH as the margin quote currency, significantly reducing trading fees and increasing rebates to compete with Trade on cost (USDH is a native stablecoin issued by the Native Markets team on Hyperliquid, offering fee waivers and rebate campaigns to compete with the asset cross-chain project Unit on distribution).

- Felix started as a lending and stablecoin protocol on Hyperliquid, issuing the synthetic dollar feUSD through CDP and providing the "Felix Vanilla" matching lending market. After the launch of HIP-3, Felix expanded its business scope to become one of the HIP-3 perpetual market deployers. Felix's settlement currency also uses the USDH stablecoin.

- Dreamcash is a mobile-focused product incubated and developed by Beam, positioning itself as a mobile trading terminal for RWA perpetual contracts.

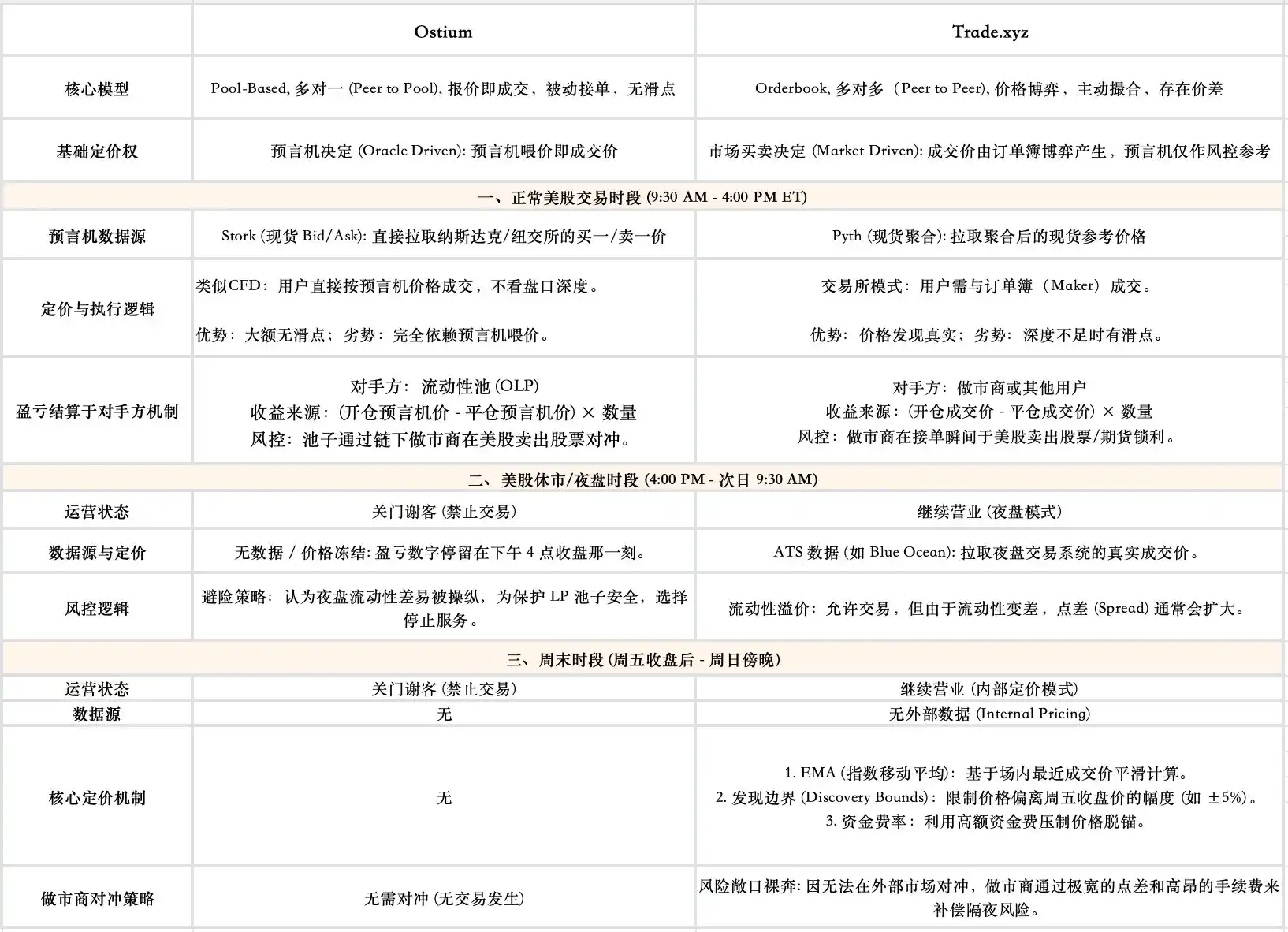

Core Pricing Mechanism: Market-Driven Pricing + Oracle Risk Control

For 24/7 RWA Perps projects built on the Orderbook model, the core technical challenge is how to provide a fair and robust price when the underlying asset's market is closed. Taking Trade, the leading project in the HIP-3 ecosystem in this field, as an example, its core design lies in a dual-track mechanism of market pricing and oracle risk control.

- Core of Price Discovery: Determined by the Market, Not the Oracle

Unlike Pool-based models that directly use oracle quotes as the transaction price, Trade's transaction price is entirely generated by the博弈 (game theory/competition) between buyers and sellers on its order book. The oracle here does not act as a "pricer" but as a "referee"; the price it provides is primarily used for risk control.

- Mark Price: Used to calculate user position profits/losses and determine liquidation

The system's P&L calculation, funding rate, and forced liquidation do not use the instantaneous transaction price but rely on a more robust mark price. Trade's mark price is generated by taking the median of the following three components: the oracle price, a long-term deviation moving average, and the immediate order book price. This design aims to smooth out noise and prevent malicious manipulation, ensuring users' accounts are not liquidated erroneously due to flash crashes on the order book.

- Oracle Data Source Switching for 24/7 Operation: To operate around the clock, the oracle's data source seamlessly switches based on US stock trading hours: it references external oracles like Pyth during normal trading hours; it references after-hours trading prices provided by ATS (Alternative Trading Systems, like Blue Ocean) during night sessions; it activates an internal pricing model during weekend market closures.

3.4 Ostium vs Trade Pricing Logic and Oracle Role Comparison

Ostium chose stronger security and price accuracy, sacrificing some availability (unavailable on weekends). Trade chose availability and博弈性 (speculative nature/game theory), sacrificing some price stability (may depeg or have high funding rate volatility on weekends). The role of the oracle also differs significantly between these two models: in Ostium's Pool-based model, the oracle is the pricer (determines the transaction), while in Trade, the oracle is the referee (only influences funding rates and decides liquidation, not how the transaction occurs).

Chapter Four RWA Perps Regulatory Constraints Analysis

4.1 Core Logic of US Derivatives Regulation: Underlying Asset Classification Determines Compliance Path

Within the US financial regulatory system, the first step in determining whether a derivative can be listed and how it is listed is to ascertain the legal attribute of its underlying asset. This directly determines the jurisdiction of regulatory authority and, consequently, the type of license the exchange must obtain.

For assets like gold, silver, foreign exchange (FX), and Bitcoin, US law defines them as "commodities." Perpetual contracts based on such assets fall under the category of commodity futures, and their regulatory path is relatively singular and clear: they fall entirely under the jurisdiction of the Commodity Futures Trading Commission (CFTC). Exchanges only need to register as a Designated Contract Market (DCM) and connect to a Derivatives Clearing Organization (DCO) to conduct business.

However, once the underlying asset of a perpetual contract becomes a single stock or a narrow-based security index, the situation changes fundamentally: Derivatives involving single securities or a small basket of securities must be jointly regulated by the SEC and the CFTC.

The requirement for joint regulation by the SEC and the CFTC is the primary reason why there are currently no compliant single-stock perpetual contracts in the US market. The background of this regulation dates back to a jurisdictional turf war between the SEC and the CFTC in the 1980s: the two agencies battled over the regulation of newly emerging stock futures contracts. The ultimate solution to this dispute was the Shad-Johnson Agreement signed in 1982, which, in an almost "one-size-fits-all" manner, directly prohibited the trading of single-stock futures and narrow-based stock index futures on US exchanges. The ban's original intention was to avoid continued friction between the agencies. Although the Commodity Futures Modernization Act (CFMA) of 2000 amended this ban, allowing such contracts to be traded in the market as "Security Futures Products," the attached conditions were extremely stringent: the product had to be dually regulated by both the SEC and the CFTC. This became the fundamental legal obstacle hindering innovation in equity-based derivatives.

Any platform wishing to offer single-stock perpetual contracts to US retail clients cannot hold just a single license but must complete the following two registrations simultaneously:

- Register with the CFTC as a Designated Contract Market (DCM) or Swap Execution Facility (SEF)

- Register with the SEC as a National Securities Exchange

This means the platform must simultaneously meet two sets of compliance standards, formulated by different agencies, which may conflict in areas like margin calculation, information disclosure, and trade reporting. This extremely high compliance threshold and operational cost effectively constitute an "entry ban" for single-stock perpetual contracts, resulting in the current near absence of such compliant retail products in the US.

4.2 Exchange Architecture Conflict: Why Compliance Migration Costs Are Extremely High

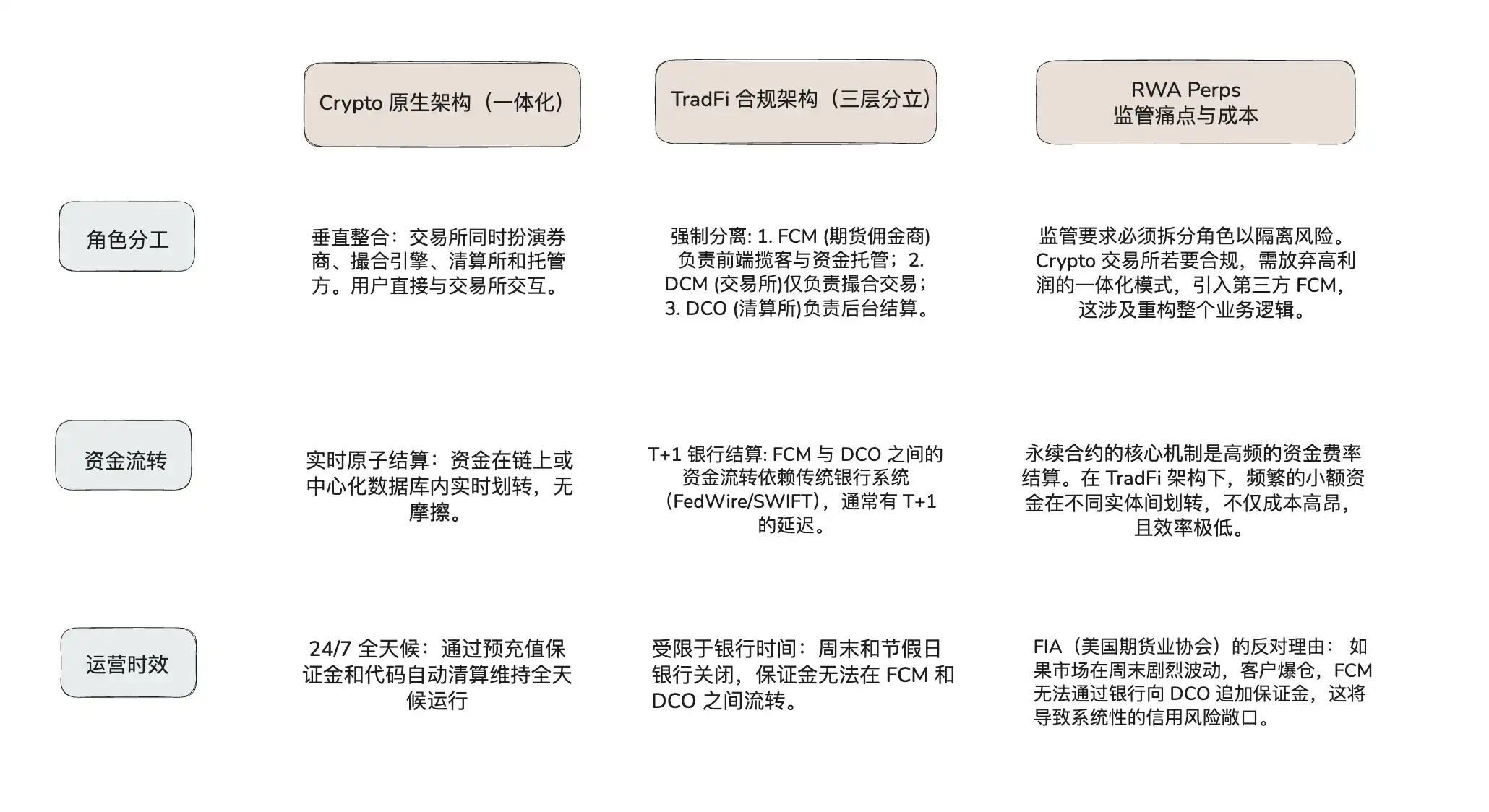

If US exchanges like Coinbase or Robinhood genuinely wanted to launch Equity Perps products, besides facing the difficulty of obtaining the aforementioned legal licenses, they would also need to address the conflict in underlying infrastructure architecture.

Cryptocurrency exchanges普遍 (generally) adopt a "vertically integrated" monolithic architecture, while US regulations require a risk-segregated "three-tier分立 (separated)" architecture. If a crypto exchange wants to become compliant, it must dismantle its existing efficient tech stack to adapt to traditional finance's clearing processes.

Crypto vs. TradFi Market Architecture Comparative Analysis:

Therefore, for US exchanges to launch Equity Perps, they not only need to solve the legal issue of "dual licensing" but also need to resolve the physical contradiction between the "24/7 trading demand" and the "non-24/7 banking settlement system." This infrastructure mismatch is currently the biggest sticking point.

4.3 Window of Opportunity for Offshore Markets: Regulation S

Due to the regulatory restrictions in the US being difficult to overcome in the short term, the vast majority of single-stock perpetual contract liquidity is squeezed into offshore markets. Offshore exchanges (serving non-US clients) typically rely on the exemption provided by Regulation S under US securities law. The core logic of this regulation is: as long as the issuance and sale of the security product occur entirely outside the United States, and the issuer does not engage in Directed Selling Efforts targeting US persons, registration with the SEC is not required. This requires platforms to technically implement strict geo-fencing to block US IPs and explicitly prohibit US users in their legal terms.

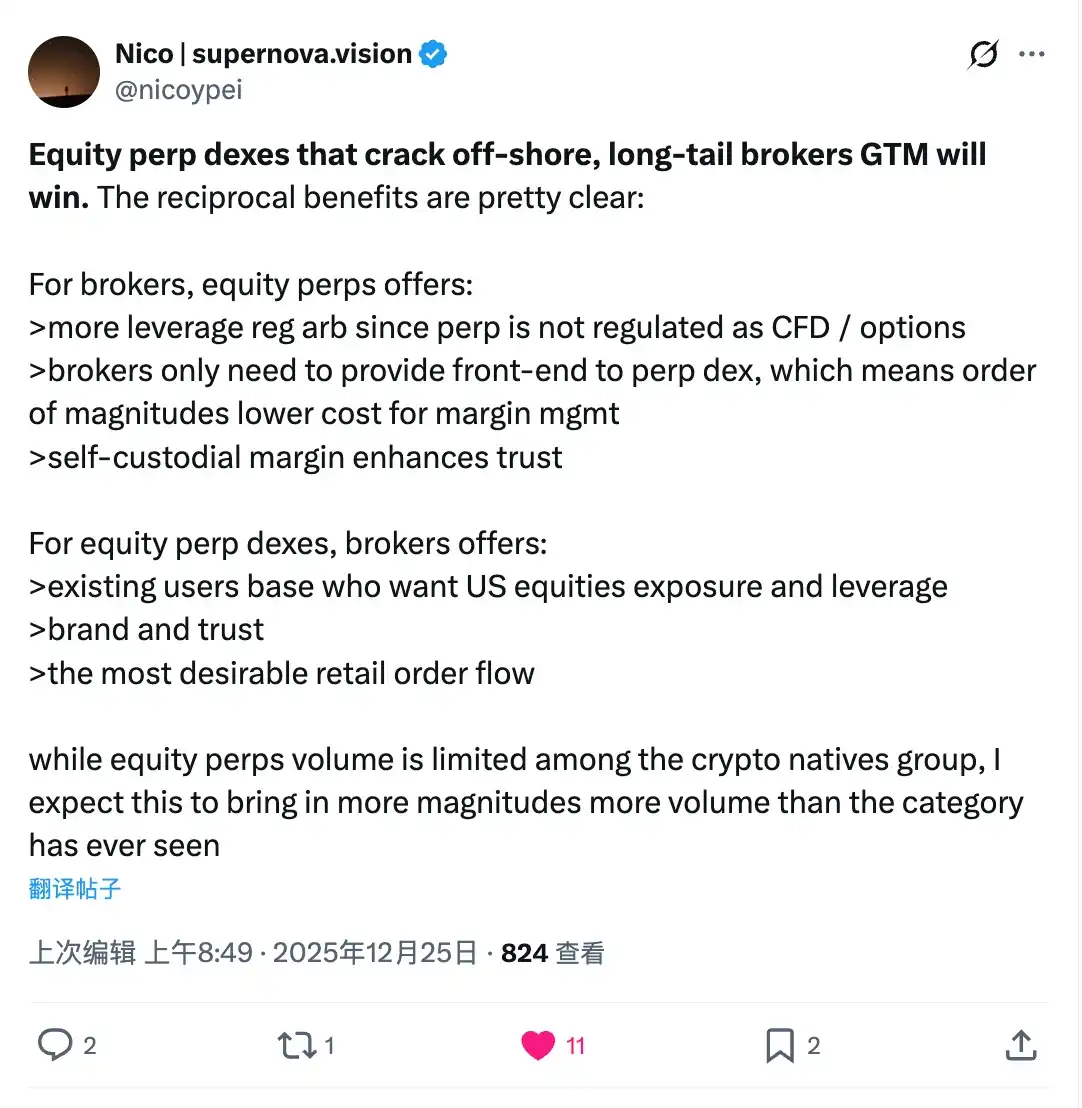

Against this backdrop, RWA Perps Dexes are facing a unique market window of opportunity. They have the chance to establish a mutually beneficial distribution model by cooperating with traditional long-tail brokers in offshore regions:

CFD Broker + RWA Perps Dex Mutual Benefit Model: This cooperation could be attractive to traditional brokers. Compared to the traditional CFD business, which faces increasingly tight regulation (e.g., EU ESMA leverage restrictions), on-chain perpetual contracts often reside in a regulatory grey area, potentially offering higher leverage. More importantly, brokers only need to maintain front-end user relationships, outsourcing the complex margin management, clearing, and hedging risks to the on-chain protocol (back-end), significantly reducing their middle and back-office operational costs. Simultaneously, the self-custody nature of DEXs solves the user trust issue regarding fund misappropriation by small and medium-sized brokers.

For Equity Perps Dexes, this model solves the most棘手 (thorny) customer acquisition problem. Crypto-native users have relatively limited interest in US stock trading, while traditional brokers hold a large amount of real retail流量 (traffic/flow) seeking exposure to US stocks. By embedding themselves as a technical back-end into brokers, DEXes can maintain technological neutrality while having compliant brokers handle KYC/AML processes on the front-end, potentially breaking through the original DeFi world to achieve scaled growth.

4.4 Potential Legal Risks

Although the offshore and DeFi models are commercially sound, one must also be wary of the "long-arm jurisdiction" risk from US regulators. If an offshore protocol cannot completely sever ties with US users at the technical and compliance levels (e.g., through front-end checks or IP blocking), or if its commercial activities are deemed to involve the US market, it could still face severe regulatory penalties.

Chapter Five External Variable: The Dual Impact of NYSE's 24/7 Plan

The news that NYSE's parent company, ICE, plans to launch a 7x24 hour trading market constitutes the largest external variable for the RWA perpetual contracts赛道 (sector/track). If this change materializes, it will have a profound dual impact on DeFi. If users can trade Tesla stock legally and safely 7x24 on a regulated platform like the NYSE or Interactive Brokers, the "all-day trading" advantage that DeFi protocols rely on for survival could be somewhat diminished. At that point, DeFi may need to find new value propositions, such as higher leverage rates, permissionless access mechanisms, or complex financial products built on composability, to survive direct competition with traditional financial giants.

Core Motivation and Mechanism Innovation: From "T+2" to "On-Chain 24/7"

The 24/7 trading platform planned by the NYSE aims to utilize blockchain technology to achieve tokenized trading of US stocks and ETFs. Its core innovation lies in using stablecoin deposits, instant clearing and settlement (T+0), and multi-chain custody to彻底 (thoroughly) break the drawbacks of the traditional stock market's "separation of trading and settlement," eliminating settlement risks exposed in events like GameStop. This move is a strategic defense by the NYSE against competition from peers like Nasdaq and to meet global capital's demand for all-weather liquidity. It marks traditional exchanges evolving from "electronic order books" to "comprehensive on-chain infrastructure," attempting to merge the efficiency advantages of DeFi under the highest regulatory standards.

Catalysis and Challenge for the RWA Ecosystem: The End of the Liquidity Bottleneck

NYSE's entry provides top-level endorsement for RWA tokenization, solving the "liquidity drought" and "pricing disconnect" caused by traditional market weekend closures for on-chain assets. For the RWA perpetual contracts market, a 24/7 spot price feed will significantly reduce arbitrage costs and funding rate volatility, improving market depth. Although NYSE's compliant "walled garden" model may squeeze the生存空间 (living space) of some non-compliant, synthetic asset-type projects, it also points the way for compliant stablecoins and clearing facilities. Crypto-native RWA projects need to use the window of opportunity before its expected 2026 launch to establish differentiated positioning (e.g., higher leverage, no门槛 (threshold), cross-protocol interoperability) to complement or compete with traditional giants.

Future Landscape Outlook: Deep Integration of Traditional and Crypto Finance

Although there are concerns within the crypto community about the investment pressure and regulatory surveillance brought by "24/7 all-day monitoring," the trend of finance moving on-chain is irreversible. In the medium to long term, the intervention of traditional giants will reshape the value chain, forcing intermediaries like brokers and custodian banks to transform. The future market will evolve into a coexisting ecosystem of competition and cooperation: compliant platforms like NYSE will provide highly credible underlying spot liquidity, while DeFi protocols will continue to leverage flexibility in innovative derivatives and global asset allocation. As the boundaries between crypto and traditional assets blur, the global capital market will enter a new era driven by AI, real-time pricing, and atomic settlement.

Summary

- Structural Upgrade of Delta One (Linear Derivative) Demand. Currently, retail traders often rely on inefficient trading tools when seeking directional leverage. US 0DTE (zero days to expiration) options subject pure directional bets to unnecessary Theta (time value) decay; while the massive offshore CFD (Contract for Difference) market, worth $30 trillion, suffers from issues like broker opacity and counterparty risk. RWA perpetual contracts completely strip away time decay and centralized risk, providing a transparent, mathematically linear on-chain alternative for this tangible market demand.

- Architectural Trade-offs in Asynchronous Markets. Connecting 24/7 crypto infrastructure with traditional markets bound by physical trading hours forces protocols to compromise between high leverage, continuous trading, and externalized risk. To cope with traditional market closures, two distinct models have currently evolved: Ostium's actively hedged liquidity pool prioritizes solvency, eliminating gap risk entirely by pausing trading during closures; while Trade.xyz (based on Hyperliquid) maintains 24/7 uninterrupted trading by transforming weekend volatility risk into dynamic funding rates and market maker spreads.

- Offshore Distribution Strategy. Facing dual jurisdiction from the SEC and CFTC, launching compliant single-stock perpetual contracts for retail domestically in the US is currently unrealistic. Therefore, the early core growth engine for RWA Perps will rely on markets outside the US (via Regulation S exemptions). In terms of distribution, RWA Perps Dexes may explore cooperation models with traditional CFD brokers in the future,无需 (not needing to) acquire retail users directly on the front end but acting as the "back-end clearing engine" for regional offshore brokers to achieve scaled expansion—outsourcing KYC and front-end acquisition to traditional financial entities while focusing on margin management and atomic settlement on-chain.

- Traditional Financial Infrastructure Adapting to 24/7. Traditional institutions like the New York Stock Exchange (NYSE) are advancing plans for continuous trading of US stocks, which could soon break DeFi's monopoly on "all-day trading." Although this change could彻底消除 (completely eliminate) weekend gap risk for on-chain protocols, it also forces DeFi to diversify its competitive strategies. In the long run, RWA perpetual contracts must establish differentiated advantages in permissionless access, capital efficiency, and higher leverage rates, eventually evolving into a "high-speed execution layer" built on top of regulated traditional spot markets.

Looking ahead, RWA Perps is not just a shadow market对标 (benchmarked against) Nasdaq or CME; it is more fundamentally a底层重构 (underlying restructuring) of pricing power, global liquidity distribution, and risk transfer mechanisms. As liquidity facilities improve, it will become the optimal承载容器 (carrying vessel) for global leverage demand flowing on-chain.