This report is authored by Tiger Research. In 2025, the U.S. government is pursuing a policy supportive of cryptocurrency, with a clear and concise goal: to have the existing cryptocurrency industry operate under the same regulatory framework as the traditional financial sector.

Key Takeaways

- The U.S. is working to integrate cryptocurrency into its existing financial infrastructure, rather than simply absorbing the entire industry.

- Over the past year, Congress, the Securities and Exchange Commission (SEC), and the Commodity Futures Trading Commission (CFTC) have introduced and adjusted rules to gradually bring cryptocurrency into this system.

- Despite tensions among regulators, the U.S. continues to refine the regulatory framework while supporting industry growth.

1. The U.S. Absorption of the Cryptocurrency Industry

Following President Trump's re-election, the administration launched a series of aggressive pro-cryptocurrency policies. This marks a sharp turn from previous stances—where the cryptocurrency industry was primarily seen as an object of regulation and control. The U.S. has entered a once-unimaginable phase, absorbing the cryptocurrency industry into its existing system at a pace approaching unilateral decision-making.

Shifts in the positions of the SEC and CFTC, along with traditional financial institutions increasingly engaging in cryptocurrency-related businesses, signal that broad structural changes are underway.

Notably, all this has occurred just one year since President Trump's re-election. What specific changes have taken place in U.S. regulation and policy so far?

2. A Year of Change in the U.S. Cryptocurrency Stance

In 2025, with the Trump administration taking office, U.S. cryptocurrency policy reached a major turning point. The executive branch, Congress, and regulatory agencies acted in concert, focusing on reducing market uncertainty and integrating cryptocurrency into the existing financial infrastructure.

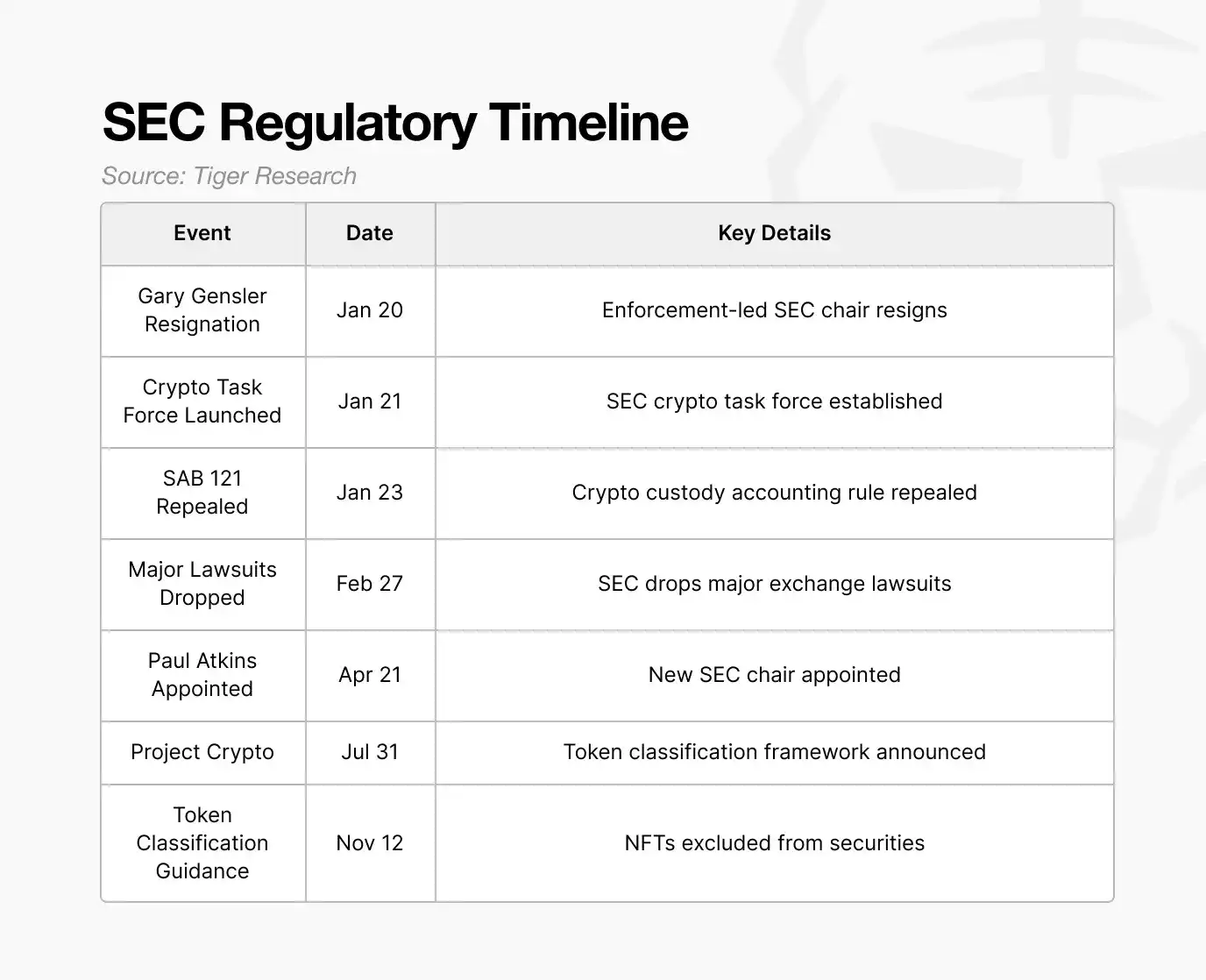

2.1. The Securities and Exchange Commission (SEC)

Previously, the SEC primarily relied on enforcement actions to address cryptocurrency-related activities. In major cases involving Ripple, Coinbase, Binance, and Kraken's staking services, the SEC filed lawsuits without providing clear standards for the legal attributes of tokens or which activities were permitted, often interpreting rules after the fact. This led cryptocurrency companies to focus more on managing regulatory risks than on business expansion.

This stance began to change after the resignation of Chairman Gary Gensler, who held a conservative view of the cryptocurrency industry. Under the leadership of Paul Atkins, the SEC shifted to a more open approach, beginning to build foundational rules aimed at bringing the cryptocurrency industry into the regulatory framework, rather than relying solely on litigation for oversight.

A key example is the announcement of the "Crypto Project." Through this project, the SEC signaled its intent to establish clear standards for determining which tokens are securities and which are not. This once directionless regulator is beginning to reshape itself into a more inclusive agency.

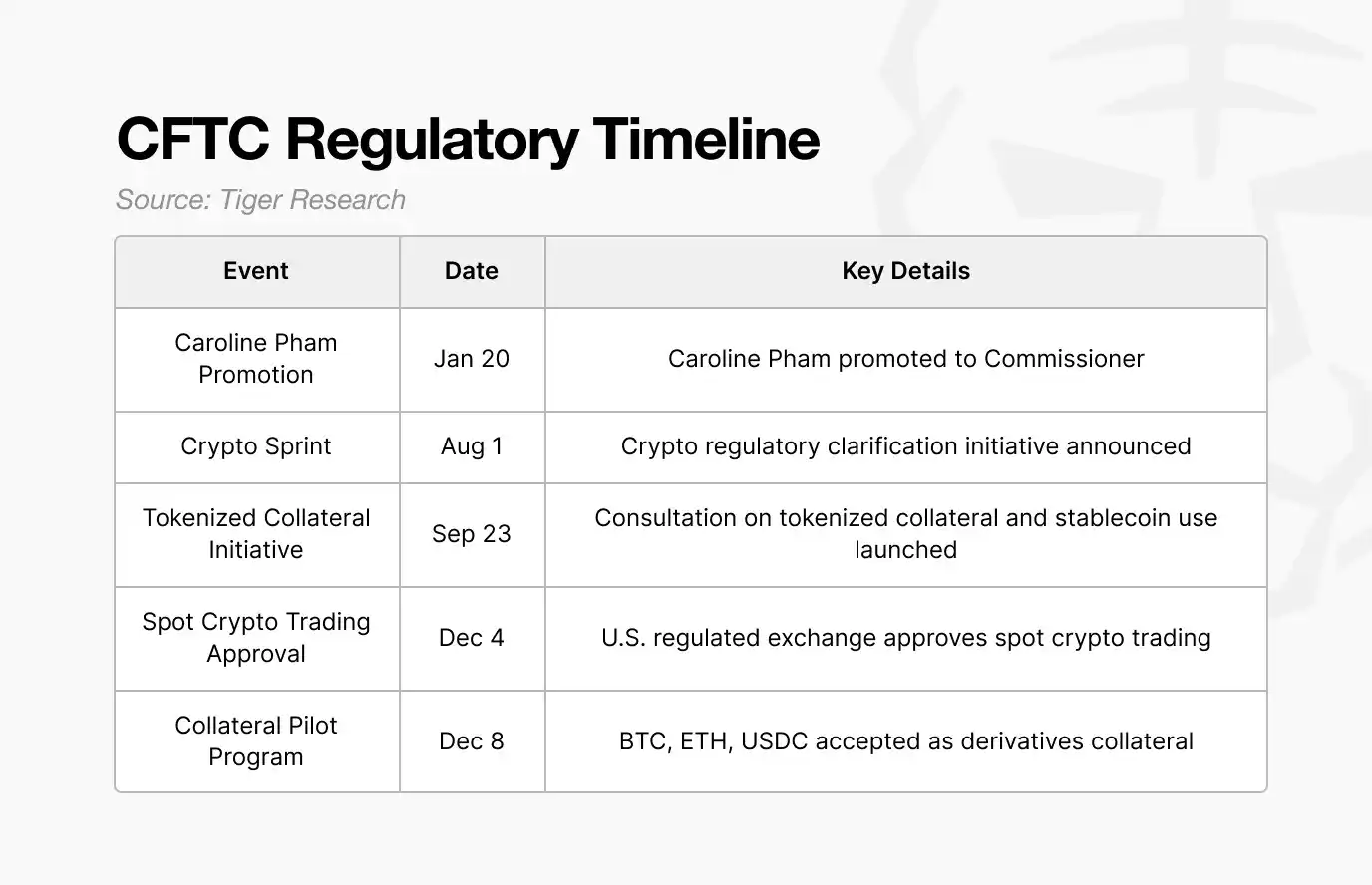

2.2. The Commodity Futures Trading Commission (CFTC)

In the past, the CFTC's involvement with cryptocurrency was largely limited to derivatives market regulation. This year, however, it adopted a more proactive stance, formally recognizing Bitcoin and Ethereum as commodities and supporting their use by traditional institutions.

The "Digital Asset Collateral Pilot Program" is a key initiative. Through this program, Bitcoin, Ethereum, and USDC were approved as collateral for derivatives trading. The CFTC applied haircut ratios and risk management standards, treating these assets in the same manner as traditional collateral.

This shift indicates that the CFTC no longer views crypto assets purely as speculative instruments but has begun to recognize them as stable collateral assets on par with traditional financial assets.

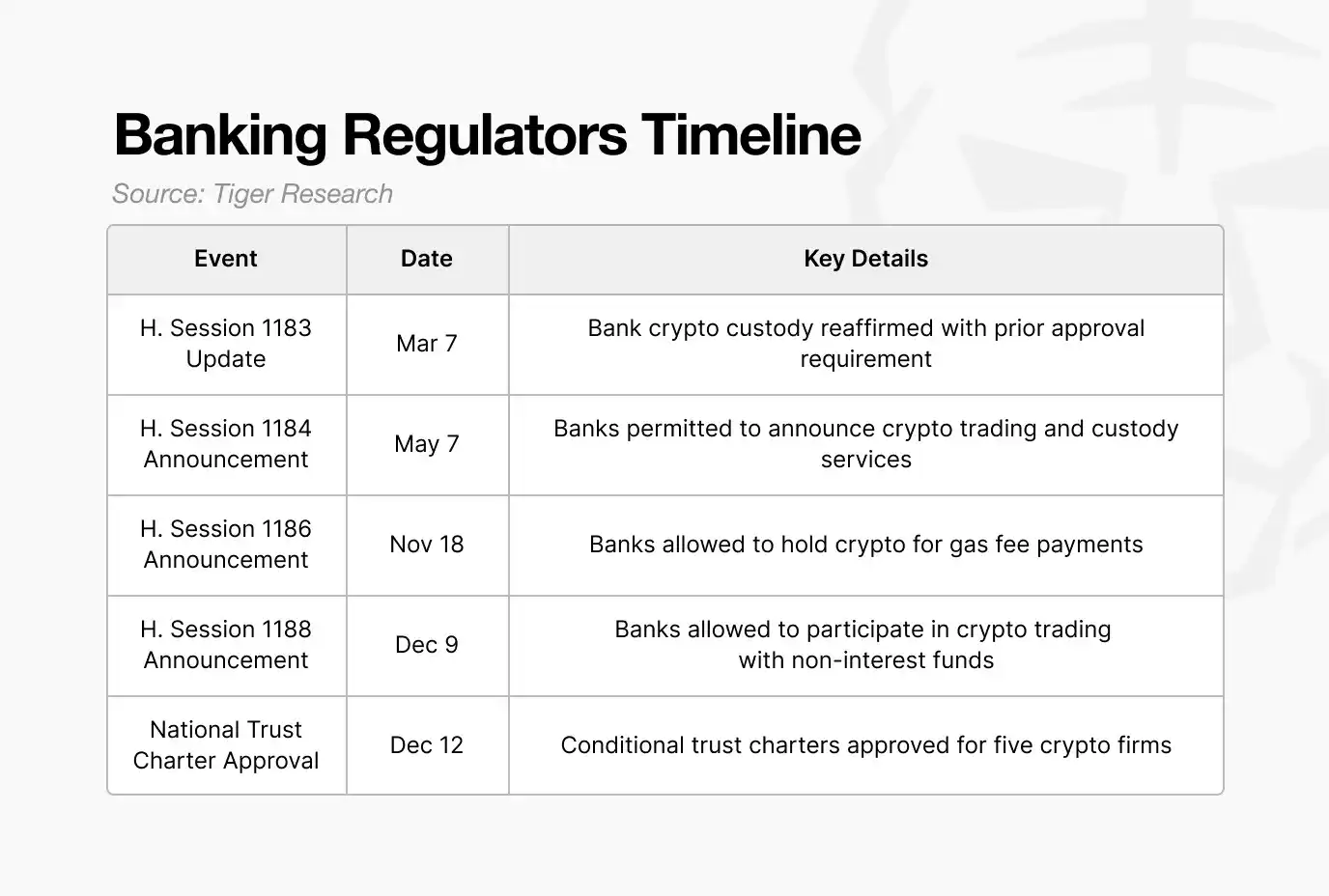

2.3. The Office of the Comptroller of the Currency (OCC)

Previously, the OCC kept its distance from the cryptocurrency industry. Crypto companies had to apply for licenses state by state, making it difficult to enter the federal banking regulatory system. Their business expansion was limited, and structural barriers hindered connections with the traditional financial system, forcing most to operate outside the regulated framework.

This approach has now changed. The OCC has chosen to bring cryptocurrency companies into the existing bank regulatory framework rather than exclude them from the financial system. It issued a series of interpretive letters (formal documents clarifying whether specific financial activities are permitted), gradually expanding the scope of allowed businesses to include crypto asset custody, trading, and even banks paying on-chain transaction fees.

This series of changes culminated in December: the OCC conditionally approved national trust bank charters for major companies like Circle and Ripple. This move is significant because it grants these crypto companies status equal to that of traditional financial institutions. Under single federal oversight, they can operate nationwide, and transfers that previously required intermediary banks can now be handled directly, just like traditional banks.

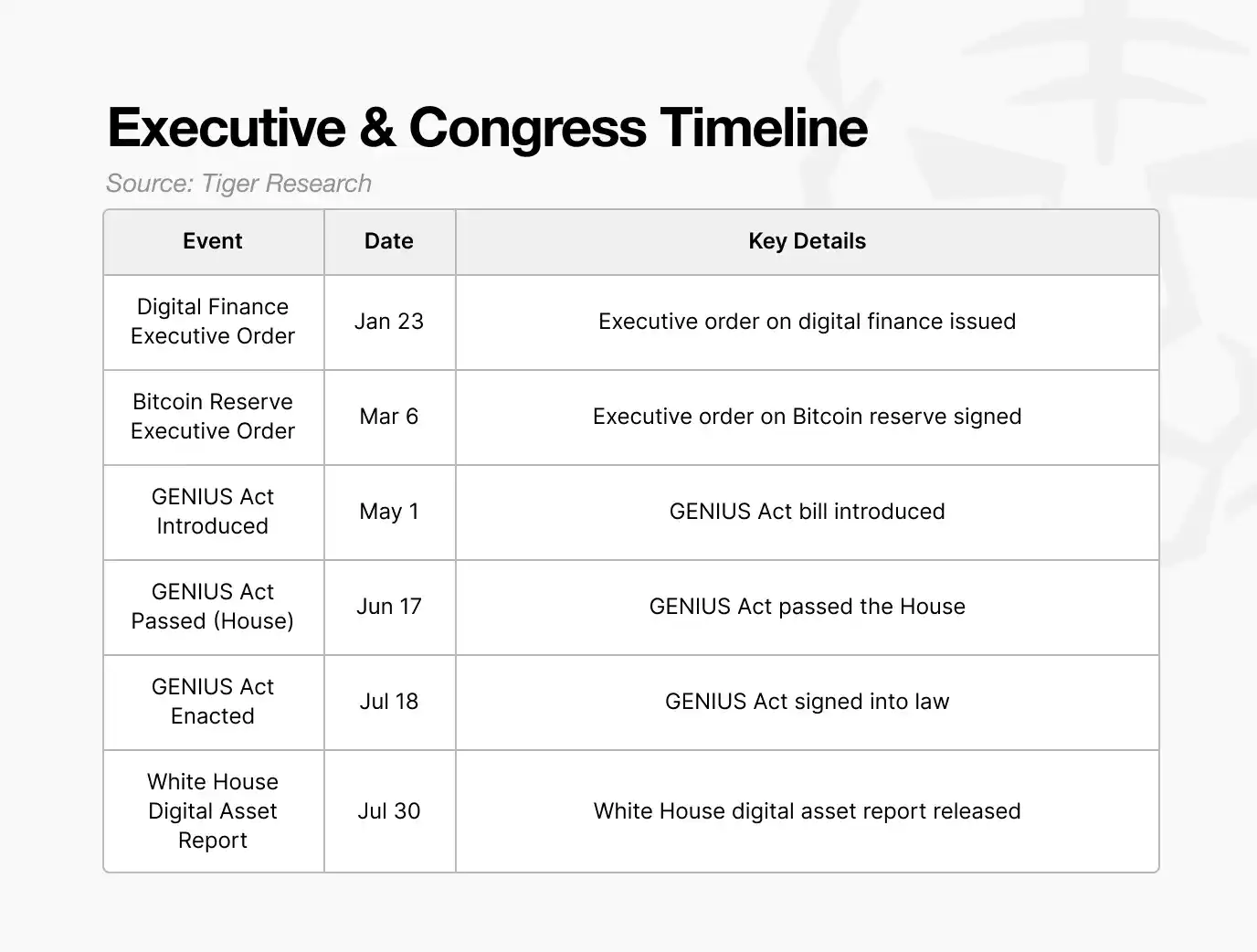

2.4. Legislation and Executive Orders

Previously, although stablecoin legislation had been brewing in the U.S. since 2022, repeated delays created a regulatory vacuum. There was a lack of clear standards regarding reserve composition, regulatory authority, and issuance requirements. Investors could not reliably verify whether issuers held sufficient reserves, raising concerns about the transparency of some issuers' reserves.

The "GENIUS Act" addressed these issues by clearly defining stablecoin issuance requirements and reserve standards. It requires issuers to hold reserves equivalent to 100% of the issued amount, prohibits the re-hypothecation of reserve assets, and consolidates regulatory authority under federal financial regulators.

Thus, stablecoins have become digital dollars with legally recognized payment capabilities.

3. Direction Set, Competition and Checks and Balances Coexist

Over the past year, the direction of U.S. cryptocurrency policy has been clear: to integrate the cryptocurrency industry into the formal financial system. However, this process is not uniform and frictionless.

Divergent views still exist within the U.S. The debate surrounding the privacy-mixing service Tornado Cash is a typical example: the executive branch actively enforces laws to block illicit fund flows, while the SEC chairman publicly warns against excessive suppression of privacy. This indicates that perceptions of cryptocurrency within the U.S. government are not entirely unified.

But these differences do not equate to policy instability; they are more akin to inherent features of the U.S. decision-making system. Agencies with different responsibilities interpret issues from their own perspectives, sometimes publicly disagreeing, moving forward through checks, balances, and persuasion. The tension between strict enforcement and protecting innovation may cause short-term friction, but in the long run, it helps make regulatory standards more specific and precise.

The key is that this tension has not stalled progress. Even amidst debate, the U.S. continues to advance on multiple fronts: the SEC's rulemaking, the CFTC's infrastructure integration, the OCC's institutional absorption, and Congressional legislation establishing standards. It does not wait for complete consensus but allows competition and coordination to proceed simultaneously, driving the system forward continuously.

Ultimately, the U.S. has neither given cryptocurrency free rein nor attempted to suppress its development. Instead, it has simultaneously reshaped regulation, leadership, and market infrastructure. By transforming internal debate and tension into momentum, the U.S. has chosen a strategy to draw the global cryptocurrency industry center towards itself.

Original Source: Tiger Research

The past year has been crucial precisely because this direction has moved beyond declarations and been concretely translated into specific policies and execution.