Original Author: JayZhou 3 Points Blockchain

Original Link:

https://mp.weixin.qq.com/s/G9d8zhrbwUtGpOzNrWXcHg

I. The Background of Kevin Warsh's Career: From Crisis Witness to Policy Critic

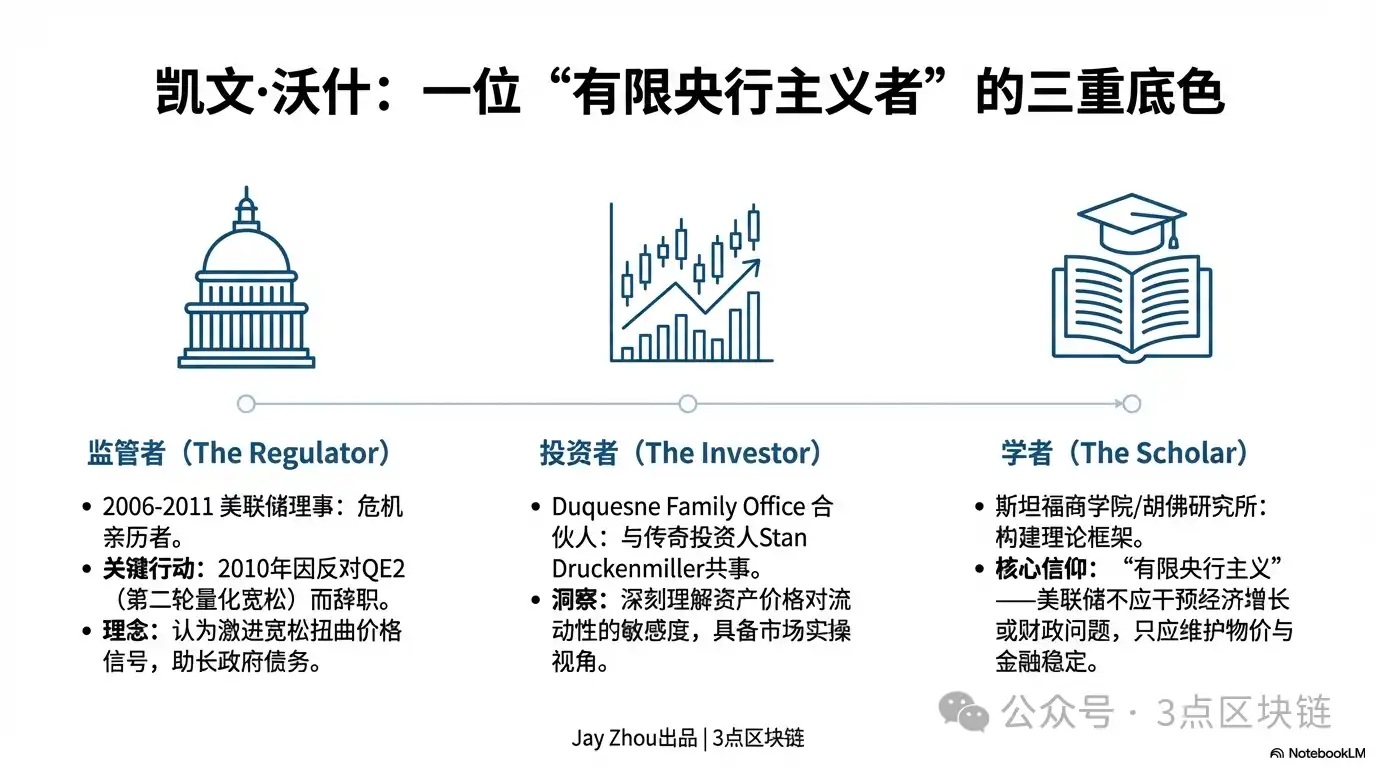

Kevin Warsh's career has always navigated the intersection of public policy and private markets, shaping his critical perspective and pragmatic style on monetary policy. Understanding Warsh's policy stance requires examining his triple identity across regulation, academia, and investment.

1.1 Federal Reserve Governor During the Crisis: The "Defector" from Quantitative Easing

From 2006 to 2011, Warsh served as a Federal Reserve Governor through the entire global financial crisis. During this period, the Fed shifted from traditional interest rate controls to large-scale asset purchase programs (QE), expanding its balance sheet from $900 billion to $2.9 trillion. As the Fed's liaison to the markets, Warsh was deeply involved in crafting crisis response policies but also became one of the first key members to say "no" to quantitative easing.

In 2010, when the Fed was酝酿 the second round of quantitative easing (QE2), Warsh publicly expressed opposition. He believed that with signs of economic revival already apparent, continuing to expand asset purchases would drag the Fed into the political whirlpool of fiscal policy and distort market price signals. After QE2 was officially launched, Warsh chose to resign in protest. This act of "defection" became a defining event of his career.

This experience shaped Warsh's core view of "limited central banking": the Fed's primary responsibility is to maintain price stability and financial stability, not to intervene in economic growth or solve fiscal problems through balance sheet operations. He sharply criticized the Fed's aggressive policies over the past 15 years, arguing that persistent quantitative easing fostered a "monetary dominance" era—artificially low interest rates not only inflated asset bubbles but also fueled the accumulation of U.S. government debt. By 2026, U.S. federal government debt had surpassed $38 trillion, with net interest payments nearly matching defense spending, a situation Warsh had warned would be a consequence of such policies.

1.2 A Multidimensional Perspective from a Crossover Career: From Family Office to Stanford's Podium

After leaving the Fed, Warsh's career entered a "crossover phase." He joined the family office of legendary investor Stan Druckenmiller, Duquesne, as a partner, deeply involved in global macro investment decisions. Simultaneously, as a Distinguished Visiting Fellow at the Hoover Institution and a lecturer at Stanford Graduate School of Business, he built a policy analysis framework combining theory and practice.

This experience spanning regulatory agencies, investment firms, and academia endowed Warsh's policy stance with dual attributes of "top-level design" and "market practice." From a regulator's perspective, he deeply understands the spillover effects of Fed policies on financial markets; from an investor's perspective, he grasps asset price sensitivity to liquidity changes; from a scholar's perspective, he can step back from short-term policy cycles to examine the long-term logic of monetary policy.

Particularly noteworthy is that Warsh's personal network adds a political dimension to his appointment—his father-in-law is Ronald Lauder, head of the Estée Lauder Group and a close friend of Donald Trump. This connection raises market concerns that Warsh might struggle to resist Trump's political pressure, especially the latter's explicit demand for "significant interest rate cuts." However, judging from Warsh's career trajectory, he has always been labeled as an advocate for "policy independence." The interplay between this "political connection" and "policy autonomy" will be a core point to watch once he helms the Fed.

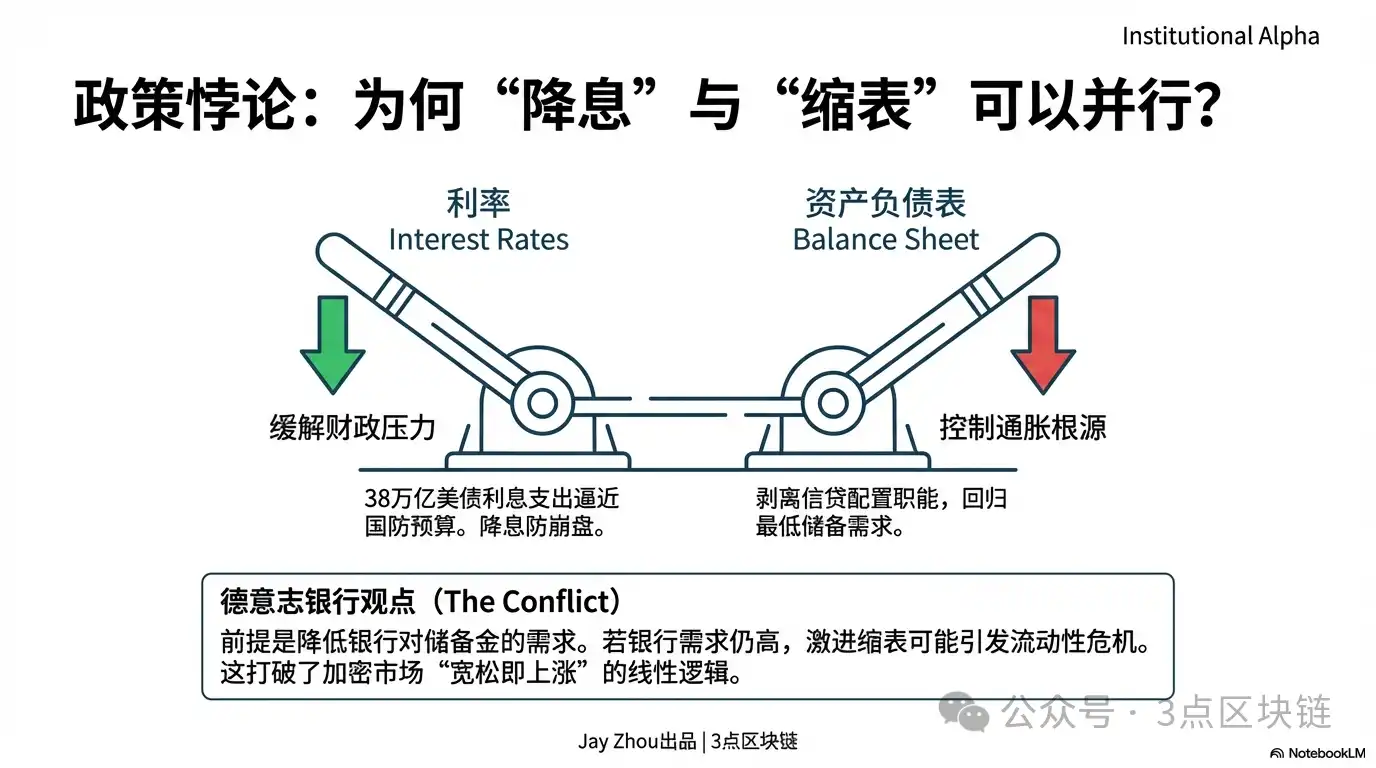

1.3 The Core of Policy Stance: The "Paradoxical" Control of Simultaneous Rate Cuts and Balance Sheet Reduction

A research report by Deutsche Bank's Matthew Luzzetti team accurately summarizes Warsh's policy framework: "rate cuts and balance sheet reduction in parallel." This policy combination seems contradictory but directly addresses the core dilemma facing the Fed—needing to alleviate the pressure of high interest rates on government debt while avoiding a resurgence of inflation triggered by excess liquidity.

Warsh's policy logic can be broken down into three levels:

- Underlying Logic of Rate Cuts: Against the backdrop of slowing economic growth and high debt pressure, moderately lower policy rates to reduce the burden of government interest payments and ease corporate financing pressure. But Warsh explicitly opposes "unlimited rate cuts"; he stated he did not support the Fed's decision to cut rates by 50 basis points in September 2025, believing excessive easing would undermine the achievements in inflation control.

- Core Goal of Balance Sheet Reduction: By reducing the balance sheet, strip the Fed of the "credit allocation" function it assumed after the financial crisis and return to a traditional monetary policy framework. Warsh believes the Fed's balance sheet should be maintained at the minimum level "to meet the reserve needs of the banking system," not become the "main player" influencing market liquidity.

- Prerequisite for Policy Implementation: The key to simultaneous rate cuts and balance sheet reduction lies in reducing banks' reserve requirements through regulatory reforms. Only when banks do not need to hold large amounts of excess reserves will balance sheet reduction not trigger a market liquidity crisis. However, the Deutsche Bank report points out that this prerequisite is questionable in the short term—the Fed recently restarted its reserve management purchase program, and the banking system's demand for reserves remains high.

This "paradoxical" control is fundamentally different from the linear logic familiar to the crypto market—"easing means rising, tightening means falling"—casting a layer of uncertainty over the future trajectory of the crypto market.

II. Warsh and Trump: The Complex Relationship Network from "Old Acquaintance" to "Ally"

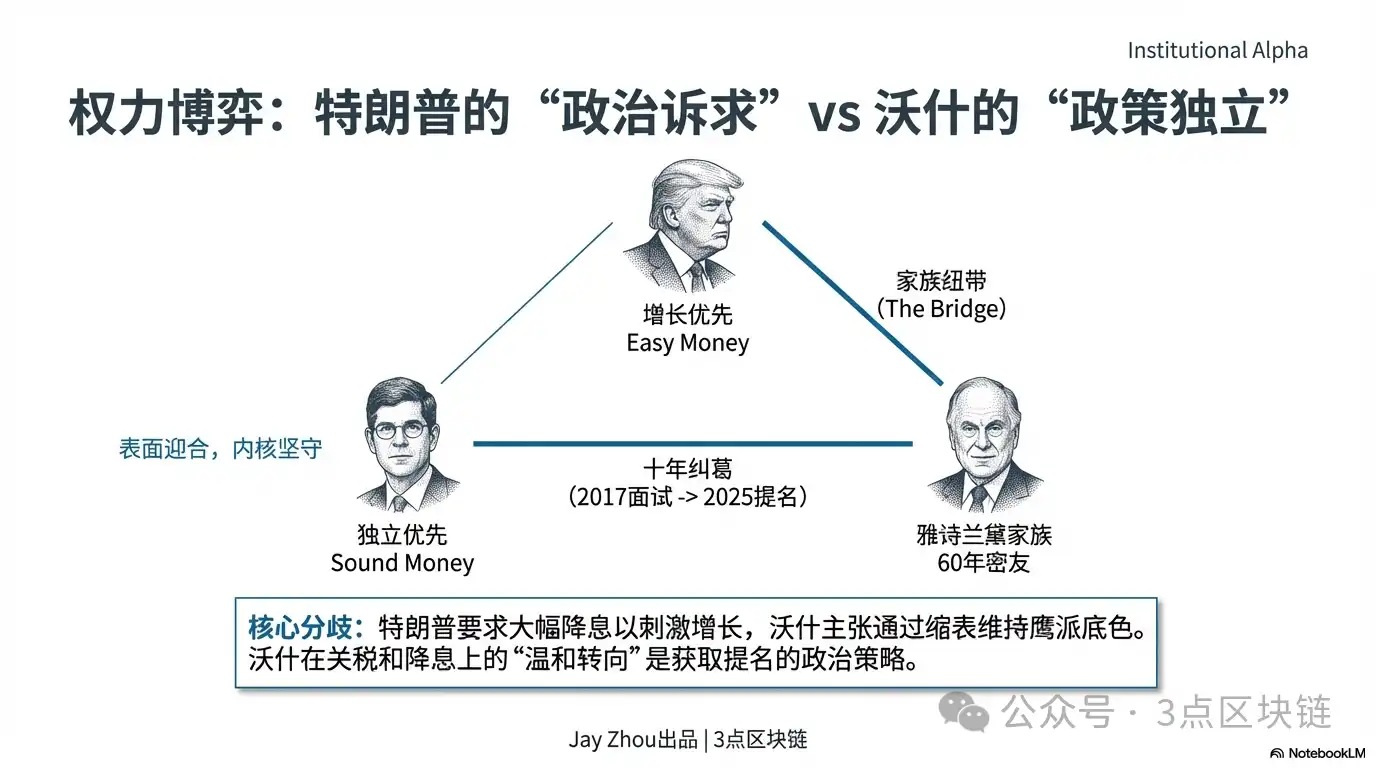

The relationship between Kevin Warsh and Donald Trump is a key thread to understanding his appointment as Fed Chair and a core variable in predicting his policy direction. Their connection did not begin with the 2026 nomination but spans nearly a decade of dual political and private ties, intertwining family connections, policy ideas, and power dynamics.

2.1 Family Ties: The "Political Bridge" of the Estée Lauder Family

Warsh's most direct connection to Trump stems from his marriage—his wife, Jane Lauder, is an heir to the Estée Lauder Group, and his father-in-law, Ronald Lauder, is a close friend of 60 years and a core political ally of Trump.

Lauder and Trump's friendship began at the New York Military Academy; they were not only classmates but also long-term business partners and political supporters. Lauder was a major donor to Trump's 2016 and 2024 presidential campaigns and was one of the first to suggest the "purchase of Greenland" to Trump, a highly controversial proposal that later became a signature event of Trump's first term. Trump biographer Tim O'Brien once stated, "For Trump, anyone connected to powerful or famous people is crucial." Lauder's family background undoubtedly provided Warsh with a "political passport" within Trump's decision-making circle.

This foundation of trust from family ties is Warsh's unique advantage over other candidates. In Trump's political logic, "personal recommendations" and "family connections" often determine appointment outcomes more than professional qualifications. In December 2025, Trump explicitly named Warsh as the "top candidate" for Fed Chair in an interview with The Wall Street Journal, an announcement behind which Lauder's influence cannot be ignored.

2.2 A Decade of Gamesmanship: From "Failed Interview" to "Handpicked Nominee"

Policy interactions between Warsh and Trump date back to Trump's first presidential term in 2017. That year, when selecting the Fed Chair, Trump personally "interviewed" Warsh but ultimately chose then-Fed Governor Jerome Powell. This decision later became a "regret" for Trump—in 2020, Trump confided to Warsh in a private setting, "Kevin, I should have used you a little bit back then. Since you wanted the job, why weren't you more aggressive at the time?"

After Trump returned to the White House in 2025, their interactions became more frequent. Warsh not only provided economic policy advice to Trump's transition team but was also considered a potential candidate for Treasury Secretary. More importantly, Warsh's "moderate shift" in policy stance gradually aligned him with Trump's core demands. Although Warsh was known as a "hawk" during his Fed tenure, in recent years he has publicly supported Trump's tariff policies and begun calling for the Fed to accelerate the pace of rate cuts. This adjustment in stance has been interpreted by the market as "political calculation to secure the Fed Chair position."

On January 29, 2026, after meeting with Warsh at the White House, Trump decided to announce the Fed Chair nomination on the morning of the 30th. This hasty schedule adjustment demonstrated the "closeness" and "decision-making efficiency" of their relationship. Trump posted on Truth Social, "I have known Kevin for many years, he is a true genius and will go down in history." This high praise starkly contrasts with his continued criticism of Powell.

2.3 Ideological Alignment: From "Policy Differences" to "Shared Goals"

The relationship between Warsh and Trump is not merely one of "political dependence" but a "strategic alliance" based on alignment in some policy ideas. Their core consensus is reflected in three aspects:

- Shared Criticism of Powell's Policies: Trump has long criticized Powell's "excessive money printing" for causing soaring inflation, while Warsh, from an academic angle, accuses the Powell-era Fed of "mission creep," overfocusing on non-core issues like employment and climate, weakening monetary policy independence. This shared view of "Powell's policy failures" became the starting point for their cooperation.

- Shared Demand for "Rate Cuts": Since returning to the White House in early 2025, Trump has repeatedly publicly pressured the Fed to cut rates, arguing that high interest rates cost the U.S. hundreds of billions of dollars in additional debt interest annually, dragging down economic growth. Warsh's proposed framework of "rate cuts and balance sheet reduction in parallel"恰好 responds to Trump's demand for cuts while maintaining his own "hawkish底色" through "balance sheet reduction," achieving a balance between "political correctness" and "academic rigor."

- Differential Understanding of "Fed Independence": Although Warsh emphasizes that "Fed independence is a valuable cause," both he and Trump believe the Fed should reduce its reliance on economic data and abandon "forward guidance," a policy tool Trump considers "meaningless." This shared pursuit of "policy simplification" found them common ground on monetary policy operations.

Notably, Warsh's shift in stance is not entirely about "appeasing" Trump. Cui Xiao, Senior US Economist at Pictet Wealth Management, points out that Warsh "wanted the Fed Chair position very much recently," hence his dovish turn on interest rates, but his core policy framework—"limited central banking" and "balance sheet reduction first"—remains unchanged. This strategy of "superficial迎合, core adherence" will be key for Warsh to balance political pressure and policy independence.

2.4 Power Balance: The Game of "Political Dependence" vs. "Policy Autonomy"

The relationship between Warsh and Trump is essentially a classic game of "political appointment" vs. "central bank independence." For the crypto market, the outcome of this game will directly determine the direction of Fed policy, thereby affecting the global liquidity landscape.

From Trump's perspective, the core goal of nominating Warsh is to "control monetary policy." Since early 2025, Trump has repeatedly publicly criticized Powell for "acting too slowly" and believes high interest rates harm the U.S. economy and government finances. He needs a Fed Chair who "can both cut rates and obey orders" to achieve his political goal of "prioritizing economic growth." Warsh's family background and stance shift make Trump believe he can "control" this new Fed Chair.

But judging from Warsh's career, he has always been labeled as an advocate for "policy independence." In 2010, he resigned in opposition to QE2, an act of "resistance by withdrawal" demonstrating his firm belief in "central bank independence." The Deutsche Bank report notes that the market will closely watch whether Warsh can maintain policy autonomy under Trump's pressure, which will be a key factor affecting market confidence.

This power balance game could have three possible outcomes:

For crypto investors, the core indicators to watch in this game are: the policy statement from Warsh's first FOMC meeting after taking office, the specific details of the balance sheet reduction plan, and his public statements regarding Trump's policies. These signals will directly determine the short-term trends and long-term structure of the crypto market.

III. Powell vs. Warsh: The Policy Divide Between Two Generations of Fed Chairs

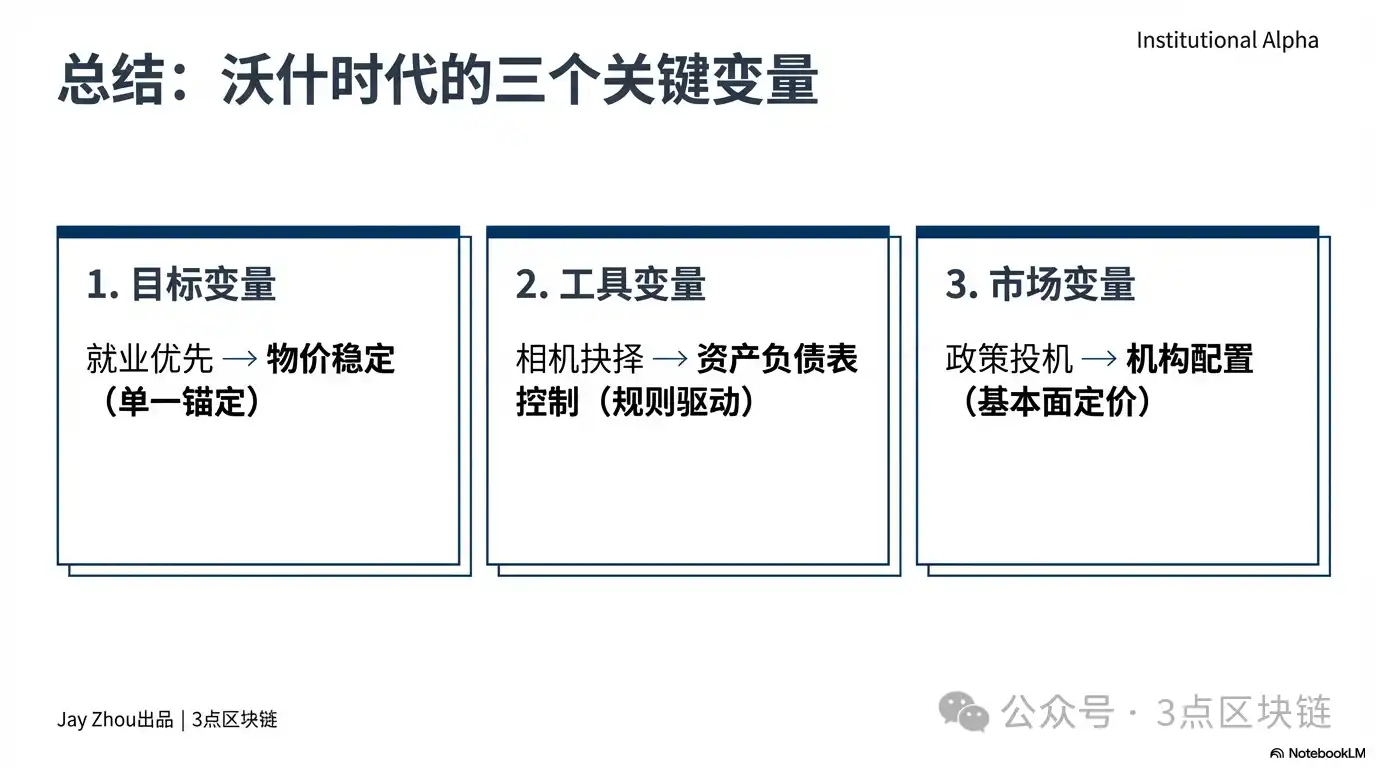

To understand the impact of Warsh's policies on the crypto market, one must first clarify the differences in monetary policy between him and his predecessor, Jerome Powell. The Fed policy under Powell's era was characterized by "discretion," with its policy cycles highly correlated with the bull and bear cycles of the crypto market. Warsh's policy framework, however, emphasizes "rules-based" approaches and "central bank independence." This difference will reshape the pricing logic of the crypto market.

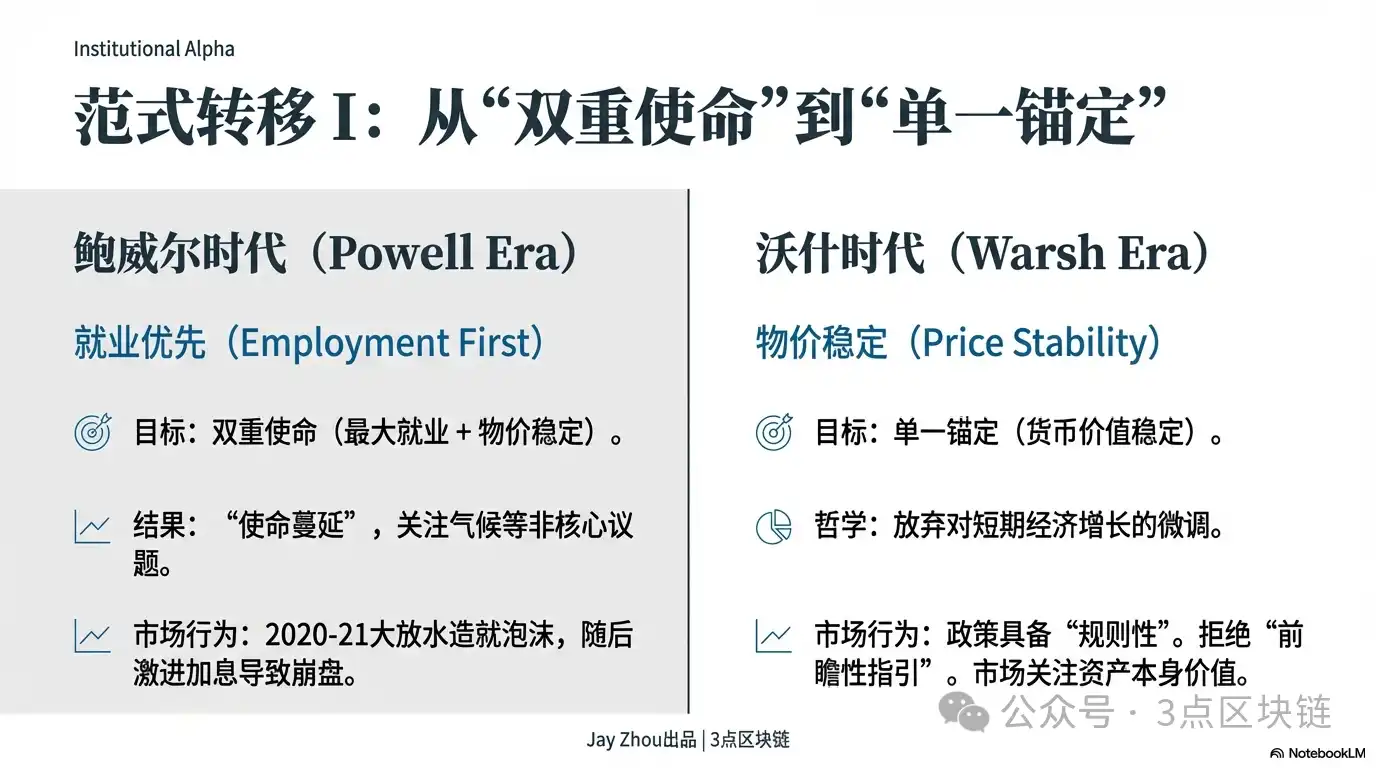

3.1 Differences in Policy Goals: From "Dual Mandate" to "Single Anchor"

Powell's eight years at the helm of the Fed始终 revolved around the dual mandate of "maximum employment" and "price stability." After the COVID-19 outbreak in 2020, Powell quickly lowered the federal funds rate to the 0-0.25% zero lower bound and launched an unlimited quantitative easing program. The Fed's balance sheet expanded by nearly $4 trillion in 18 months, peaking at $9 trillion.

This "employment-first" policy orientation brought an unprecedented liquidity feast to the crypto market. From 2020 to 2021, Bitcoin's price soared from under $10,000 to $69,000, Ethereum rose from $200 to $4,891, and the total market capitalization of crypto assets exceeded $3 trillion. At that time, the market viewed the Fed's easing policies as the core driver of crypto asset appreciation, with Bitcoin being赋予 the "digital gold" safe-haven attribute, becoming a popular hedge against inflation.

But as inflation surged to a 40-year high in the second half of 2021, Powell's policy focus shifted to "price stability." In March 2022, the Fed initiated the most aggressive加息 cycle since the 1980s, raising rates by 525 basis points cumulatively over 17 months, while simultaneously starting balance sheet reduction (quantitative tightening, QT), shrinking assets by $95 billion monthly. This policy shift directly triggered a crypto market crash: in 2022, the total crypto market capitalization evaporated by $1.45 trillion, Bitcoin fell to $15,000, Ethereum dropped below $900, and leading institutions like Three Arrows Capital and FTX collapsed successively, plunging the crypto market into a prolonged bear market.

Unlike Powell, Warsh's policy goals are closer to a "single anchor"—returning the Fed's core responsibility to "maintaining the stability of monetary value." He sharply criticizes the Powell-era Fed for "mission creep," believing it over-focused on non-core issues like employment, climate, and inclusion, weakening monetary policy independence and effectiveness. Warsh explicitly states that the Fed should reduce its reliance on economic data, abandon forward guidance—a tool "of little use in normal times"—and instead achieve long-term price stability by controlling money supply and balance sheet size.

This difference in policy goals意味着 Fed policy under Warsh will be more "rules-based" and "predictable," but it may come at the cost of short-term economic growth and employment stability. For the crypto market, this means the logic of a "policy-driven market" will be weakened, and the pricing of crypto assets will rely more on their own fundamentals rather than Fed policy shifts.

3.2 Divergence in Policy Tools: From "Discretion" to "Rules-Driven"

The Powell-era Fed excelled at using a combination of "forward guidance" and "data dependence" to guide capital flows by managing market expectations. For example, Powell clearly stated in 2020 that "rates will remain low until 2023," and emphasized in 2022 that "hikes will continue until inflation falls back to the 2% target." Such clear policy messages allowed the market to adjust asset allocations in advance.

But Warsh believes forward guidance is a "special tool for crisis times, not suitable for normal economic conditions." He criticizes the Powell-era Fed for over-relying on "black-box DSGE models," ignoring the core impact of money supply and balance sheet size on inflation. Warsh advocates that the Fed should adopt more transparent, rules-based policy tools, such as fixed money supply growth rates or balance sheet reduction paths, to reduce market speculation on policy.

The divergence in policy tools will directly affect crypto market volatility. Fed policies under Powell often caused剧烈波动 in the crypto market: In November 2025, Powell announced a pause in QT and a 25-basis-point rate cut; Bitcoin's price first fell then rose after the news, with fluctuations exceeding 5%. In January 2026, Powell indicated a "low probability of a rate cut before June," causing the crypto market to enter sideways consolidation, with Bitcoin's volatility dropping to historical lows.

Another major divergence between Powell and Warsh lies in their strategies for handling political pressure. During his tenure, Powell repeatedly resisted Trump's pressure to cut rates, insisting on hiking to fight inflation, thus维护了 Fed independence. But in 2025, as U.S. federal government debt surpassed $38 trillion and net interest payments approached defense spending, Powell's policies had to compromise with fiscal pressure—pausing QT and implementing small rate cuts to ease the government's debt servicing burden.

The political pressure Warsh faces will far exceed that faced by Powell. When nominating Warsh, Trump explicitly stated his desire for the Fed to cut rates significantly to stimulate economic growth and reduce government debt costs. But Warsh has repeatedly emphasized in public that Fed independence is "a valuable cause," and he will not yield to political pressure. The Deutsche Bank report notes that the market will closely watch whether Warsh can maintain policy independence under Trump's pressure, a key factor affecting market confidence.

For the crypto market, if Warsh yields to political pressure and implements a combination of "significant rate cuts + mild QT," it will release liquidity in the short term, benefiting crypto asset prices. But if Warsh insists on his policy主张 of "small rate cuts + aggressive QT," it will lead to持续 tightening of market liquidity, potentially prolonging the crypto bear market.

IV. The Warsh Era: Reshaping the Crypto Market Landscape and Survival Logic

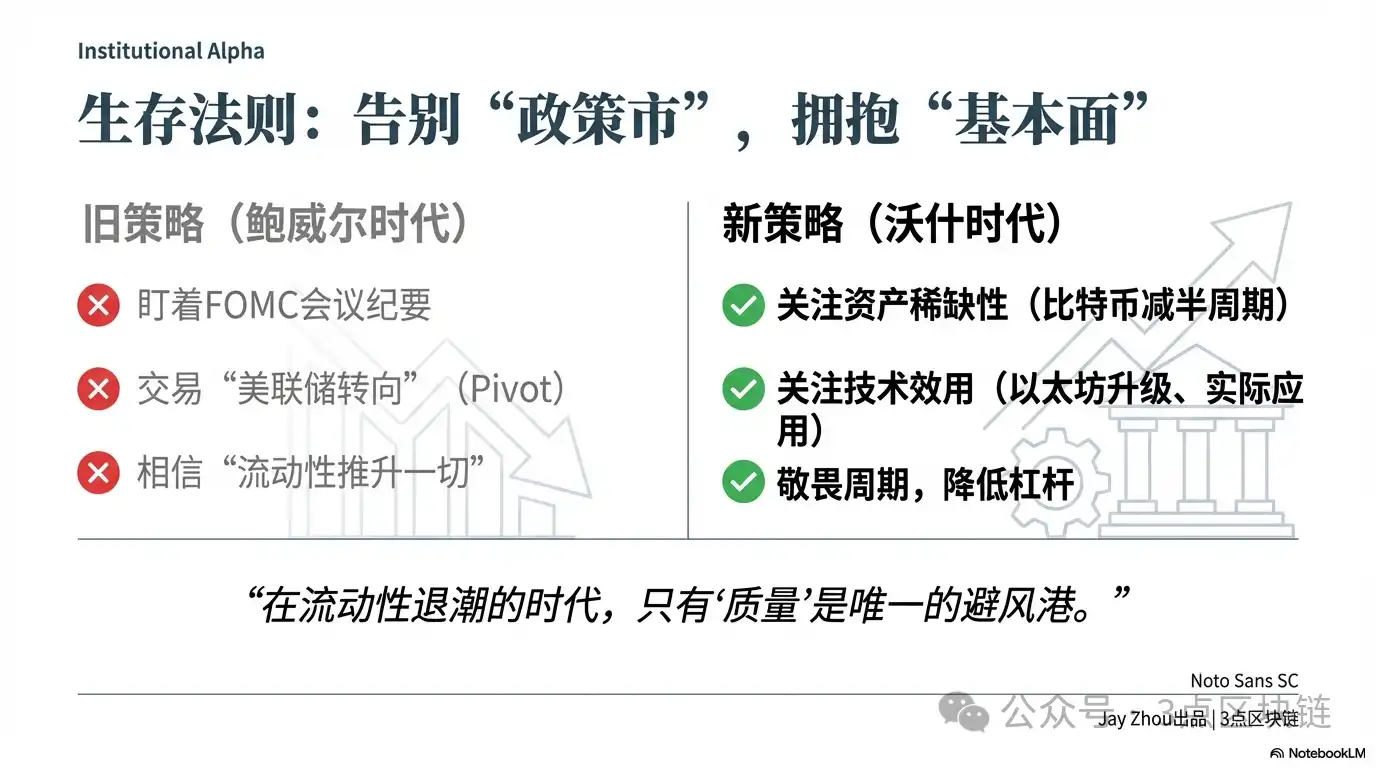

Kevin Warsh's policy stance will reshape the crypto market landscape across three dimensions: liquidity, regulation, and capital flows. Under the policy framework of "rate cuts and QT in parallel," the crypto market will move away from the "policy-driven market" logic of the Powell era and enter a new phase driven by fundamentals. For investors, understanding and adapting to this landscape change will be key to navigating the bear market.

4.1 Liquidity Game: The Dual Test of Short-Term Benefits and Long-Term Headwinds

Warsh's policy combination of "rate cuts and QT in parallel" will have a dual impact on crypto market liquidity: short-term positive shock and long-term negative suppression.

In the short term, rate cuts will lower USD funding costs, easing global USD liquidity tightness. Historical data shows that Fed rate cuts often prompt capital to shift from USD assets to risk assets. After Powell's cuts in 2020, the crypto market experienced a major bull run; in November 2025, when Powell paused QT and cut rates by 25 basis points, Bitcoin's price rebounded from $85,000 to $92,000. If Warsh implements rate cuts after formally taking office in June 2026, the crypto market could see a short-term rebound, with Bitcoin potentially breaking the $90,000 mark and Ethereum possibly returning above $3,000.

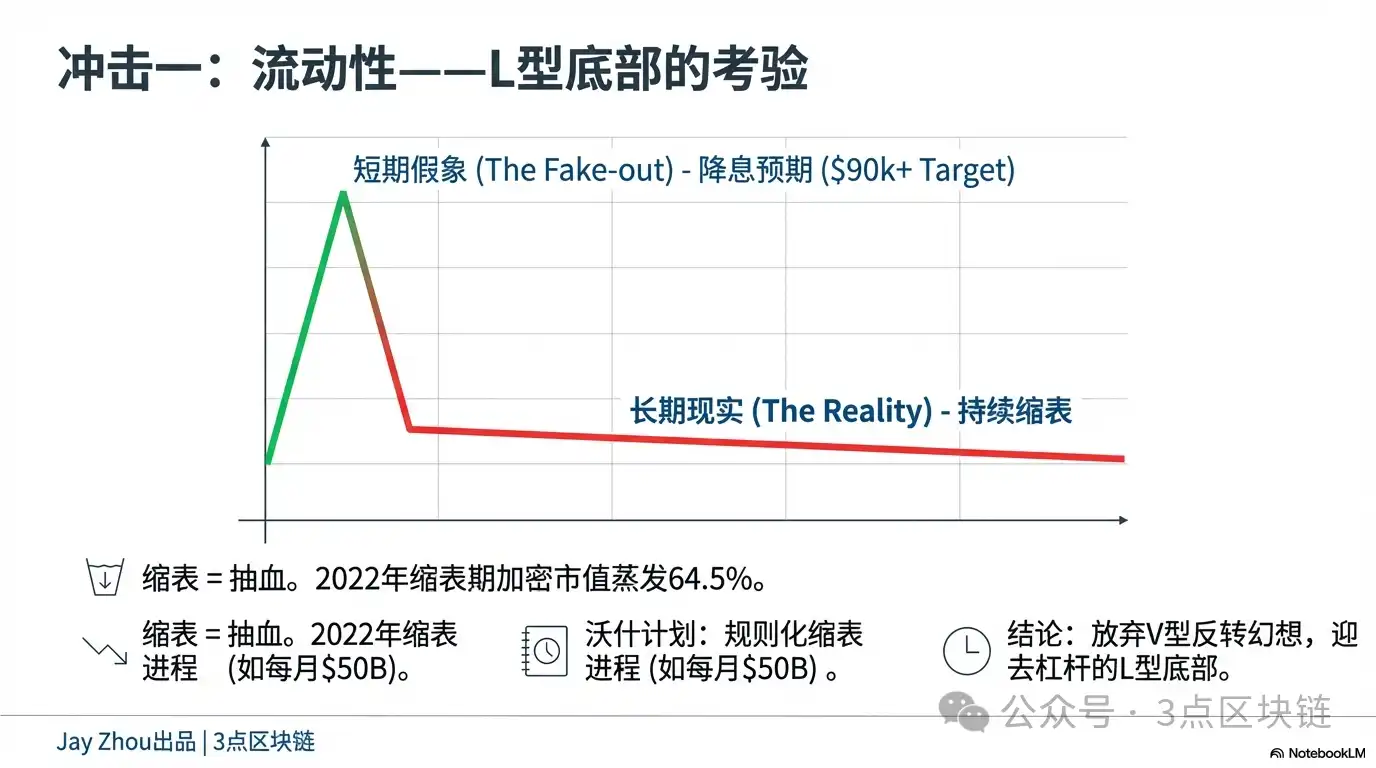

But in the long term, QT will continuously drain market liquidity, suppressing crypto asset valuations. The Fed's QT process essentially withdraws the liquidity injected during the financial crisis, leading to a reduction in global USD supply and a lower valuation ceiling for risk assets. During the Fed's QT in 2022, the total crypto market capitalization evaporated by 64.5%. This historical experience shows that QT's bearish impact on the crypto market far exceeds that of rate hikes.

More importantly, Warsh's QT policy is not a "one-time operation" but a "rules-based process." According to Deutsche Bank's预测, Warsh might set a fixed QT path, such as reducing assets by $50 billion monthly until the Fed's balance sheet shrinks to around 20% of GDP. This predictable QT process will allow the market to price in the impact of liquidity tightening in advance. The decline in the crypto market might not be as剧烈 as in 2022 but could show a trend of "persistent gradual decline."

For crypto investors, this means the difficulty of "buying the bottom" will increase significantly. In the Powell era, investors could time the market bottom by predicting the end of the加息 cycle or the start of the cutting cycle. But in the Warsh era, the long-term and certain nature of the QT process will likely result in an "L-shaped" bottom for the crypto market. Investors need to abandon the speculative mindset of "buying the dip for a bounce" and instead focus on the long-term value of crypto assets.

4.2 Regulatory Restructuring: Accelerated Compliance and Narrowed Innovation Space

Warsh's policy stance will not only affect crypto market liquidity but also accelerate the compliance process within the crypto industry.

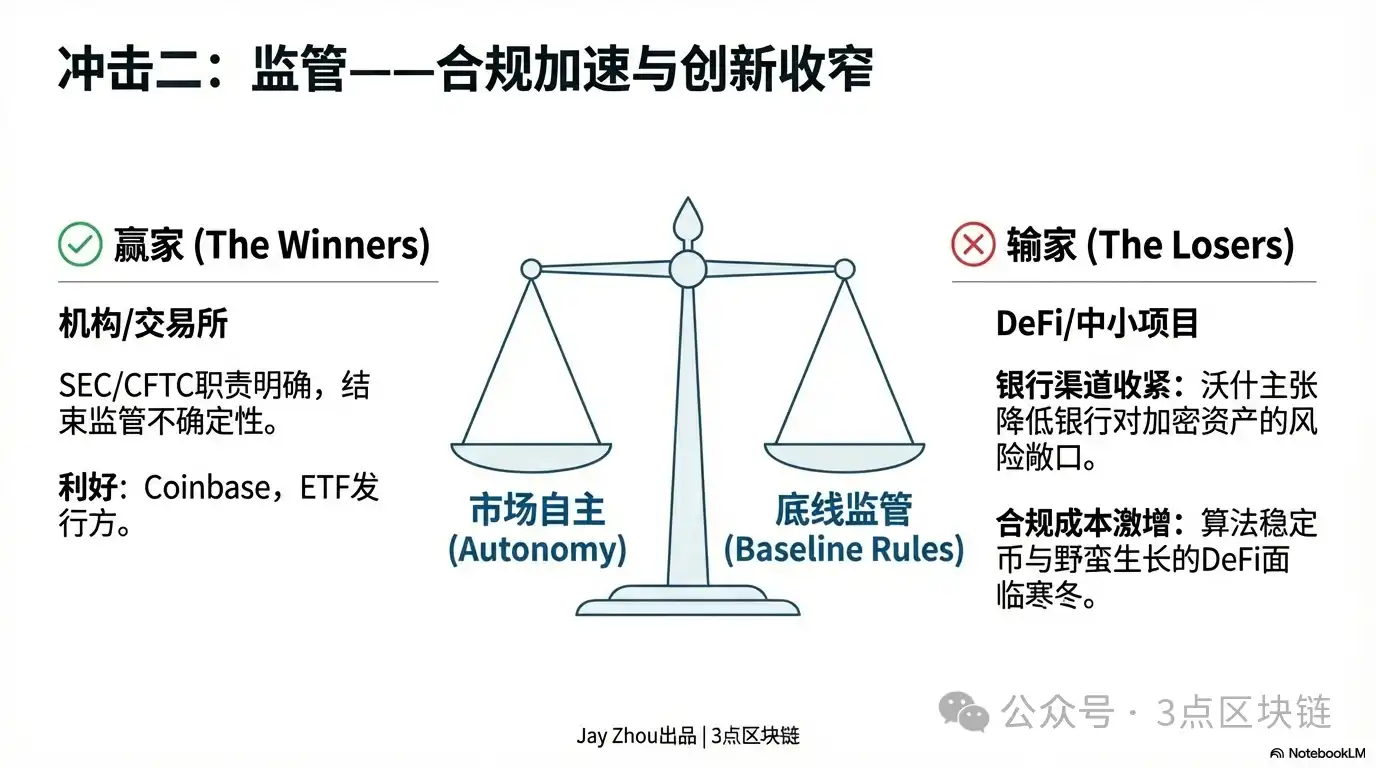

During his tenure as a Fed Governor, Warsh was known for "emphasizing financial stability." He repeatedly warned that financial innovation脱离 regulatory frameworks could trigger systemic risks. Regarding crypto regulation, Warsh's core view is "market autonomy + baseline regulation"—opposing excessive government intervention in crypto market innovation while emphasizing that crypto assets must comply with basic regulatory rules like anti-money laundering (AML) and counter-terrorism financing (CTF).

In the short term, Warsh's regulatory approach might provide a "breathing space" for the crypto market. Compared to the Powell-era Fed, Warsh is more inclined to let the market, not the government, lead the development of crypto assets. He might oppose direct Fed regulation of cryptocurrencies, instead pushing existing regulators like the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) to clarify the legal attributes and regulatory framework for crypto assets. This would help address the current "regulatory uncertainty" facing the crypto market and attract more institutional capital.

But in the long term, Warsh's regulatory approach will drive a "shakeout and differentiation" within the crypto industry. On one hand, accelerated compliance will force leading institutions like crypto exchanges and stablecoin issuers to strengthen risk controls and adhere to regulations. For example, exchanges like Coinbase and Binance may need to increase transparency, disclosing more user data and transaction information; stablecoins like USDT and USDC may need to undergo stricter reserve audits to ensure the 1:1 peg to the USD.

On the other hand, rising compliance costs will squeeze the生存空间 of small and medium-sized crypto projects. Warsh advocates reducing bank reserve requirements through "regulatory reforms," meaning banks will scrutinize the financing needs of crypto projects more strictly. Small and medium-sized crypto projects may struggle to obtain bank loans, relying instead on venture capital or ICO financing, significantly increasing the difficulty of fundraising. Additionally, Warsh's cautious regulatory attitude towards innovative products like "algorithmic stablecoins" and "decentralized finance (DeFi)" might limit innovation in these areas.

For crypto investors, this means the "龙头 effect" will become more pronounced. Mainstream crypto assets with high compliance levels and good liquidity, like Bitcoin and Ethereum, will be the preferred配置 choice for institutional funds. Altcoins lacking real application scenarios and with high compliance risks may be淘汰 by the market, eventually going to zero.

4.3 Capital Flows: Divergence Between Institutional Inflows and Retail Outflows

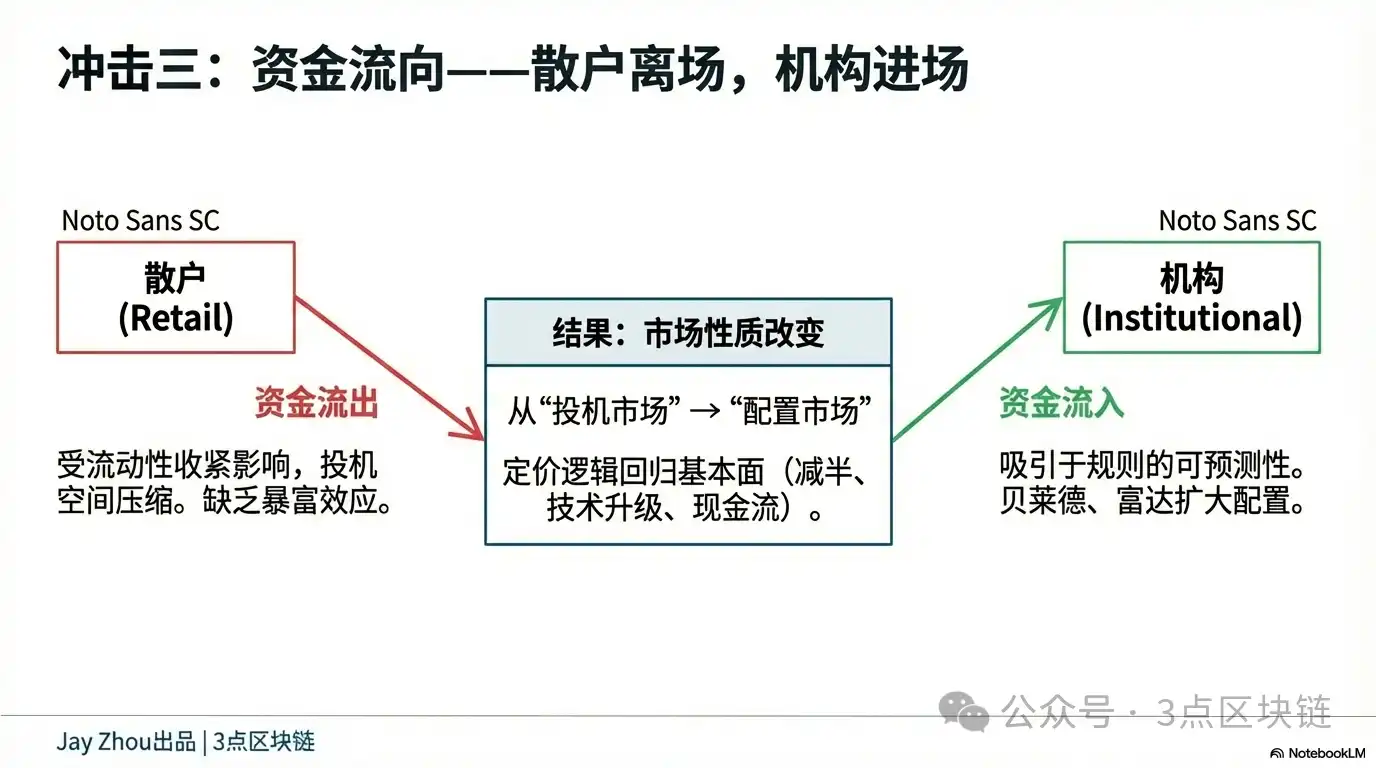

Fed policy under Warsh will drive a divergence in crypto market capital flows—accelerated institutional entry and持续 retail exit.

From an institutional perspective, Warsh's "rules-driven" policy will increase market predictability, attracting more traditional financial institutions to allocate crypto assets. For example, asset management giants like BlackRock and Fidelity might expand their Bitcoin ETF holdings, incorporating crypto assets into long-term investment portfolios; investment banks like JPMorgan and Goldman Sachs might launch more crypto derivatives to meet institutional investors' hedging needs.

Institutional entry will bring two significant changes: First, crypto market volatility will further decrease. Institutional investors tend to hold long-term rather than speculate short-term, reducing crypto asset price fluctuations. For instance, Bitcoin's intraday volatility might drop from the current 3% to 1%-2%, comparable to traditional assets like gold and stocks. Second, crypto market pricing logic will become more rational. Institutional investors focus more on crypto asset fundamentals, such as Bitcoin's scarcity, Ethereum's technological upgrades, and the profitability of crypto projects, rather than market sentiment or speculative炒作.

From a retail perspective, Warsh's QT policy will lead to持续 tightening of market liquidity, compressing the投机 space for retail investors. The 2022 crypto bear market already proved that when market liquidity dries up, retail investors are often the biggest victims—they buy high chasing rallies and sell low cutting losses, ultimately losing their capital. In the Warsh era, the long-term and certain nature of the QT process will make it difficult for retail investors to profit from short-term speculation, forcing them to exit and观望.

The divergence in capital flows will push the crypto market from a "retail-dominated speculative market" to an "institution-dominated allocation market." This means the crypto market will gradually mature, and its linkage with traditional financial markets will strengthen further. But for retail investors, it also means the "get-rich-quick opportunities" in the crypto market will become increasingly scarce, and investing in crypto assets will require more professional knowledge and a longer-term perspective.

V. Conclusion: Farewell to the Policy-Driven Market, Embrace the Fundamentals

Kevin Warsh's nomination marks the entry of US monetary policy into a全新的 era. This "crossover" figure spanning regulation, investment, and academia, along with his complex relationship network with Trump, will be a key variable influencing the direction of US monetary policy. For the crypto market, this monetary policy transformation is both a challenge and an opportunity.

The challenge is that Warsh's policy of "rate cuts and QT in parallel" may lead to持续 tightening of market liquidity, potentially prolonging the crypto bear market. The traditional logic of a "policy-driven market" will be weakened, and crypto asset pricing will rely more on their own fundamentals rather than Fed policy shifts.

The opportunity is that Warsh's "rules-driven" policy will increase market predictability, attracting more institutional capital and pushing the crypto market from a "retail-dominated speculative market" to an "institution-dominated allocation market." This might be the necessary path for the crypto market to mature and the beginning of true value回归 for crypto assets.

In the Warsh era, crypto investors need to abandon the speculative mindset of "buying the dip for a bounce" and instead focus on the long-term value of crypto assets—Bitcoin's halving cycle, Ethereum's upgrade progress, and the practical application scenarios of crypto projects. These are the core factors determining the future trajectory of crypto assets. Only by respecting the market and adhering to value can one navigate the waves of this monetary policy transformation, weather the bear market, and await the dawn.