Dollar-backed stablecoins are now more than just a crypto payment tool. Recent reports say that they may also be helping the U.S. extend dollar influence abroad, in a way that keeps real capital at home.

Here’s what you need to know.

Stablecoins – A secret weapon?

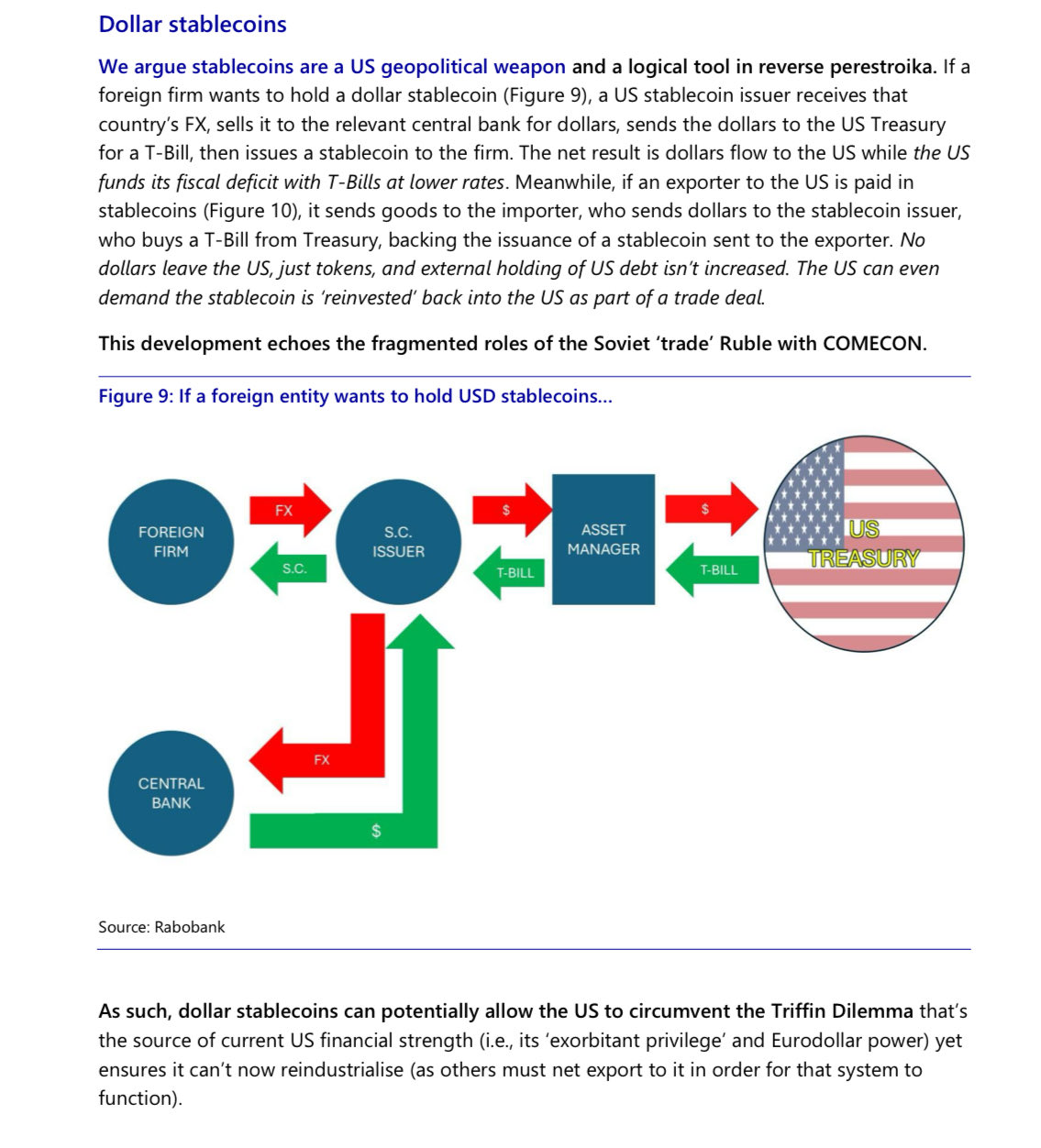

A report by Rabobank has stated that dollar-backed stablecoins are spreading dollar influence, without letting real dollars leave the country.

Source: X

The idea is that when a foreign firm wants a dollar stablecoin, a U.S. issuer converts that demand into Treasury bill purchases. Dollars flow back to the U.S. government, helping fund deficits at lower rates, while the firm gets digital dollars instead of cash.

In trade, it goes a step further. U.S. importers can pay exporters in stablecoins, while the underlying dollars stay parked in Treasuries. Only tokens move across borders.

With comparisons to the Soviet-era trade ruble, dollars are exported digitally… all while keeping the power at home.

Non-dollar stablecoins step up

- Share

- Tweet

-