Original Title: Why the defi lending moat is bigger than you think

Original Author: Silvio, Crypto Researcher

Original Compilation: Ding Dang, Odaily Planet Daily

As the market share of Vaults and Curators continues to grow in the DeFi world, the market has begun to question: Are lending protocols being squeezed for profit margins? Is lending no longer a good business?

But if we shift our perspective back to the entire on-chain credit value chain, the conclusion is quite the opposite. Lending protocols still occupy the most solid moat in this value chain. We can quantify this with data.

On Aave and SparkLend, the interest fees that Vaults pay to lending protocols actually exceed the revenue generated by the Vaults themselves. This fact directly challenges the mainstream narrative that "distribution is king."

At least in the lending space, distribution is not king.

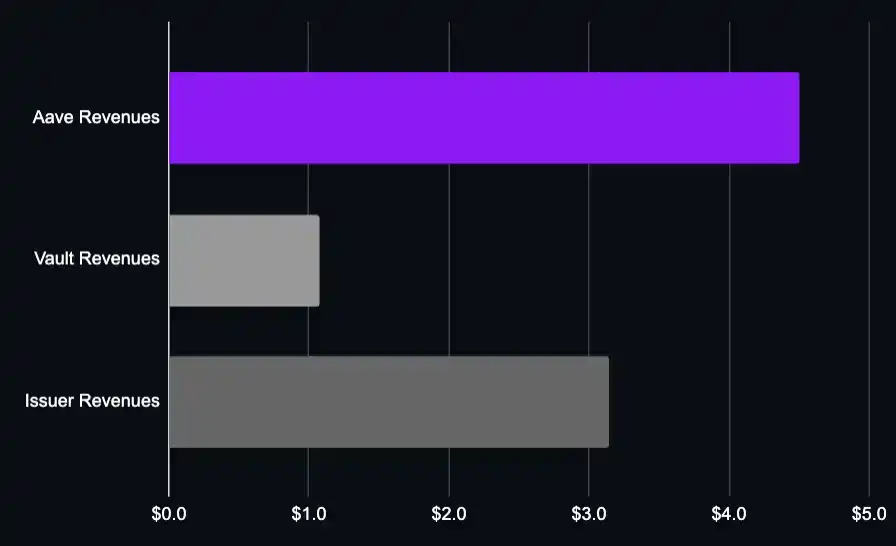

Simply put: Aave not only earns more than the various Vaults built on top of it, but also more than the asset issuers used for lending, such as Lido and Ether.fi.

To understand why, we need to deconstruct the complete value chain of DeFi lending and re-examine the value capture capabilities of each role by following the flow of funds and fees.

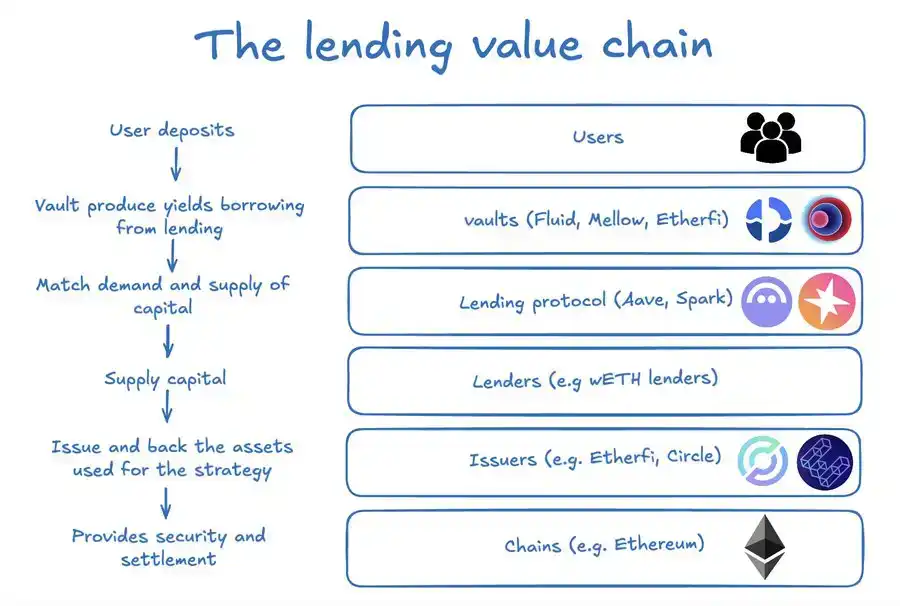

Deconstructing the Lending Value Chain

The annualized revenue scale of the entire lending market has exceeded $100 million. This value is not generated by a single link but is co-created by a complex stack: the underlying settlement blockchain, asset issuers, capital lenders, the lending protocol itself, and the Vaults responsible for distribution and strategy execution.

As mentioned in previous articles, a large number of use cases in the current lending market originate from basis trading and liquidity mining opportunities, and we have deconstructed the main strategy logic.

So, who is actually "demanding" the capital in the lending market?

I analyzed the top 50 wallet addresses on Aave and SparkLend and labeled the main borrowers.

1. The largest borrowers are various Vaults and strategy platforms like Fluid, Treehouse, Mellow, Ether.fi, Lido (which are also asset issuers). They control the distribution capability to end-users, helping users obtain higher yields without having to manage complex loops and risks themselves.

2. There are also large institutional capital providers, such as Abraxas Capital, which deploy external capital into similar strategies. Their economic model is essentially very close to that of Vaults.

But Vaults are not the whole story. At least the following participants are involved in this chain:

· Users: Deposit assets, hoping to obtain additional yields through Vaults or strategy managers.

· Lending Protocols: Provide infrastructure and liquidity matching, generating protocol revenue by charging interest to the borrowing side and taking a certain percentage.

· Lenders: Capital providers, who can be either ordinary users or other Vaults.

· Asset Issuers: Most on-chain lending assets have underlying supported assets that themselves generate yield, part of which is captured by the issuer.

· Blockchain Network: The underlying "rail" where all activities occur.

Lending Protocols Earn More Than Downstream Vaults

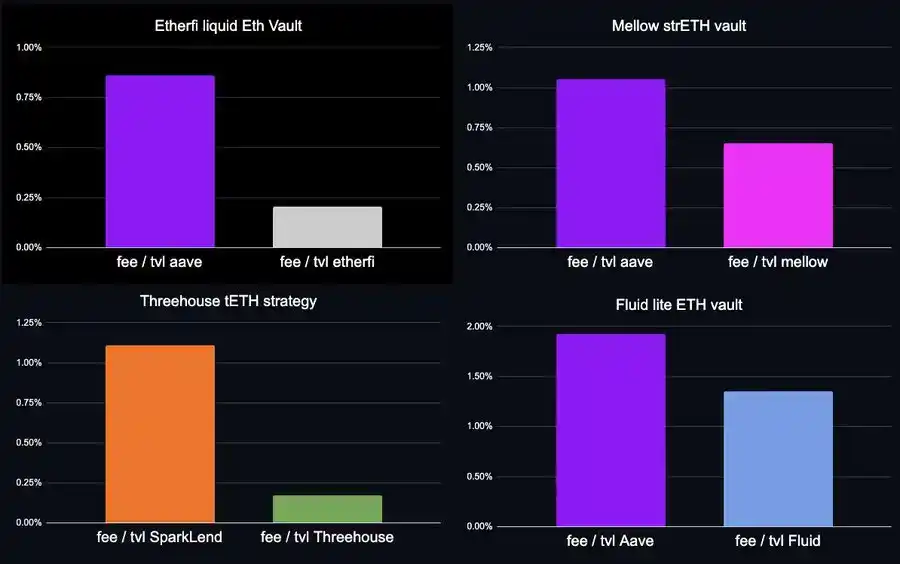

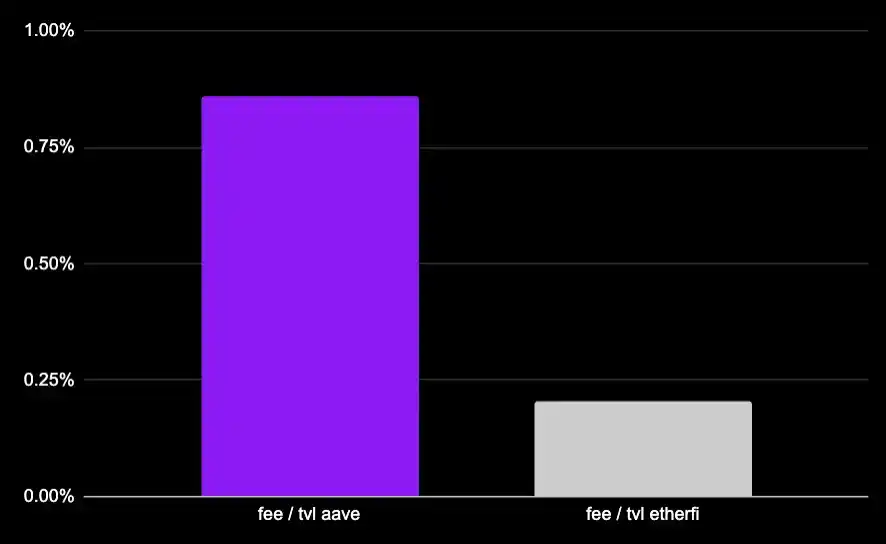

Take Ether.fi's ETH liquid staking Vault as an example. It is the second-largest borrower on Aave, with an outstanding loan size of approximately $1.5 billion. The strategy itself is very typical:

· Deposit weETH (approx. +2.9%)

· Borrow wETH (approx. –2%)

· The Vault charges a 0.5% platform management fee on TVL.

Out of Ether.fi's total TVL, approximately $215 million is the net liquidity actually deployed on Aave. This portion of TVL brings in about $1.07 million in platform fee revenue annually for the Vault.

However, at the same time, this strategy pays about $4.5 million in interest fees to Aave annually (calculation: $1.5 billion borrowed × 2% borrowing APY × 15% reserve factor).

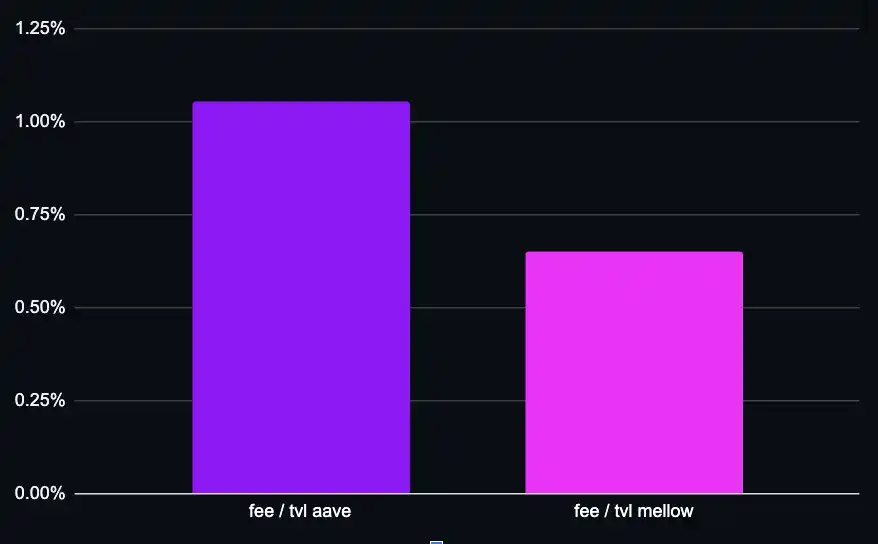

Even for one of the largest and most successful loop strategies in DeFi, the value captured by the lending protocol is several times that of the Vault.

Of course, Ether.fi is also the issuer of weETH, and this Vault itself directly creates demand for weETH.

But even considering the Vault strategy yield + asset issuer yield together, the economic value created by the lending layer (Aave) is still higher.

In other words, the lending protocol is the link that creates the largest incremental value in the entire stack.

We can perform the same analysis on other commonly used Vaults:

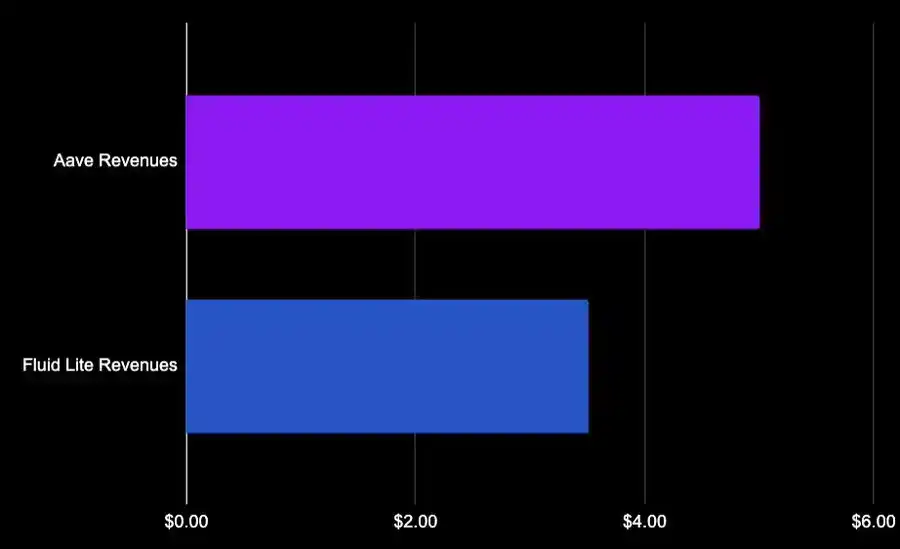

Fluid Lite ETH: 20% performance fee + 0.05% exit fee, no platform management fee. Borrows $1.7 billion wETH from Aave, pays about $33 million in interest, of which about $5 million goes to Aave. Fluid's revenue is close to $4 million.

Mellow Protocol strETH charges a 10% performance fee, with a borrowing size of $165 million and a TVL of only about $37 million. Once again, we see that in terms of TVL, the value captured by Aave exceeds that of the Vault itself.

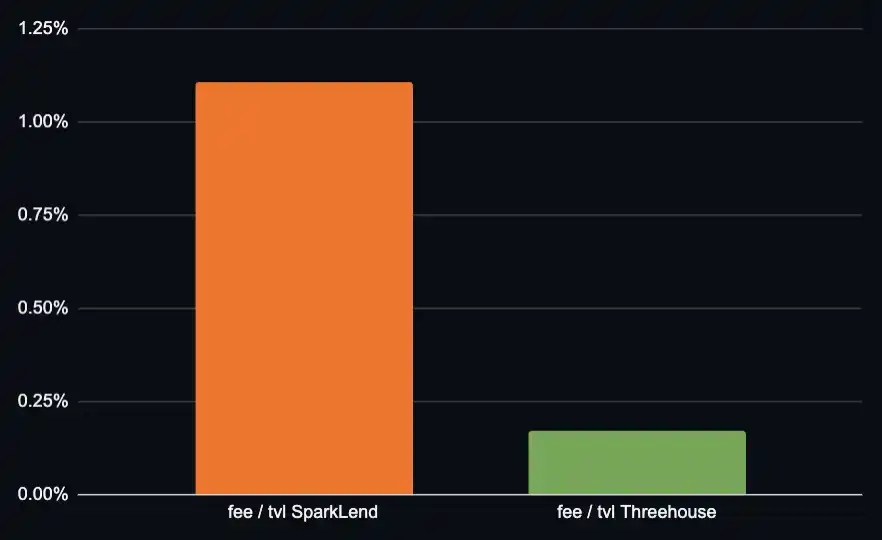

Let's look at another example. On SparkLend, the second-largest lending protocol on Ethereum, Treehouse is one of the important participants, running an ETH loop strategy:

· TVL approx. $34 million

· Borrows $133 million

· Charges a performance fee only on marginal yields above 2.6%

SparkLend, as a lending protocol, has higher value capture capability in terms of TVL than the Vault.

The pricing structure of Vaults greatly affects their own capturable value; but for lending protocols, their revenue depends more on the nominal borrowing size, which is relatively stable.

Even shifting to USD-denominated strategies, although the leverage is lower, the higher interest rates often offset this impact. I don't believe the conclusion would fundamentally change.

In relatively closed markets, more value might flow to curators, such as Stakehouse Prime Vault (26% performance fee, with incentives provided by Morpho). But this is not the end state of Morpho's pricing mechanism, and curators themselves are also engaging in distribution collaborations with other platforms.

Lending Protocol vs. Asset Issuer

So the question arises: Is it better to be Aave or Lido?

This question is more complex than comparing Vaults because staking assets not only generate yield themselves but also indirectly create stablecoin interest income for the protocol through the lending market. We can only make approximate estimates.

Lido has approximately $4.42 billion in assets in Ethereum core markets supporting lending positions, with annualized performance fee revenue of about $11 million.

These positions roughly equally support ETH and stablecoin lending. At the current net interest margin (NIM) of about 0.4%, the corresponding lending yield is about $17 million, which is already significantly higher than Lido's direct revenue (and this is at a historically low NIM level).

The True Moat of Lending Protocols

If we only compare using the deposit profit model of traditional finance, DeFi lending protocols seem to be a low-margin industry. But this comparison ignores where the real moat lies.

In the on-chain credit system, lending protocols capture more value than the downstream distribution layer and, overall, more than the upstream asset issuers.

Viewed in isolation, lending seems like a thin-profit business; but placed within the complete credit stack, it is the layer with the strongest value capture capability relative to all other participants—Vaults, issuers, distribution channels.