Author: Iron Pillar Brother in CRYPTO

The most fundamental, yet most hidden, organizational coordination mechanism in modern society is not currency itself, but the continuous extension of the debtor-creditor relationship.

Whether it's a country, a community, an organization, or an individual, the essential action being repeated is: trading the future for the present.

The economic growth and consumer prosperity we take for granted do not stem from wealth appearing out of thin air, but from a highly institutionalized consensus: the future can be allocated in advance. Debt is the technical implementation of this consensus.

Understanding the world from this perspective reveals a more fundamental core: who has a greater ability to discount the future into the present, and who has the power to define the future.

In this sense, the creation and contraction of money are merely expressions of the world of debt. The magic of finance really boils down to one thing: the intertemporal exchange of resources.

I. Understanding Gold and the Dollar from a Debt Perspective

If you place debt at the center of how the world operates, the roles of gold and the dollar immediately become clear. The dollar is not money; it is a tool for coordinating and denominating debt.

U.S. Treasury debt is not simply a liability of the United States itself. Placed within the global balance sheet, the dollar system is: the U.S. outputs promises about the future, and the world provides present productive capacity to承接 (undertake) the debt. Using the dollar as a contract, the two parties have reached the largest intertemporal transaction in human history.

The uniqueness of gold lies in the fact that it is the only financial asset that does not correspond to any liability. It requires no one's endorsement, no one's promise; it is the final settlement in itself. On the balance sheet, gold is the only asset without a counterparty.

Precisely because of this, gold often appears inefficient, unyielding, and lacking imagination when the debt system is functioning well. But when people begin to doubt whether the future can be smoothly兑现 (honored/cashed in), the value of gold is re-understood.

Some say gold hedges against geopolitical risk. But if you continue to deconstruct this using the balance sheet, this statement is incomplete. Geopolitics does not directly destroy wealth; what it truly disrupts is the stability of debt relationships.

II. Hedging is About Finding a Healthy Balance Sheet

Understanding the logic above, it becomes clear that if you understand the world as an ever-expanding balance sheet, then so-called hedging is not about finding a certain asset that is forever safe, but rather, at different stages, finding balance sheet structures that are still healthy and sustainable. The most fundamental risk is not volatility, but an imbalance in the debt structure.

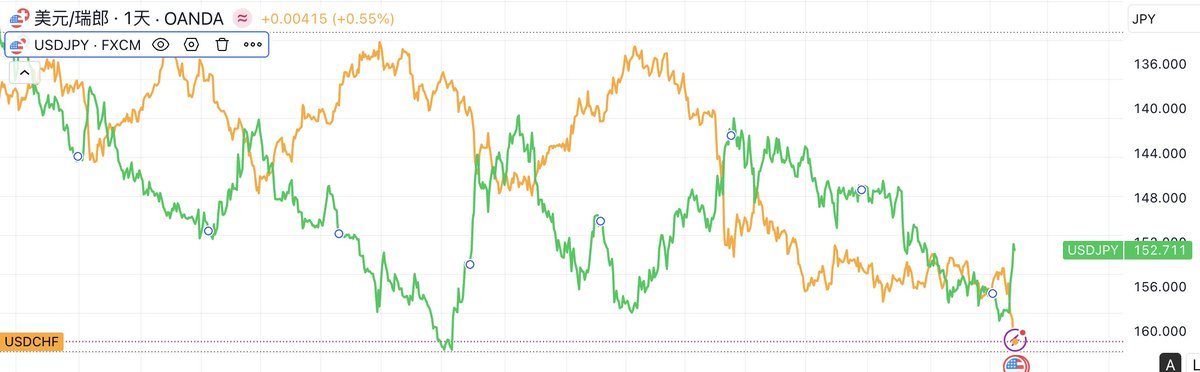

Therefore, if observing recent market trends, the depreciation of the dollar and the huge fluctuations of the yen are accompanied by the rapid appreciation of the fiat currency of countries with relatively healthy balance sheets, like Switzerland.

If we extend this view further, why is silver rising? Why are more commodities rising? Looking at it from a broader macro perspective, there is currently only one fundamental variable affecting the debtor-creditor relationship: AI.

AI is not merely an industry; in my view, its fundamentality lies in its ability to reshape the balance sheet. On one end, it infinitely drives down human efficiency costs exponentially—software becomes cheaper, labor is replaced, information processing approaches zero cost. On the other end, however, it creates an unprecedented rigid capital demand in the real world—computing power, electricity, land, energy, and minerals have become the most powerful real-world constraints.

These two forces are simultaneously acting on the global balance sheet: the efficiency side is becoming lighter, while the capital side is becoming heavier. This is fundamental to the current reshaping of the debt system.

In other words: any work that can be digitized, logicalized, or automated is seeing its cost approach zero. Software, copywriting, design, basic code—these once expensive intellectual assets are becoming as cheap as tap water. But everything has its cost. Correspondingly, the generation of every Token is背后 (backed by) the burning of computing chips, the consumption of electricity, and the transmission through copper cables. The smarter AI becomes, the more贪婪 (rapaciously) it demands from the physical world.

Over the past few decades, global growth relied more on financial engineering—credit expansion, leverage rolling, expectation management. The future could be continuously discounted, making debt seem light and controllable. But when growth becomes re-bound to variables that cannot be虚构 (fabricated/fictionalized), like computing power, electricity, resources, and productive capacity, debt is no longer just a numbers game. From this angle, when you look at silver and commodities, what the market is pricing is the提前定价 (pre-pricing) of future production capacity constraints.

Thus, when growth is locked in by physical constraints, the magic of debt fails. Because no matter how much currency you inject, if there isn't enough copper to build power grids, enough silver to make panels, AI's computing power cannot run.

III. Has the End Times for the Dollar Arrived?

Nothing is eternal, including gold. Understanding the operating logic of the debt world means one must also accept a less pleasing conclusion: gold is not the eternal answer either. Its current rise is merely due to the scarcity of being an asset without a counterparty. However, gold cannot generate cash flow, cannot improve production efficiency, and cannot replace real capital formation. From a balance sheet perspective, it's roughly equivalent to temporarily freezing risk.

Returning to the dollar, why is it still used for pricing even though the market has long been singing its demise? It's because you need the world's deepest asset pool for collateral, settlement, and hedging; you hold U.S. debt not just because you believe in the U.S., but because you need an asset recognized by the global financial system that can be used for抵押融资 (collateralized financing) at any time.

The strength of the dollar lies not in its financial correctness, but in the irreplaceability of its network effects. It is currently the only container in human civilization capable of承载 (bearing/carrying) the extension of tens of trillions in debt.

Over the past few decades, the core capability of the dollar system has been: discounting the future into the present. The U.S. issues debt, the world buys it; the U.S. consumes, the world supplies. This is essentially the global redistribution of time value.

But as the U.S. fiscal path relies increasingly on持续扩表 (continuous balance sheet expansion) and debt rolling, the credit of the dollar undergoes a subtle change: it remains the best choice, but it is no longer a free choice; the opportunity cost has risen significantly.

But the fatal blow is not this. It is that when growth relies increasingly on electricity, computing power, resources, and productive capacity, the financial system's expertise in using expectations, leverage, and discount rates to凭空 (out of thin air) bring the future to the present will encounter the hard constraints of the physical world.

The so-called Greenland (likely referring to resource acquisition/control), tariffs, and manufacturing reshoring are essentially games围绕 (revolving around) these hard constraints. In other words, the U.S. must率先 (take the lead in) completing the reshaping of AI infrastructure, turning the dollar into the sole voucher for purchasing the world's strongest computing power and most efficient productive capacity. This is the necessary condition for the dollar's王者归来 (return of the king).

Otherwise, against the backdrop of physical constraints and AI redefining global division of labor, the dollar system will gradually lose its ability to discount the future, slowly moving towards its末法时代 (end times/dharma-ending age). A slow but irreversible relative decline, until a monetary anchor that better represents real productive capacity and technological dominance emerges to replace it.