Author: Zuo Ye

Coinbase's last-minute defection has led to a stall in the subsequent Clarity Act of the Genius Act in Congress, with the "passive yield" mechanism of stablecoins becoming a focal point.

The banking industry believes that up to $6 trillion in deposits could flow into stablecoins, especially with Coinbase sharing 50% of the profits from USDC, which would siphon deposits from small local banks and community banks, further complicating financing for small businesses and ordinary people.

Coinbase counters that yield generation is merely an operational and incentive mechanism. With sufficient asset reserves for stablecoins, it will not cause a systemic crisis but will instead free more people from the "exploitation" of the banking industry's 0.01% demand deposit interest rate.

The yield mechanism, after three rounds of on-chain yield-bearing stablecoins, remains a hot topic that the traditional financial industry has yet to catch up with. We live in a world of vast disparities: the crypto space moves fast, while TradFi has scale.

Yield Capitalism

The reduction in U.S. Treasury purchases and the increase in gold acquisitions are happening simultaneously. U.S. Treasuries need new buyers, and Tether and Circle are stepping up to the task.

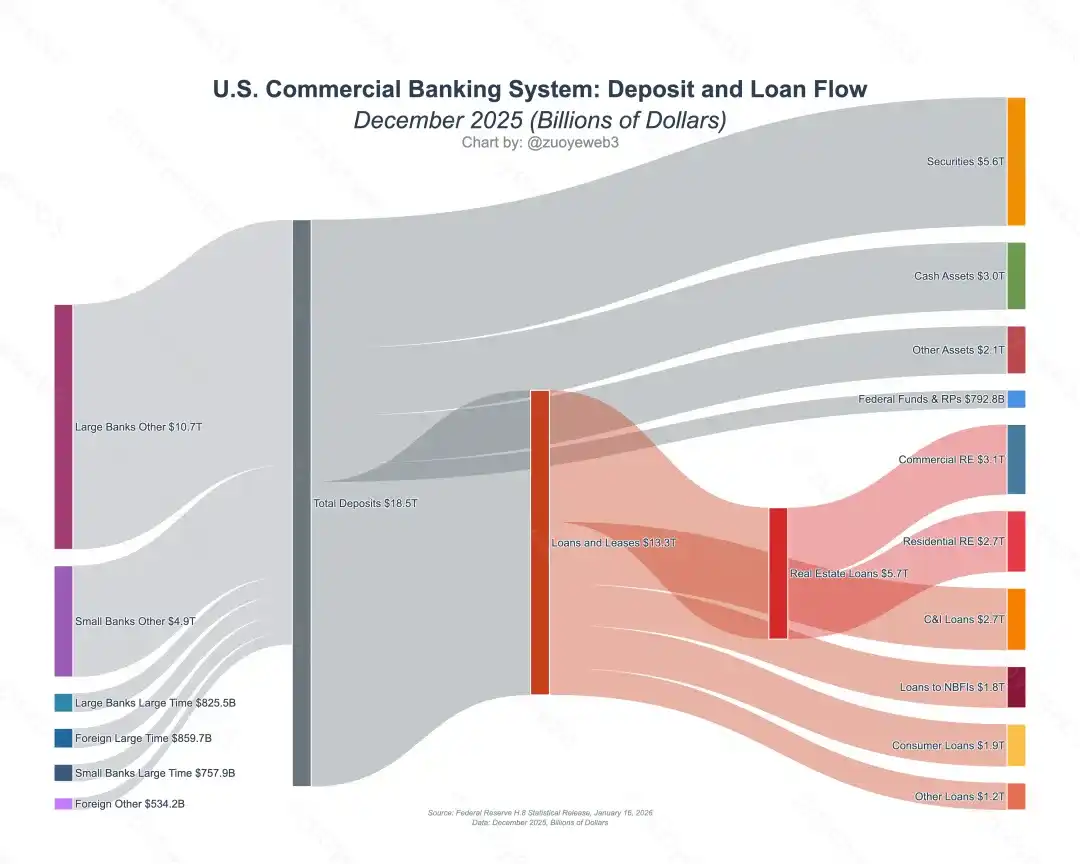

Facing Coinbase's USDC offering an annualized yield of up to 3.35%, the banking industry has two main arguments for defense. First, the deposit scale of the U.S. banking industry is as high as $18 trillion. If demand deposit interest rates are too high, banks will further increase loan rates, ultimately raising financing costs for businesses and personal credit costs.

Image description: Flow of deposits and loans in U.S. commercial banks, Image source: @NewYorkFed

Second, yield-bearing stablecoin issuers are increasingly favoring the purchase of U.S. Treasuries, which undermines the banking industry's role in dollar circulation. Additionally, on-chain stablecoins participating in DeFi could potentially cause a systemic financial crisis.

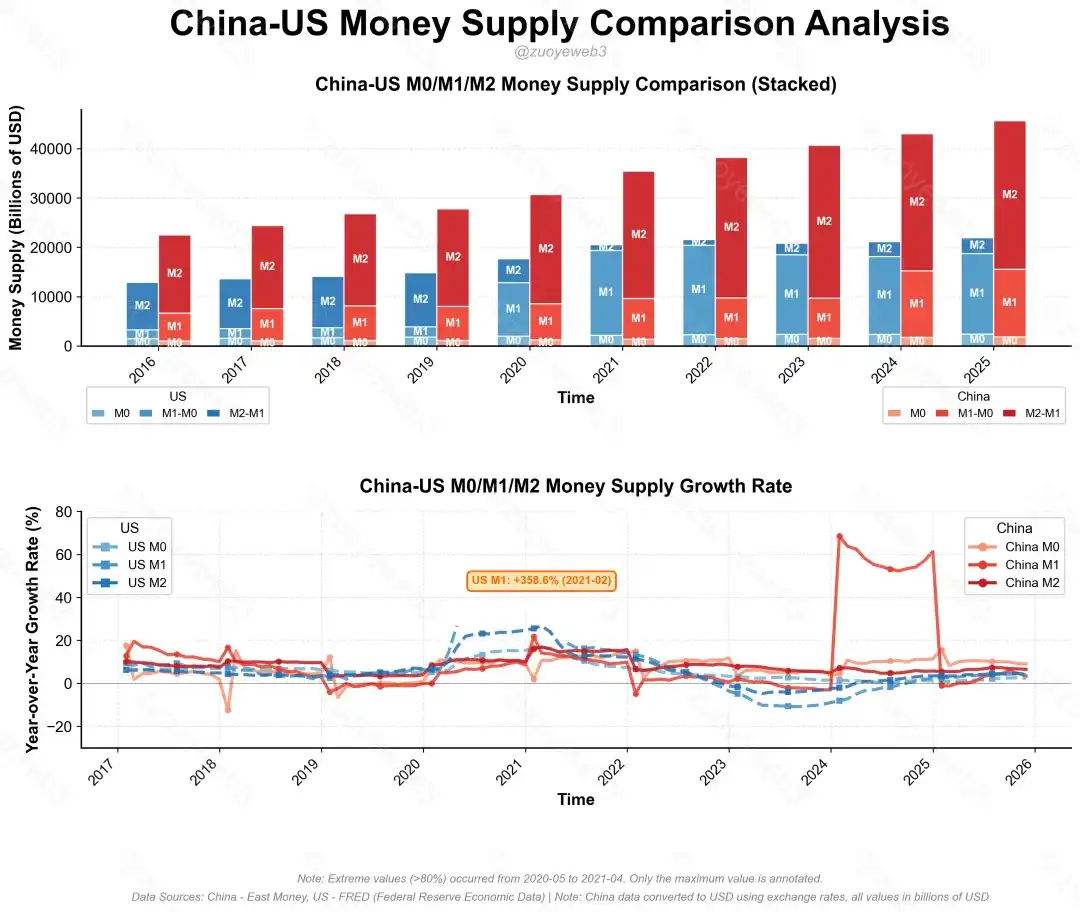

Image description: Comparison of China and U.S. M0/M1/M2, Image source: @zuoyeweb3

Addressing these two issues specifically, the current USDC issuance is $75 billion, with $40 billion invested in U.S. Treasuries. Tether's issuance is $180 billion, with $130 billion invested in U.S. Treasuries. Calculating only stablecoins issued based on U.S. Treasuries amounts to $170 billion, accounting for 3%/0.8%/0.7% of the U.S. M0/M1/M2.

However, according to Ark Invest's statistics, the share of the three largest foreign buyers of U.S. Treasuries has dropped from 23% in 2011 to 6% in 2024. With the tariff war spreading to Europe, U.S. Treasuries need more external buyers to maintain their global status. Fundamentally, the U.S. has no reason to reject stablecoins.

Although the Genius Act prohibits offering interest to attract customers, GUSD issued by Paxos in partnership with Kraken and PYUSD issued with Paypal can still bypass this restriction. Either Paxos and other third parties act as the operational entity, or custodial institutions like Anchorage offer interest to institutional clients.

In fact, crypto peers, including Ripple and a16z, hope to pass the bill as soon as possible, rejecting passive yield but also exploring active yield. Only Coinbase is putting up a stubborn resistance.

The core issue lies in scale expansion. The total issuance of various stablecoins is currently $300 billion, with strictly defined on-chain yield-bearing stablecoins at $30 billion. Compared to the two major real-world obstacles, the practical impact feared by the banking industry is still far in the future.

Within the crypto space, since the collapse of UST in 2022, the only highlight has been USDe and sUSDe issued by Ethena, forming the main model of on-chain yield-bearing stablecoins. However, after sparking a frenzy in 2025, it quickly went through three phases:

- 2025.7.29: Starting with the carry trade arbitrage initiated by USDe in collaboration with Aave, the scale rapidly dropped from $10 billion to $6.5 billion after the 10·11 major liquidation. It abandoned building its own blockchain and essentially transformed into a white-label platform.

- 11·03 xUSD depegging incident: This led to a FUD crisis for many vault managers on Morpho/Euler. The issuance and scale of on-chain stablecoins plateaued, no longer maintaining the growth trend since July.

- The Plasma deposit activity, which wasn't remembered until December: Including Tempo supported by Paradigm and Stripe, Stable supported by Tether, and Plasma and other stablecoin blockchains, all lacked staying power and failed to make breakthroughs in P2P payments and off-chain enterprise adoption.

Outside the crypto space, as mentioned earlier, the banking industry's strict blockade against stablecoin yield generation is evident. The stablecoinization of the payment industry is an unstoppable trend but remains strangely disconnected from DeFi. Firstly, the three crises did not affect the payment industry's enthusiasm for stablecoins. Secondly, the yield mechanism can indeed improve overall economic efficiency.

Payment Embraces On-Chain Vaults

It is not capital that creates interest, but interest that creates capital.

Ethena is gradually bowing out, but it at least leaves behind an opportunity for stablecoins to be reborn, truly a case of "a whale falls, and all things flourish":

- Yield mechanism generalization: It has spread from stablecoins to all assets, such as Perp DEX and Binance's RWUSD product lines.

- Vaults are basically mature: For example, white-label platforms for generic yield stablecoins based on the earnings of Morpho vault managers like Stakehouse.

If we observe the current operation process of stablecoins, it has significantly diverged from traditional USDT, especially with the embedded existence of yield-bearing products.

Image description: Stablecoin issuance paradigm, Image source: @zuoyeweb3

USDC/USDT based on U.S. Treasuries are not only the foundation for issuing stablecoins like Ethena's but also the pools of USDC in lending can further衍生 as the underlying source for yield mechanisms. This is the true current state of on-chain stablecoin adoption.

Except for TRC-20 USDT on Tron, the destination for most stablecoins is DeFi. This not only disproves the banking industry's fear that yield-bearing stablecoins will harm the financial system but also disproves the sanctity of "passive yield" that Coinbase staunchly defends. The Morpho yield vaults that Coinbase connects to are also products operated by Stakehouse.

Coinbase plays a dual role in skimming profits: it takes profits from USDC issuance and also takes profits from Morpho's operations. It's more Meituan than Meituan, more Didi than Didi.

Beyond Coinbase, on-chain stablecoins can already avoid excessive skimming by issuers and channel providers. However, the cracks between yield generation, stablecoins, and payments still require innovative mechanisms to erase.

In other words, if yield-bearing stablecoins can only divert funds from the banking industry to DeFi Vaults, becoming non-productive speculative bubbles and ultimately a self-fulfilling prophecy, $6 trillion in stablecoins would be enough to trigger a systemic crisis.

To promote the growth of stablecoin scale, increase their real-world utility, and still retain the yield mechanism, the only way is to make yield generation a universal standard in the payment industry.

Taking Airwallex's Yield product as an example, it not only offers a higher annualized yield than Coinbase's USDC deposits but also supports merchants with multi-currency yield products, underpinned by money market funds.

Image description: Airwallex Yield Product, Image source: @airwallex

Comparing this to Stakehouse's on-chain vaults, the only difference is the real business scenarios that Airwallex and others possess, allowing for efficient use of corporate idle funds. However, if combined by on-chain vaults, not only would the yield be higher, but the yield-bearing stablecoins could also be used normally.

Different from USDC's holding-to-earn-yield and Airwallex's idle-funds-yield, yield-bearing stablecoins "earn yield while usable," embedding the yield mechanism into the entire process before, during, and after use. Even after consumption, a Points mechanism can be added.

Compared to the difficult customer acquisition for U Cards on the C-end, payment channels need the financial innovation of stablecoins more. Trip.com's overseas version supports U deposits, backed by the Singapore-licensed gateway Triple-A. For Trip.com, it's just integrating a new third-party payment. For Triple-A, choosing which stablecoin to use is a matter of code selection.

After the disputes involving Morpho/Aave/Sonic, no one believes that "Code is Law" anymore; the concept of decentralization has been severely damaged. But "Money is Code" is increasingly clear. Even from a legal perspective, quite a few yield-bearing stablecoins are more compliant than USDT.

This way, users, merchants, and channel providers can all get what they want: users get interest, merchants get customer traffic, and channels get benefits. This is also the most embedded and feasible path for commercial scenarios currently.

Conclusion

The deposit-ization of funds, the yield-ization of deposits.

The crypto industry is at a turning point. Selling its own assets to outsiders is gradually becoming unworkable; altcoins and Meme coins are inadequate. The path for stablecoins to break out of the circle is too far from retail investors because retail cannot profit from the real adoption of stablecoins.

Half a year ago, stablecoins were an asset issuance method. Now, stablecoins need to have hidden appreciation potential.

After the flameout of leverage-based USDe and xUSD, expanding the use cases and holder base of stablecoins, thereby having retail act as LPs to provide liquidity for on-chain vaults, is currently more feasible.

Problems stack upon problems. This will create new issues of vault misconduct, which previously only affected the crypto space and were relatively controllable. Once it spills over to real businesses and users, the entire stablecoin ecosystem will be rejected. How to control the vaults? We need new methods. This is the theme of the next article: Everyone is a Vault Manager,透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视透视 Vaults.