Australia moved closer to tokenization, with the Reserve Bank of Australia (RBA) outlining its next phase.

At the ‘Beyond Tomorrow’ forum on the 25th of March, Assistant Governor Brad Jones said the focus had shifted from “if” to “how” tokenization would be implemented.

He stated,

First, we no longer see the main question as whether tokenisation has a future in Australia’s financial system, but rather, how.

How tokenization will be implemented

Australia appeared positioned to advance tokenization across asset classes, with a focus on enabling 24/7 trading.

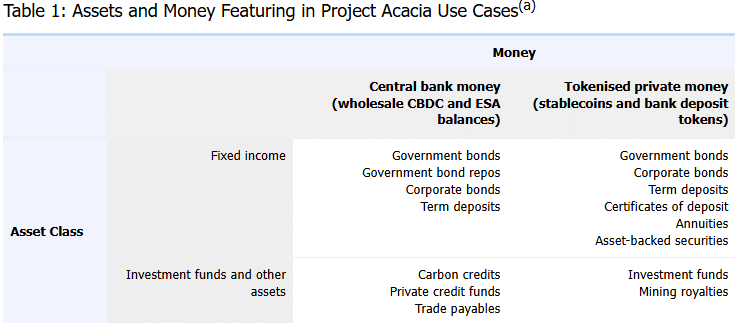

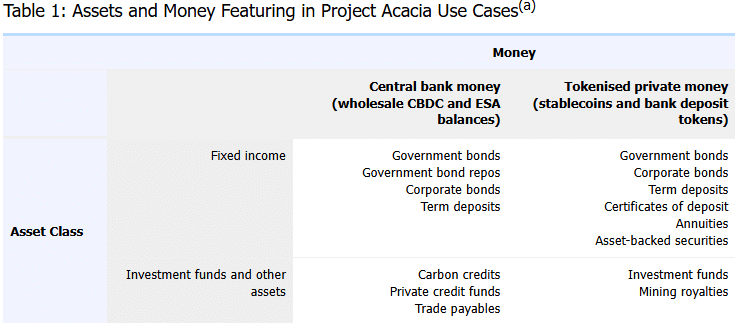

On the RBA website, Jones detailed findings from Project Acacia, which projected $16.7 billion in annual efficiency gains.

The central bank noted that stablecoins and bank deposits could coexist within the system.

The pilot covered fixed income and investment funds, with transactions flowing through both central bank money and tokenized private money.

These included government bonds, corporate bonds, carbon credits, and private credit funds.

However, the RBA confirmed it would work with the Council of Financial Regulators (CFR) and DFCRC to support implementation.

That coordination could accelerate Australia’s stablecoin market and broader digital economy.

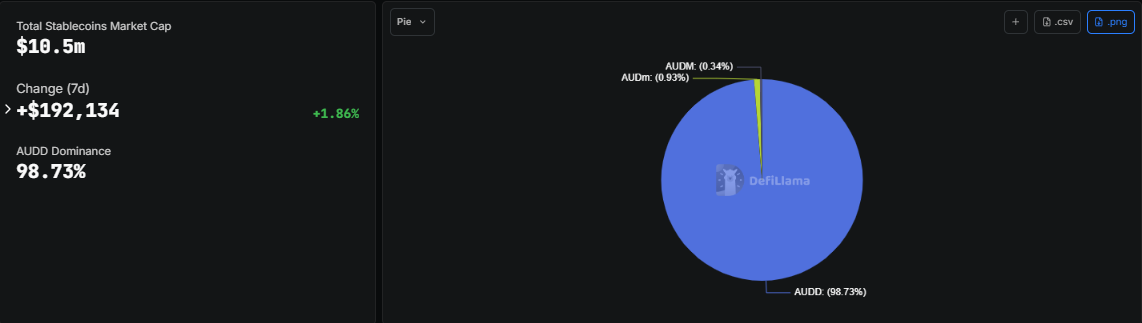

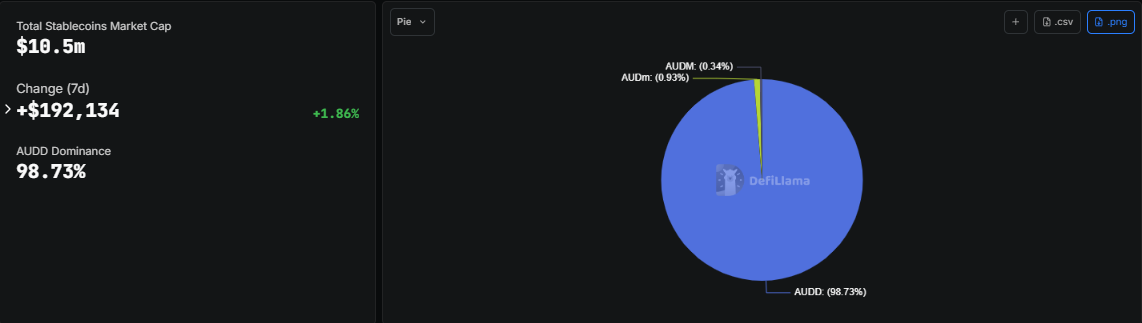

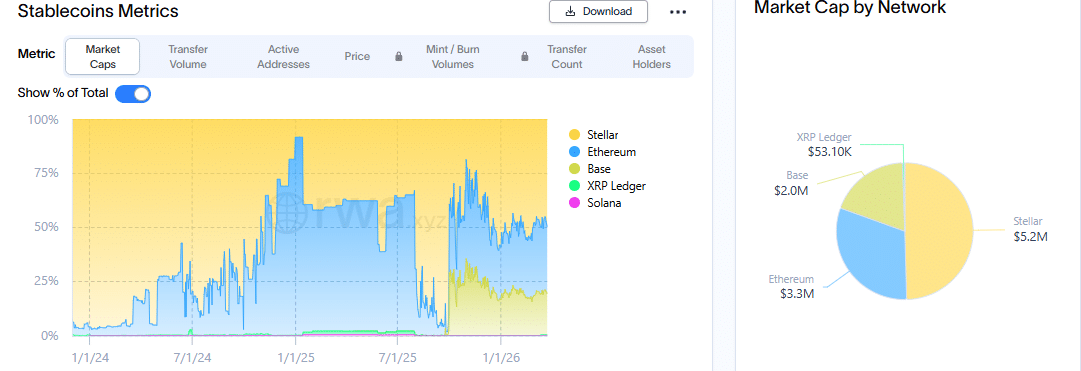

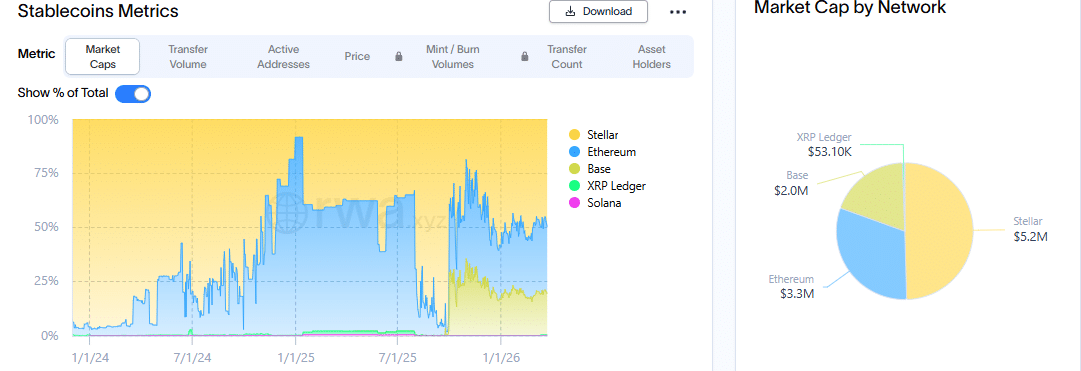

Australia dollar [AUD] stablecoins market cap

Speaking of the market cap for Australian dollar stablecoins, it is relatively low, probably due to regulatory hurdles before the RBA move.

As per DeFiLlama, their total market cap was at $10.5 million, a growth of 1.86% this week. In this lot, AUDD led with a dominance of 98.73%, equivalent to $10.35 million.

Others in the list were AUDm and AUDM, accounting for 0.93% and 0.34% of the total cap, respectively. The joint had a cap of about $133K.

Narrowing down the analysis to AUDD, it was spread across five major blockchains.

The largest share of its cap, about 48%, was on Stellar [XLM], equal to $5.2 million, as Ethereum [ETH] came second with 31% of the total.

Base Chain held 19%, which represented $2 million. Meanwhile, less than 1% of its total share was on Solana [SOL] and XRP Ledger.

The projection from Project Acacia, together with the implementation, was a precedent for the growth of tokenization in the Australian market.

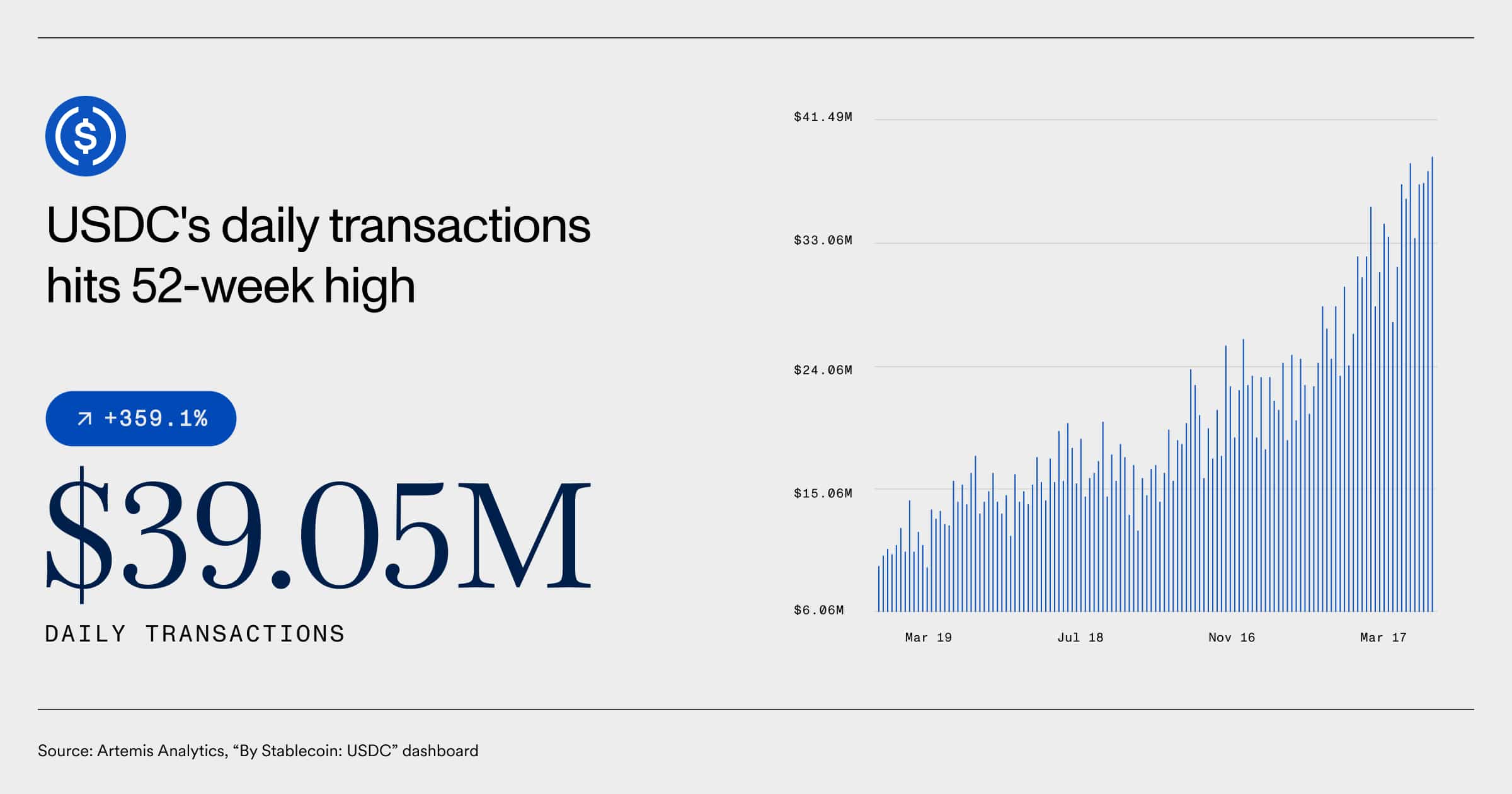

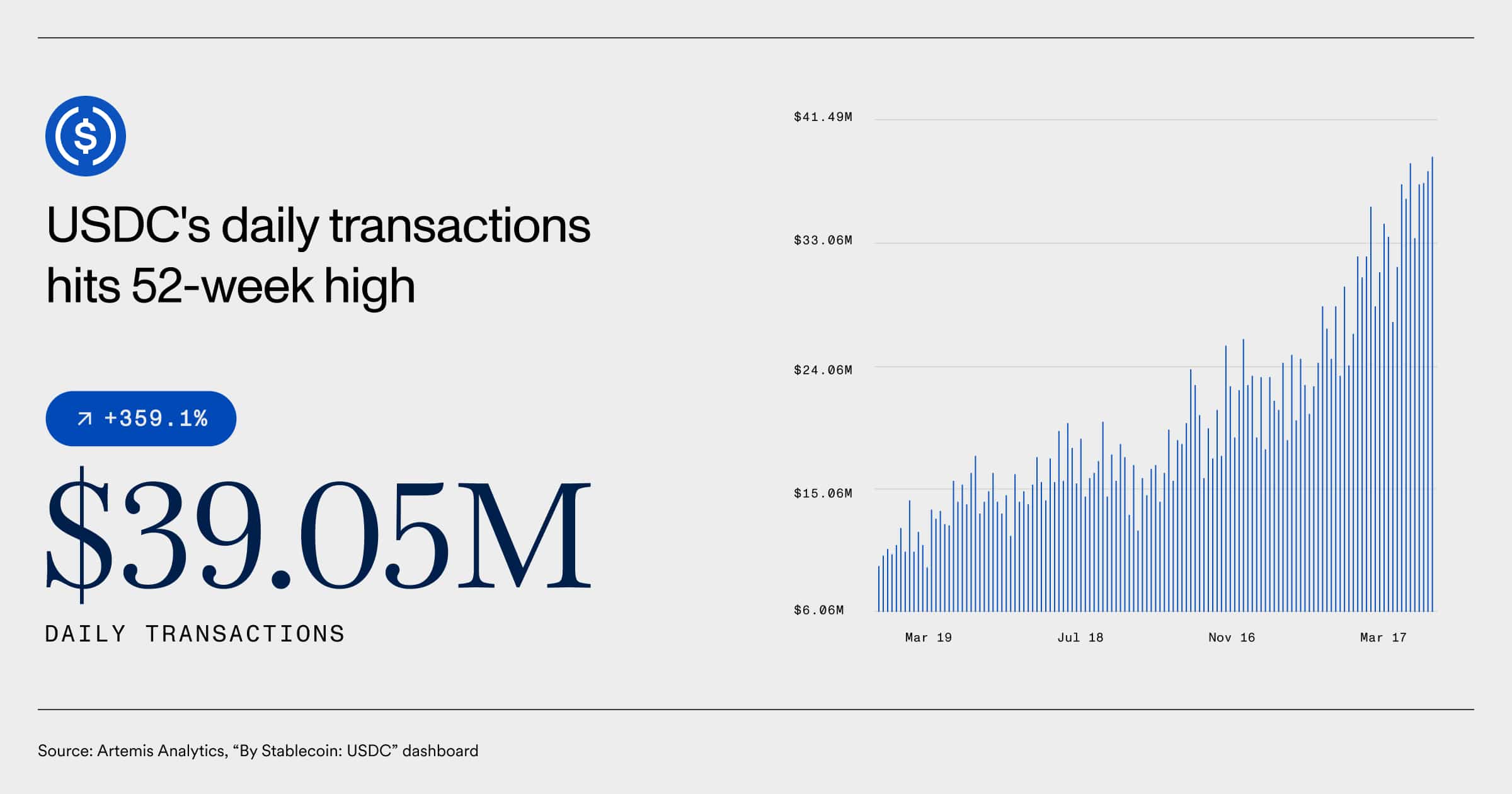

Daily transactions surge

Tokenization was heavily reliant on stablecoins.

For context, daily transactions for USD Coin [USDC] had hit a 52-week high of $39.05 million. This equated to a 359% growth since March 2019.

However, the growth of the Australian dollar stablecoin market was nowhere near that of the USD-backed ones. Therefore, tokenization could spur growth in AUD-backed stablecoins and real-world assets (RWAs) in the country.

Final Summary

- RBA shifts from asking whether tokenization was happening to how to implement it.

- The market cap of AUD-backed stablecoins has stayed relatively low, but the regulations could shift this trend.