Original | Odaily Planet Daily (@OdailyChina)

Author | Azuma (@azuma_eth)

More than 30 hours have passed since the bridge contract of Kelp DAO's rsETH was compromised. Although the parties involved (LayerZero, Kelp DAO, Aave) have made statements (primarily "shifting blame" and emphasizing their own innocence), a final solution has yet to be provided.

Therefore, this article aims to discuss the current positions and attitudes of the involved parties, explore the reasons for the delay in finalizing a solution, and attempt to speculate on how the incident might ultimately be resolved.

Odaily Note: For background, please refer to "DeFi Hacked Again for $292 Million, Is Even Aave Unsafe Now?"

Who Should Be Responsible?

First, let's discuss the issue of responsibility.

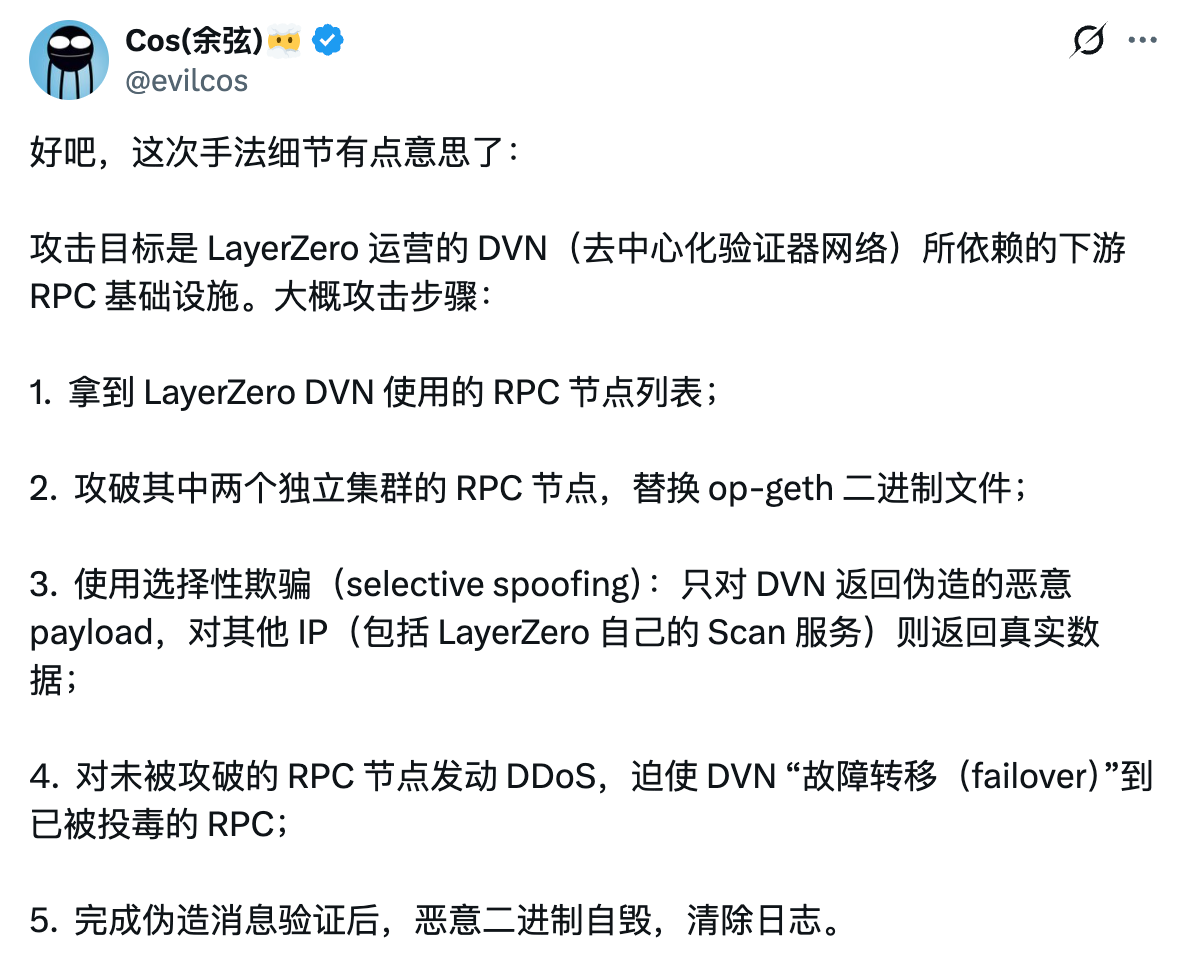

According to the details disclosed by LayerZero, the direct cause of the incident is quite clear: the downstream RPC infrastructure relied upon by LayerZero's operated Decentralized Verifier Network (DVN) was compromised (see the analysis by SlowMist founder Yu Xian in the image below). Furthermore, because Kelp DAO's bridge contract used a 1/1 DVN configuration, the attacker only needed to complete one forged message verification to carry out the attack.

LayerZero believes that Kelp DAO, which adopted the 1/1 DVN configuration, is the most directly responsible party in this incident. This is indisputable—such an obvious "single point of failure" is utterly absurd.

However, as the underlying cross-chain protocol, LayerZero should also bear some responsibility. While LayerZero allows each upper-layer application to configure the number and threshold of DVNs itself, and the 1/1 DVN was Kelp DAO's own choice, as the designer of the underlying architecture, it should also avoid allowing such an obviously flawed configuration.

Finally, there are lending protocols like Aave (focusing on Aave here). Although they are also indirectly affected victims, objectively speaking, Aave's excessive lending permissions granted to rsETH and other LRT assets for expansion purposes are the direct reason it finds itself in its current passive position. Additionally, it is worth mentioning that Aave's former risk control team, BGD Labs (now separated from Aave), explicitly pointed out the DVN issue with Kelp DAO back in January last year. Kelp accepted the advice at the time but clearly did not make the changes... Aave's failure to continue supervising and taking corresponding measures is also a case of reaping what it sowed.

So the assignment of responsibility is clear: Kelp DAO bears primary responsibility, LayerZero secondary responsibility, and Aave also has some indirect responsibility.

The Awkward Reality

Reality is always more complex than theoretical expectations. The most critical issue is that the Kelp DAO team, which should bear the primary responsibility, does not have enough money to cover the shortfall... Directly imposing a loss write-down on all rsETH holders or betraying Layer2 token holders is essentially a dead end.

So who has the money? The first is LayerZero, which is facing a reputation crisis due to this incident, has been temporarily disabled by multiple institutions and protocols such as Bitgo, Tron, Ethena, Curve, and ether.fi, and risks losing a significant share of the cross-chain market. The second is Aave, which is facing huge potential bad debts and watching over ten billion dollars in TVL flow out.

Thus, the "ulterior motives" of each party are clear. The primarily responsible party, Kelp DAO, is basically paralyzed and unable to lead the subsequent compensation efforts; what to do needs to be discussed with the two bigger players. Meanwhile, LayerZero and Aave, the secondary and indirectly responsible parties with the ability to pay, have both stated that their protocols did not have vulnerabilities, clearly indicating they are not planning to easily take on such a huge responsibility... So the situation seems somewhat deadlocked for now.

However, I do not believe this situation will last long because both major protocols have a need to resolve the issue quickly—LayerZero cannot abandon its OFT cross-chain ecosystem ambitions, and Aave cannot ignore the continued outflow of existing funds.

The Key to the各方博弈 (Parties' Game Theory)

This morning, Aave issued an updated statement on the incident. The most important piece of information in the statement was—Aave emphasized that "rsETH on the Ethereum mainnet is fully backed".

How should this be understood? We need to start with the design of rsETH.

rsETH is essentially a liquidity restaking voucher token issued by Kelp DAO. Each rsETH token is backed by 1 ETH within the staking and restaking system, following the path "ETH - Lido - EigenLayer - Kelp DAO - rsETH".

The rsETH on the mainnet refers to the original voucher tokens issued by Kelp DAO on Ethereum. Later, to expand within the Layer2 ecosystem, Kelp DAO would use LayerZero's bridge contract (the thing that caused trouble in this incident) to map the mainnet rsETH to various Layer2s. For every 1 rsETH issued on a Layer2, the corresponding rsETH on the mainnet is deposited into Kelp DAO's custodian contract, to be released only when the Layer2 rsETH is bridged back to the mainnet.

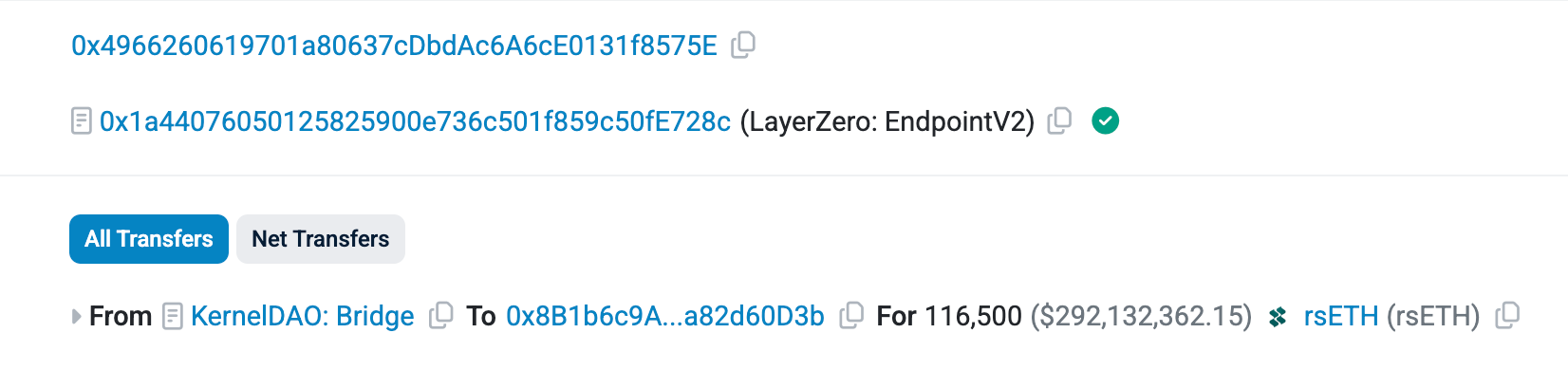

Now, back to the incident itself. As mentioned earlier, the reason for the theft was that the hacker tricked the DVN into forging a cross-chain message, causing the bridge contract to "mistakenly release" 116,500 rsETH—note, this did not involve printing new coins out of thin air, but rather obtaining the original voucher tokens from the mainnet that should not have been released.

The problem lies precisely here. These tokens were already circulating on Layer2 through mapping, while the tokens on the mainnet were in a locked state. However, after the hacker obtained them, they deposited them into lending protocols like Aave and borrowed more liquid WETH, thus completing their escape—again, it must be emphasized that the rsETH deposited by the hacker was real, which is why Aave supported the抵押借贷 (collateralized lending) behavior for this token.

Now, looking back at Aave's statement is very interesting. The phrase "rsETH on the Ethereum mainnet is fully backed" is essentially saying: "These coins are real! Kelp DAO, you should support us in using these coins to redeem the underlying ETH (contracts are paused, redemption is currently not possible)... As for the mapped version of rsETH on Layer2 that lost the backing of the mainnet rsETH, we can't deal with that!"

This is likely Aave's inclination. Although emphasizing the value of mainnet rsETH means disregarding the value of the mapped rsETH on Layer2, and since Aave itself also has some rsETH debt positions on its Layer2 lending products (current real-time scale is $359 million), this would also create some bad debt. But weighing the two evils, Aave most likely assessed the potential impact of both options and determined that protecting its core mainnet product best serves its maximum interests.

But this is just the stance of Aave alone. How the incident is resolved ultimately depends on whether an agreement can be reached with LayerZero and Kelp DAO.

Although the latter have not yet issued further statements, I personally believe LayerZero will have difficulty accepting this solution, because abandoning the mapped tokens on Layer2 would directly threaten LayerZero's cross-chain reputation.

Potential Solutions

The problem must ultimately be solved. Various big names on social media have been offering suggestions to Aave, LayerZero, and Kelp DAO these past two days.

DefiLlama founder 0xngmi speculated on three possible paths but also stated that all three have obvious flaws. The first path is for all rsETH holders to jointly bear an 18.5% value write-down (proportion of lost tokens/issued tokens), with Kelp DAO taking the blame itself, and Aave also bearing roughly $216 million in bad debt on the mainnet. The second path is to disregard the value of all mapped rsETH on Layer2, thus preserving Aave's mainnet product, but likely causing the Layer2 ecosystem to collapse and Kelp DAO's reputation to hit zero. The third path is to fully compensate holders of rsETH before the hacker attack based on a snapshot, with subsequent buyers or transferees bearing the losses themselves. However, since funds have moved significantly after the attack, this is practically impossible to execute.

OneKey founder Yishi stated: "The best outcome now is to negotiate with the hacker, offer a 10–15% bounty, get most of the funds back, and everyone is happy. If negotiations fail, the LayerZero生态基金 (ecosystem fund) should contribute the most—it's the richest, has the most long-term interest, and paying up could save the OFT ecosystem. Kelp DAO is the poorest; either use tokens + future revenue to compensate, or simply sell the entire project to LayerZero or Bitmine. Aave's Umbrella and stkAAVE cover the last layer, but WETH depositors absolutely must not suffer a value write-down. Otherwise, Morpho, Spark, Fluid, Euler would all undergo repricing simultaneously, the entire LRT sector would be blacklisted, and the entire DeFi industry would be set back three years."

In any case, the parties will certainly continue to argue for a while longer, as involving hundreds of millions in real money means no one wants to be the biggest sucker.

As for how much more time is needed to provide a solution, as mentioned earlier, the two giants dare not delay too long. LayerZero is currently forced into a pause by various partner institutions and protocols; delaying longer will likely lead these partners to switch cross-chain solutions. Aave's situation is also not optimistic; the utilization rates of multiple pools have reached 100%, leaving depositors 'trapped'... If ETH were to suddenly plummet sharply, Aave would likely be unable to effectively liquidate (which is indeed the case now) and could incur more bad debt, ultimately causing the problem to snowball—if it reaches this point, the foundation of the industry could be shaken, a situation obviously no one would like to see.