Author: Chloe

Original Title: Following the Decline but Not the Rise, Why Did Bitcoin Plummet Again?

After a period of sideways consolidation, the cryptocurrency market experienced a price drop from last night to this morning. Bitcoin fluctuated and declined sharply within just a few hours, quickly falling below the $85,000 mark, dropping from around $89,000 on the 28th to near $82,000 on the 30th, with an overall decline of about 7-8%, hitting the lowest point since last November.

This sudden and severe pullback that caught investors off guard is the result of a combination of factors: a collapse in tech stock sentiment, rising geopolitical risks, and internal liquidity drying up in the crypto market.

Microsoft's Earnings Report Sparks Investor Concerns Over AI Benefits

The starting point of this crypto market decline is largely related to the opening of the U.S. stock market. According to foreign media reports, after the U.S. stock market opened on Thursday, global markets immediately entered a downward trend. The core momentum came from the earnings report released by tech giant Microsoft after the U.S. market closed the previous day.

Although the software giant's revenue actually grew by 17% in the fourth quarter, the slowdown in its cloud division's growth and the massive spending in the artificial intelligence field raised investors' concerns about over-investment in AI in the tech industry. Microsoft's stock price plummeted by 12% after the earnings report, dragging down the entire tech sector.

After the U.S. stock market opened on Thursday morning, the Nasdaq Composite Index fell by about 2.3%, and the S&P 500 Index dropped by about 1.5%. The comprehensive rout of tech stocks quickly spread to the cryptocurrency market. Bitcoin's price rapidly declined in a short period, hitting a low of $81,000. According to CoinGecko data, Bitcoin's recent trading price has accumulated a 6% drop compared to a week ago.

Cryptocurrencies as the First Risk Assets Sold Off by the Market

Timot Lamarre, Research Director at Unchained, pointed out that although many people view Bitcoin as the world's hardest currency, the vast majority of market participants still regard Bitcoin as a tech stock trading target. This perception makes it difficult for Bitcoin to remain unaffected when traditional tech stocks suffer heavy losses. Historical data also confirms this; there is a significant correlation between Bitcoin and the U.S. stock market, especially tech stocks. When investors become skeptical about the prospects of the tech industry, cryptocurrencies are often among the first risk assets to be sold off.

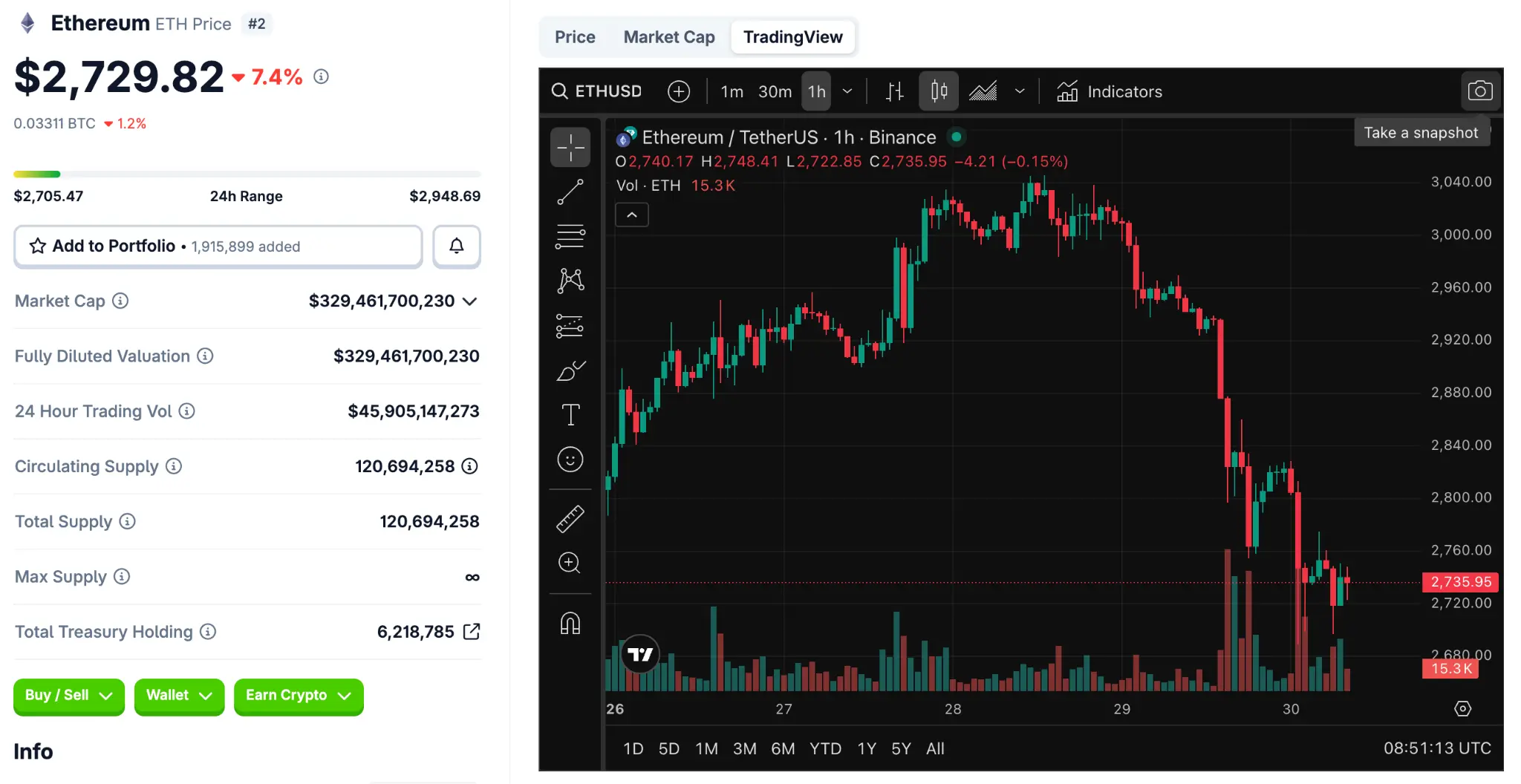

Meanwhile, Ethereum fell by over 7% in a single day, with its trading price dropping to around $2,729. Besides these two major cryptocurrencies, other top-ten crypto assets by market cap also generally experienced declines of 4% to 6%.

Among mainstream coins, popular tokens like XRP and Solana also saw similar single-day declines. Overall, the total market capitalization of the cryptocurrency market fell by about 5%, now reduced to $2.79 trillion.

Large-Scale Liquidation Events Create a Vicious Cycle

In addition, this sharp decline also caused large-scale leveraged liquidation events. According to CoinGlass data, in the past 24 hours, over 200,000 traders had their positions liquidated, with a total liquidation amount exceeding $813 million. Among them, long positions accounted for the vast majority of the liquidations, reaching nearly $700 million, indicating that there were a large number of bullish bets in the market before the price plummeted.

DLNews data shows that just the positions betting on Bitcoin's price rise had $313.7 million liquidated that day, with another $327 million in Bitcoin-related positions wiped out in the past 24 hours. Ethereum followed closely, with liquidation amounts reaching $134 million.

Such large-scale liquidation events often create a vicious cycle.

When prices start to fall, the forced liquidation of leveraged positions further exacerbates selling pressure, pushing prices down further and triggering more liquidations. This avalanche effect is particularly evident in environments with insufficient liquidity, causing prices to fall much faster than market expectations.

Unstable Middle East Situation, Multiple Macro Risk Factors Erupt

Besides the drag from tech stocks, multiple macro risk factors are also putting pressure on the market simultaneously. Tensions between the U.S. and Iran have reheated. According to a Reuters report, U.S. War Secretary Pete Hegseth said today that regardless of what decision President Trump makes regarding Iran, the U.S. military will be ready to carry out its mission to ensure that the Tehran regime does not develop nuclear capabilities, "They should not seek nuclear capabilities, and whatever the President expects from the War Department, we will be ready to accomplish the mission."

Some U.S. officials also revealed that Trump is evaluating various options but has not yet decided whether to use military force against Iran. However, Trump has repeatedly warned that if the Iranian regime resumes its nuclear program, the U.S. will take action.

At the same time, the risk of a U.S. government shutdown is also being priced into the market. As negotiations remain deadlocked before the critical deadline, without a last-minute agreement, multiple federal agencies could face operational disruptions, delayed payments, and reduced recent fiscal clarity. Historical data shows that during the past three government shutdowns, Bitcoin prices experienced significant declines, with the highest drop reaching 16%.

Fragile Crypto Market Structure, Deeper Declines, Difficult Rebound

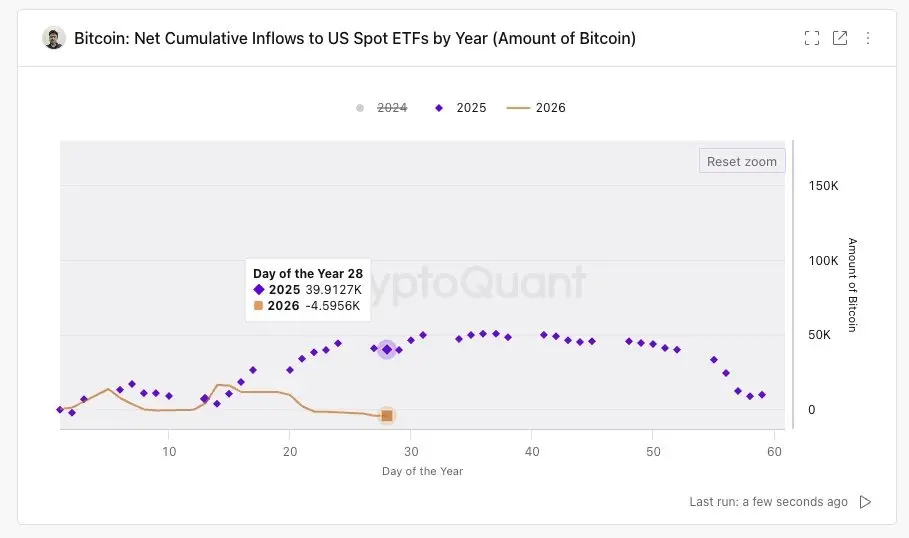

Finally, the inherent fragility of the crypto market structure should be the most important attribution in this downward trend. U.S. spot Bitcoin ETFs have net sold about 4,600 Bitcoins year-to-date, compared to a net inflow of nearly 40,000 Bitcoins during the same period last year. ETFs were supposed to be the most stable source of buying power in this cycle. Now that this support has disappeared, the rebound has lost momentum, and the decline has become more severe due to a lack of承接 (buying support).

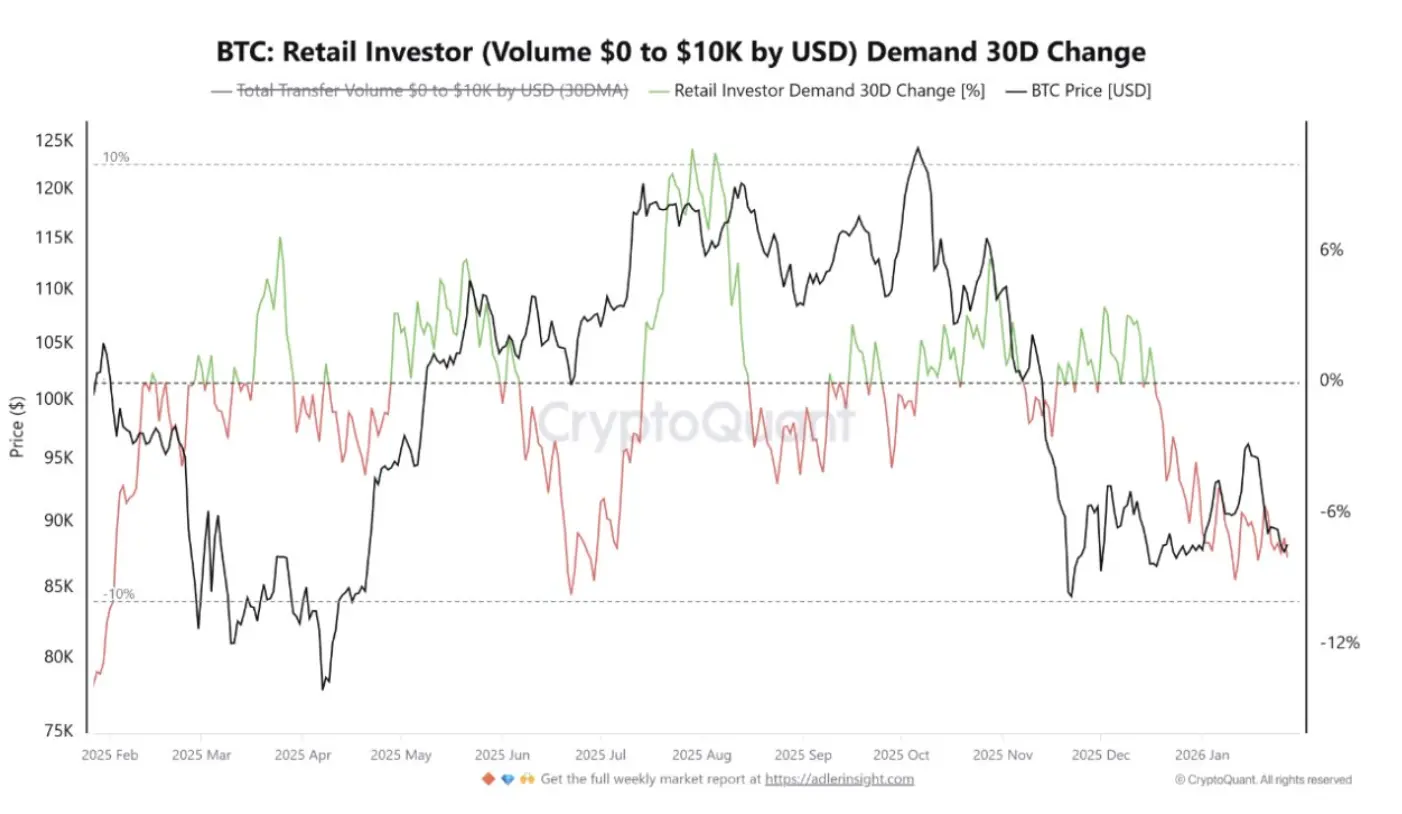

Meanwhile, retail investors are also withdrawing. On-chain data shows that small transactions between $0 and $10,000 have shrunk sharply in the past month, not only buying slowing down but also a substantial decrease in the number of participants. And when ETF buying disappears and retail investors exit, the market is left only with short-term traders and leveraged speculators, inevitably amplifying volatility.

Crypto Market Maturing, But Market Structure Remains Fragile

Additionally, according to Beincrypto, most coin holders are still in a profitable state. The Bitcoin Loss Supply indicator is low by historical standards, meaning a large number of筹码 (chips/holdings) have not yet experienced real pain. This often indicates that Bitcoin will fall further rather than having bottomed out. "Only when prices continue to探 (probe/decline), and more holders turn to losses, will the real panic selling begin."

However, according to Pantera Capital's outlook for this year's行情 (market trend), judging from historical cycles, the current duration of the decline for non-Bitcoin tokens has been on par with the bear markets of 2018 and 2022 (about 12-14 months), and market sentiment has also been compressed to near capitulation levels, which may mean it is接近 (approaching) a cyclical bottom.

Although the cryptocurrency market has become increasingly, it still cannot withstand the叠加 (overlay/combination) of multiple negative factors. It can be said that the U.S. stock sell-off, U.S.-Iran tensions, and the potential government shutdown acted as catalysts for this sharp decline, but the liquidity drought caused by ETF outflows and reduced retail demand points to an inherently fragile market structure.

If subsequent tech earnings reports fail to convey strong confidence, or if geopolitical conditions worsen further, Bitcoin and the crypto market may need to undergo deeper adjustments to regroup.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush