On Wall Street, ‘TACO trading’ is out of style, and everyone is now discussing a new trading pattern—‘NACHO’.

Since the U.S.-Israel airstrike on Iran on February 28th, the Strait of Hormuz has remained closed. Oil prices are now up over 50% from pre-war levels, and the market's expectation for Federal Reserve rate cuts in 2026 has been compressed from 2 cuts pre-war to the current 0 cuts. Yet, during the same period, the S&P 500 has hit record highs, rallying for six consecutive weeks—its longest winning streak since 2024.

Wall Street has given this seemingly contradictory market state a name: NACHO, short for ‘Not A Chance Hormuz Opens’. It's the opposite of TACO (Trump Always Chickens Out). TACO bets on ‘people backing down’—that Trump would retreat at critical moments. NACHO bets on ‘things getting stuck’—that this time, the Strait of Hormuz cannot be reopened with just one Truth Social post.

eToro market analyst Zavier Wong described this shift: ‘For most of the crisis, every ceasefire headline caused oil prices to plunge sharply. Traders kept betting on a solution that never arrived. NACHO means the market acknowledges that high oil prices are not a one-time shock; they are the current market environment itself.’

Two Diverging Lines in Early April

March 23rd was the tipping point where the TACO pattern failed. That morning, Trump announced on Truth Social that he had held ‘very good constructive talks’ with Iran and ordered the Pentagon to halt strikes on Iranian energy facilities for five days. S&P 500 futures rebounded nearly 4% from lows within minutes, instantly adding $1.7 trillion in market value. Brent crude fell from $109 intraday to $92.

Then, Iranian officials denied the talks took place. According to Iranian state media, a ‘senior security official’ called it a market manipulation tactic, stating no dialogue ever occurred. The gains were halved within two hours, with the S&P closing only +1.15% and Brent rebounding to $99.94.

That was the first time in 14 months that Trump's ‘backing down’ no longer moved the market effectively. The reason isn't complicated: backing down in the TACO pattern was one-sided, deliverable with a single post. The retreat on March 23rd required Iran's cooperation. When the counterparty didn't cooperate, the retreat turned into a lie.

From that day on, market behavior fundamentally changed. Brent crude never fell back to the pre-war level of $67 in the following six weeks, with its May average price still maintained at $109.57. In between, there were U.S.-Iran ceasefire agreements on April 7th and 8th, a brief return of oil prices to ‘initial war levels’ on April 17th, and news on May 7th that the U.S. and Iran were close to a deal. None of these ‘ceasefire headlines’ brought oil prices back to the baseline.

But the S&P headed north. It rose 10% in April alone, its strongest month since November 2020, setting 7 intraday all-time highs during the period. On May 1st, it broke 7,230 points intraday, closing at 7,398 points on May 7th.

The two lines completely decoupled in early April. In the TACO era, they moved together: threats came, oil and the S&P fell; backing down came, oil and the S&P rebounded. In the NACHO era, they speak two different languages: oil prices say ‘Hormuz is shut for good,’ while the S&P says ‘it's none of my business.’

Three Markets, Three Reactions

NACHO is not just talk; it's the same bet placed with real money across three separate derivative markets.

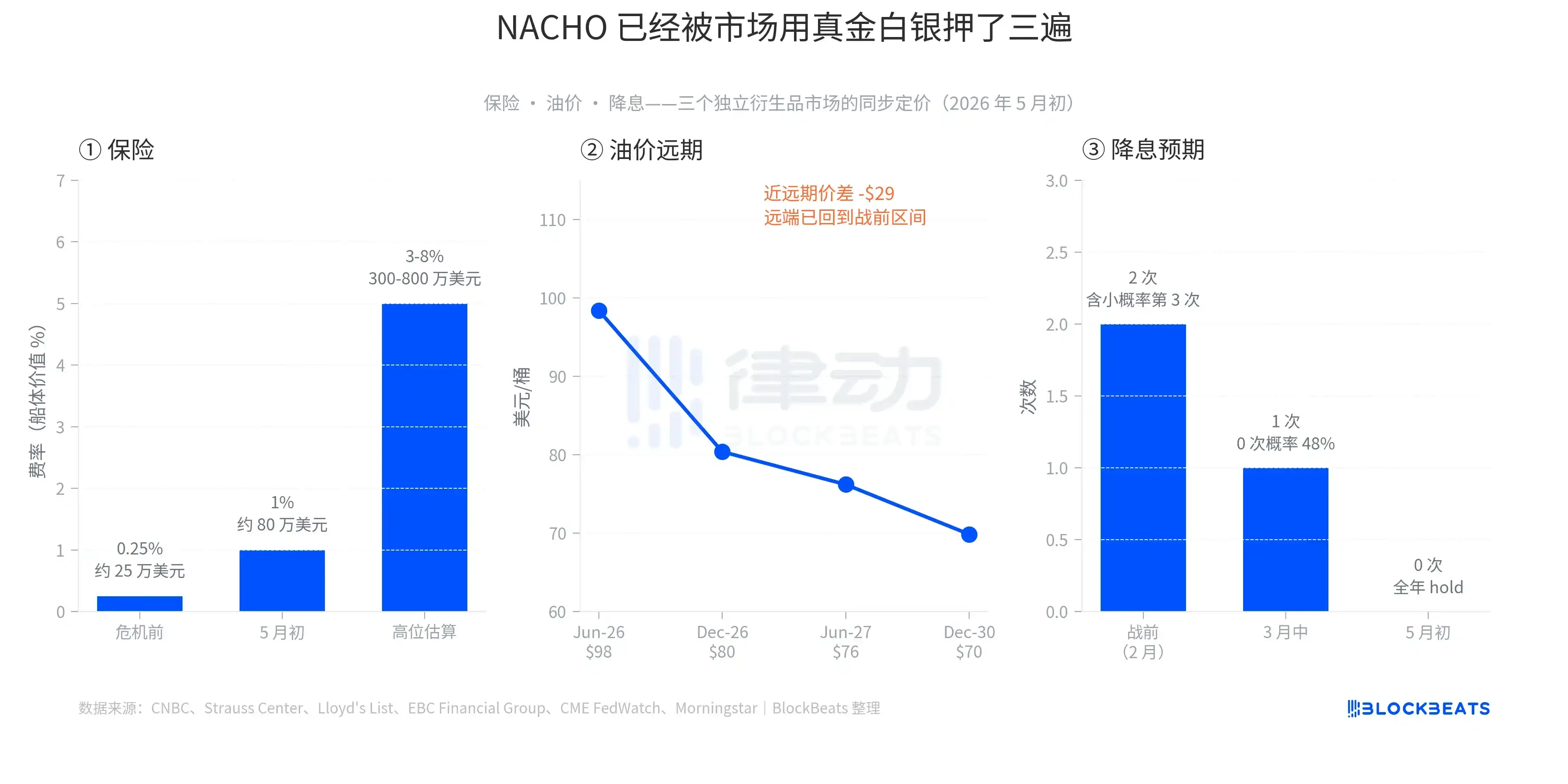

The first layer is insurance. According to historical data from the Strauss Center, war risk insurance rates for the Strait of Hormuz once soared to 3.5% of hull value during the 2003 U.S. invasion of Iraq, reaching 7.5% at the peak of the ‘Tanker War’ in the 1984 Iran-Iraq War after the attack on the Yanbu Pride tanker. The baseline before this crisis was 0.125% to 0.25%. By early May, this rate had entered the 1% range, with some policies surging to 3%–8%.

Converted to the insurance cost for a single Very Large Crude Carrier (VLCC) per transit, the fee has jumped from about $250,000 pre-war to the current $800,000 to $8 million. An insurer's job is to price risk. The practical implication of this layer is: if insurers simply won't provide coverage, shipowners won't risk uninsured transit. The ‘physical reopening’ and ‘de facto navigation’ of the Strait are two different things.

The second layer is oil prices. Early May data shows the Brent Jun-26 contract at $98.41, Dec-26 at $80.39, Jun-27 at $76.20, Dec-30 at $69.85. The spread between the front month and Dec-30 is about $28.5, one of the steepest backwardation (near-term price higher than long-term) structures in the past five years. This curve tells a very specific story: the market believes spot supply is tight but will eventually ease, with long-term prices returning to the pre-war $60–$70 range. In other words, high oil prices are not the final state but a bounded window. However, this window is long enough that traders won't bet on it ending suddenly.

The third layer is rate cuts. In early February 2026, the market expected the Fed to cut rates twice that year, with a small chance of a third cut. By mid-March, as oil prices surged, this was compressed to 1 cut, with a 48% probability of 0 cuts. On April 29th, the Fed held rates at 3.50%–3.75%. By May 6th, the CME FedWatch tool showed a 70% probability of another hold at the June meeting. For the entirety of 2026, the market had already priced in 0 rate cuts. Hedge fund legend Paul Tudor Jones even said in a May 7th CNBC interview, ‘Not even Volcker could get the Fed to cut rates now.’

All three layers have left their mark in the derivative markets—it's not just narrative; it's real money.

A Differentiated Market

The second, less obvious detail of NACHO is that it has already created differentiated pricing within the broader market.

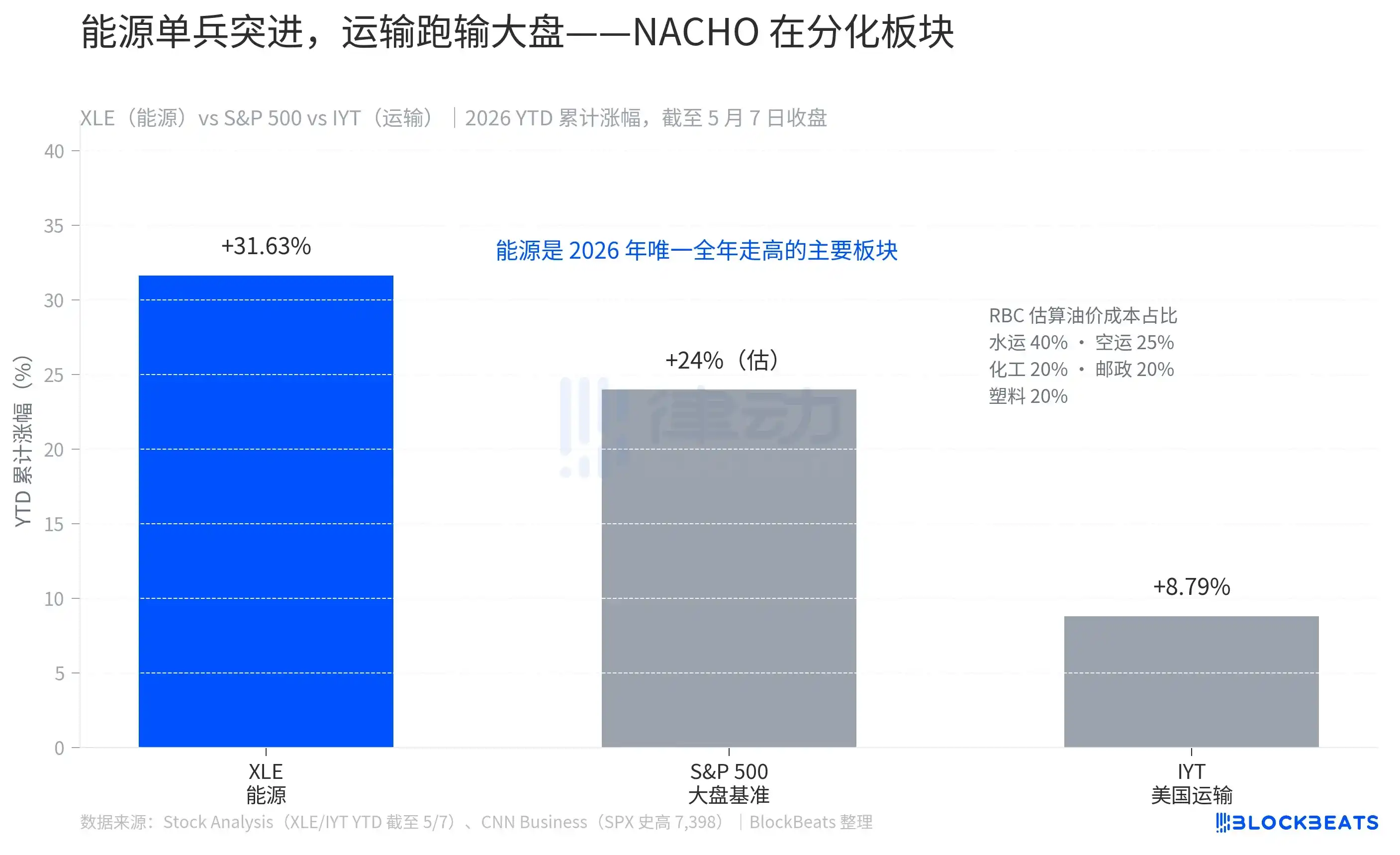

As of the May 7th close, the Energy Sector ETF (XLE, State Street's Energy Select Sector Fund) was up 31.63% year-to-date, the only major sector in positive territory for 2026. Over the same period, the S&P 500 rose about 24%. The Transportation Sector ETF (IYT, iShares U.S. Transportation ETF) gained only 8.79% year-to-date, underperforming the broader market by over 15 percentage points.

This gap is not random. According to RBC Capital Markets estimates, fuel costs constitute 40% of operating costs for the water transport industry, 25% for air transport, and 20% each for chemicals, postal/courier services, and rubber/plastics. If fuel is a major item on your cost sheet, NACHO hits you directly in the face.

XLE's 31.63% gain is not a short-term bounce; it's the result of 8 weeks of sustained outperformance. IYT's 8.79% gain isn't weakness; it's rising with the broader market while having its returns split by oil prices. The market has clearly told readers how NACHO calculates the odds—just look at how much the transportation ETF is underperforming the market.

But NACHO is not an indefinite bet; it has a very specific deadline: June 1st.

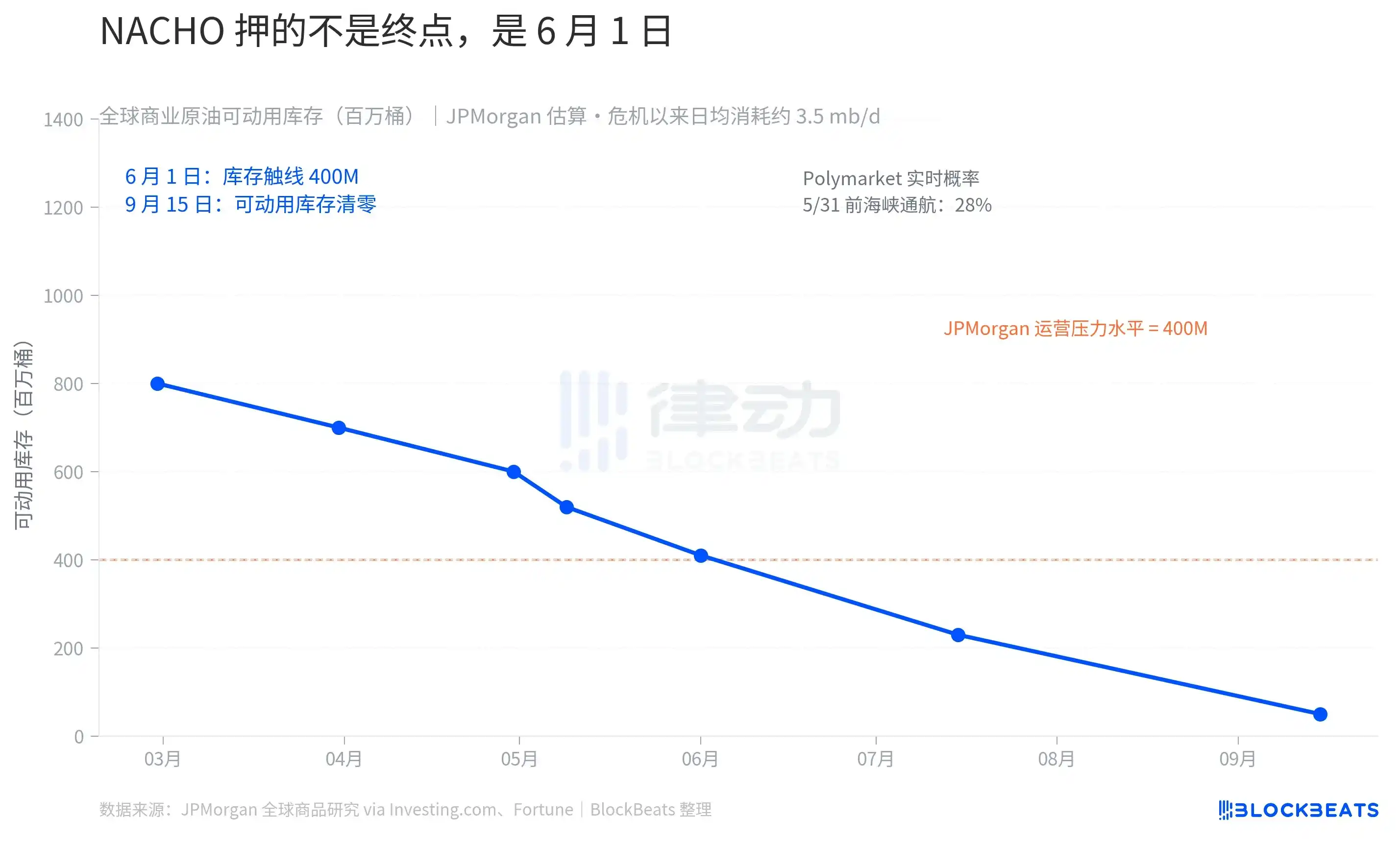

According to estimates from JPMorgan's commodity research team, global commercial crude oil inventories were around 8.4 billion barrels at the beginning of 2026, but only about 800 million barrels of that was ‘practically usable.’ The rest consisted of pipeline fill, tank bottom inventories, minimum terminal storage—the parts necessary to keep the system running daily. Since the crisis began, 280 million barrels have been drawn down, leaving roughly 520 million barrels of usable inventory. JPMorgan's exact words were, ‘Commercial inventories are expected to approach operational stress levels by early June.’

‘Operational stress level’ is a concrete physical concept. JPMorgan explains, ‘The system doesn't collapse because oil disappears; it collapses because the flow network no longer has sufficient working inventory.’ Once this line is breached, the only choices for companies and governments are to either squeeze the minimum inventory needed to maintain operations (which damages the infrastructure itself) or wait for new supply. If Hormuz remains closed until September, OECD commercial inventories could fall to the so-called ‘operational floor.’ According to a Fortune report, European jet fuel inventories are projected to fall below the 23-day supply threshold in June—a key industry warning line.

Prediction market odds are synchronized with the physical clock. According to Polymarket data from May 9th, the probability of ‘the Strait of Hormuz resuming normal traffic before May 31st’ is 28%, with only a 2% probability before May 15th. Active positions worth $9.92 million on that market are betting that NACHO won't fail at least within May.

The market is no longer trading Trump's next Truth Social post; it's trading the early-June inventory data for the Strait of Hormuz.