Author: Deep Tide TechFlow

Original Title: U.S. Small-Cap Stock Index Hits Record High, An Overlooked Crypto Cycle Signal?

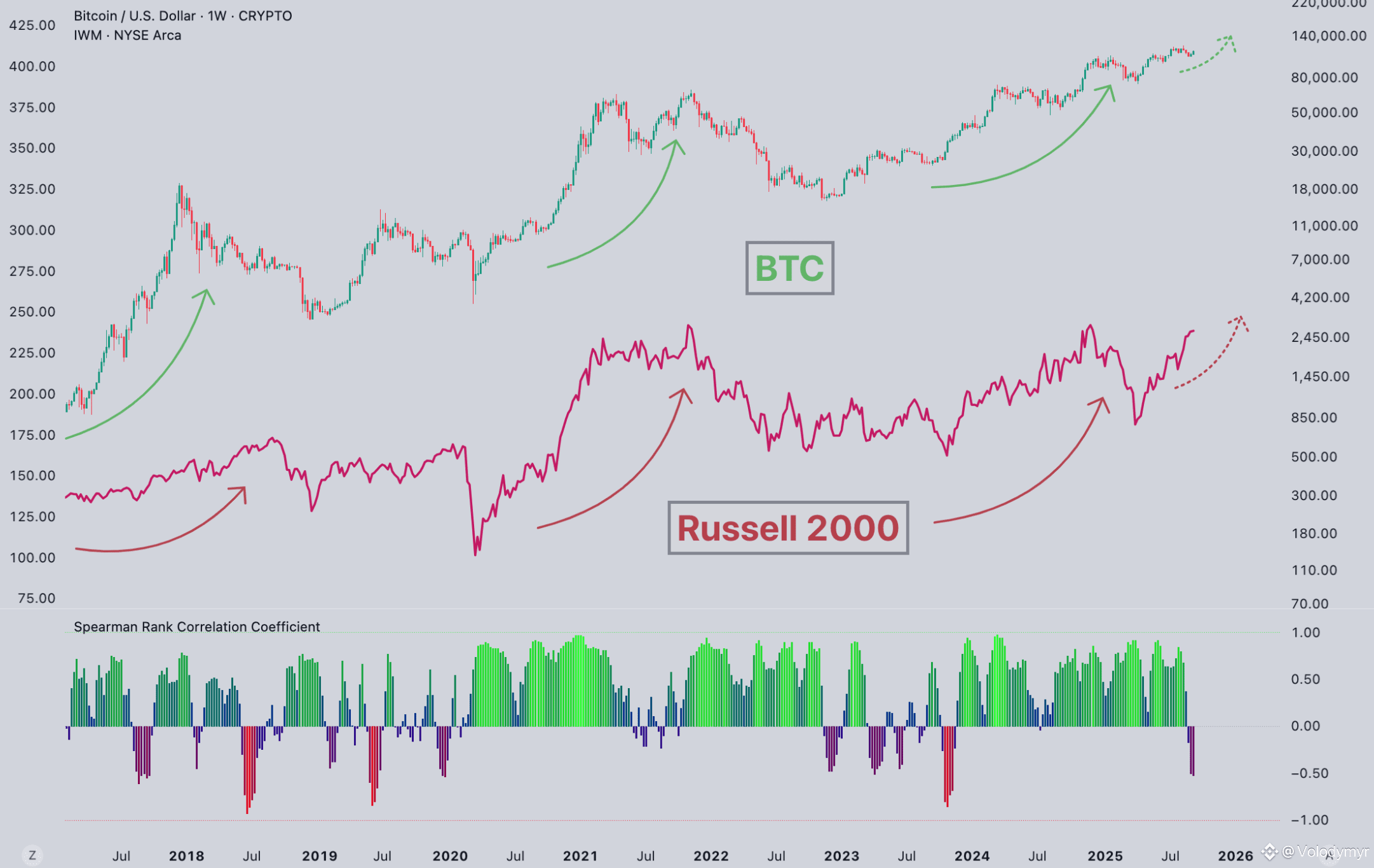

Three weeks into 2026, the Russell 2000 Index has risen 9%, breaking through 2700 points.

This U.S. small-cap stock index had been moving sideways for three years since its previous high at the end of 2021, only breaking through for the first time last November. It has now entered the "price discovery" phase, with no historical resistance levels to reference.

Recently, a view has been circulating: when the Russell 2000 broke out in 2016 and 2020, BTC also started a bull run, hitting both times. Now it has broken out again—will crypto follow?

Looking at the data, it does seem like a leading signal, at least historically validated.

The Russell 2000 tracks the 2,000 smallest companies by market cap in the U.S. stock market, with a median market cap of just over $1 billion. Compared to star stocks like Apple and Microsoft in the S&P 500, these small companies share a common trait: they rely mainly on bank loans for financing, not bond issuance.

When interest rates rise, their financing costs are the first to suffer; when rates fall, they are the first to benefit.

Therefore, traders like to use the Russell 2000 as a "risk appetite thermometer." A new high indicates that the market is willing to put money into higher-risk assets.

There is another layer of logic. Small-cap stocks are concentrated in the U.S. domestic market, unlike globally diversified companies like Apple and Microsoft. A rise in the Russell 2000, to some extent, reflects the domestic economic sentiment in the U.S.

2016 and 2020: Two Breakouts in the Small-Cap Index, Two BTC Takeoffs

First, the data.

In 2016, the Federal Reserve was nearing the end of its rate-hiking cycle, and Trump's election brought expectations of tax cuts, boosting risk appetite. BTC had just undergone a halving, with supply contraction meeting rising demand, leading to the 2017 bull run.

The 2020 breakout was even stronger. The pandemic caused a major crash, and the Fed went all out with money printing, pushing rates to the floor. Institutions entered the market on a large scale for the first time, with MicroStrategy and Tesla buying heavily, driving BTC from over $10,000 to $69,000.

The timing of the Russell 2000 breakout and the BTC bull market确实 aligns in both cases.

But there are only two historical samples.

Looking back to November 2024, the Russell 2000 first broke through its 2021 high. At the same time, BTC was already near $100,000.

From the April 2024 halving, BTC rose from $63,000 to the current $90,000, a gain of about 50%. Sounds good, but compared to the 5x and 27x gains in the same period of the previous two cycles, the difference is significant.

A few possible reasons.

First, institutional entry has dampened volatility. After the ETF approval in January 2024, giants like BlackRock and Fidelity entered the market, with ETFs alone absorbing hundreds of billions of dollars. Institutional money doesn't chase pumps and dumps like retail, smoothing out volatility. The upside is that crashes are less severe, but the downside is the lack of vertical rallies like in 2017.

Second, the marginal effect of halvings is diminishing. After the fourth halving, BTC's annual inflation rate dropped from 1.7% to 0.85%. Sounds like a halving, but 94% of BTC has already been mined. The dilution of new supply on the存量 is getting smaller, and the "supply shock" from halvings is weakening each time.

Third, BTC broke its previous high in March 2024, the first time it has done so before a halving. ETF expectations提前释放了一波 demand, so by the time the halving arrived, the利好 was already priced in.

Coincidence, or the Same Liquidity Logic?

The Russell 2000 and BTC—one is a U.S. small-cap stock index, the other a crypto leader—why would they move in sync?

My understanding is that they are sensitive to the same macro signals.

When the Fed signals easing, money moves out along the risk curve. First to government bonds, then to blue chips, then to small caps, and finally to high-beta assets like crypto.

A Russell 2000 breakout is like a green light in the middle of that chain.

A JPMorgan study last year noted that BTC has the highest correlation with small-cap tech stocks in the Russell 2000. The reason is that crypto projects rely on VC funding, and blockchain innovation is concentrated in small companies rather than large tech giants. Essentially, the people buying small-cap stocks and those buying crypto have similar risk appetites.

But I hesitate to call this a causal relationship. Two samples aren't enough statistically.

Moreover, in 2016 and 2020, BTC itself had its own halving cycle. The Russell 2000 might just have been another macro signal appearing concurrently, not necessarily leading.

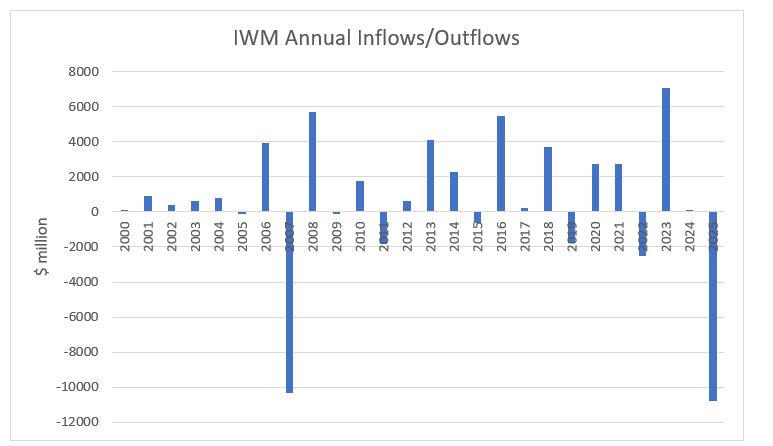

Additionally, an interesting phenomenon: although the Russell index is rising, money is flowing out.

In 2025, the Russell 2000 rose over 40%, but U.S. small-cap ETFs saw nearly $20 billion in net outflows for the year. This contrasts sharply with past bull markets—when the index rose, funds flowed in.

(Source: etf.com)

Another data point: about 40% of companies in the Russell 2000 reported negative earnings in Q3 2025, near a historical high. This proportion has more than doubled since 2007.

The index hits a new high, fundamentals are concerning, and money is still leaving.

How to explain this? One possibility is a few stocks driving the index; another is passive fund rebalancing. But either way, the "return of risk appetite" narrative takes a hit.

Lately, if you follow macro and finance content, you'll notice more voices on investment video blogs and crypto Twitter saying "the Russell 2000 breakout is a leading signal for BTC's rise."

The Russell 2000 breakout确实 was a signal present before the 2016 and 2020 crypto bull markets, and it's here again. It has value as an observation window, but my view is: don't use it as a trading signal.

Two samples can't establish causality, and this cycle has several variables different from before: ETFs changed the capital structure, volatility has been suppressed by institutions, and the halving effect is fading. The old script might not play out the same way.

The "resonance" between the Russell 2000 and BTC might only be answered once this cycle concludes.

Note:

Data sources: Yahoo Finance, TradingEconomics, JPMorgan Research, BeInCrypto. As of January 2026.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush