On July 1, Robinhood held a product launch event, announcing a series of new products at once.

The Robinhood Chain Layer 2 public mainnet officially launched. This is a network built on Arbitrum, focusing on tokenized real-world assets and DeFi applications.

Users can trade tokenized stocks on decentralized exchanges like Uniswap, Rialto, Lighter, and 1inch via Robinhood Chain, and use these assets in DeFi scenarios, including as collateral for lending or depositing into liquidity pools to earn yields.

With the mainnet launch, Robinhood's Stock Tokens are now fully accessible. Users can use related products in over 120 countries via the Robinhood Wallet, with availability varying by jurisdiction.

Simultaneously, Robinhood launched Robinhood Earn. This product allows users to lend out the USDG stablecoin via self-custody wallets, with an expected annualized yield of approximately 7%. The underlying lending infrastructure is provided by Morpho, with support from DeFi protocols like Steakhouse, Ethena, Spark, and Maple. The company states that insurance mechanisms have also been introduced to reduce risk exposure.

Additionally, Robinhood announced the expansion of its European perpetual futures products to cover commodities, ETFs, and forex markets, with plans to launch crypto trading in the UK. Following the acquisition of WonderFi, Robinhood's services have also entered the Canadian market.

Image Source: RootData

In the US market, Robinhood introduced Agentic Accounts for crypto users. Eligible users can connect AI models to Robinhood's trading infrastructure while retaining control over fund allocation and trading parameters.

On the day of the event, Robinhood's stock price closed up 8.35% and continued to rise during the US market session tonight.

This is not just a regular crypto product update. Robinhood is gradually placing stocks, cryptocurrencies, tokenized assets, stablecoin yields, perpetual futures, and AI trading tools into the same financial account system. The company's core identity was once a zero-commission brokerage; now, it seems to be moving closer to becoming an "everything exchange."

The significance of Robinhood Chain lies here as well. It's not just about adding another Layer 2; more importantly, Robinhood doesn't want to be just a front-end on others' chains in the long term.

Over the past few years, the common approach for financial companies entering the crypto industry has been to integrate with existing public chains. The platform handles users, interfaces, and product packaging, while underlying settlement, gas fees, liquidity, and DeFi applications occur on external networks.

This model allows for quick launch and leverages existing ecosystems. However, for financial platforms that already have massive user entry points, a long-term issue arises: users are within their own app, but assets and settlement happen on someone else's turf.

For Robinhood, this issue is particularly sensitive. It has nearly 28 million funded accounts, with users already accustomed to trading stocks, options, and crypto. This means Robinhood is no longer just a stock trading app but is evolving into a comprehensive financial entry point covering multiple asset classes and trading forms.

In this context, launching its own chain becomes a natural extension. If Robinhood only directs users to external DeFi, it remains merely a channel provider. If tokenized stocks, USDG lending, AI agent trading, and future RWA products all run on its own chain, it can more deeply control trading, settlement, collateral, yields, and asset flows.

The platform transforms from an interface provider to an owner of financial rails—this is a deeper change.

Following the launch of Robinhood Chain, protocols like Uniswap, 1inch, Lighter, Morpho, Chainlink, BitGo, Ethena, and EtherFi have successively integrated, covering trading, liquidity, lending, oracles, custody, and cross-chain functions.

More notably, the new DEX Arcus, launched by dYdX, chose to deploy on Robinhood Chain rather than dYdX's own chain. This decision sparked controversy within the dYdX community, indicating that institutional chains are competing not just for end-users but also for protocols, liquidity, and product attention.

This is why more financial companies are launching their own chains. Circle's launch of Arc is a stablecoin issuer wanting to tighten its grip on the circulation and settlement rails of USDC. Coinbase's launch of Base is an exchange hoping to keep user, asset, and developer activity within its own ecosystem. Robinhood Chain represents brokers and retail trading platforms starting to compete for the on-chain settlement layer of tokenized assets.

Their asset endowments differ, but they face the same problem. If they don't build their own settlement layer, they risk transitioning from being masters of user and asset entry points to tenants on others' chains.

This wave of chain launches also differs from the previous public chain boom. The last wave focused more on TPS, ecosystem incentives, and fundraising narratives. Now, when financial companies launch chains, the focus shifts to stablecoin gas payments, compliance privacy, RWA issuance, on-chain collateral, AI agent trading, institutional settlement, and internalizing yields.

However, for Robinhood, what's truly noteworthy may not be just Robinhood Chain.

Just last month, Robinhood announced laying off 10% of its staff, about 290 people, expecting to incur approximately $20 million in severance and benefit restructuring costs, plus about $8 million in stock-based compensation expenses. CEO Vlad Tenev stated that while the company's current business condition is very strong, it must avoid excessive institutional hierarchy and needs to keep the team lean and highly focused.

On one hand, reducing organizational costs; on the other, intensively launching new businesses. The signal from Robinhood is clear: it doesn't want to be just a zero-commission broker or just a crypto trading entry point; it aims to keep more trading, issuance, settlement, and yield processes within its own system.

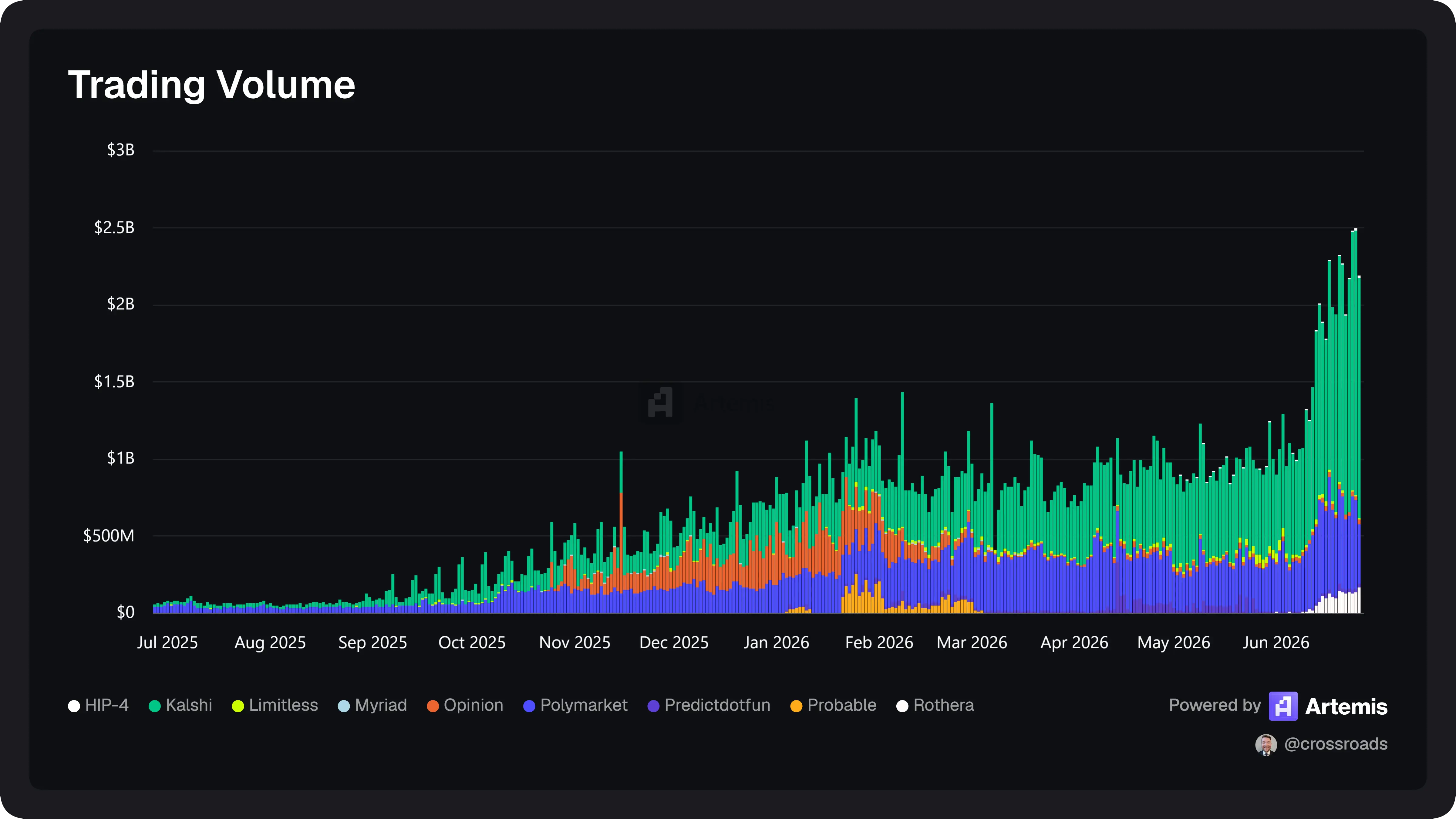

And the backdrop to all this is that due to shrinking institutional trading volume, Robinhood's cryptocurrency transaction revenue is plummeting, nearly halving to $134 million in Q1, with Q2 expected to fall below that figure. Currently, the company's revenue growth is mainly driven by a surge in prediction market revenue.

According to calculations by analyst Dr. Crossroads, as of June 25, Robinhood's Q2 event contract trading volume has reached approximately 12.3 billion contracts. Based on a $0.01 fee per contract, this business is expected to generate at least $123 million in revenue for the quarter, with annualized revenue potentially reaching $500 million, likely marking the first time this business's revenue exceeds its crypto trading revenue.

Its newly launched prediction market platform, Rothera, achieved over 900 million contracts in trading volume in its first week, contributing nearly 60% of the company's potential contract trading growth. Simultaneously, the company plans to cut fees from $0.02 to $0.006 per contract, using price advantages to keep trading volume and profits within its own ecosystem.

Ultimately, the product launch is about ambition, while the financial report is about reality. How many developers Robinhood Chain can attract is important, but whether the prediction markets can sustainably fill the revenue gap left by declining crypto spot trading will also impact the market's repricing of this company.

For Robinhood, the real question is no longer just whether it can launch a chain, but whether it can turn stocks, crypto, prediction markets, tokenized assets, stablecoin yields, and AI trading into a sustainable business within a single account system.