Original | Odaily Planet Daily (@OdailyChina)

Author | Ethan (@ethanzhang_web3)

On January 29, the U.S. Securities and Exchange Commission (SEC) released a new guidance document on tokenized securities. The issuance of this document coincided with the rescheduling of the originally planned public event "SEC and CFTC Collaborative Regulation"—the interagency coordination dialogue, originally set for January 27, was adjusted to 2:00–3:00 PM EST on January 29.

Now that this interagency coordination dialogue has concluded, the SEC has preemptively used this guidance document to send a clear signal: in constructing the regulatory framework for crypto assets, the SEC has chosen to start with "structural clarification" as an entry point, delineating and clarifying the identities of tokenization practices in the market.

Odaily Planet Daily will, through this article, break down how this document redefines the regulatory logic of "tokenized securities" and which hot projects will face critical tests as a result.

Core Objective: Re-labeling "Tokenization Practices"

Directly turning to the original text of the "Statement on Tokenized Securities," the document's goal is straightforward to the point of being一目了然: the SEC is not establishing a new framework for tokenized securities but is attempting to answer a more fundamental question—under existing federal securities laws, into which category of financial instruments should the various tokenization operations in the market be classified?

Why is such "labeling" necessary? Because current market tokenization practices are extremely chaotic: some involve securities issuers themselves using blockchain to register equity, while others involve third parties casually issuing tokens claiming to be "pegged to a certain stock"; some on-chain assets can actually trigger official equity changes, while others don't even have a known issuer. These differences blur regulatory boundaries, and investors can easily be misled by the name "tokenized stock." What the SEC aims to do is first "structurally sort out" these chaotic phenomena.

According to the document, tokenized securities are broadly categorized into two types: issuer-led tokenized securities (led by the securities issuer or its agent) and third-party-led tokenized securities (initiated by third parties unrelated to the issuer).

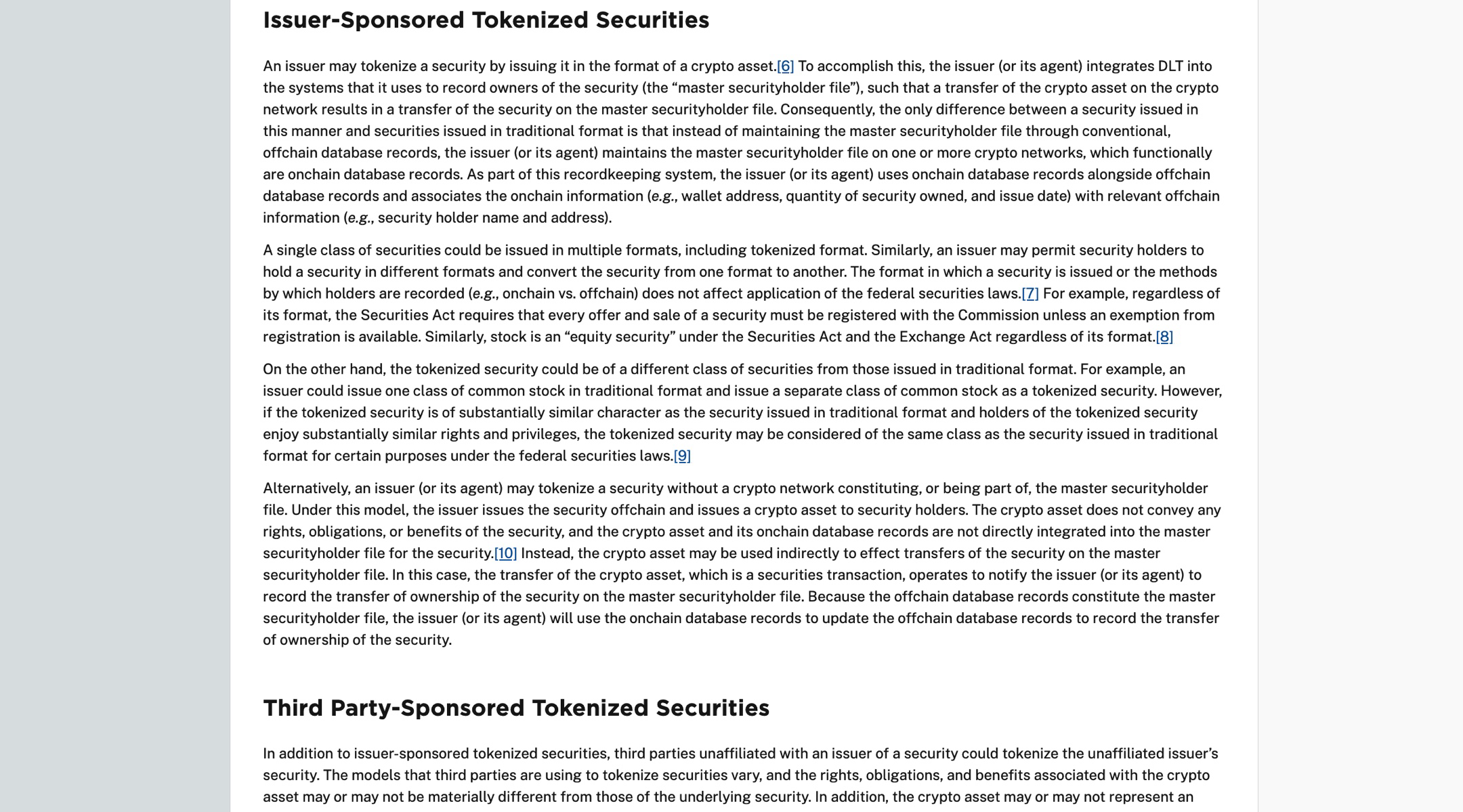

Issuer-Led: Technological Upgrade, No Change in Rights Essence

In the issuer-led model, blockchain is directly integrated into the securities holder registration system. Whether the on-chain ledger is used as the primary registration system or in parallel with an off-chain database, the core logic remains the same—the transfer of on-chain assets simultaneously triggers changes in the official holder register for the security. The SEC particularly emphasizes that this structure differs from traditional securities only in the registration technology; it does not involve changes in the nature of the security, rights and obligations, or regulatory requirements. The same class of security can exist simultaneously in traditional and tokenized forms, and issuance and trading still fully apply the Securities Act and the Securities Exchange Act.

The document also mentions that issuers could theoretically issue tokenized securities of a "different class" from traditional securities, but the SEC adds a key qualification: if the tokenized security is "substantially identical" to the traditional security in terms of rights and obligations, it may still be considered the same class in specific legal contexts. This statement is not encouraging structural complexity but reiterating that the judgment standard is always based on "rights and economic substance."

Third-Party-Led: Prudential Supervision, Risks and Rights Need Reassessment

In contrast, third-party-led tokenization structures are placed under a more cautious regulatory lens. According to the document, when a third party tokenizes an existing security without the issuer's participation, the on-chain asset may not represent ownership of the underlying security, nor does it necessarily constitute a claim against the issuer. More critically, token holders must additionally bear the risks of the third party itself (such as custody risk, bankruptcy risk), risks that do not exist when directly holding the original security.

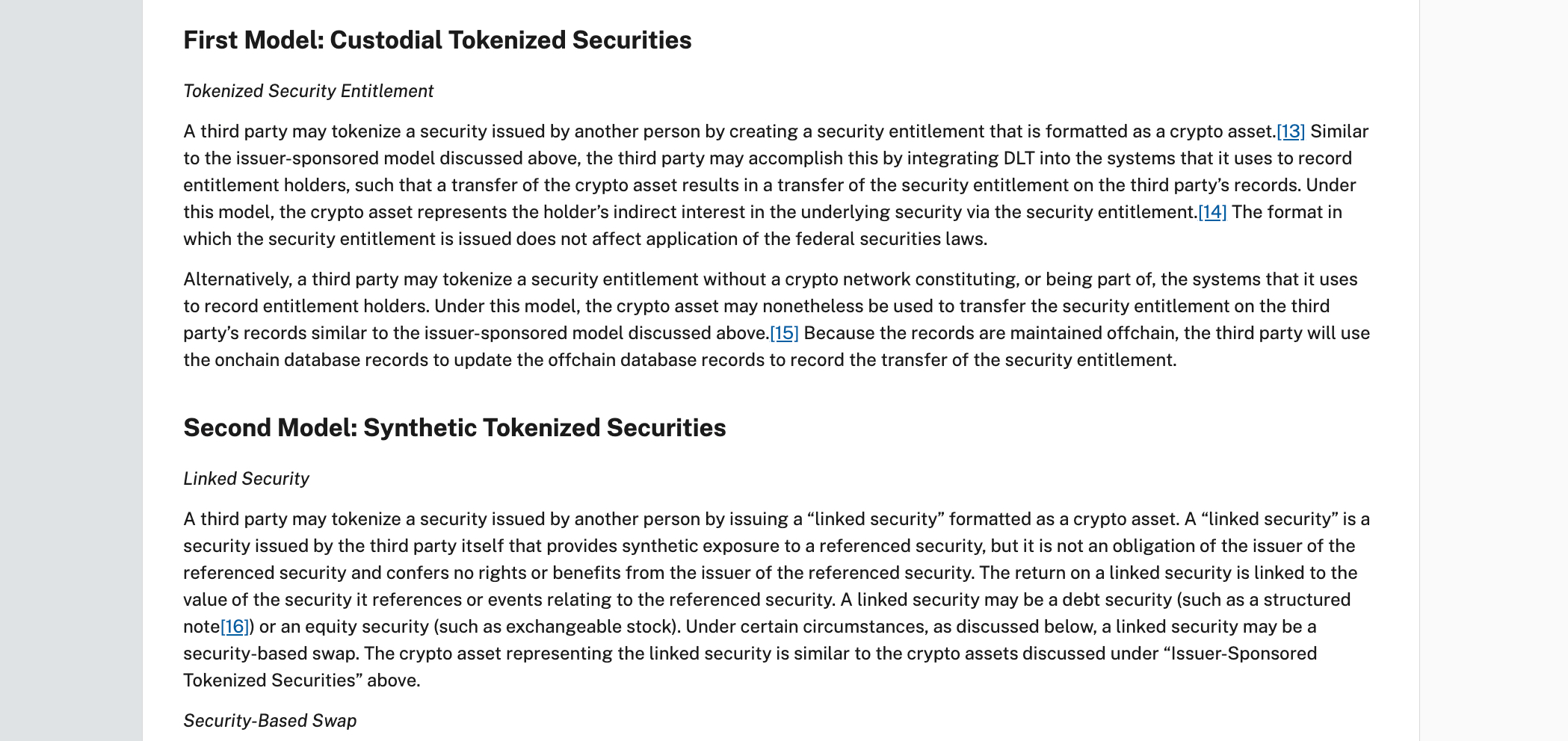

Based on this difference, the document further divides third-party tokenization into two typical models:

- Custodial Tokenized Securities: Essentially "securities entitlement certificates," meaning the third party uses the token form to prove the holder's indirect interest in the securities it custodies (e.g., tokenized entitlement certificates issued by a custodian);

- Synthetic Tokenized Securities: Closer to structured notes or security-based swaps, financial instruments issued by a third party to track the price performance of the underlying security, granting no shareholder rights (e.g., tokenized derivatives pegged to stock prices).

Although third-party-led tokenization structures carry many risks, they still meet certain demands in the market. For some investors, such products offer a relatively convenient and low-cost investment avenue. For example, some small investors may not be able to directly participate in trading stocks of certain large companies. Through custodial or synthetic tokenized securities issued by third parties, they can gain similar investment opportunities with a lower barrier to entry. Additionally, some investors are attracted by the innovative form and potential high returns of tokenized securities, and although they may understand the risks, they are still willing to bear certain risks for possible rewards.

Core Principle: Form Does Not Change Liability or Attribute

Throughout the text, the SEC repeatedly emphasizes not the compliance of the technological path, but an unchanging regulatory logic: as long as the economic substance of a financial instrument meets the definition of a security or derivative, the application of federal securities laws will not change due to "tokenization". Name, packaging method, or even the use of blockchain are not determining factors.

From this perspective, this new guidance is more like a "structural clarification note." It does not make value judgments on the future of tokenized securities but clarifies a premise: in the U.S. legal system, tokenization can only change the form, not the liability and attribute. Subsequent market developments will unfold under this premise.

Back to the Real-World: Which "Tokenized Stocks" Are Being Redefined?

If interpreted only at the textual level, this new guidance might seem like just a clarification of classification structure; but placed in the context of the real market, its direction is quite clear. What it responds to is precisely a batch of "tokenized stock" practices that have already come to the forefront.

The most typical division first appears on the point of whether the issuer participates. In the path of direct issuer participation, tokenization is seen more as a technological upgrade of the registration and settlement system. Around the time this guidance was released, asset management firm F/m Investments had already submitted an application to the SEC, hoping to maintain the holder records of its Treasury ETF on a permissioned blockchain. The common feature of such attempts is that: blockchain is merely incorporated into the existing securities infrastructure, and the legal relationship between the issuer and investors remains unchanged. Precisely because of this, although this path progresses slowly, it has always been within a framework that the SEC can understand and engage with.

In stark contrast is another type of practice that entered the market earlier and is more controversial. Taking Robinhood's "tokenized U.S. stocks" product launched in Europe as an example, its trading experience and price linkage methods are highly similar to real stocks, but the related tokens are not authorized by the issuers. Similar market chaos was also reflected in rumors about "OpenAI tokenized equity"—previously, some third-party platforms claimed to offer "OpenAI on-chain equity certificates," attracting investor attention. Subsequently, OpenAI publicly denied any association with any "tokenized equity", an action that actually highlighted the core problem of such structures—the on-chain asset does not represent a direct claim to the issuer's equity. In the SEC's context, this type of product is closer to a synthetic exposure constructed by a third party, rather than a real stock.

A similar situation also appears in "tokenized stocks" products launched by some crypto-native platforms. Whether providing securities entitlement certificates through custody or tracking stock price performance through contract structures, these products function "like stocks," but in terms of legal relationship, the entity investors face has shifted from the issuing company to the platform or intermediary itself. This is precisely the real-world context in which the SEC repeatedly emphasizes third-party risks in the new guidance.

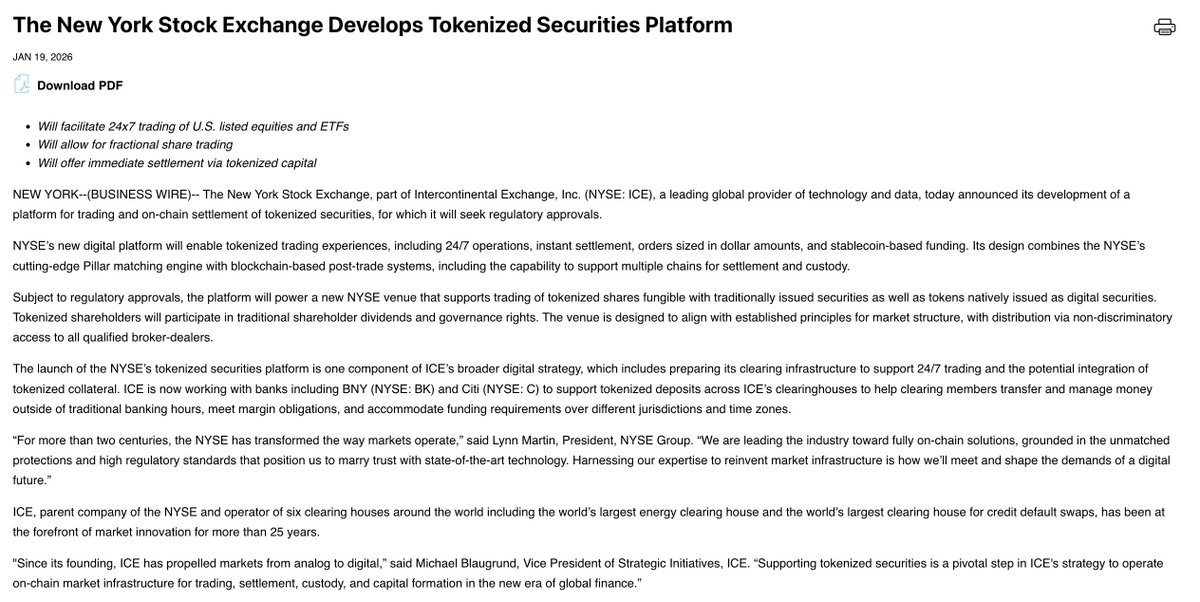

Conversely, those frequently mentioned attempts that consistently emphasize "compliance first"—such as Kraken's xStocks plan, and internal explorations around tokenized stocks and ETFs by the NYSE and DTCC—their commonality lies not in how advanced the technology is, but in whether the issuer, custody, clearing, and regulatory responsibilities are fully integrated into the existing system. The slow progress of these projects恰恰说明恰恰说明 (precisely illustrates) that there is no "get on the bus first, then buy a ticket" shortcut for tokenization in the U.S. market.

Conclusion: Tokenization is Not a Shortcut, But a "Revealing Mirror" of Responsibility

The essence of this SEC guidance is an "identity calibration"—before tokenization moves from concept to落地 (landing), first clarify "what is equity, and who is bearing the responsibility."

In U.S. regulatory logic, blockchain is never a tool to circumvent securities laws. Whether tokenization can be established depends on whether the issuer participates, whether rights and obligations are clear, and whether risks are correctly assumed: if these three conditions are met, it is a technological upgrade of the existing financial system; if one is missing, the so-called "tokenized stock" is, in the eyes of regulators, another type of financial product.

Therefore, the boundary drawn by this document is not one of "permitted vs. prohibited," but rather a "screening question on responsibility"—it is reclassifying the tokenization practices in the market: some are evolving towards securities infrastructure, while others must正视 (face squarely) their "non-equity" nature.

For the market, this might not be a bad thing. At least from now on, tokenization is no longer a vague and enticing label, but a path that must be taken seriously, with no room for speculation.

Related Links

《OpenAI Angrily Denounces Robinhood's Unauthorized Use, Whose Interests Do Tokenized Stocks Touch?》

《Robinhood Rewrites the Global Trading Landscape, Stock-like Tokens Enter an Era of Dimensionality Reduction Strike》

《NYSE Plans to Launch 7*24 Hour Tokenized Stock Trading, "Competitors" Are Stunned》