Author: Yuanchuan Investment Review

A recent unemployment report from Anthropic sent chills down the spines of financial professionals.

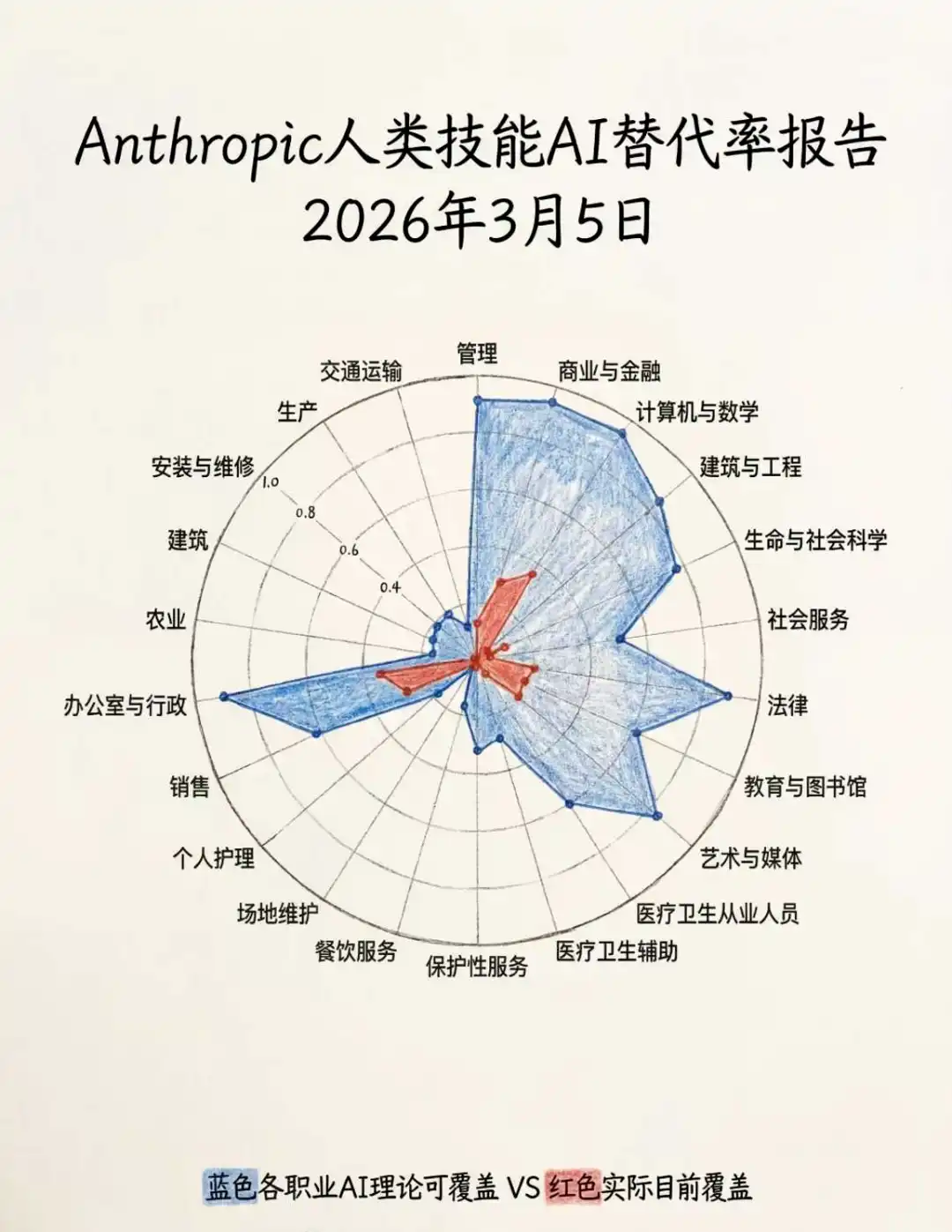

The report indicated that the substitution rate for financial positions is as high as 94%, ranking second among all professions, but the current actual substitution rate is only 28%, leaving immense room for growth in the future. Fortunately, 30% of professions are almost unaffected, so financial professionals can still consider reemployment opportunities such as dishwashers and plumbers.

After being in the industry for a long time, one always feels anxious—financial professionals live in a world of "comparison," with daily pressure from sales evaluations and performance rankings. Not learning creates a sense of unease.

For example, after the Spring Festival holiday, while some financial registrars were still engaging in Q&A with chatbots upon returning to their desks, their colleagues at the next desk were already raising eight lobsters, passionately arguing about the rise and fall of crude oil.

The financial industry never rejects efficiency, from manual order reporting to programmatic trading, from offline bank sales to internet-based distribution. But this time, AI is not replacing inefficient financial tools but the people behind them who are inefficient. After all, the highest cost in the financial industry is people. Behind the profits of asset management companies lies the comparison of how to manage more money with fewer people.

Thus, private equity firms have begun embracing advanced productivity: Diewei Asset Management offers online courses on how to tame "digital researchers" that work autonomously 24/7; Mingxi Capital uses Manus to automatically generate promotional materials for dividend index enhancement, with layouts rivaling the sophistication of the magazine era. Even clients have become more cautious—while wealth managers are promoting popular private equity funds, they themselves turn to Douban to ask whether they should buy them.

The private equity industry is gradually entering its "Detroit: Become Human" moment, with substitution already taking place at every step of the mature chain: investment research, operations, and sales.

Salaries vs. Token Costs

In a competitive environment where operational costs remain high and Alpha is increasingly difficult to obtain, human efficiency is a metric that private equity bosses rack their brains to optimize every night before bed.

In the private equity industry chain, researchers' salaries are generally not low. According to Mulifang data, quantitative equity researchers typically earn an annual salary of 800,000 to 1.5 million yuan, while subjective researchers earn slightly less. However, there are occasionally astonishing incentives—earlier this year, a subjective researcher at a billion-yuan fund received a year-end bonus of over 20 million yuan for recommending Nvidia.

If private equity firms can successfully rely on AI for investment, they can save tens of millions in costs. If AI works 24/7, it reduces the hourly wage while increasing output. Expenses like travel, overtime, transportation, and meal allowances, which would otherwise be deducted from the boss's Carried Interest, are not required by AI.

In the asset management field, all technological advancements essentially boil down to two words: improve efficiency and reduce costs. Private equity bosses don’t care whether AI can truly think like a human; they only care whether the work gets done.

Howard Marks calculated the economic account: if AI can produce the analytical results of a research assistant with an annual salary of $200,000, it doesn’t matter to the payer whether it is truly thinking or merely pattern matching. The key is whether the work output is reliable enough to be useful.

After the Spring Festival, eight securities firms’ quantitative teams collectively released "lobster-raising" tutorials, accelerating the process of replacing human researchers. They tested OpenClaw, which can actively produce research results like a human.

On the Jinmen APP, a roadshow titled "OpenClaw: From Beginner to Master" by Kaiyuan Quantitative was played 4,839 times; Northeast’s Xu Jianhua promoted 20 skills that can skyrocket investment research efficiency tenfold; Fangzheng’s Cao Chunxiao used lobsters to replicate the PB-ROE strategy, the cup-with-handle stock selection strategy, and fully automated factor mining and backtesting.

Upon closer thought, this is equivalent to simultaneously OTA-updating the skill sets of Buffett, O’Neil, and Simons.

The studious trader

While sell-side firms are vigorously promoting, buy-side firms are learning actively. A Beijing-based private equity firm, fearing contamination of its main systems, issued new computers to each researcher and provided a 50,000-yuan token subsidy specifically for raising lobsters [1].

Yang Xinbin of Snowball Asset Management trained two lobster researchers, stating that he now has more conversations with AI than with humans. The AI Agent he independently trained can accomplish in two days what a mature quantitative researcher might take half a year to do, with even greater potential.

Paul Wu of Qinyuan Investment has gradually integrated AI into various departments, finding that AI can complete closed-loop tasks in some roles and operate independently with iterations. He foresees that in the near future, company expenses will shift to purchasing and maintaining an Apple analyst agent, and later perhaps an investment portfolio advisor named Paul.

In the past, many private equity firms suffered from wear and tear in research conversion—researchers felt fund managers were incompetent, while fund managers felt researchers were useless. The emergence of OpenClaw has given private equity bosses a glimpse of a new possibility: they no longer have to endure the internal friction of磨合 with mediocre researchers or worry about core researchers being poached by competitors with high salaries.

In terms of characteristics, lobsters meet all the ideal expectations fund managers have for researchers: they work around the clock without breaks or slacking; they have long-term memory沉淀, recalling key data effortlessly; they are absolutely loyal and obedient, never leaving to start their own firms with core strategies; they continuously self-iterate, unlike old-school researchers who become stuck in their ways and are淘汰 by the times.

If the cost of silicon-based tokens is far lower than carbon-based salaries in the future, how can private equity bosses resist an AI researcher that is obedient, useful, and trainable?

Substitution Isn’t Just Because of Lobsters

While subjective private equity is still weighing whether token costs are cost-effective, quantitative firms, with their self-built computing infrastructure, have already compressed token costs to extremely low levels. However, they remain unusually calm in the face of this热潮.

"OpenClaw is nothing more than a semi-finished product, like a toy, in the quantitative technology circle," a senior quantitative professional from Shanghai told me. Its significance lies in lowering the technical threshold for subjective institutions and retail investors, providing a clear cost recovery path for the massive upfront infrastructure investments of large model companies. But it holds little significance for严肃的生产 environments like quantitative investment.

Another top quantitative professional was more blunt, calling the lobster phenomenon in the financial circle akin to a pyramid scheme. OpenClaw has characteristics like randomness, non-systematicity, and low security, which could introduce significant uncertainty into the entire quantitative system.

Cui Yuchun of Xuntu Technology believes there is no need for anxiety, as OpenClaw is not advanced productivity in the quantitative circle:

Lobsters are even significantly weaker than Agents like Manus and Kimi in terms of Agent optimization and tool invocation (involving investment research browsers, writing, data analysis tools, etc.). For a researcher without a programming background, it takes 5-10 hours to deploy and launch, and most tasks cannot achieve results above 60 points.

While retail investors using the China Stock Analysis Skill via lobsters for stock selection feel like they’ve opened a door to a new world, quantitative firms have already built Multi-Agent platforms. With a richer arsenal of Agents, they碾压 lobsters. However, the operation of this powerful system may not require more humans.

Traditional quantitative investment research systems typically adopt a pipeline architecture: data cleaning → factor calculation → model prediction → portfolio optimization. In the AI era, some institutions have begun simplifying this to role分工 → tool invocation → workflow design, akin to top overseas quantitative firms like Man Group. Standardized, repetitive tasks are gradually being taken over by AI Agents, eliminating the need for so many researchers to be异化 in factor sweatshops.

For example, Xiyue Investment’s Apollo AI multi-agent system embeds AI Agents into various links such as investment research, data, trading, and operations. Founder Zhou Xin形容 it as having seven or eight hundred additional AI employees.

With quantitative firms' sci-fi-like "unmanned factory"碾压 from the front and retail investors reducing information asymmetry with OpenClaw from the rear, subjective fund managers in the middle efficiency zone are in an awkward position—watching the information painstakingly produced by their researchers, being降维打击 by quant above and步步紧逼 by retail below, inevitably falling into the着急 of AI FOMO (Fear Of Missing Out).

During the Spring Festival, I read the annual report of a top subjective manager in Shenzhen, who lamented that fund managers have excessively high expectations of researchers:

Fund managers hope researchers can remain sensitive to the market, promptly identify opportunities, provide leading research and judgments ahead of peers, and even stay within the "core circle" at all times. If a researcher can achieve this, why would they need a fund manager? They could simply trade stocks on their own to make a fortune. Why would they serve a fund manager?

Thus, he lowered his expectations—researchers are only responsible for researching specific targets and issues. They neither need to discover opportunities nor provide investment recommendations; these are the fund manager’s responsibilities.

Conversely, if what a subjective fund manager needs is merely someone who doesn’t penetrate the core of the industry front lines and only tracks targets through desk analysis, isn’t such a researcher the next to be replaced by an AI Agent?

Epilogue

Being in the A-share market these past two years feels like being put on fast-forward.

Especially in the first half of the year, there have been many events. Last Spring Festival, Deepseek was released; during the Qingming holiday, there was talk of violent tax increases; and this Spring Festival, everyone was raising lobsters. Before the first month was even over, war broke out in the Middle East. The brains of financial professionals have been in a state of overload, and it’s hard to remember when the last holiday without studying was. At least as a small editor, my brain’s computing power is already insufficient.

I recall that two years ago, when communicating with fund managers for articles, I often heard them happily describe their work state with an awkward sentence—"I tap dance to work every day." But in recent exchanges, they discuss the "iteration" organized by their teams, the "iteration" of investment philosophies, and the "iteration" of industry认知 without smiles.

AI is developing so fast, peers are improving so quickly—it seems that only through iteration can one avoid being淘汰.

The industry is still too anxious.

AI doesn’t understand human nature; it cannot predict whether the transactions in the A-share market, crowded with retail investors, are based on third-order or fifth-order derivatives at any given moment; AI lacks empathy—it cannot understand why someone would hold onto two oil stocks套了 for so many years, waiting only for the day they break even; AI cannot take responsibility—it won’t be堵在门口 by investors for losing 30%, nor does it need to憋 apology letters reflecting on its soul and检讨自我.

If AI replaces all fund managers and researchers in the future, the efficient market hypothesis would hold true, there would be no所谓的 Alpha, and it would be almost impossible for another Buffett to emerge.

So the real question is, in the future asset management industry, when AI takes over data scraping, model running, and report writing, what is left for humans? What remains is precisely the passion for investing, the intuition for uncertainty, and the reason to stay even when criticized for researching less effectively than AI.

We cannot change the trend of AI’s increasing proportion, but we can change the mindset of being busy coping and tired of chasing.

Just like in the game "Detroit: Become Human," the ultimate choice players must make is not to eliminate AI or submit to it, but to decide what roles humans and AI should各自 play.