Author: Delphi Digital

Compiled by: AididiaoJP, Foresight News

The size of the cryptocurrency options market far exceeds most people's perceptions. Trading volume for cryptocurrency derivatives on the Chicago Mercantile Exchange (CME) is 46% higher than the record high set last year. Institutional investors need clear risk management tools to hedge large positions, and options are the only cryptocurrency instrument that provides this functionality.

Reshaping the Landscape

By mid-2025, the total open interest in Bitcoin options reached $65 billion, surpassing futures open interest for the first time. Futures are leverage tools, while options allow funds to set a cap on losses for their $500 million Bitcoin holdings by paying a premium. This turning point indicates that tools with defined risk functions are gradually replacing pure leverage tools.

This growth has been concentrated on two platforms. Deribit has been the mainstream platform for cryptocurrency options trading for years. After being acquired by Coinbase for $2.9 billion in 2025, it gained institutional-grade endorsement. Meanwhile, IBIT options, launched in late 2024, brought traditional financial capital into this field. The options market is expanding rapidly, but the vast majority of trading still requires intermediaries.

On-Chain Options Are Still in Their Infancy

The market share of decentralized derivatives has climbed from 2% to over 10% in two years. Hyperliquid has proven that decentralized exchanges (DEXs) can rival centralized exchanges in speed and transparency. However, no similar representative project has emerged for on-chain options yet.

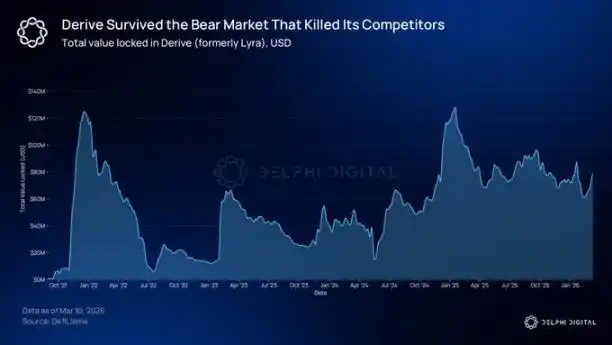

@DeriveXYZ remains the leading on-chain options protocol, with a nominal options trading volume exceeding $700 million in the past 30 days. The protocol was launched in August 2021 under the name Lyra as an options automated market maker (AMM). After weathering the bear market, it was completely rebuilt in 2023 and is now built on its own OP Stack Layer 2 with a gas-free central limit order book.

This rebuild fundamentally changed the pricing mechanism. Market makers quote prices directly on the order book, leading to narrower spreads, more precise pricing, and support for larger trades. Traders enjoy zero gas fees and sub-second execution speeds.

Its portfolio margin system has also attracted institutional attention. The system assesses overall position risk through scenario analysis. For example, if a trader holds both a long call option and a short put option on the same underlying asset, the system does not charge margin for each leg separately.

The collateral required for a hedged position is lower than the simple sum of the individual parts, which is the common logic in traditional financial derivatives trading desks. Derive also offers perpetual contracts and lending services on the same Layer 2, supporting cross-product cross-margining.

@KyanExchange is moving in the same direction but in a different way. This platform combines an order book matching engine with on-chain portfolio margining, supporting multi-leg operations in a single atomic transaction. Traders can deploy an iron condor strategy with just a few clicks.

Kyan's liquidation mechanism also differs from most DeFi protocols. When a margin threshold is breached, the platform does not liquidate the entire account but executes a partial close-out, only closing the minimum number of positions necessary to bring the account back to the margin requirement. Kyan is currently in the Arbitrum test phase, with a mainnet launch imminent.

Who Needs Options?

Asset management companies building structured products urgently need the clearly defined risk-return profiles provided by options. Take J.P. Morgan's Equity Premium Income ETF as an example. This fund is built on a covered call strategy and is one of the largest actively managed funds globally. The total assets under management for yield products based on derivatives exceed one hundred billion dollars. As more institutional capital moves on-chain, the corresponding hedging needs will migrate as well.

Currently, more and more institutional investors already hold or plan to allocate to digital assets in the short term. The open interest for IBIT options has surpassed that of the gold ETF GLD. In 2025, the CME processed a nominal trading volume of $3 trillion in cryptocurrency derivatives.

The Timing is Ripening

Most early on-chain options protocols failed to survive, primarily due to regulatory uncertainty. For instance, Opyn was fined by the CFTC for operating an unlicensed derivatives exchange. At that time, teams developing products could not predict whether their product would be deemed illegal the next quarter.

This situation is now improving. In September 2025, the U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) jointly issued a statement allowing regulated exchanges to conduct spot crypto asset trading. The CLARITY Act has passed the House of Representatives, proposing to place spot markets for digital commodities under CFTC oversight. The Senate version is still under negotiation and is currently stalled. CME Group will launch 24/7 cryptocurrency options trading on May 29th. While this does not guarantee that on-chain protocols will necessarily succeed, the overall environment has undergone a fundamental shift.