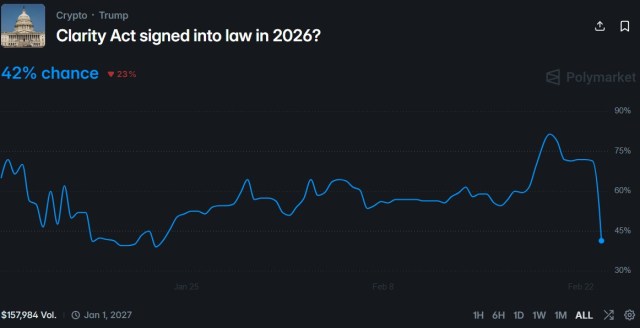

The likelihood that the long‐awaited crypto market structure legislation, known as the CLARITY Act, will become law this year has fallen sharply over the past 24 hours, according to data from prediction platform Polymarket.

Traders now assign the bill a 42% chance of passing in 2026, reflecting growing skepticism that ongoing negotiations between the crypto industry and the banking sector will produce a breakthrough in time.

Crypto And Banks Remain Divided

The drop in confidence comes despite months of high-level discussions at the White House. Lawmakers and industry representatives have been attempting to build consensus around a broader market structure framework.

However, three key White House meetings between crypto firms and banking representatives have yet to yield a final agreement. Even so, public messaging from officials has remained upbeat.

As Bitcoinist reported last week, Patrick Witt, Executive Director of the President’s Council of Advisors for Digital Assets, described the latest round of talks as “a big step forward.” “We’re close,” Witt wrote, adding that if both sides continue negotiating in good faith, he expects the administration’s March 1 deadline to be met.

At the center of the discussions is draft legislative language designed to address concerns raised by banks in a document titled “Yield and Interest Prohibition Principles.”

While the proposed text acknowledges the banking sector’s objections, it also makes clear that any restrictions on crypto rewards programs would be narrowly tailored.

One significant outcome of the negotiations is that paying yield on idle stablecoin balances — a major objective for many crypto firms — is effectively off the table.

Instead, the debate has shifted toward whether companies should be permitted to offer rewards tied to specific user activities rather than simple account balances.

How New Rules Could Change Bitcoin Derivatives Markets

Beyond the political back‐and‐forth, market expert MartyParty recently highlighted potential structural shifts that could follow the bill’s passage, arguing that the changes may be more significant than many investors realize.

In the Bitcoin (BTC) futures market, clearer jurisdictional boundaries would likely cement the Commodity Futures Trading Commission’s (CFTC) authority over digital asset commodities.

The expert believes that could accelerate the growth of regulated US trading venues, similar to CME, and potentially open the door to CFTC‐registered perpetual futures platforms.

According to MartyParty’s analysis, clear commodity classification may also encourage greater institutional participation, particularly from funds that are restricted from investing in assets deemed securities.

Perpetual futures contracts — a crypto‐native product widely used outside the United States — could also evolve. With CFTC registration, US‐based perpetual products might emerge with stronger consumer protections, greater transparency around funding rates, and tighter safeguards against manipulation.

Greater regulatory clarity could also reduce discrepancies between spot and futures markets, narrowing price gaps and stabilizing funding dynamics. At the same time, stricter leverage caps or margin requirements imposed under CFTC rules could limit the extreme levels of retail speculation currently seen on offshore platforms.

Bitcoin options markets would likely experience parallel shifts. The expert asserts that a clearer regulatory framework could encourage the development of additional US‐regulated options venues offering both physically settled and cash‐settled contracts tied to Bitcoin futures.

Reduced enforcement uncertainty may also lower implied volatility premiums, potentially making options more affordable for hedging and speculative strategies.

Institutional investors, in particular, could more confidently deploy advanced strategies — including collars and straddles — if Bitcoin’s commodity status is firmly established.

Featured image from OpenArt, chart from TradingView.com