Original|Odaily Planet Daily(@OdailyChina)

Author|Wenser(@wenser 2010 )

Recently, the once-popular "internet-famous shoe" brand Allbirds announced it would sell its footwear business and raise $50 million to transform into an AI computing infrastructure company called NewBird AI. Upon the news, its stock price surged, once reaching a high of $24.31, and has now settled at $16.99, still maintaining a staggering single-day increase of 582.33%.

Upon closer thought, $50 million is a drop in the bucket in the AI computing power赛道 (track/field), which often sees orders in the tens of billions of dollars. However, this move reminds me of the soaring stock prices of numerous DAT (Digital Asset Treasury) companies in Q3 of last year.

While the era where a simple announcement of转型 (transformation) into a DAT could cause a listed company's stock price to multiply several times has ended, we are now ushering in a new era of "listed companies transforming into AI computing power sellers". The reason is none other than "supply and demand".

Behind the网红鞋 (internet-famous shoe) changing tracks: The AI computing power gap has become a major issue

Recent hot topics such as the Claude model's perceived reduction in intelligence and the tightening of KYC policies have sparked widespread discussion. The reality reflected behind these events, however, is the structural gap in AI computing power.

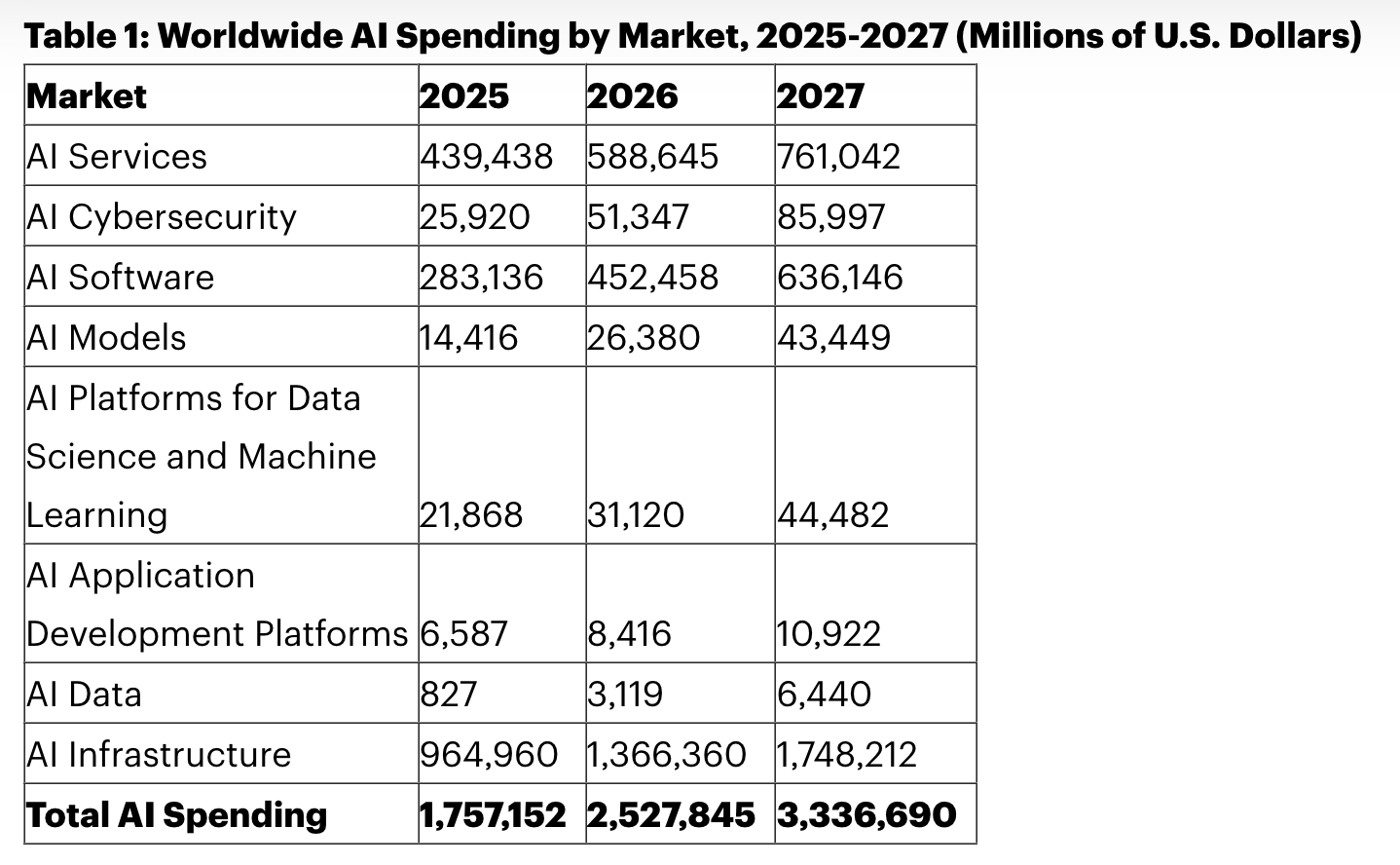

A report from the US market research firm Gartner points out that global AI spending will reach $2.52 trillion in 2026, a year-on-year increase of 44%;其中 (among which) AI infrastructure alone (including servers, accelerators, storage, and data center platforms) is expected to consume approximately $1.37 trillion, accounting for over half of the total expenditure.

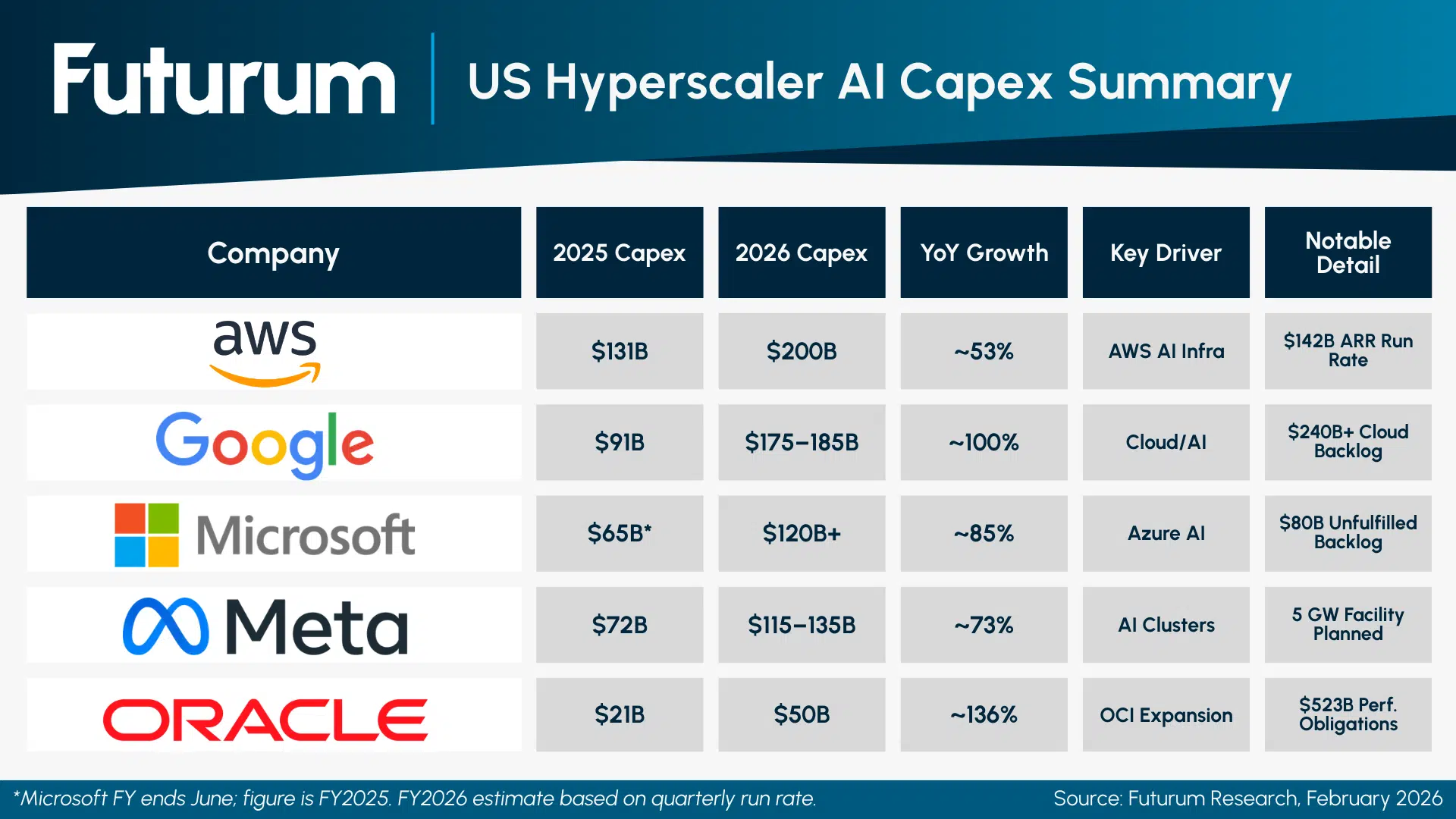

Regarding AI giants, the planned infrastructure capital expenditure for five companies—Microsoft, Alphabet (Google's parent company), Amazon, Meta, and Oracle—in 2026 totals approximately $660 billion to $690 billion, a figure roughly double that of 2025; the vast majority of these funds will be used for AI computing power, data centers, and networks. All cloud provider giants have stated that their markets are in a state of supply shortage.

Considering the approximately 36-52 week delivery cycle for GPU data centers, the situation of limited computing power and data supply will likely persist at least until Q3 2026.

It is worth mentioning that the current structural computing power gap stems not only from the demand of AI large model companies training various models but also from the rapidly expanding demand for daily inference model deployment from billions of global users. The computing resource gap from both B2B and B2C businesses has jointly led to the current supply-demand imbalance in the computing power market. No wonder Jensen Huang, founder of Nvidia, confidently stated at this year's CES: "(Nvidia's) AI chip and infrastructure market size could reach $1 trillion by 2027."

Apart from the computing power gap, consistent with the pace of various mining companies transforming into AI computing power and data centers, AI is competing with the cryptocurrency industry for critical resources like electricity. According to the recently released "2026 AI Index Report" by Stanford University, the overall electricity demand of current AI systems is already close to half the scale of Bitcoin mining and approaches the total electricity consumption of countries like Switzerland or Austria.

Undoubtedly, with AI becoming the sole narrative driving US stock market and even global tech companies, "having business related to AI" has become a necessity for many listed companies.

When the AI computing power business becomes the next DAT model: A test of the robustness of the AI narrative

What Allbirds has initiated might be another wave of热潮 (hot trend) similar to the emergence of DAT companies last year.

The reason for this judgment lies in the fact that the DAT treasury model in the cryptocurrency industry and the AI transformation of listed companies already have overlapping areas, and there have been mature cases previously.

From July to September last year, with the emergence of以太坊 (Ethereum) DAT companies like Bitmine and Sharplink, a large number of BTC DAT, ETH DAT, SOL DAT, BNB DAT, and various altcoin DAT listed companies became the "star stocks" of that time—many stock标的 (targets)上演了 (staged) miracles in the capital market, doubling or even increasing tenfold within just a few days.

On the other hand, transformation cases in the AI赛道 (track) are equally impressive.

Last year, Axe Compute(Odaily Planet Daily Note: formerly Predictive Oncology Inc.), which held Aethir (ATH) as its DAT reserve asset,上演了一场 (staged a) major drama of a listed company's transformation into AI computing power. Previously, the company's main business was medical equipment, and it had also explored services like providing a tumor drug response prediction platform and 3D cell culture models to support cancer drug development. In September last year, the company率先 (took the lead in) initiating a strategic transformation involving ATH token DAT, causing its stock price to surge nearly 200%; subsequently, after completing over $340 million in financing, it officially announced its transformation into a GPU computing infrastructure company, changing its stock ticker to AGPU.

CoreWeave (CRWV), which has now successively reached order cooperation with chip giants like Nvidia and AI giants like Anthropic, is also one of the players on the "AI fast lane". As an established mining enterprise, CoreWeave's transformation over the past 3 years of rapid AI development has been quite thorough: initially, it signed a $22.4 billion infrastructure contract with OpenAI; last year, it again signed an $11.7 billion AI agreement with Vast Data, which is invested in by Nvidia; recently, it reached a data center leasing agreement with Anthropic. According to financial report data, CoreWeave's revenue in 2025 was $5.13 billion, a year-on-year increase of 168%; its planned capital expenditure for 2026 exceeds $30 billion. At the time of writing, its market capitalization is approximately $62.4 billion. For more information, recommended reading "Analyzing CoreWeave: From Crypto Miner to AI Cloud Service Provider". As for the AI transformation of other mining companies, they are too numerous to count. See "The Great Migration of Mining Companies: Some Already Hold $12.8 Billion in AI Orders".

Of course, compared to the tens-of-billions-of-dollars orders of mining companies, Allbirds' current fundraising amount is rather insignificant. Furthermore, from a practical purchasing power perspective, compared to high-performance GPUs costing $25,000 to $40,000 each, $50 million can only勉强 (barely) purchase less than 2000 GPUs. However, some analysts believe its positioning might be as an acquisition target for a large "alternative cloud" company seeking a backdoor listing.

In other words, Allbirds' internet-famous shoe label has been torn off, while the "AI concept stock" label has instead become a香饽饽 (highly sought-after commodity). Its real value does not lie in how many GPUs $50 million can buy, but in retaining the shell of a Nasdaq-listed company—this holds certain吸引力 (attraction) for AI infrastructure companies wanting to quickly enter the public market.

Finally, although from a capital operation perspective, the AI computing power business model is quite similar to last year's DAT treasury model, they still differ in the following aspects:

First, is the real business revenue of the AI industry compared to the cryptocurrency industry. According to Anthropic's previous statements, its annualized revenue has exceeded $30 billion, a figure that was only at $9 billion in 2025; additionally, as of February, OpenAI's annualized revenue had surpassed $25 billion. Although valuations reaching thousands of billions seem high, the real business revenue provides more stable data support compared to the highly volatile market capitalization of cryptocurrencies. Various large model companies are the best buyers in the AI computing power business because the computing power shortage is an objective reality.

Second, is the high operational门槛 (threshold) of the AI computing power industry. Unlike the "hoarding coins" strategy of DAT treasury companies, the AI computing power business is not simply about purchasing GPUs. It also requires the construction of an entire operational chain including data centers, electricity, cooling, networks,运维团队 (operation and maintenance teams), customer acquisition. Therefore, its entry barrier, duration, and team requirements are higher, making it relatively more difficult to "fake". Ultimately, the underlying asset of DAT is a financial asset; whereas the underlying asset of an AI computing power company is an operational physical asset.

Third, is the sustained cash flow of the AI computing power industry. For DAT treasury companies, whether it's BTC, ETH, or altcoins like SOL and BNB, their main income高度依赖 (heavily relies on) the rise and fall of coin prices (staking income is merely nominal), lacking regular business income; the AI computing power business, however, can generate sustained cash flow through long-term leasing contracts, which is real cash inflow.

Of course, from the perspectives of financing structure, backdoor listings, and speculative sentiment, the two remain highly similar; and in terms of attracting scrutiny and pressure from regulatory agencies, listed companies后续 (subsequently) wanting to transform into AI computing power companies will inevitably face various restrictions and持续关注 (ongoing attention).

As industry insiders expressed views after Allbirds' stock price surge:

- Matt Domo, CEO of FifthVantage, believes that Allbirds' AI transformation this time seems more like a means to boost its sluggish stock price. Investors should be wary of "AI washing" phenomena, where companies attempt to exaggerate or even fabricate their AI capabilities for marketing. Additionally, companies trying to catch热门趋势 (hot trends) through aggressive transformations are not without precedent; many companies tried to ride the blockchain bandwagon in late 2017 to early 2018.

- Jason Schloetzer, Associate Professor at Georgetown University's McDonough School of Business, pointed out that this initial $50 million financing is "minuscule compared to the actual investment required to become a service provider in this field." However, from a more optimistic perspective, the influx of大量新玩家 (many new players) into the AI field may also reflect the "sustained enthusiasm" for growth in the market.

- Jay Goldberg, an analyst at Seaport Research,则认为 (believes that) it is hard to imagine a company like Allbirds, which is "半路出家 (switching careers midstream)", being able to provide competitive products or services in this field.

As the AI era train roars forward, there will always be those trying their utmost to cling to the door for a desperate gamble. As for whether they can stay on the train or be swept under the wheels by the fierce wind, we will have to wait for time to reveal the answer.