Authored by: Metrics Ventures

Over the past year, gold's performance has been particularly striking. More importantly, the demand structure has undergone significant changes: the willingness of central banks and sovereign entities to allocate has noticeably increased. This can no longer be simply explained as inflation hedging or short-term safe-haven trading. A more reasonable understanding is that gold is responding to a deeper change—a repricing of sovereign monetary credit and the effectiveness of global governance.

This change was repeatedly discussed at this year's Davos Forum. Whether in formal agendas or private discussions, phrases like "imbalance in the world governance structure," "the old order is breaking," and "we are entering a phase from which there is no return" almost became the common context. On Tuesday, Canadian Prime Minister Mark Carney's speech at Davos clearly articulated this sense of unease pervading the venue. He bluntly stated that the so-called "rules-based international order" is disintegrating, and humanity is moving from a once useful, albeit fictional, narrative towards a harsher reality: great power competition is no longer constrained, economic integration is being weaponized, and rules are selectively applied in the face of power.

Carney did not simply blame a single country but pointed to a more widespread change in circumstances. When tariffs, financial infrastructure, supply chains, and even security commitments can be used as bargaining chips, the multilateral institutions—whether the WTO, the UN, or other rule-based frameworks—on which medium-sized powers and open economies rely for survival are losing their binding force. In such an environment, continuing to pretend that the rules are still functioning normally becomes a form of self-deception. He used Havel's metaphor of "living within a lie" to remind countries: the real risk is not that the order is changing, but that people are still acting according to the language and assumptions of the old order.

More notably, what Carney repeatedly emphasized was not ideological confrontation but a shift in governance choices. When rules no longer automatically provide security, nations turn to another rationality: enhancing strategic autonomy, diversifying dependencies, and building "pressure-resistant" capabilities. In his view, this is a typical risk management logic, not a betrayal of values. But it is precisely here that the foundation sustaining the old order begins to loosen—because once countries no longer believe the system can consistently provide public goods, they will instead buy "insurance" for themselves.

If we abstract the Davos discussions from specific countries, we find a deeper common direction: countries have not suddenly become more conservative but have begun to tacitly accept that a key assumption is failing—that the existing global governance system can long-term coordinate fiscal, monetary, and international responsibilities. When this premise is no longer widely believed, national behavior shifts from "division of labor within rules" to "preparing for uncertainty." And this shift will ultimately be reflected in the most fundamental areas: debt, fiscal policy, and currency.

It is here that the cracks in world governance begin to penetrate financial pricing. National debt is no longer just a macro-control tool but is re-examined as a discount of governance capacity and political constraints; sovereign currency is no longer just a medium of exchange but is required to simultaneously bear the functions of intertemporal commitment, international responsibility, and crisis buffer. Once the market begins to doubt whether these roles can still be fulfilled simultaneously, the impact on monetary credit is no longer an extreme scenario but a gradual yet irreversible process.

And all this does not stem from the fiscal mistakes of a particular country but is embedded within the current international monetary system. The dollar-centric system dictates that the world must have a long-term deficit center that absorbs external savings, and it also dictates that surpluses and deficits are not accidental but a role division solidified by the system. The US dollar is both a sovereign currency of the United States and the basis for global reserves, pricing, and safe assets. This means that global demand for "risk-free dollar assets" further intensifies when uncertainty rises. To provide these assets to the world, the US can only fulfill this role by continuously incurring external liabilities.

In an environment of financialization and free capital flows, this division of labor is constantly amplified. Surpluses are no longer primarily digested through adjustments in commodity prices or exchange rates but are transformed into long-term allocations to US Treasury bonds and dollar-denominated financial assets; deficits are no longer immediately constrained but are postponed and absorbed through the financial system and central bank intervention. As long as the world still believes that dollar assets possess irreplaceable safety in a crisis, this imbalance can persist long-term, even being seen as a source of systemic stability.

But when governance trust declines, rule constraints weaken, and financial tools are frequently weaponized, this structural imbalance begins to be repriced. Surpluses and deficits are no longer just macroeconomic phenomena but become risk exposures themselves. It is also against this backdrop that Japan and China, both surplus countries, have gradually moved towards different paths.

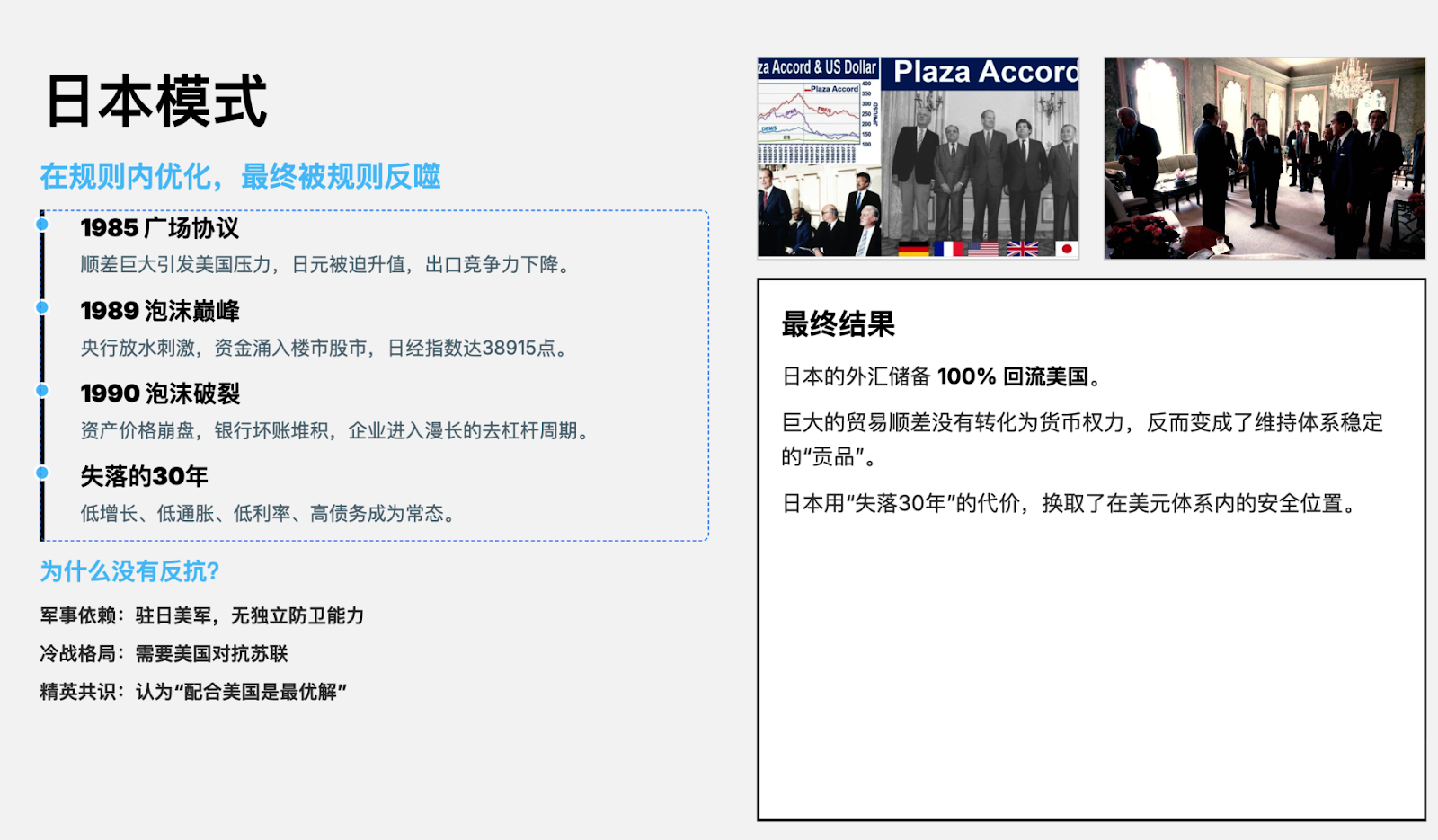

Japan has played the most typical and "cooperative" surplus country role in this system. Under external pressure and rule constraints, Japan chose to absorb adjustment costs through currency appreciation, financial liberalization, and long-term accommodative policies, thereby maintaining the stability of the overall order. This strategy reduced friction in the short term but transformed structural adjustments into domestic low growth, high debt, and deep central bank intervention. The surplus did not disappear but was internalized as the cost of long-term stagnation; Japan's monetary internationalization capacity was also significantly limited in this process.

China entered this system later, and its stage of development and internal constraints were significantly different from Japan's. Faced with surplus expansion and external pressure, China did not fully choose to clear rapidly through price and financial channels but, within the framework of exchange rate management, capital account controls, and industrial upgrading, sought to preserve policy autonomy as much as possible. This choice has long placed China in controversy, accused of "distorting rules" or "free-riding," but from a governance perspective, it appears more like a strategic arrangement to buy time and space for internal transformation within the existing system, rather than simple institutional arbitrage.

More importantly, this path did not stop at "maintaining a surplus" but quietly changed the structure of renminbi demand. As China's position in global trade, manufacturing, and key supply chains has risen, the renminbi is no longer just a settlement tool but is increasingly seen by more economies as a practical option for reducing external dependence and diversifying currency risk. Against the backdrop of intensified geopolitics and the instrumentalization of financial sanctions, sole reliance on the dollar system itself begins to be seen as a risk exposure, giving demand for renminbi settlement, renminbi financing, and renminbi asset allocation a clear strategic motivation.

Once renminbi demand shifts from passive use to active allocation, its impact is no longer limited to the trade level but transmits to the financial level. More frequent and stable usage scenarios mean the market needs a deeper and more liquid renminbi asset pool to accommodate this demand. Increased liquidity, in turn, affects how assets are priced, gradually moving renminbi assets from "domestic policy pricing" towards "a logic closer to international marginal pricing." This process does not rely on complete capital liberalization but is更多的是 pulled by real demand, representing a gradual yet hard-to-reverse change.

It is also in this contrast that "the East rises while the West declines" has once again become a proposition that can be seriously discussed in recent years. It is no longer an emotional judgment about the rise and fall of a particular country but a reflection of the changing costs of systemic roles. As the self-healing capacity of the dollar system declines, the space for the deficit center to continue absorbing imbalances through debt and financial expansion is shrinking; meanwhile, the importance of surplus economies in industrial chains, security, and regional arrangements is rising. In this process, China, by not fully replicating Japan's adjustment path, has retained industrial, policy, and monetary space, giving it higher strategic elasticity in systemic restructuring.

But this change does not mean a new single hegemonic currency is forming. A more realistic picture is the monetary system moving towards a multi-center and coexisting structure. The centrality of the US dollar may be weakened but will not disappear quickly; the status of the renminbi in trade settlement, regional finance, and liquidity provision will gradually increase, yet not necessarily predicated on full free floatation, but more reliant on trade networks, industrial chain depth, and policy credibility. Monetary internationalization here is no longer an institutional label but an outcome that is used into existence.

In such systemic evolution, the logic of reserve assets also changes accordingly. Gold's return to a core position is not because it can provide yield, but because it does not rely on any country's tax base, political stability, or international commitments; it is a direct response to governance uncertainty. It provides countries with a de-sovereign, de-credit reserve option, particularly suited to function in an environment lacking consensus and with weakened rule constraints.

Bitcoin represents another tier of de-sovereign asset. Although its performance has lagged behind gold and some traditional assets over the past year and a half, its core logic has not been disproven. As a digital, scarce asset not attached to any single governance system, it更像 is more like a long-term option on future monetary forms. As monetary system restructuring becomes more explicit and liquidity is reallocated, its pricing logic is more likely to catch up in later stages rather than lead in the early phases.

If these clues are finally gathered together, one finds that what this as-yet-unnamed order migration is truly changing is not short-term power comparisons, but the preconditions for the validity of assets. When rules no longer automatically provide safety, when monetary credit itself becomes a risk that needs to be hedged, the core question of asset allocation is no longer betting on who wins, but how to remain valid in a world where uncertainty has become the norm.

Against this backdrop, gold is a defensive response, while more directional choices are embodied in the renminbi and Bitcoin. The renminbi represents the real liquidity embedded in the new order, a bet on monetary restructuring pulled by trade, industry, and real demand; Bitcoin represents the ultimate hedge against governance uncertainty, a long-term option detached from any single sovereign system. Choosing them is not a statement of stance, but a largely self-consistent outcome of asset allocation under the premise that the cracks in world governance have already become explicit.

History does not announce itself with dramatic events. It is often only at a moment when looking back that people realize the order has already, imperceptibly, migrated.