Following the plunge in gold and silver, the U.S. stock market is also under pressure. On February 2, Nasdaq index futures fell nearly 1% in pre-market trading, the S&P 500 index has retreated 0.43% from its high, and the fear index VIX surged to 17.44, indicating a clear shift toward caution in market sentiment.

From a technical perspective, the Nasdaq index has been oscillating at high levels for three months, forming a rising wedge pattern. Now, this key upward trend line has been effectively broken for the second time, dealing a significant blow to market confidence.

If tonight's closing price falls below the previous low, forming a "Lower Low," a larger-scale downtrend may begin.

Adding to market unease is the ongoing fallout from the "Epstein Files" over the weekend. These archives, comprising over 3 million pages, have implicated Kevin Warsh, the Trump administration's nominee for the next Federal Reserve Chair.

His name appeared on the guest email list for the "St. Barts Christmas Party" in 2010. This distant political gossip has now become a real risk looming over the market.

Escalating Political Risks

Market panic stems primarily from a reassessment of policy uncertainties in the potential "Trump 2.0" era. Warsh is a staunch hawk, and his nomination almost signals the end of the low-interest-rate era.

Warsh has long been an outspoken critic of the Fed, advocating for an "institutional shift." He publicly criticized the Fed for cutting rates by a full percentage point in 2024 when inflation was above target and then hesitating, damaging its credibility.

Warsh's core argument is that the Fed's massive balance sheet distorts the healthy functioning of the economy and fuels asset bubbles. He advocates for reducing the balance sheet, even if it requires tightening policies. This combination of "hawkish rate cuts" has raised concerns about a potential sharp tightening of monetary policy.

The release of the Epstein files has exposed the market to significant, unpredictable political risks. Although there is currently no evidence of Warsh's involvement in illegal activities, his association with this century's scandal itself constitutes a major political liability, making the already contentious nomination even more difficult.

Additionally, the uncertainty surrounding the Trump administration's signature tariff policies is also worrying the market. If the new round of tariffs expands in scope, it could not only hurt consumer confidence and corporate profits but also further inflate the already massive fiscal deficit.

It is projected that the U.S. fiscal deficit will reach $601 billion in the first three months of 2026 alone. This fiscal outlook, combined with the political trust crisis exposed by the Epstein files, creates an extremely fragile market environment.

Global Market and Commodity "Bloodbath"

The commodity market was the first to trigger a "long squeeze" stampede. Traditional safe-haven assets like gold and silver experienced an epic collapse, with gold prices falling by 12% at one point and silver plummeting by 36%. After ETF orders reached 30B in a single day, silver recorded its largest one-day drop since 1980, with highly leveraged long positions being liquidated en masse in a short period.

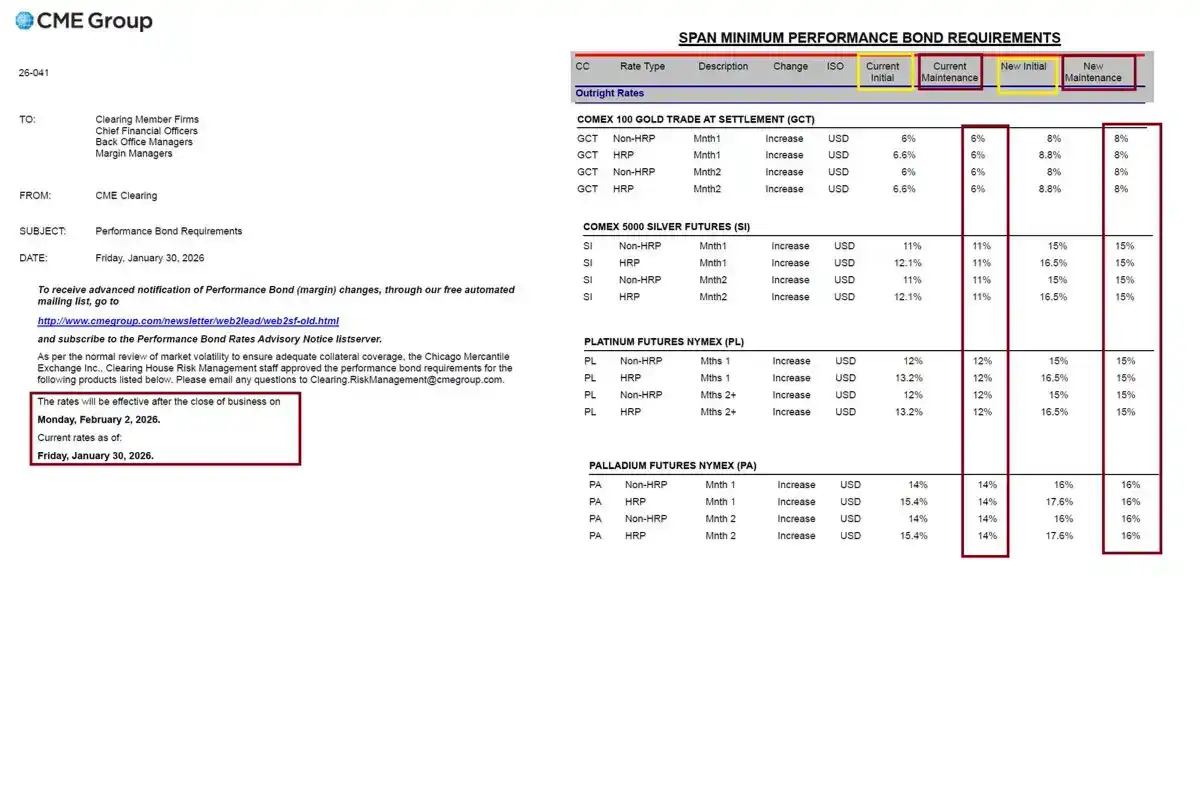

As prices fell, the Chicago Mercantile Exchange (CME) quickly raised margin requirements for gold and silver futures. For example, the margin ratio for non-high-risk silver futures accounts increased from 11% to 15%. This forced many underfunded long traders to be liquidated, with selling pressure further crushing prices and creating a vicious cycle. According to statistics, the liquidation amount for tokenized futures alone reached $140 million within 24 hours.

The storm also spread domestically, with several gold shops in Shenzhen's Shuibei district "exploding" due to participation in unqualified gold futures betting trades, involving up to 10 billion yuan and affecting thousands of investors.

Crude oil prices were not spared either, falling 5.51% to $61.62 per barrel. Weakness in Asian stock markets had already sounded the alarm, with the Nikkei index falling 1.11% and the Hang Seng Index plunging 3.15%. Bitcoin, a barometer of risk assets, also fell below the psychological threshold of $75,000. Behind this series of chain reactions may be a global deleveraging event unfolding.

When investors are forced to liquidate positions in one market (e.g., commodity futures) due to high leverage, they have to sell assets in other markets (e.g., Asian stocks, Bitcoin) to raise margin, triggering cross-market risk contagion. If this liquidity drought continues, the next target for selling could be U.S. stocks, which are currently at high valuations.

Economic Data and AI Bubble

Cracks in the economic landscape are also becoming clearer. The upcoming employment report has become the focus of market attention. If the data shows an unexpectedly cooling labor market, concerns about an economic recession will quickly intensify. The Fed is currently keeping rates unchanged, but facing persistently high inflation, its policy space is extremely limited. If inflation does not fall as expected, future rate hikes will be inevitable.

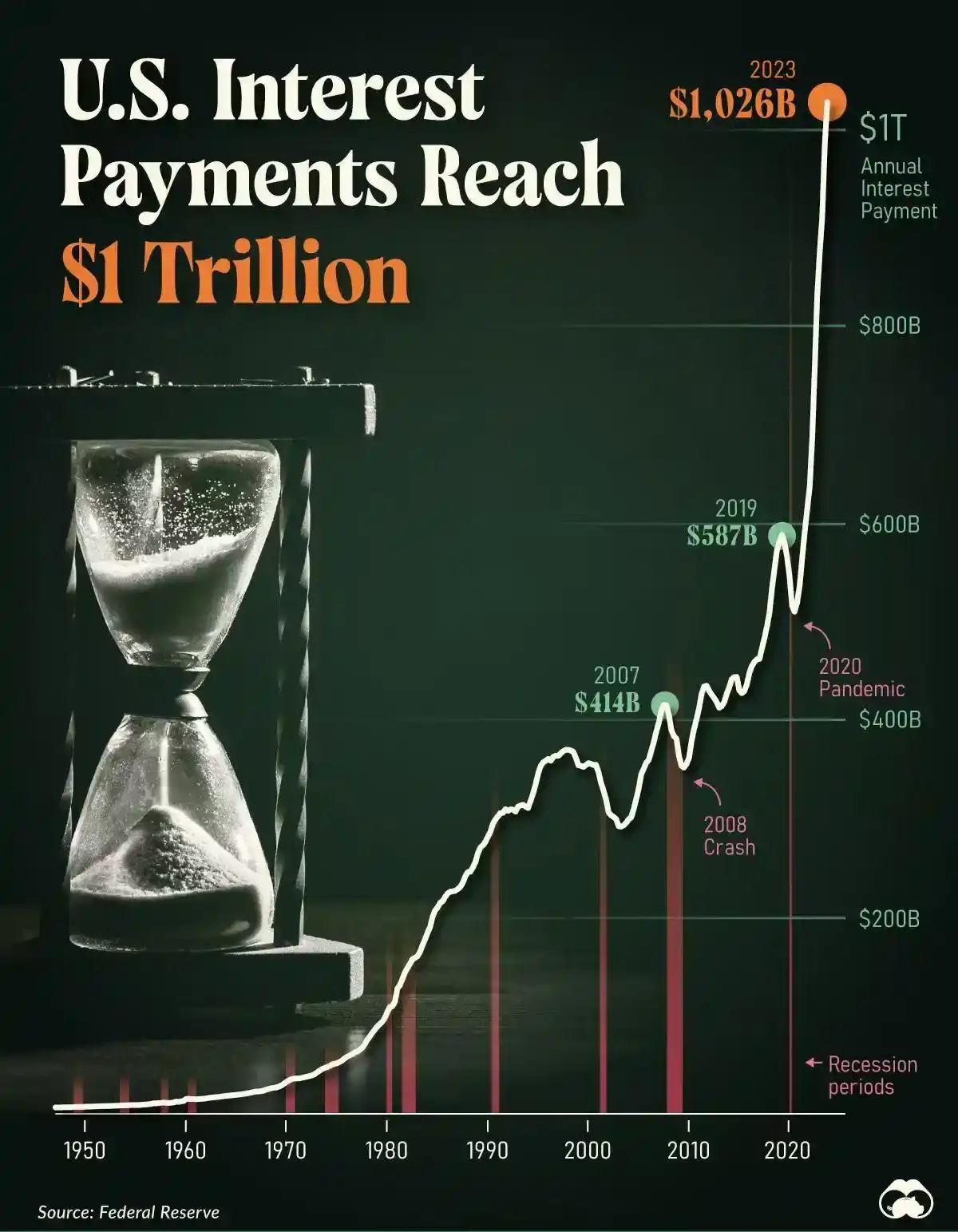

The 10-year U.S. Treasury yield has climbed to 4.218%, and the massive annual interest payments on U.S. government debt are adding to the fiscal woes. Historically, an inverted yield curve has been a reliable leading indicator of economic recessions, and the market is once again approaching this dangerous edge.

Meanwhile, the AI narrative that supported the market boom in 2025 is also showing cracks. The recent weakness in the Nasdaq index, particularly with software stocks becoming the most oversold sector in the S&P 500, indicates that market enthusiasm for AI is cooling.

Investors are beginning to realize that the commercialization and profit realization of AI are far more prolonged and challenging than imagined.

The upcoming corporate profit season, especially the earnings reports of tech giants like Amazon and Alphabet, will serve as a "litmus test" for AI. If the reports fall short of expectations, a large-scale sell-off may be inevitable.

The Ghost of 1979

The current geopolitical and macroeconomic environment bears a remarkable resemblance to 1979, which makes many seasoned investors uneasy.

1979 marked the end of the Cold War détente. In December of that year, the Soviet invasion of Afghanistan led to a sharp deterioration in U.S.-Soviet relations, pushing global geopolitical tensions to a peak.

Almost simultaneously, the Iranian Revolution triggered the second oil crisis, causing oil prices to soar and the global economy to fall into the mire of "stagflation" (economic stagnation coupled with high inflation). At the time, the Fed, under political pressure, failed to take decisive action promptly, leading to失控 inflation. It eventually took the appointment of new Chair Paul Volcker and his "shock therapy" of sharp rate hikes to curb it, but at the cost of a deep recession.

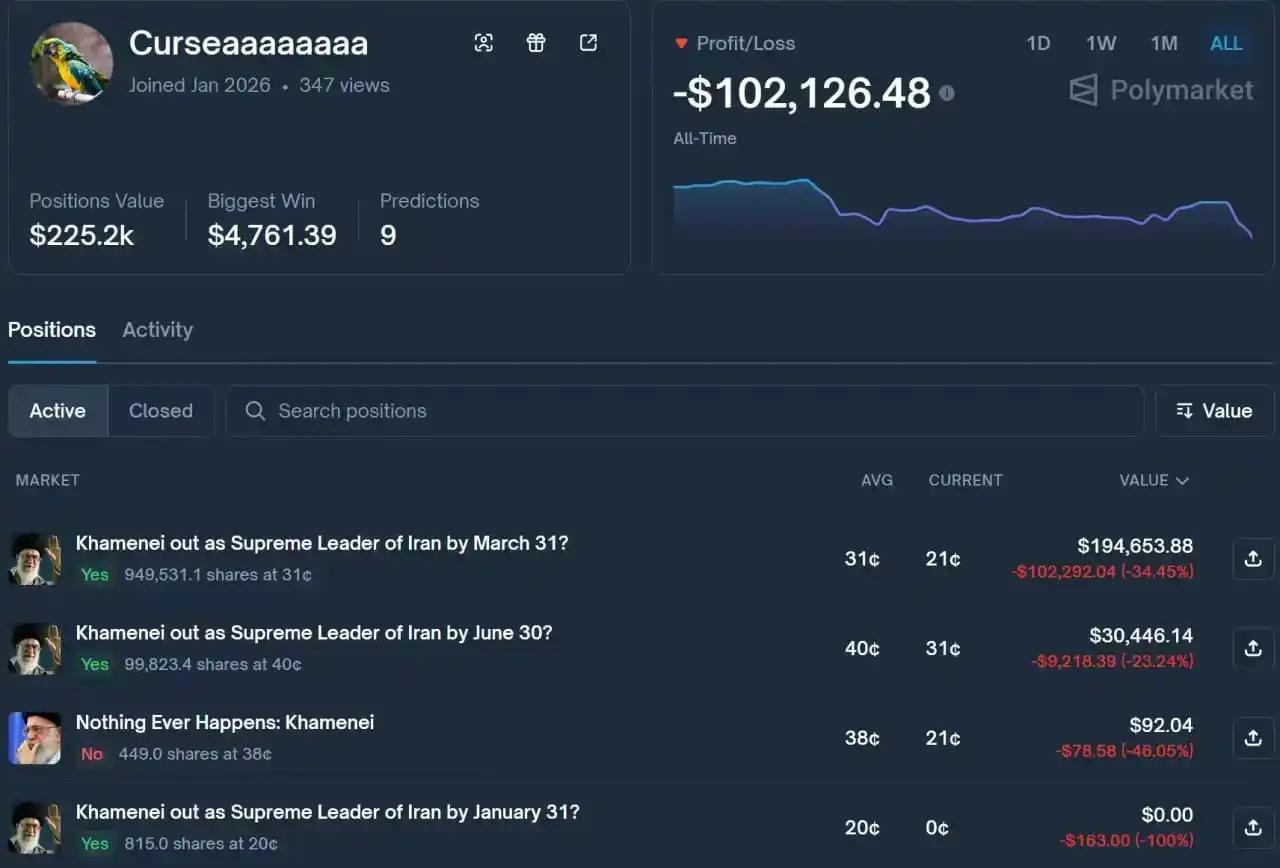

Today, we are once again facing a similar situation: heightened geopolitical tensions in the Middle East. According to data from prediction market Polymarket, as of February 2, the market believes there is a 31% probability of the U.S. striking Iran by the end of the month, with insider whales making huge bets on Khamenei's ouster.

Meanwhile, energy prices are highly volatile, and global inflationary pressures remain high. The potential interference of the Trump administration with Fed independence, coupled with the nomination of a hawk like Warsh, recalls the risks of policy errors under political pressure.

If history repeats itself, aggressive tightening policies adopted to control inflation could end this artificially prolonged bull market, triggering a dollar confidence crisis and a significant correction in U.S. stocks similar to the late 1970s and early 1980s.

For investors who have been riding high on the狂欢 of 2025, it may be time to reassess risks and prepare for potential market volatility.