Original Author: ChandlerZ, Foresight News

Recently, Hong Kong, China announced through a government gazette that the authorities are conducting consultations on the implementation of the Organisation for Economic Co-operation and Development (OECD)'s Crypto-Asset Reporting Framework (CARF) and related amendments to the Common Reporting Standard (CRS).

It was pointed out that since 2018, Hong Kong has been automatically exchanging financial account information with partner tax jurisdictions annually under the Common Reporting Standard developed by the OECD, enabling relevant tax authorities to use this information for tax assessments, as well as detecting and combating tax evasion. The future goal is to automatically exchange tax-related information on crypto asset transactions with relevant partner tax jurisdictions starting from 2028, and to implement the revised new CRS rules from 2029.

Additionally, starting from January 1, 2026, the first batch of over 40 countries, including the UK, will implement new crypto asset tax regulatory rules, requiring local crypto service providers to begin collecting user crypto wallet and transaction data in preparation for subsequent cross-border tax information exchange.

Taking the UK as an example, crypto exchanges operating in the UK must begin collecting detailed transaction records and complete information for all UK customers. HMRC will use the collected data to cross-check users' tax returns to ensure tax compliance, and violators will face sanctions. Industry insiders point out that the relevant data may be used for identity verification, anti-money laundering, and criminal investigations in the future, having a profound impact on the anonymity and compliance environment of the crypto industry.

"Is crypto trading taxation becoming a reality?" A wide-ranging discussion has begun in the market. If Hong Kong reports, will mainland China also report? Will crypto trading be subject to back taxes in the future?

What is the CARF Global Taxation Framework

The "Crypto-Asset Reporting Framework" is a set of international standards for crypto asset tax information transparency developed by the OECD under the authorization of the G20. Its core purpose is to bring crypto asset transactions, which were previously difficult for tax authorities to penetrate and highly prone to cross-border flow, into a network of information that can be collected in a standardized manner and automatically exchanged between tax authorities. The OECD adopted and published the rules and commentary of CARF in 2022, clarifying that its design goal is to collect taxpayer-related information in a unified manner and automatically exchange it annually with the jurisdictions where taxpayers are tax residents, thereby reducing the risk of cross-border crypto asset tax evasion and underreporting.

In the context of CARF, crypto assets are not equivalent to Bitcoin or Ethereum in the narrow sense; any digital value carrier that can be held and transferred in a decentralized manner without the involvement of traditional financial intermediaries is within the scope. Its coverage is deliberately made closer to the real market form, including stablecoins, derivatives issued in the form of crypto assets, and even bringing some NFTs into the observation scope that may trigger similar tax risks.

Corresponding to the coverage, CARF's reporting obligations focus on market intermediaries that provide key services for transactions and exchanges. The OECD's approach is to anchor compliance at the link that is most capable of mastering transaction value and counterparty information. Any entity or individual that commercially facilitates or executes exchange transactions of relevant crypto assets for customers (including exchanges between crypto assets and fiat currency, as well as swaps between crypto assets) may in principle be identified as a Reporting Crypto Asset Service Provider and bear the obligations of data collection, due diligence, and reporting.

What is the relationship between CARF and the previously discussed CRS?

Understanding CARF requires placing it within the larger global tax information exchange system for comparison. The previous wave of tax supplements for Hong Kong and US stocks occurred under the mechanism of the Common Reporting Standard (CRS).

Over the past decade, cross-border tax transparency has mainly relied on the CRS standard. Countries require banks, securities firms, funds, and other financial institutions to identify account holders who are non-resident taxpayers and report key information such as account balance, interest, dividends, and disposal gains to their domestic tax authorities annually, which are then automatically exchanged with the other country's tax authorities.

China began fully implementing CRS in September 2018, exchanging resident financial account information with over 100 countries and regions. After data declaration, tax authorities issued notices based on CRS and other data, requiring users to explain the situation and pay back taxes.

CRS operates relatively maturely in the traditional financial system, but a large amount of crypto asset transactions, exchanges, and transfers occur outside the bank account system, especially forming an independent value circulation network between centralized trading platforms, custodial wallets, and on-chain transfers, making it difficult for CRS alone to achieve the same level of penetration. CARF supplements the on-chain and crypto asset market structure that CRS originally had difficulty covering.

While launching CARF, the OECD conducted the first systematic revision of CRS. On the one hand, it brought new financial products such as electronic money products and central bank digital currencies (CBDCs) into the scope of CRS; on the other hand, it adjusted the caliber for paths that indirectly invest in crypto assets through derivatives or investment vehicles to avoid the market circumventing information declaration and exchange through product structures. Overall, CARF is responsible for the transaction and service provider dimensions of the native crypto asset market, while the revised CRS continues to be responsible for the relevant risk exposures that may be carried within the financial account system. Together, they form a more complete automatic exchange puzzle.

The OECD pointed out that after the technical transmission format and supporting guidance for CARF and the revised CRS are perfected, the first batch of cross-border automatic exchanges is expected to start in 2027; before that, multiple jurisdictions will first implement domestic data collection and reporting requirements to prepare the data foundation for subsequent cross-border exchanges.

At the EU level, DAC8 was approved by member states in October 2023 and published in the official gazette in the same month. Its system design is based on the OECD's CARF international standards, aiming to incorporate crypto asset user information into automatic exchanges between member states' tax authorities.

Will Mainland China also join?

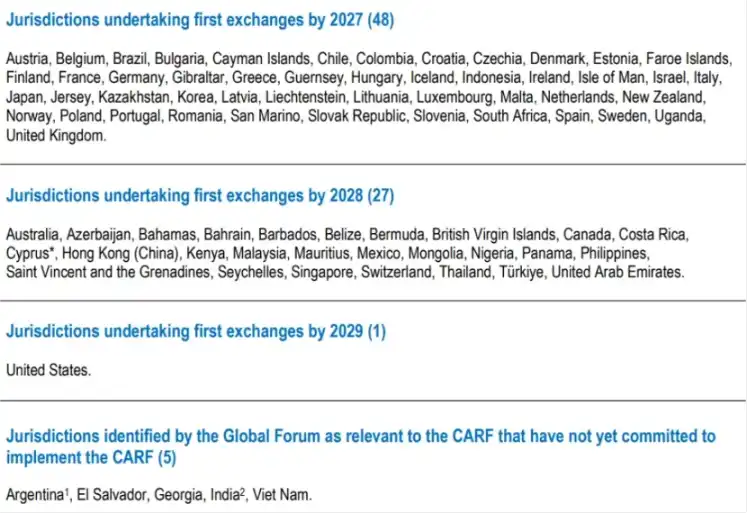

As of early December 2025, 76 countries/regions globally have committed to adopting CARF. The UK and the EU will be the first to implement this framework (data collection starting in 2026, first exchange in 2027); Singapore, the UAE, and Hong Kong, China follow closely, planning to collect data in 2027 and fully implement in 2028; Switzerland has postponed the implementation to 2027 and is still prudently assessing exchange partners; the US IRS's CARF joining proposal is still under internal review.

This means that China is not on the first batch of exchange lists, and CARF data will not be automatically exchanged with Chinese tax authorities through the CARF mechanism.

China has accumulated mature systems and collection and management experience under the CRS automatic exchange system, indicating that it has the infrastructure in terms of legal design, due diligence caliber, data exchange governance, and information security to undertake international standards.

The problem is that the compliance anchor of CARF mainly falls on regulated crypto asset service providers, while mainland China has long adopted a strong regulatory or even prohibitive governance approach towards virtual currency-related businesses. There is no locally licensed trading platform system that can be routinely included in CARF.

Hong Kong's advancement of CARF may increase the intensity of tax resident identification and information reporting for customers by crypto service providers in Hong Kong, but this does not automatically mean that the relevant information will naturally flow back to mainland tax authorities. Whether cross-border exchange occurs still depends on whether mainland China chooses to participate and establish exchange relationships with relevant jurisdictions, as well as arrangements between the two places regarding data usage restrictions, privacy protection, and technical对接.

But it is equally important to emphasize that not having joined does not mean it can be ignored. Even without the automatic exchange path of CARF, cross-border tax information may still flow through existing tax treaties and international collection and management cooperation frameworks, through case-by-case requests, joint law enforcement, or other cooperation methods. As major jurisdictions around the world begin to systematically collect crypto asset transaction and transfer data, the clues available to tax authorities will be more complete, and cross-border risk identification capabilities will also improve simultaneously.

For individuals and institutions, the most realistic change is that as long as the main operational path relies on centralized trading platforms, custody services, or fiat currency gateways, the traceability and追溯性 of transaction data will become increasingly stronger, and the compliance exposure will shift from a probability event to a常态.