Hyperliquid [HYPE] continued its short-term downtrend to fall below the $37 level on the 2nd of April. Since the 15th of March, $37 has acted as a reliable short-term support.

Each retest has seen a price bounce, but none of the bounces of the past two weeks were enough to drive prices to the local highs at $43.7. The final week of March saw a move above the psychological $40 mark, but the bears were quick to seize control of the trends thereafter.

At the same time, Bitcoin [BTC] and many prominent crypto altcoins were posting losses and reeling under selling pressure. The market sentiment remained extremely pessimistic.

Does this mean HYPE investors should sell and wait for the downtrend to continue?

HYPE investors should not miss THIS chance

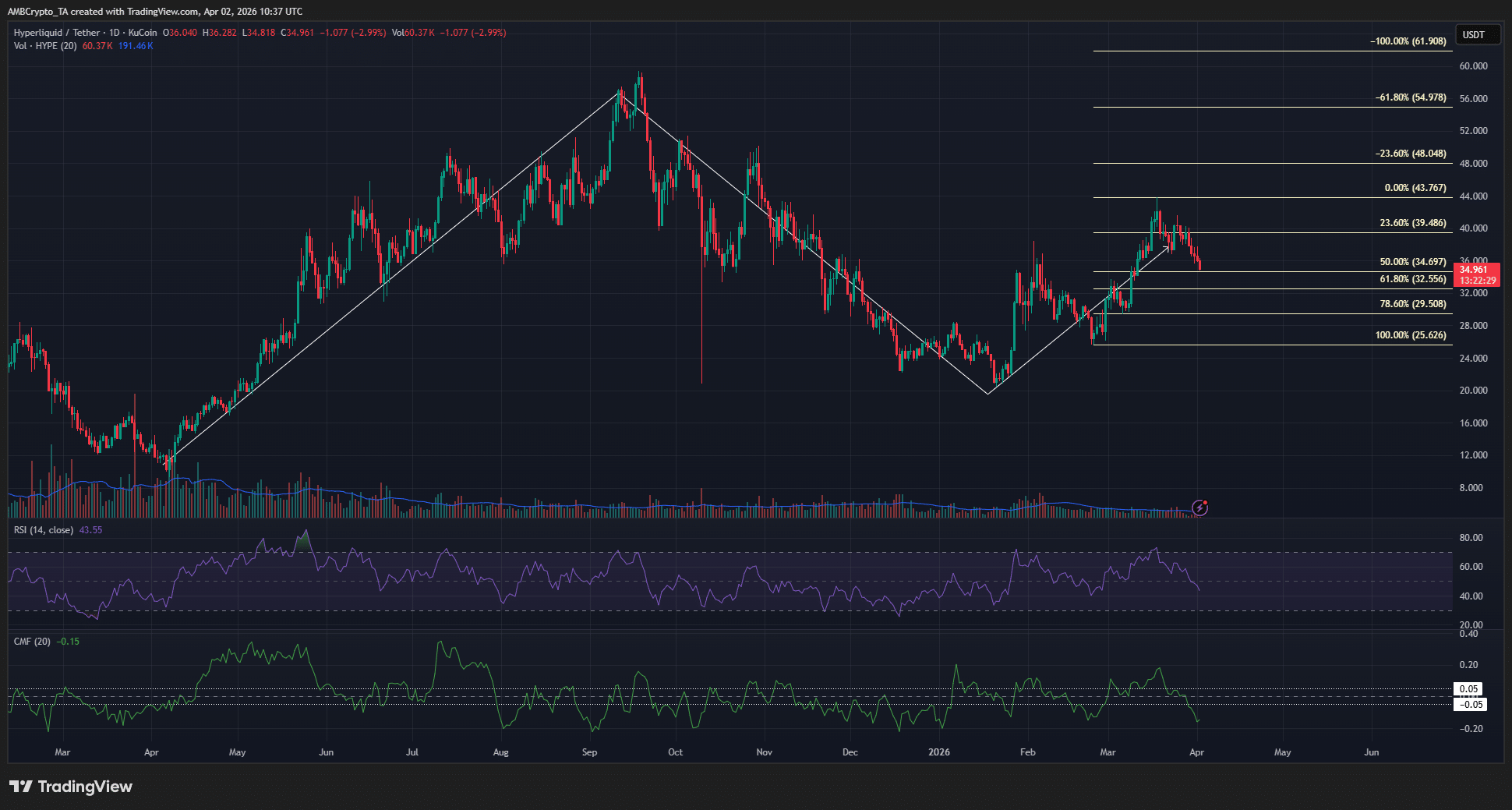

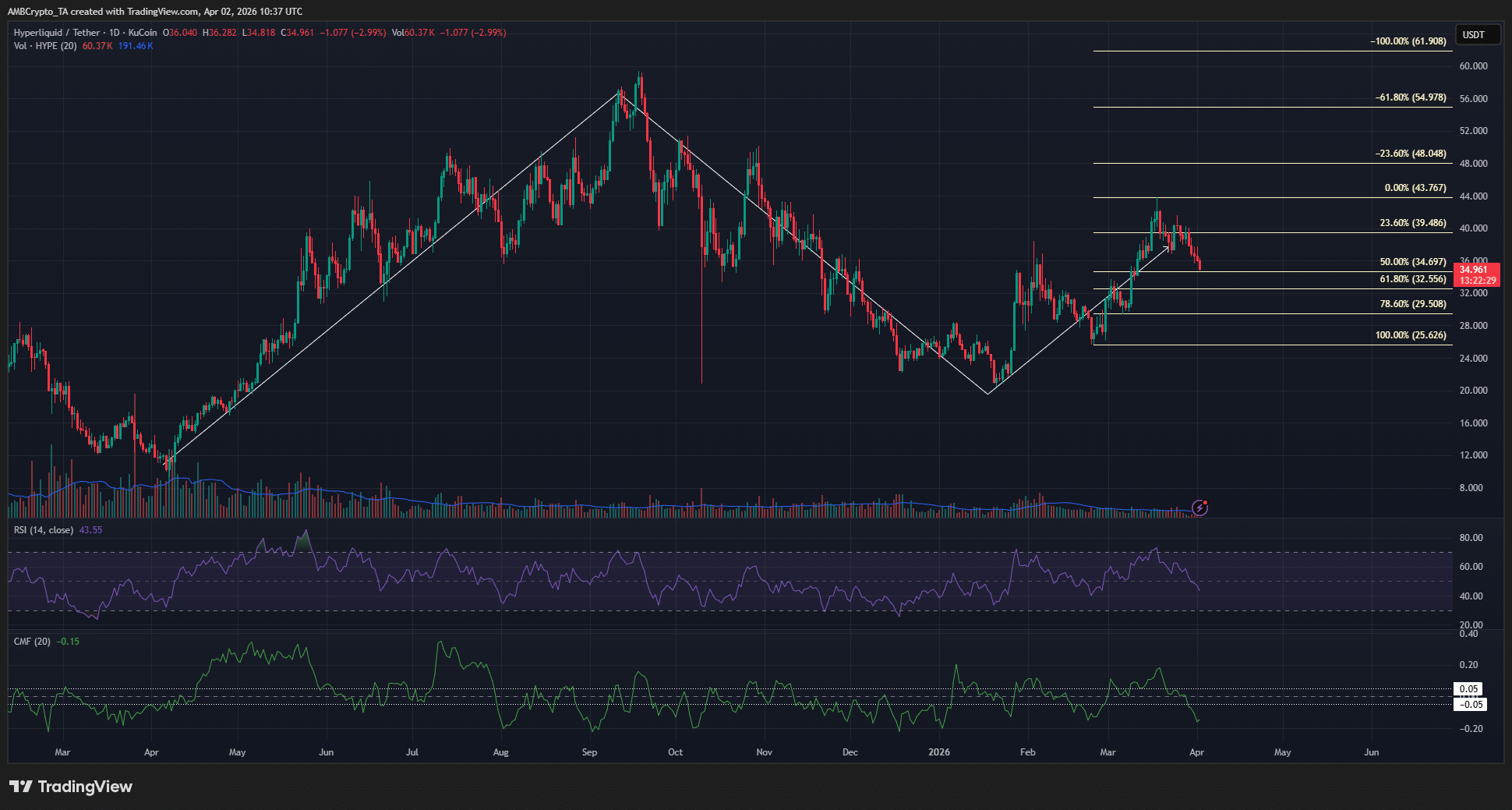

While the recent Hyperliquid token price losses seem grievous, they might just be part of a retracement. The long-term structure showed that HYPE saw a rally in 2025 that nearly reached $60, then pulled back to $20 by year-end.

The push higher to $43.7 since then has been part of the next bullish wave higher. The rally in March saw a pullback over the past two weeks, and this retracement could continue for a bit longer.

The Fibonacci retracement levels plotted for the most recent swing move higher from $25.6 showed that there was more space for HYPE to fall. The $32.44 and $29.5 were the levels in the golden pocket that long-term buyers will want to keep an eye on.

Yet, they shouldn’t rush to buy, either. At press time, the RSI showed that the momentum had turned bearish, with the RSI sliding below neutral 50. The CMF also reflected hefty capital outflows from the market, with a reading of -0.15.

Traders’ call to action: Wait

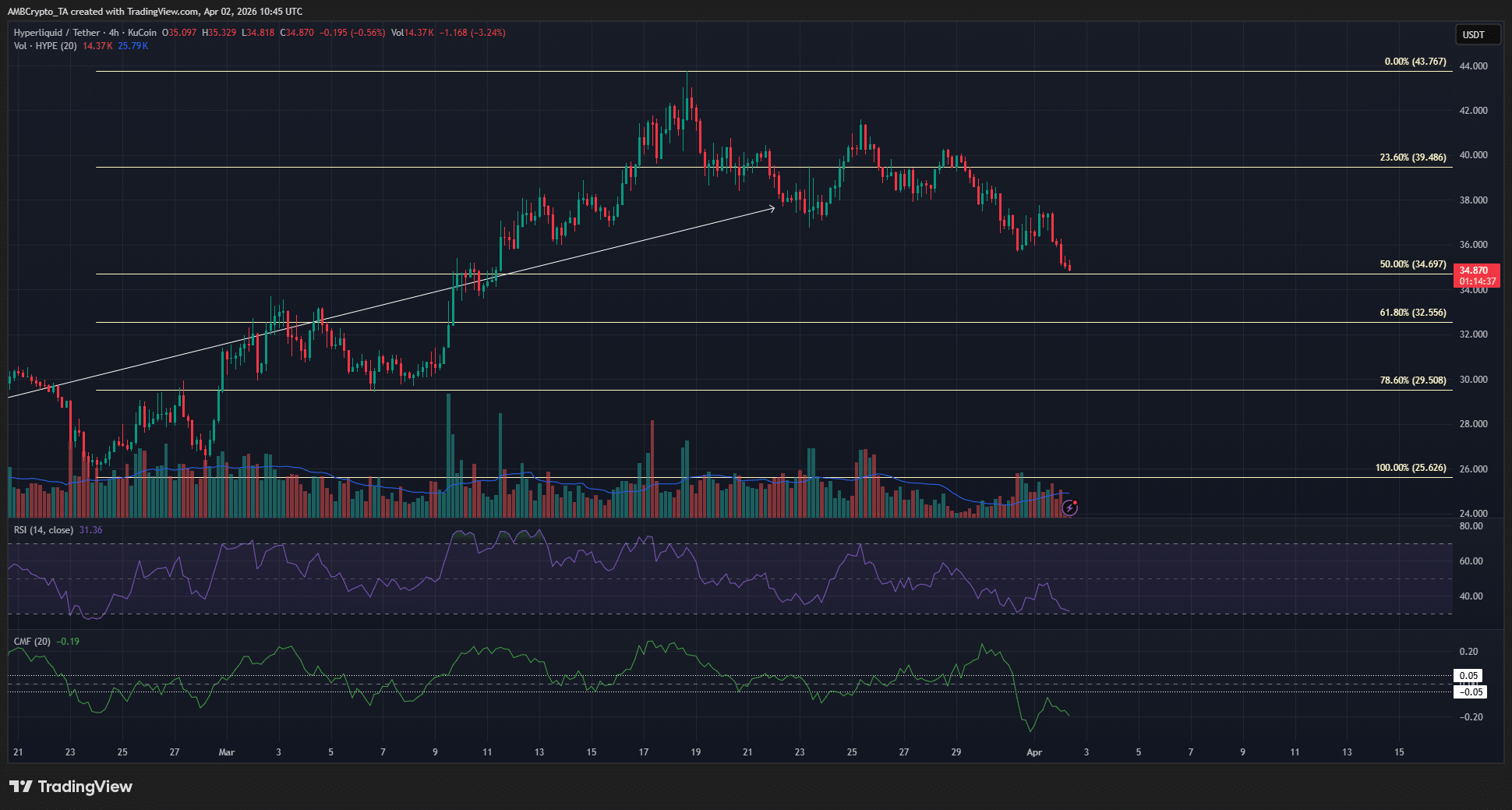

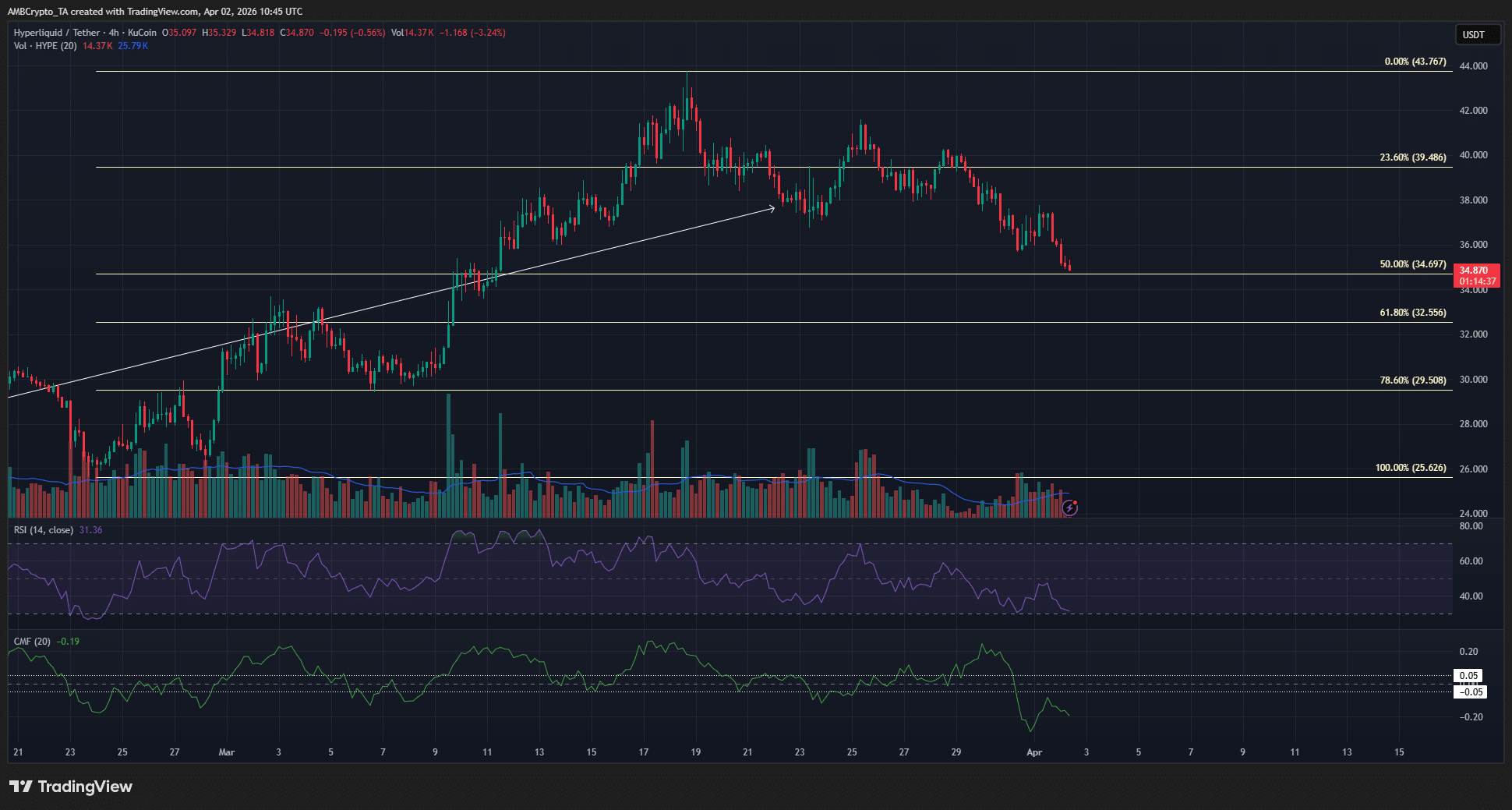

The 4-hour chart showed a bearish structure in place for HYPE. The lower high it set below $42 on the 25th of March was the swing high on this timeframe. Meanwhile, the $29.55-$32.5 zone remained the demand zone for buyers to defend.

A move back above $41.59 is needed to prove this retracement idea wrong and show that the token has what it takes to make new highs past $43.7. Until this happens, long-term investors can wait for the retracement to end before buying.

Final Summary

- The long-term Hyperliquid token price trend was bullish, but the current short-term trend was bearish.

- The current sell-off comes with the longer-term structure’s pullback. Therefore, investors with a time horizon will be watching the $29-$32 demand zone.