Author: Claude, Shenchao TechFlow

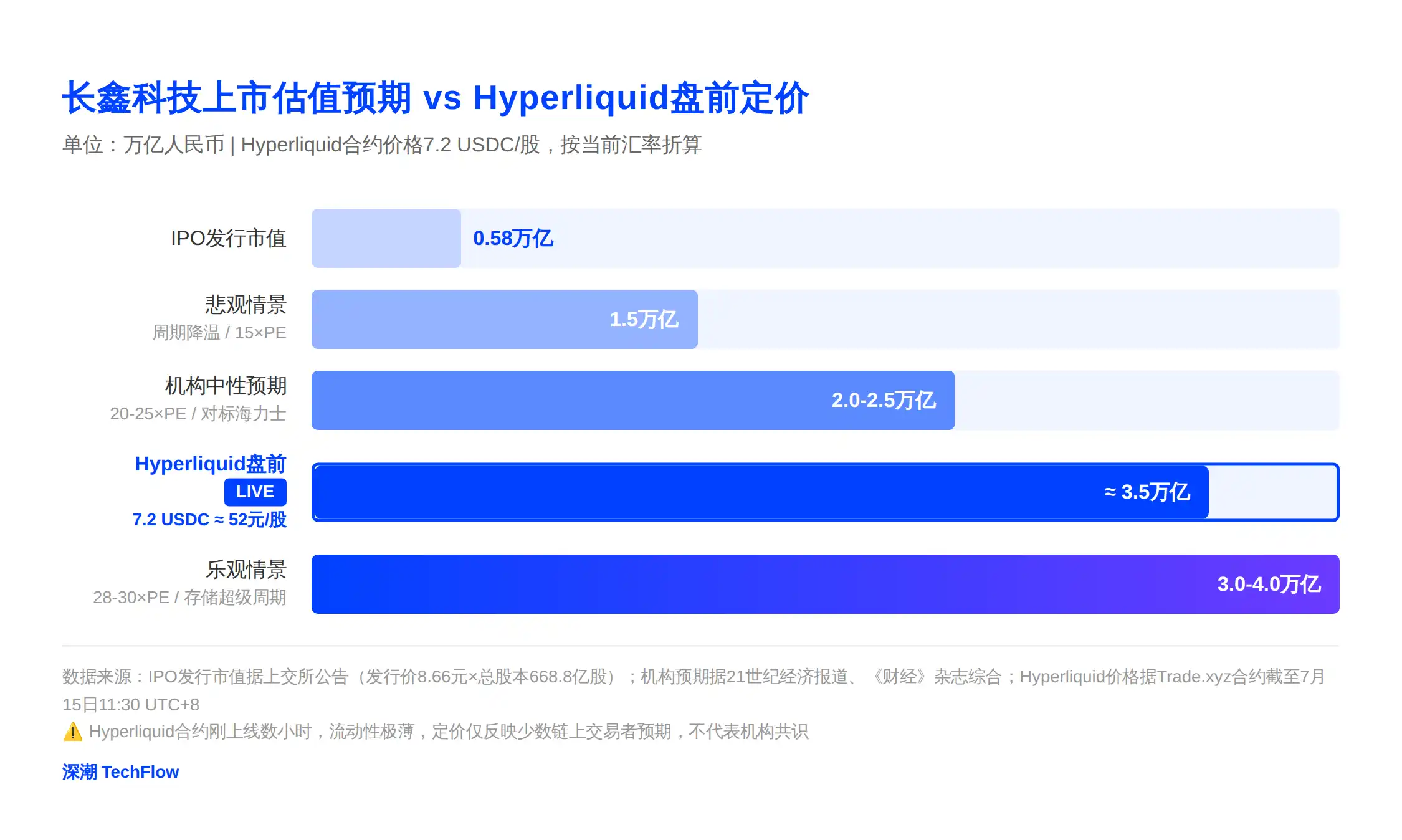

Shenchao Guide: Changxin Technology's STAR Market IPO is priced at 8.66 yuan/share, raising 57.9 billion yuan, with subscriptions starting on July 16. On the eve of subscription, Trade.xyz deployed a CXMT perpetual contract on Hyperliquid. The current trading price is 7.2 USDC (approximately 52 yuan/share). The 24-hour trading volume is $1.32 million, open interest is $2.41 million, and the implied market cap is about 3.5 trillion yuan, at the upper end of institutional expectations of 2-3 trillion yuan. This is the first time a pre-IPO contract on-chain has targeted a STAR Market IPO, and it's the most direct entry point for overseas investors to intervene in the "Chinese Storage Substitution" narrative.

Changxin Technology hasn't rung the bell at the Shanghai Stock Exchange, but price discovery in the crypto market has already begun.

According to a Bloomberg report on July 15, Trade.xyz deployed a Changxin Technology (CXMT) perpetual contract on the Hyperliquid blockchain, with contract code xyz:CXMTUSD. As of writing, the contract's 24-hour trading volume is approximately $1.32 million, open interest is about $2.41 million, and the funding rate is 0.0014%. The price has risen from an initial mark price of around $6 to $7.2, a 20% increase in 24 hours.

This is not Hyperliquid's first attempt at pre-IPO pricing. In May this year, before AI chip company Cerebras went public, the Hyperliquid pre-IPO contract price differed from the Nasdaq opening price by only 1.3%. In June, on SpaceX's IPO day, the on-chain contract saw a single-day trading volume of $1.38 billion. However, targeting a STAR Market-listed company is a first.

$7.2 Equals Approximately 52 Yuan/Share, Implied Market Cap of ~3.5 Trillion Yuan

The contract tracks the per-share price in USDC, using the same logic as the pre-IPO contracts for SpaceX and Cerebras.

Converted at the current exchange rate, $7.2 is approximately 52 yuan/share. Multiplying by the total post-issuance shares of 66.88 billion, the implied total market capitalization is about 3.5 trillion yuan, roughly 6 times the IPO issuance market cap of 579.2 billion yuan.

This pricing falls within the optimistic range of sell-side institutional expectations. The 21st Century Business Herald quoted investment banking sources saying that Changxin Technology's post-listing valuation is expected to reach 2 to 2.5 trillion yuan; Caijing Magazine, synthesizing calculations from multiple institutions, gave an optimistic scenario of 3 to 4+ trillion yuan. Hyperliquid's pre-market pricing of 3.5 trillion yuan sits between the upper end of the neutral range and the lower end of the optimistic range.

Another interpretation: If these on-chain traders' judgment is accurate, Changxin Technology's stock price may open around 50 yuan on its first trading day, about 6 times the 8.66 yuan issue price. The average first-day gain for STAR Market IPOs in the first half of this year was 489%, so a 6x opening is not unrealistic.

With less than 24 hours since the contract launched, the $1.32 million trading volume and $2.41 million open interest represent preliminary liquidity for the on-chain market, but there's still an order-of-magnitude gap compared to the $1.38 billion single-day trading volume on SpaceX's listing day. This price reflects the directional judgment of early participants, not institutional-grade pricing.

A-Shares Can't Be Sold on Purchase Day, No Short Selling: Perpetual Contracts Naturally Fill the Gap

Why would crypto traders care about a Chinese A-share? The views of some investors on overseas social media platforms might explain. The structural limitations of the A-share market are precisely the opportunity for perpetual contracts.

There are two structural limitations in the A-share market. T+1 settlement means you cannot sell on the same day you buy, and short selling (securities lending) is not available for individual STAR Market stocks. For a stock like Changxin Technology, which may experience massive volatility on its first trading day, A-share holders face an awkward situation: even if they profit from the daily limit-up, they cannot lock in that profit on the same day, fully exposed to the risk of a high-open low-close the next day.

The perpetual contracts on Hyperliquid don't have these restrictions. They trade 24/7, allow both long and short positions, and leverage is adjustable. In theory, investors holding Changxin Technology A-shares could open short positions on Hyperliquid to hedge overnight risks.

However, the absence of an arbitrage path is a real issue. Cerebras and SpaceX listed on Nasdaq, allowing global investors to freely arbitrage between the underlying stock and the contract, leading to rapid price convergence. Changxin Technology is listing on the Shanghai Stock Exchange's STAR Market. The 500,000 yuan asset threshold and QFII quota restrictions prevent the vast majority of overseas retail investors from directly buying the underlying shares.

A price gap may persist long-term between the contract price and the actual A-share trading price, for which investors need to price in an additional premium.

Foreign Capital Can't Buy A-Shares, DeFi Becomes the Entry Point for the "Chinese Storage Substitution" Narrative

Blockchain.News explicitly stated in its report: The CXMT contract provides overseas traders with a channel to bypass the STAR Market's 500,000 yuan threshold.

This demand isn't fabricated. Changxin Technology is the world's fourth-largest DRAM supplier, with a 7.7% global market share in Q1. SemiAnalysis predicts it may surpass Micron to become the world's third-largest by year-end. Apple has begun testing Changxin Technology's DRAM chips for devices in the Chinese market (according to the Financial Times report on July 8). Expected net profit attributable to shareholders for the first half of 2026 is 50 to 57 billion yuan, with a profit margin of about 70%, on par with SK Hynix's 73% and Samsung's 81%.

For a company like this going public, global storage industry investors are paying attention, but most can't buy it. Crypto research firm Citrini has repeatedly recommended Hyperliquid's perpetual contract scenario in paid research reports, while also being bullish on Changxin Technology.

Given foreign capital's inability to directly participate in A-shares, the Hyperliquid contract may become the most convenient channel for them to engage with the "Chinese Storage Substitution" theme.

From a broader perspective, this is the first time DeFi infrastructure is being used to create a parallel pricing market for a STAR Market target. Hyperliquid's HIP-3 framework allows any entity staking 500,000 HYPE tokens (worth approximately $28 million) to deploy a perpetual contract. Trade.xyz, utilizing this mechanism, has successively launched pre-IPO contracts for companies like SpaceX, Cerebras, OpenAI, and Anthropic, generating over $1.46 billion in cumulative trading volume. After TradingView integrated data sources from Hyperliquid and Trade.xyz on July 2, price charts for on-chain perpetual contracts have entered mainstream market terminals.

It's worth noting that Hyperliquid's Policy Center and TradeXYZ recently met with the SEC's Crypto Assets and Cyber Unit to discuss cryptocurrency regulation. Based on the current regulatory trajectory, US regulation is the primary compliance focus for the platform; the Chinese regulatory risk brought by A-share targets is not currently within its consideration.

(Note: Hyperliquid is not available to users in China.)

57.9B in Fundraising, 66B H1 Net Profit: Changxin Technology Itself is the Event of the Year

Returning to the A-share context, even without the Hyperliquid contract, Changxin Technology's IPO itself is already a landmark event in the 2026 Chinese capital market.

The issue price is 8.66 yuan/share. Based on the initial issuance of 6.688 billion shares, it's expected to raise 57.9 billion yuan, nearly double the original plan of 29.5 billion yuan. If the over-allotment option is fully exercised, the fundraising amount will reach 66.6 billion yuan, making it the largest IPO in Asia this year and the largest semiconductor IPO in A-share history. The price-to-earnings (P/E) ratio is 308.92x, far exceeding the industry average of 76.32x. However, the market isn't concerned because the Q1 net profit of 33 billion yuan is rapidly diluting the valuation. The company expects revenue of 110 to 120 billion yuan and net profit attributable to shareholders of 50 to 57 billion yuan for the first half of 2026, representing year-over-year growth exceeding 2244%.

More importantly, timing. The global DRAM market is in a rare super-cycle boom. Samsung, SK Hynix, and Micron are shifting significant capacity to HBM high-bandwidth memory required for AI servers, leading to tight supply of consumer-grade DRAM. In Q1, DRAM contract prices surged 90% to 95% quarter-over-quarter, the largest single-quarter increase in history. Changxin Technology focuses on consumer-grade DDR5 and LPDDR5X products, with a monthly capacity of 200,000 to 300,000 wafers. It is one of the few global manufacturers expanding production of consumer-grade DRAM against the trend, capturing the capacity gap strategically left by the three giants.

On the A-share IPO subscription side, all 71 new IPOs in the first half of this year rose on their debut, with STAR Market IPOs averaging a 489% first-day gain. Retail investors can participate in the online subscription on July 16, subscription code 787825, with an estimated listing date of July 27.

For A-share investors, the July 16 subscription is the main gate. For overseas investors, Hyperliquid's CXMT contract has opened a side door. After the official listing on July 27, whether the contract price can quickly converge to the actual trading price like Cerebras will be a key test to see if this model can be replicated for A-shares. But even if the price doesn't converge, the mere existence of this parallel market itself demonstrates that global capital's interest in the Chinese storage substitution narrative is more than just talk.