CoinW Research Institute

Original Title: US-Iran Conflict Escalation: How Do Prediction Markets Price War Risk Ahead of Oil Prices?

Abstract

This article takes the escalation of the US-Iran conflict as a starting point to analyze how a geopolitical event is rapidly transformed into a global risk variable in the contemporary financial system. Since the event occurred on a weekend when traditional financial markets were closed, on-chain markets remained operational. Crypto assets and on-chain commodity contracts experienced sharp fluctuations first, completing the initial expression of risk; prediction markets directly probabilized war and political changes, achieving real-time pricing of the event path. After traditional markets opened on Monday, energy, the US dollar, US bonds, and risk assets completed systematic confirmation, with risk premiums transmitted step by step along the macro chain. The article points out that in the 24/7 digital market environment, risk is no longer priced only at the opening bell. Geopolitics is being financialized in real-time; markets are not just passively reacting to events but are participating in the pricing of risk itself during the development of events.

1. Conflict Escalation: How a Geopolitical Event Becomes a Global Risk Variable

Recently, tensions between the US and Iran escalated sharply. Multiple media reports indicated that Iran's Supreme Leader Ayatollah Ali Khamenei was killed in an airstrike, leading to a rapid deterioration of the regional situation. Military actions and tough statements combined quickly turned the situation from a regional friction into a global focus.

Subsequently, the Islamic Revolutionary Guard Corps of Iran announced restrictions on ships passing through the Strait of Hormuz. As one of the world's most important energy transportation channels, this key hub, which long carries about one-fifth of global crude oil and liquefied natural gas transportation, once faced severe restrictions, with many shipping companies suspending passage or choosing detours.

The impact of the conflict is no longer limited to the military level. The Middle East is the core region of global energy supply, and disturbances in the Strait of Hormuz directly push up energy risk premiums, which are quickly transmitted to global markets through oil prices, inflation expectations, and capital flows.

Therefore, this conflict has become a global risk variable with systemic significance. It affects not only the regional security landscape but also the energy supply-demand balance, the dollar liquidity environment, and the valuation system of risk assets.

When war escalates into a systemic risk, where is the risk traded first? Under the structure where traditional markets operate on a time schedule while on-chain markets run 24/7, the timing of price discovery is changing.

2. Weekend Time Window: On-Chain Markets Complete the First Round of Price Discovery

It is worth noting that this conflict escalation occurred on a weekend. When the news broke, most global traditional financial markets were closed: spot gold paused quotes, crude oil futures stopped trading, and stock markets were closed. Risk had emerged, but the traditional system could not price it immediately. However, on-chain markets were still operating, and risk sentiment shifted to a still-open pricing venue.

Crypto Assets Lead Sharp Fluctuations

After the conflict news emerged, Bitcoin's price once approached $63,000, then rebounded to near $66,000, completing significant fluctuations in a short time. This volatility was not simply safe-haven buying or panic selling but a concentrated game of risk expectations in the absence of traditional anchors like gold and crude oil. When other assets could not be traded, the crypto market became an outlet for risk expression.

On-Chain Commodity Contracts: Risk Premiums Form Instantly

During the weekend, multiple media reported that on the Hyperliquid platform, perpetual contracts linked to crude oil, gold, and silver showed significant increases: crude oil perpetual contracts rose about 5% to approximately $70.6/barrel; gold perpetual contracts rose about 1.3% to approximately $5,323/ounce; silver perpetual contracts rose about 2% to approximately $94.9/ounce. Trading volumes also expanded. Silver contracts had a 24-hour trading volume of over $227 million, and gold contracts about $173 million, showing real fund participation. These were prices truly formed in the 24/7 on-chain market, reflecting the immediate judgment of market participants on supply risks and geopolitical premiums during the closure of traditional markets.

Monday Opening: Traditional Markets "Catch Up"

When traditional markets reopened, prices quickly adjusted in the direction of the weekend on-chain movements. International oil prices opened higher on Monday, with Brent crude rising to $82.37/barrel at one point, and WTI crude jumping above $75; spot gold broke through $5,300/ounce; major global stock indices futures generally weakened, with risk assets under pressure. Prices showed a clear time sequence: risk occurred on the weekend; on-chain markets fluctuated first; traditional markets completed larger-scale confirmation and diffusion on Monday.

In the time window when traditional markets were closed, on-chain markets undertook the first wave of risk expression. This structural time difference is changing the pricing rhythm of global risk events.

3. Prediction Markets: War Is Probabilized in Real-Time for the First Time

Polymarket: Explosive Pricing of Conflict Nodes

In this event, the trading scale of contracts related to conflict escalation on the on-chain prediction platform Polymarket significantly expanded.

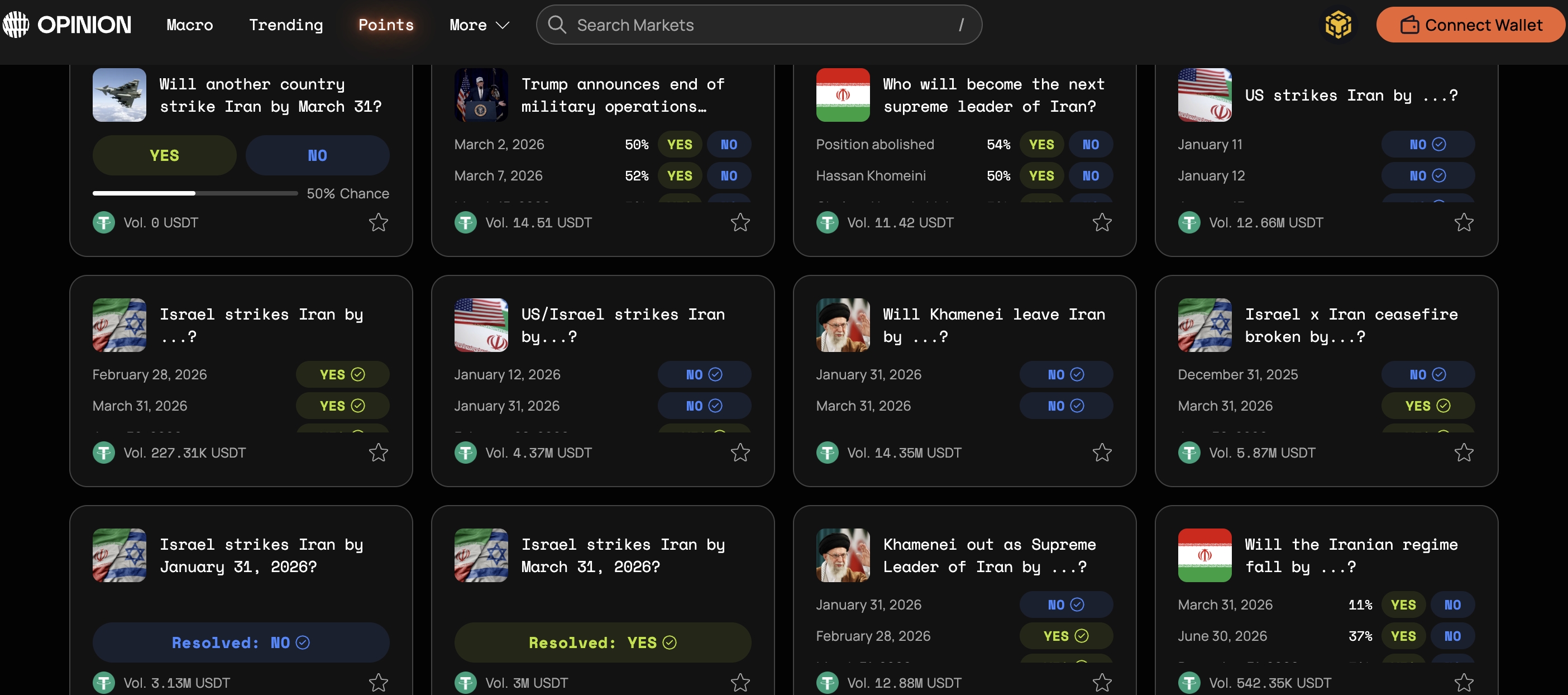

The series of contracts on "Will the US or Israel strike Iran by a certain date?" had a cumulative trading volume of over $500 million, with the trading volume on the day of the airstrike alone reaching about $90 million, becoming one of the largest geopolitical markets in the platform's history.

After the confirmation of the leader's death, contracts related to "Will Khamenei lose his position as Supreme Leader of Iran by March 31?" were quickly settled, with a trading volume of about $57 million. The implied probability of contracts like "Will the Iranian regime collapse by June 30?" once rose to nearly 50%, indicating that the market had begun to price deeper institutional risks. These data show that betting was not scattered behavior but formed concentrated and high-intensity fund participation.

Source: https://polymarket.com/event/khamenei-out-as-supreme-leader-of-iran-by-march-31

Opinion: Multi-Dimensional Pricing of Conflict Paths and Institutional Risks

On Opinion, contracts related to the US-Iran conflict also showed high activity. One type of market directly defines military triggers precisely. For example, "Will the US strike Iran by a certain date?" stipulates that it is judged as Yes only if the US military actually hits Iranian territory or official embassies with drones, missiles, or air strikes, and intercepted weapons or other forms of military action are not counted. The trading volume of this contract has exceeded $12.6 million, showing the market's high attention to specific military trigger conditions.

Source:https://app.opinion.trade/search?q=Iran

Another type of market turns to institutional layer risks. "Khamenei out as Supreme Leader of Iran by ...?" prices whether Iran's Supreme Leader Ali Khamenei loses power within a specific time window. The rules include resignation, detention, loss of position, or inability to perform duties as judgment standards, and use credible media consensus as the settlement basis, with a volume of about $12.9 million. In addition, markets like "Will the Iranian regime collapse by XX date?" and "Will the ceasefire between Israel and Iran be broken by XX date?" probabilistically express regime stability and ceasefire sustainability, respectively.

Although the number of related contracts and the overall trading scale are still lower than Polymarket, Opinion presents a clearer risk stratification: military actions, ceasefire status, leader retention, and regime direction are decomposed into multiple independent variables and priced in parallel. War is thus no longer just a single-point question of "whether it happens" but a risk path that can be segmented, quantified, and continuously corrected. Prediction markets here serve as real-time measurement tools for sovereign risk and institutional stability.

Probability Curve as a "Risk Thermometer"

Unlike crude oil or gold, prediction markets do not indirectly express risk through assets but directly probabilize pricing of "whether an event occurs." When the probability of conflict escalation rises, odds jump; when the situation eases, the probability falls. The odds curve itself becomes an immediate scale of risk sentiment. Some analysis pointed out that a few hours before the airstrike news spread widely, a small number of new wallets concentrated on buying related contracts and profited after the event was confirmed. This phenomenon sparked discussions on whether information entered the market in advance, making the time sensitivity of prediction markets particularly prominent.

Traditional markets usually reflect results through rising oil prices or falling stock markets; prediction markets directly trade "whether it escalates" and "whether it spreads." The former prices the impact, the latter prices the path. When traditional markets are not yet open, risk is already quantified and bet on the chain.

4. Traditional Asset Opening Confirmation: How Are Risk Premiums Transmitted?

When on-chain markets fluctuate first, true cross-asset linkage occurs after traditional markets reopen.

Energy: The First Stop for Risk Premiums

Energy remains the first stop for risk premiums. The Strait of Hormuz carries about 20% of global crude oil transportation. As long as the market worries that supply may be hindered, oil prices will提前计入 risk premiums in advance. Conflict escalation pushes oil prices up, thereby boosting inflation expectations and affecting interest rate policies and corporate cost structures.

Dollar and US Bonds: Tug-of-War Between Safety and Inflation

When uncertainty rises, funds usually flow to the most liquid assets, so the US dollar and US bonds benefit short-term. The dollar strengthens, and US bond yields fall阶段性, reflecting rising safe-haven demand. But if the conflict continues and pushes up inflation expectations, US bond yields may face a tug-of-war between safe-haven buying and inflationary pressure.

Positioning of Risk Assets and Bitcoin

Gold undertakes traditional safe-haven functions, crude oil embodies risk premiums, and US bonds provide a liquidity safety cushion. Bitcoin's performance is closer to high-elasticity risk assets. In the initial stage of the conflict, it did not rise unilaterally but fluctuated violently, showing its high sensitivity to liquidity and risk appetite. Therefore, in the initial stage of extreme uncertainty, Bitcoin is more like a high-beta risk asset than a pure safe-haven tool.

Overall, on-chain markets express risk first, prediction markets probabilize risk, and traditional assets complete systematic confirmation after opening. Risk premiums are transmitted step by step along energy, interest rates, and asset valuation, eventually forming a联动 reaction in global markets.

5. Structural Changes: Is the Risk Pricing Mechanism Migrating?

The significance of this event may not only lie in the conflict itself but in how risk is priced.

Geopolitics Is Being Financialized in Real-Time

In the past, geopolitics remained more at the news and diplomatic levels; now, it is being financialized in real-time. Whether war escalates, whether sanctions are implemented, and how election results evolve can all be bet on, hedged, and probabilized in the market. Risk is no longer only interpreted after the fact but is traded during the process of occurrence.

On-Chain Markets Become 24/7 Risk Buffers

On-chain markets are beginning to take on a new function. Traditional markets have weekend closures and holiday suspensions. When major events happen to occur in this gap, prices cannot reflect sentiment immediately. But on-chain markets operate 24/7, becoming a buffer for the first wave of sentiment release. Prices and probabilities fluctuate there first, and then, when traditional markets open, larger-scale confirmation and diffusion occur.

Price Discovery Rights Are Marginally Migrating

This time structure difference is bringing a deeper change: the marginal migration of price discovery rights. If on-chain contracts fluctuate first, if the odds curve of prediction markets jumps before oil prices and stock indices, will institutional investors start monitoring these data? Will macro models incorporate on-chain fluctuations into reference variables? Will media and traders regard prediction market probabilities as risk early warning signals?

These questions are not yet settled, but the direction is already apparent. The "first expression" of risk is shifting from the opening bell of traditional exchanges to digital markets that run 24/7. When war can be traded in real-time, the market is no longer just passively responding to the outcome of events but is participating in the pricing process of risk itself.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Communication Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush