Original Author: Ryan Yoon, Tiger Research

Original Compilation: Saoirse, Foresight News

99% of Web3 projects have no cash income, yet many companies still invest huge amounts of money in marketing and events every month. This article will delve into the survival rules of these projects and the truth behind "burning money".

Core Points

- 99% of Web3 projects lack cash flow, and their cost expenditures rely on tokens and external funds, not product sales.

- Premature listing (token issuance) leads to a surge in marketing expenditures, which in turn weakens the competitiveness of the core product.

- The reasonable price-to-earnings ratio (P/E) of the top 1% of projects proves that the remaining projects lack actual value support.

- Early token generation events (TGE) allow founders to "exit and cash out" regardless of the project's success or failure, creating a distorted market cycle.

- The "survival" of 99% of projects essentially stems from a system defect built on investor losses rather than corporate profits.

Prerequisite for Survival: Verified Revenue Ability

"The prerequisite for survival is having verified revenue ability"—this is the most core warning in the current Web3 field. As the market matures, investors no longer blindly chase vague "visions". If a project cannot attract real users and actual sales, token holders will quickly sell and leave.

The key issue is the "fund turnover period", which is the time a project can maintain operations in a non-profit state. Even without sales, costs such as wages and server fees still need to be paid monthly, and teams without income have almost no legal channels to maintain operating funds.

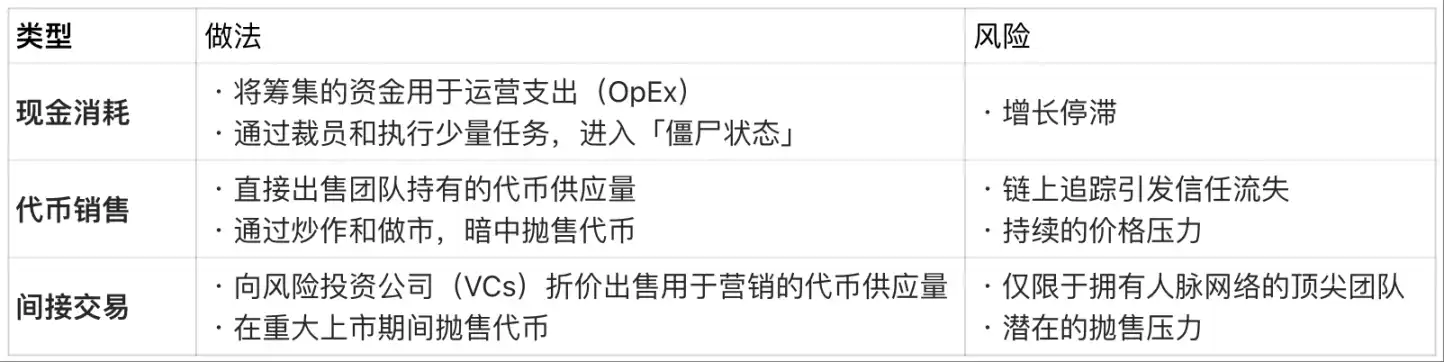

Financing costs without income:

However, this "survival by tokens and external funds" model is only a stopgap measure. There is a clear upper limit to assets and token supply. Eventually, projects that exhaust all funding sources either cease operations or quietly exit the market.

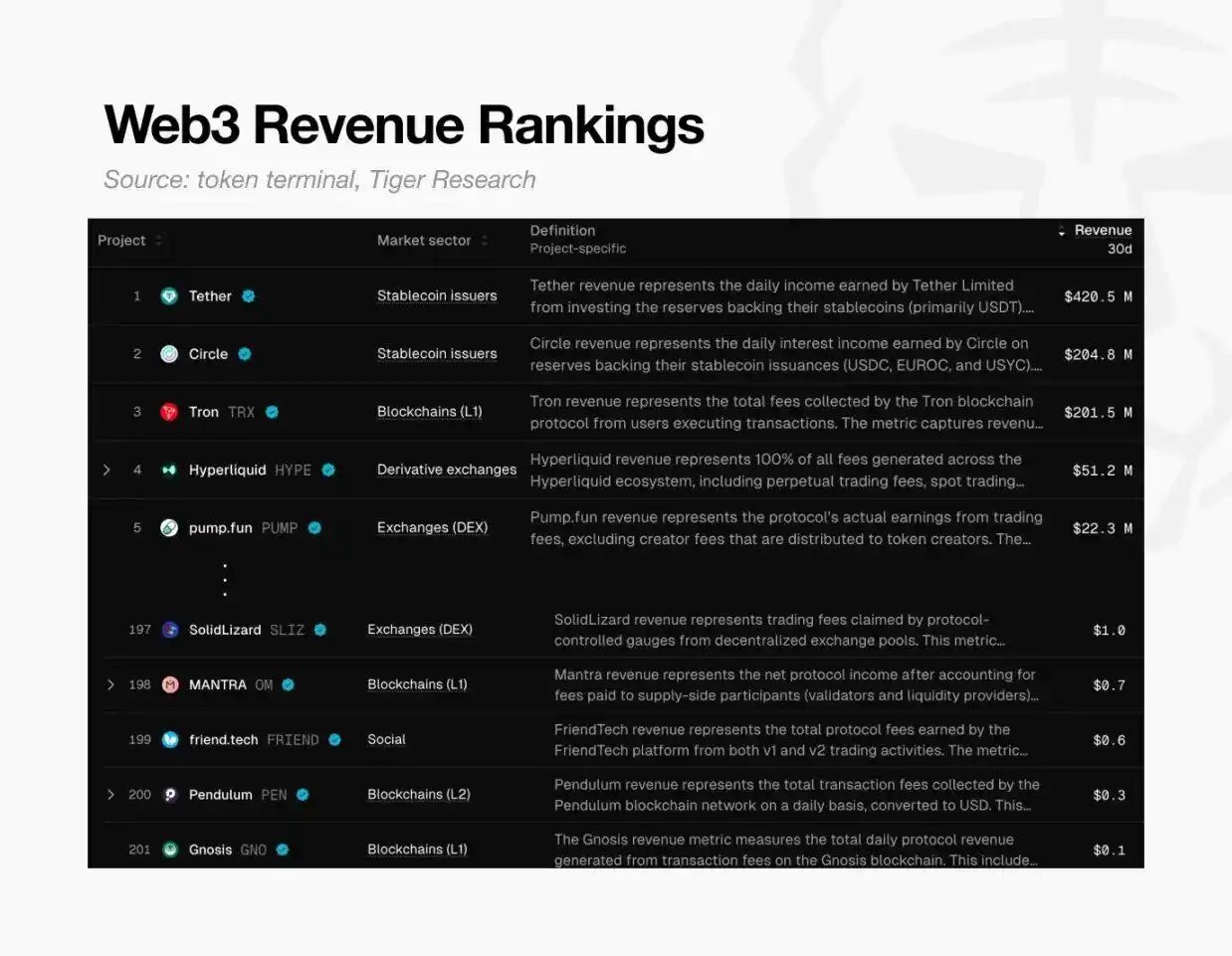

Web3 Revenue Ranking Table, Source: token terminal and Tiger Research

This crisis is universal. According to Token Terminal data, globally, only about 200 Web3 projects have achieved an income of $0.10 in the past 30 days.

This means that 99% of projects do not even have the ability to pay their own basic costs. In short, almost all cryptocurrency projects have failed to verify the feasibility of their business models and are gradually declining.

High Valuation Trap

This crisis was largely predetermined. Most Web3 projects completed their listing (token issuance) based solely on "vision", without even launching an actual product. This is in stark contrast to traditional enterprises—traditional enterprises must first prove their growth potential before an initial public offering (IPO); in the Web3 field, teams instead have to prove the rationality of their high valuation after listing (token generation event TGE).

But token holders will not wait indefinitely. As new projects emerge daily, if a project fails to meet expectations, holders will quickly sell and leave. This puts pressure on the token price, thereby threatening the project's survival. Therefore, most projects invest more funds in short-term hype rather than long-term product development. Obviously, if the product itself lacks competitiveness, even the most intensive marketing will eventually fail.

- If only focus on product development: It takes a lot of time, and during this period, market attention will gradually fade, and the fund turnover period will continue to shorten;

- If only focus on short-term hype: The project becomes empty and lacks actual value support.

Both paths ultimately lead to failure—the project cannot prove the rationality of its initial high valuation and eventually collapses.

See the Truth of 99% of Projects Through the Top 1%

However, 1% of top projects have proven the feasibility of the Web3 model with huge revenues.

We can judge the value of major profitable projects such as Hyperliquid and Pump.fun through their price-to-earnings ratio (PER). The price-to-earnings ratio is calculated as "market capitalization ÷ annual income", and this indicator can reflect whether the project valuation is reasonable relative to actual income.

Price-to-earnings ratio comparison: Top Web3 projects (2025):

Note: Hyperliquid's sales are annualized estimates based on performance since June 2025.

The data shows that the price-to-earnings ratio of profitable projects ranges from 1x to 17x. Compared with the average price-to-earnings ratio of the S&P 500 index of about 31x, these top Web3 projects are either "undervalued relative to sales" or "have excellent cash flow conditions".

The fact that top projects with actual returns can maintain a reasonable price-to-earnings ratio makes the valuation of the remaining 99% of projects untenable—it directly proves that the high valuation of most projects in the market lacks a basis in actual value.

Can This Distorted Cycle Be Broken?

Why can projects with no sales still maintain valuations of billions of dollars? For many founders, product quality is only a secondary factor—Web3's distorted structure makes "quick exit and cash out" much easier than "building a real enterprise".

The cases of Ryan and Jay can explain this well: both launched AAA-level game projects, but the final outcomes were completely different.

Founder differences: Web3 vs. traditional model comparison

Ryan: Chose TGE, abandoned deep development

He chose a path centered on "profit": obtaining early funds by selling NFTs before the game was launched; then, while the product was still in a rough development stage, he held a token generation event (TGE) based solely on an aggressive roadmap and completed the listing on a medium-sized exchange.

After listing, he maintained the token price through hype, buying time for himself. Although the game was eventually launched late, the product quality was extremely poor, and holders sold and left. Ryan finally resigned on the grounds of "taking responsibility", but he was the real winner of this game—

On the surface, he pretended to focus on work, but in reality, he received a high salary while making huge profits by selling unlocked tokens. Regardless of the project's final success or failure, he quickly accumulated wealth and exited the market.

In contrast, Jay: Followed the traditional path, focused on the product itself

He prioritized product quality over short-term hype. But the AAA-level game development takes years, during which his funds were gradually exhausted, and he fell into a "fund turnover crisis".

In the traditional model, founders have to wait until the product is launched and sales are achieved before they can get considerable returns. Although Jay raised funds through multiple rounds of financing, he eventually shut down the company before the game was developed due to lack of funds. Unlike Ryan, Jay not only did not get any profit, but also was burdened with huge debts and left a record of failure.

Who is the Real Winner?

Neither case produced a successful product, but the winner is clear: Ryan accumulated wealth by utilizing Web3's distorted valuation system, while Jay lost everything in the process of trying to build a quality product.

This is the cruel reality of the current Web3 market: using excessive valuation to exit early is much easier than building a sustainable business model; and ultimately, the cost of this "failure" is all borne by investors.

Back to the initial question: "How do 99% of non-profit Web3 projects survive?"

This cruel reality is the most honest answer to that question.