Author | Asher(@Asher_ 0210)

The credibility of "everything is predictable" continues to rise.

On the evening of January 5th, the on-chain real estate platform Parcl announced a collaboration with the prediction market Polymarket, aiming to introduce Parcl's daily housing price index into Polymarket's new real estate prediction market. Following this news, Parcl's token PRCL saw a short-term surge of over 150%, currently retracting slightly to $0.042, with a market cap of $19 million.

PRCL Price Chart

Operational Details of Polymarket's Real Estate Prediction Market Section

Collaboration Details:

- Parcl provides daily housing price indices as an independent, transparent reference data for market settlement;

- Polymarket is responsible for listing and operating the markets, where users can trade using USDC on the Polygon chain;

- Market settlements are based on Parcl's publicly verifiable index, avoiding the delays (typically monthly) and subjectivity of traditional real estate data.

Market Types:

- Predicting whether housing prices will rise/fall within a month, quarter, or year;

- Threshold markets: e.g., whether housing prices exceed a specific level;

- Each market is linked to Parcl's dedicated settlement page, displaying final values, historical data, and index calculation methods.

Coverage:

- Initially starting with high-liquidity U.S. cities, such as New York, Miami, San Francisco, Austin, etc.;

- Subsequently expanding to more cities and market types based on user demand.

Example Display:

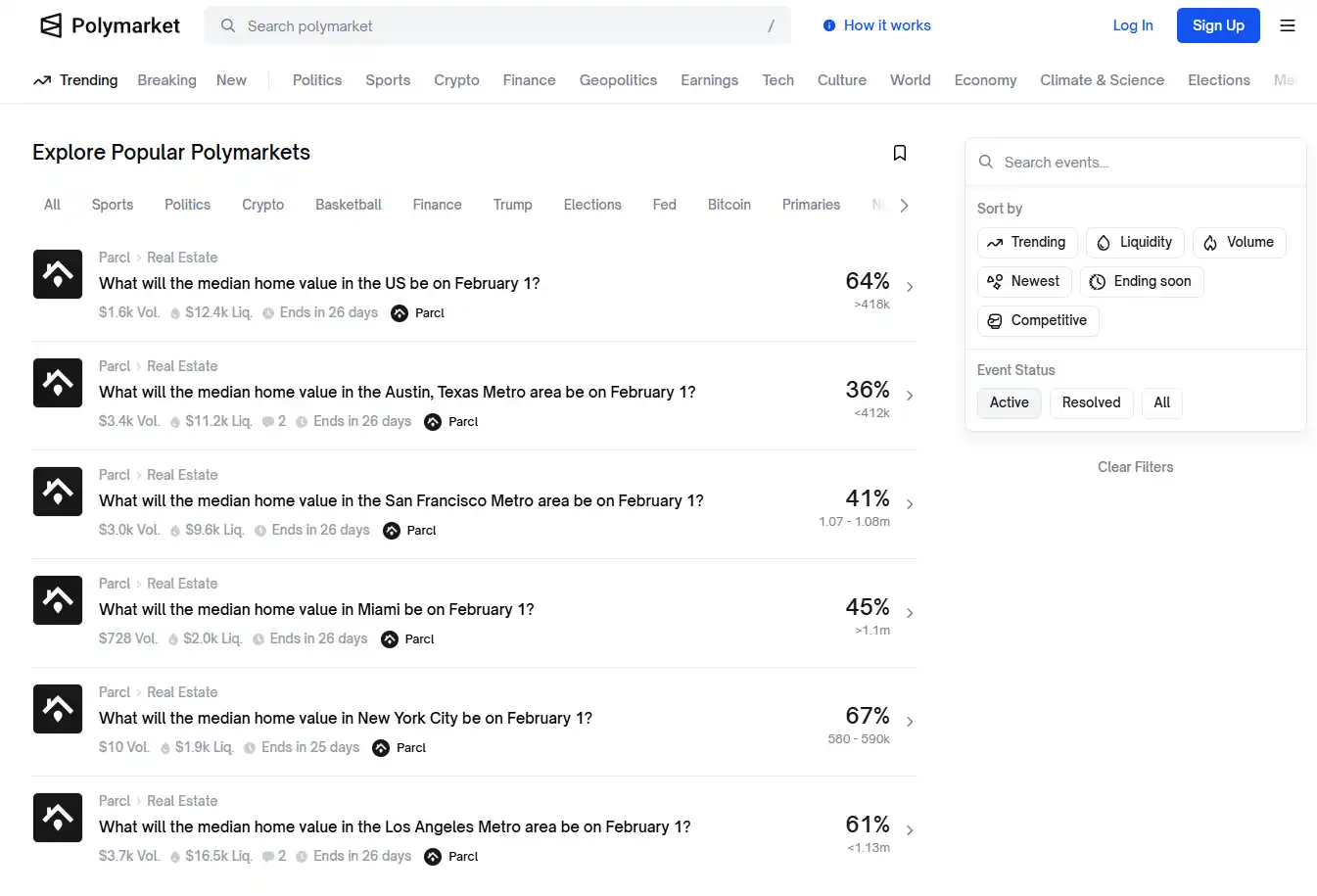

Currently, this section has only listed 7 monthly real estate prediction events, with low liquidity. The event with the highest trading volume, "U.S. Los Angeles Housing Agent Price on February 1st," has only $3,700.

Polymarket's New Real Estate Prediction Market Section

In traditional real estate markets, whether bullish or bearish, such expectations are difficult to express directly, let alone form continuous market signals. Polymarket's introduction essentially separates "judgments on housing prices" from asset transactions. As long as there is a clear settlement standard, expectations themselves can be priced independently.

The Real Estate Market Finally Sees a "Shorting Tool"

An easily overlooked fact is that the potential demand for real estate-related markets does not only come from native speculators.

In the traditional financial system, "falling housing prices" are almost a risk that cannot be directly hedged. Whether holding property or having asset structures and income sources highly dependent on a city's real estate cycle, the practical response is often to continue holding or directly sell physical assets—high transaction costs, long cycles, and a lack of flexible intermediate options. As KOL 0xMarioNawfal (@RoundtableSpace) stated: "This is far more than just betting; it's about bringing liquidity to one of the world's most illiquid markets. Imagine housing prices are at historic highs, and you expect a crash but can't sell your house—now you can hedge and short the market."

The introduction of prediction markets abstracts the decline in housing prices into a tradable risk judgment. When housing prices are high and market expectations begin to weaken, the trend of real estate prices itself can be priced separately without having to dispose of underlying assets for risk management.

Through Polymarket, the downside risk of real estate prices is abstracted into a tradable judgment rather than requiring the disposal of physical assets. From this perspective, Polymarket's real estate prediction market is closer to a simplified macro hedging mechanism than a mere speculative game around rises and falls. It does not change the liquidity structure of real estate assets themselves but provides a tradable layer that can reflect expectations in real-time for a long-term illiquid market.

Polymarket CMO Matthew Modabber stated: "Prediction markets are best suited for events with clear, verifiable data. Parcl's daily housing price index provides us with a transparent, consistent settlement foundation. Real estate should become a first-class category in prediction markets."

The collaboration between Polymarket and Parcl also introduces traditional real estate price signals into the crypto system: Originally low-frequency, closed, and high-barrier assets are broken down into settleable, verifiable, and tradable index results, resembling stock indices or crypto derivatives. This may be a more practical and demand-aligned implementation path in the RWA narrative.