Author: Claude, Deep Tide TechFlow

Deep Tide Guide: U.S.-Iran negotiations break down, the Hormuz Strait blockade is initiated, oil prices return above $100, yet the S&P 500 closed up 1% on Monday, completely erasing all losses since the Iran war to reach 6886 points. J.P. Morgan, Morgan Stanley, and BlackRock all expressed bullish views on the same day, with a consistent core logic: corporate profit resilience far outweighs the impact of geopolitical shocks. The investment section of Reddit exploded with activity, with retail investors exclaiming, 'The market simply ignores the news.'

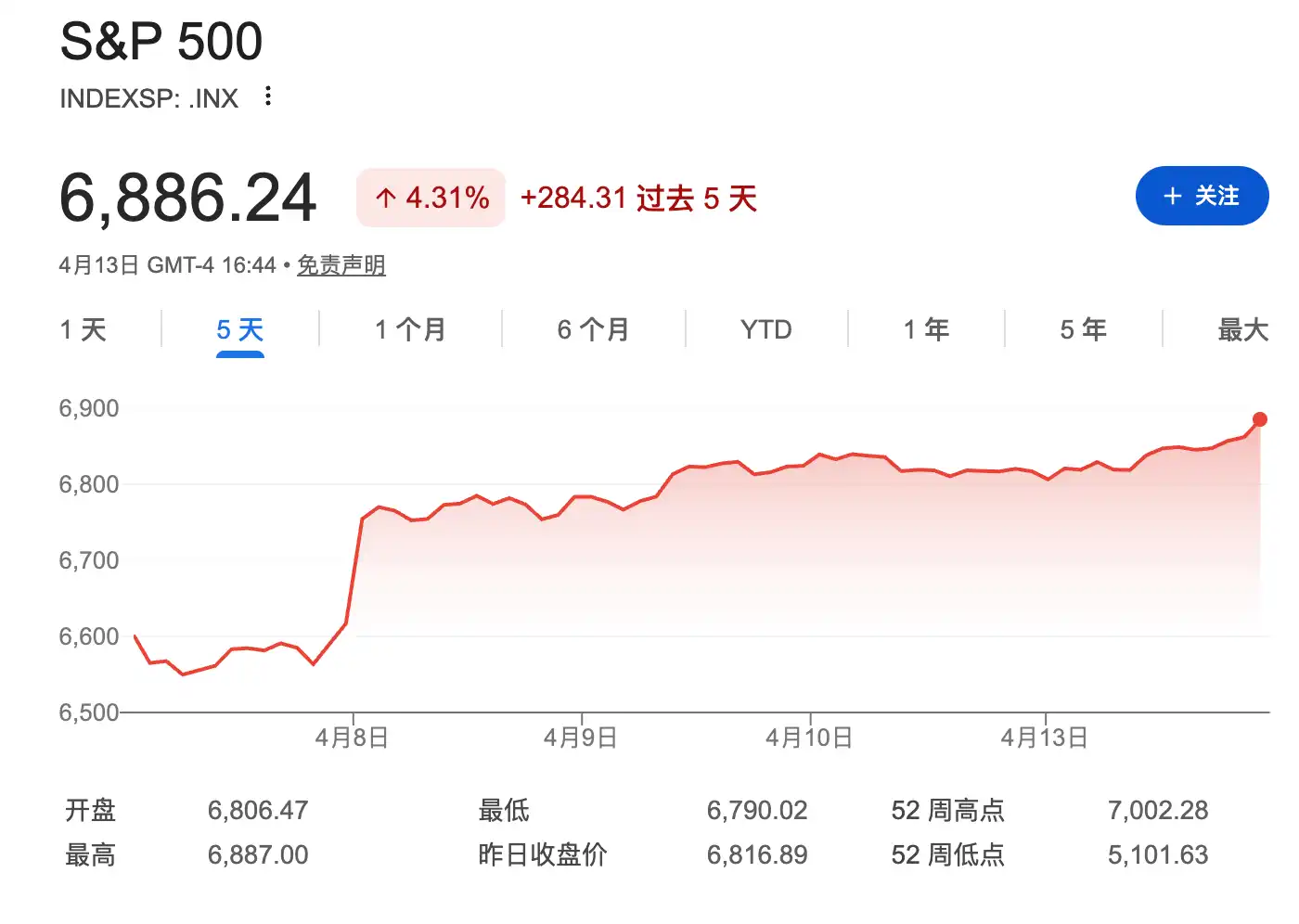

On the first trading day after the breakdown of U.S.-Iran negotiations, U.S. stocks charted a curve that left everyone puzzled.

On April 13 (Monday), the S&P 500 closed up 69 points, a gain of 1%, at 6886 points; the Dow Jones Industrial Average rose 302 points, up 0.6%; the Nasdaq Composite Index increased by 1.2%. On the same day, Trump announced on a social platform that the U.S. Navy would immediately initiate a blockade operation in the Hormuz Strait. Brent crude oil broke through $100 per barrel during the session before pulling back to close around $98.16, while WTI crude closed at $97.82.

The S&P 500 rose to its highest level since the end of February that day, fully recovering all the losses incurred since the outbreak of the Iran war. The simultaneous occurrence of surging oil prices and rising stock markets seems logically contradictory. However, the largest institutions on Wall Street provided a highly consistent explanation: corporate profits remain strong, the persistence of geopolitical shocks is limited, and the current moment presents a window for buying on the dip.

Three Major Institutions Bullish on the Same Day, Core Logic Points to Profit Resilience

J.P. Morgan, in a research report authored by strategist Mislav Matejka, stated that declines driven by geopolitical shocks should ultimately prove to be buying opportunities.

Morgan Stanley strategist Michael Wilson's team judged that the recent sell-off in the S&P 500 resembled a correction rather than the start of a sustained downturn, with supporting factors coming from improved profit growth and a return to reasonable valuations. Morgan Stanley continues to be bullish on cyclical sectors such as financials, industrials, and consumer discretionary, as well as high-quality growth targets like AI hyperscale computing.

On the same day, the BlackRock Investment Institute upgraded its rating on U.S. stocks from 'neutral' to 'overweight,' making it the most active mover among the three. Jean Boivin, head of the BlackRock Investment Institute, stated that the valuation premium of the technology sector has been eroded, while the sector's expected profit growth rate for 2026 has risen to 43%, higher than last year's 26%.

BlackRock pointed out in its weekly market report that the two signposts triggering its decision to increase exposure have appeared: first, there is tangible evidence showing that navigation through the Hormuz Strait is resuming, and second, the sustained damage of the conflict to the macroeconomy has proven to be manageable.

The three institutions cited the same set of data: according to LSEG I/B/E/S data, as of April 10, the expected Q1 profit growth rate for the S&P 500 is 13.9%, higher than the pre-war 12.7%. In other words, nearly seven weeks after the conflict erupted, analysts have not only failed to lower profit expectations but have instead raised them.

Valuation Contraction of the 'Magnificent Seven' Becomes a Reason to Buy

J.P. Morgan specifically mentioned in its report that the forward P/E premium of the 'Magnificent Seven' (Nvidia, Apple, Microsoft, Meta, Google, Amazon, and Tesla) has narrowed significantly from the previous level of 1.7 times the S&P 500 to 1.2 times.

This data constitutes a key argument for Wall Street bulls: the problem of top-heavy concentration that has suppressed market breadth over the past two years is being alleviated on its own due to valuation regression.

BlackRock pointed out that the valuation premium of the technology sector relative to the other ten sectors has fallen to its lowest level since mid-2020. The company stated that against the backdrop of firm corporate profit expectations and limited damage to global growth, it has decided to increase exposure to U.S. stocks and emerging markets.

Historical Data Backs It Up: Geopolitical Shocks Are Usually Digested Within Six Weeks

The optimism of Wall Street institutions is not without basis. Research from UBS shows that when the S&P 500 falls 5% to 10% within three to four weeks, it historically usually returns to pre-conflict levels within six months.

A review of geopolitical shock events since World War II by LPL Research shows that the average first-day reaction is approximately a 1% decline, the average peak-to-trough decline is about 5%, the average time to bottom is about 19 days, and the average recovery cycle is about 42 days.

UBS stated in a mid-March research report that from the outbreak of the conflict on February 28 to March 13, global stocks fell only about 5%, while crude oil prices rose about 40% during the same period. The stock market's 'insensitivity' to the oil price shock itself validates the above historical pattern.

On April 6, UBS lowered its year-end target price for the S&P 500 from 7700 to 7500 and its mid-term target from 7300 to 7000, but maintained its overall judgment that U.S. stocks are 'attractive,' with the 2026 EPS forecast unchanged at $310.

Reddit Investors' Soul-Searching Question: 'The Market Simply Ignores the News'

While the consensus among institutions can be explained by data, the reaction in retail communities more directly reflects current market sentiment.

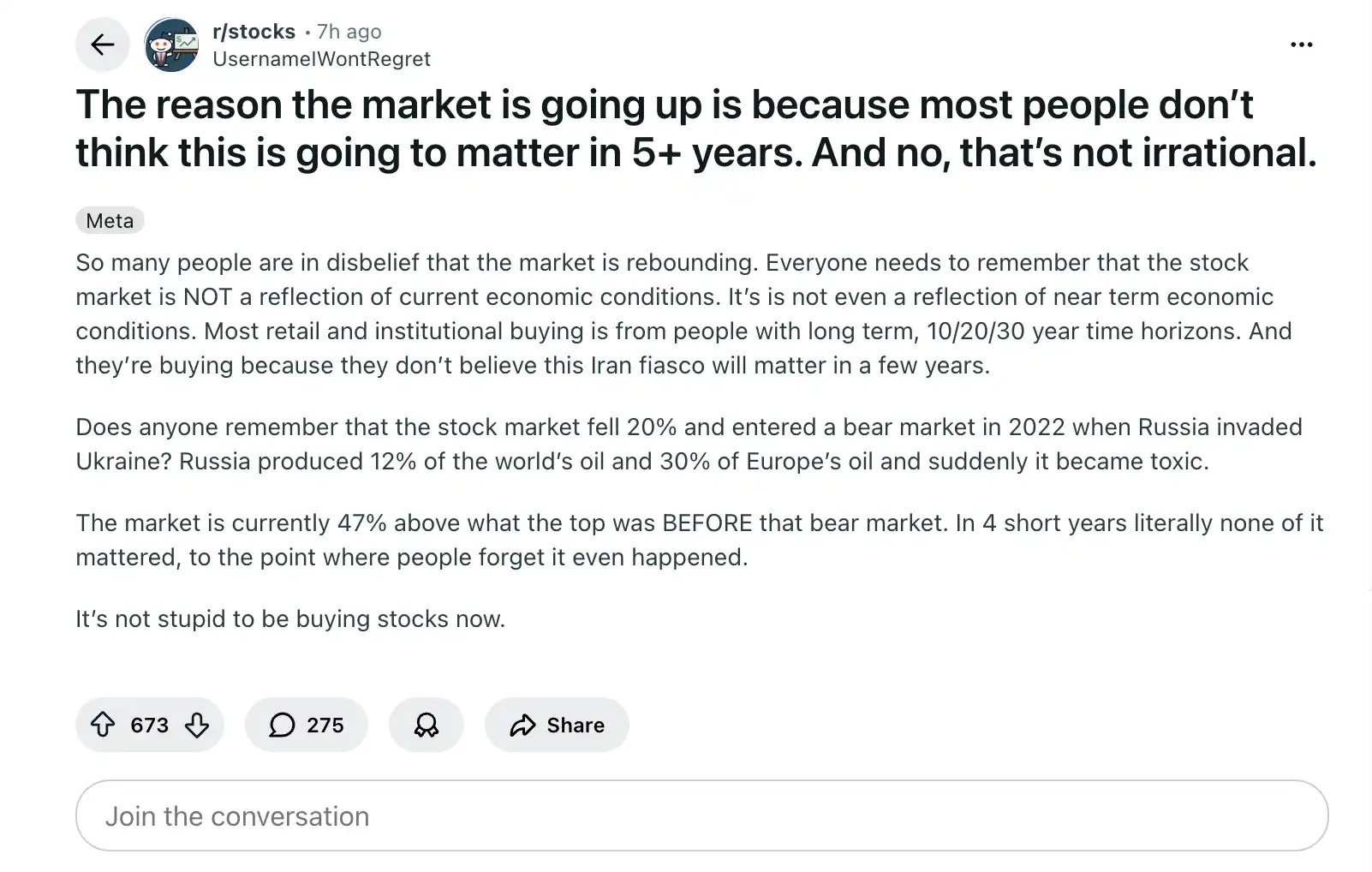

In the r/stocks subreddit, a post titled roughly 'Do you believe it now? The market doesn't move because of the news' received 923 upvotes and 159 comments. The poster's core point was: the market moves first, then finds reasons later. This Hormuz blockade is the most typical case he has experienced. A large number of comments expressed confusion about the disconnect between geopolitical risks and market pricing.

'The market is rising because most people think this won't matter in 5 years; this is not irrational.' This post received 344 upvotes and 199 comments, representing the typical stance of long-term investors.

In the r/wallstreetbets subreddit, a post with 504 upvotes pointed out that the physical oil market is 'screaming supply shock,' but the stock market remains calm, leaving traders不知所措 (at a loss) due to the contradictory signals between the two markets.

The confusion of retail investors and the confidence of institutions form a sharp contrast, but the underlying logic is actually two sides of the same coin: institutions are betting on profit resilience and the limited nature of the conflict, while retail investors are confused about why bad news hasn't translated into declines.

The answer might be simple: the market already completed a round of pricing in March and is currently in a rebound phase where 'bad news is exhausted.'