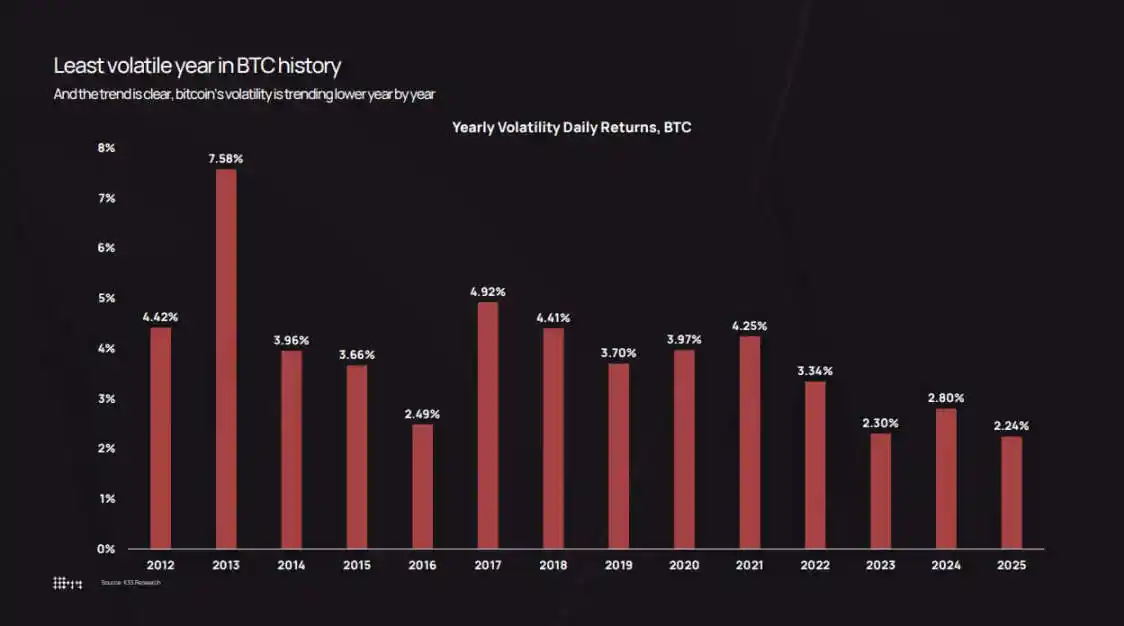

Bitcoin concluded 2025 with a realized daily volatility of 2.24%, marking the lowest annual figure on record for the asset.

K33 Research's volatility chart, which dates back to 2012—when Bitcoin's daily volatility was 7.58%—shows that volatility has steadily decreased each cycle: 3.34% in 2022, 2.80% in 2024, and dropping to 2.24% in 2025.

However, market perception diverges from the data. In October 2025, Bitcoin's price fell from $126,000 to $80,500, a nerve-wracking process; on October 10th, a wave of liquidations triggered by tariff policies wiped out $19 billion in leveraged long positions in a single day.

The paradox lies here: by traditional standards, Bitcoin's volatility has indeed decreased, but compared to previous cycles, it is attracting larger inflows of capital, and the absolute magnitude of price swings is also greater.

Low volatility does not mean "the market has gone quiet"; rather, it indicates the market is now mature enough to handle institutional-scale capital flows without reverting to the "chain-reaction" feedback loops seen in earlier cycles.

Today, ETFs, corporate treasuries, and regulated custodians act as "ballast" for market liquidity, while long-term holders are steadily reallocating assets into this infrastructure.

The end result: Bitcoin's daily returns are more stable, yet market cap fluctuations still amount to hundreds of billions of dollars—swings that would have triggered an 80% crash back in 2018 or 2021.

Volatility Continues to Decline

K33's annual volatility data documents this transition.

In 2013, Bitcoin's average daily return was 7.58%, reflecting the thin order books and speculative fervor of the market at that time. By 2017, this figure had dropped to 4.81%; in 2020, it was 3.98%; during the pandemic bull market of 2021, it saw a slight rebound to 4.13%. In 2022, the successive collapses of Luna, Three Arrows Capital, and the FTX exchange pushed volatility up to 3.34%.

Since then, volatility has continued its downward trend: 2.94% in 2023, 2.80% in 2024, and 2.24% in 2025.

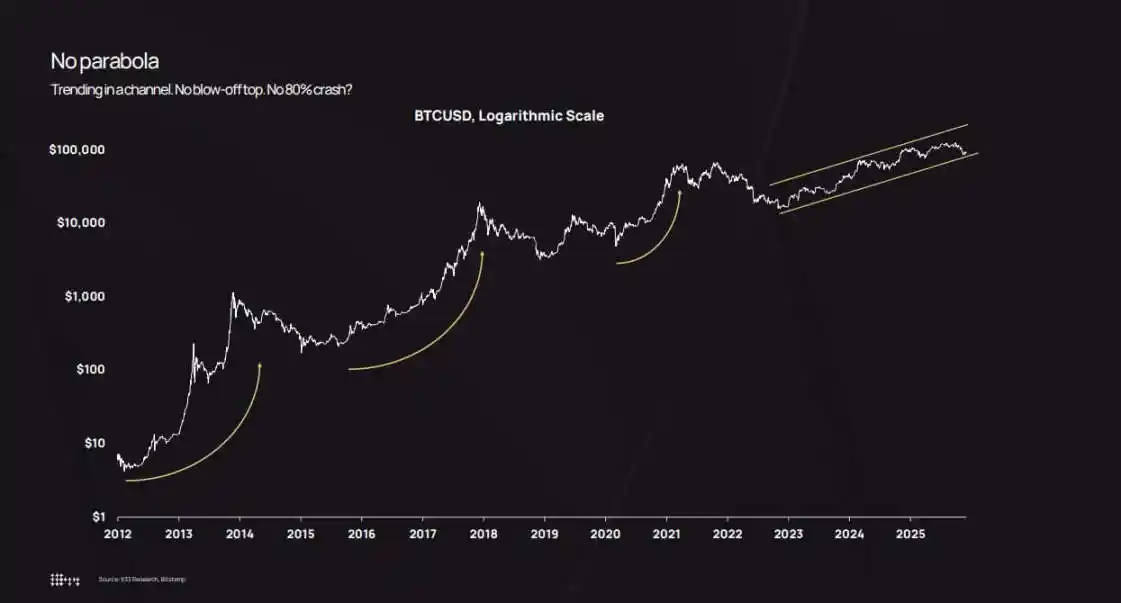

A logarithmic price chart further confirms this trend. From 2022 to 2025, Bitcoin did not experience extreme "pump-and-dump" rallies but instead climbed steadily within an upward channel.

There were pullbacks—the price dropped below $50,000 in August 2024 and to $80,500 in October 2025—but none resulted in a "parabolic surge followed by a systemic crash."

Analysis points out that the approximately 36% decline in October 2025 still falls within the normal range of historical Bitcoin drawdowns. The difference is that previous 36% corrections often occurred at the tail end of high volatility periods around 7%, whereas this one appeared during a low volatility period of 2.2%.

This creates a "perception gap": a 36% drop over six weeks still feels剧烈 intuitively; but compared to early cycles (when intraday 10% swings were the norm), the price action in 2025 was relatively calm.

Asset management firm Bitwise points out that Bitcoin's realized volatility is now lower than Nvidia's, a shift that redefines Bitcoin's positioning from a "pure speculative tool" to a "high-beta macro asset."

Market Cap Expansion, Institutional Entry, and Asset Reallocation

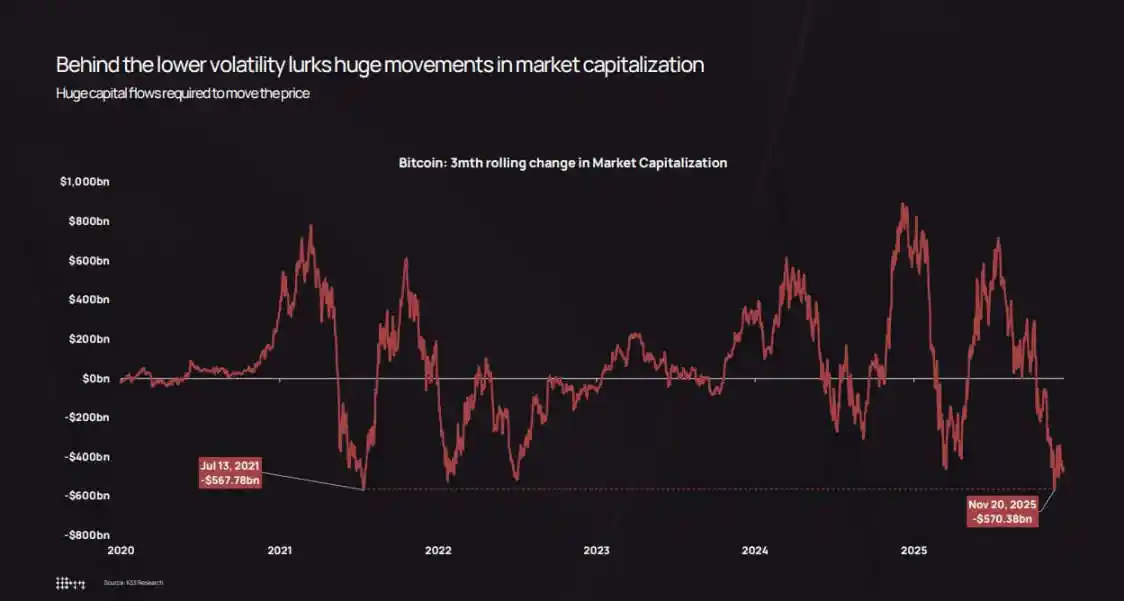

K33's core view is that the decline in realized volatility is not due to reduced capital inflows, but because it now takes much larger capital movements to move the price.

The firm's chart of "three-month changes in Bitcoin's market cap" shows that even during this low-volatility cycle, fluctuations in market cap still amount to hundreds of billions of dollars.

During the October-November 2025 pullback, Bitcoin's market cap evaporated approximately $570 billion, nearly identical to the $568 billion drawdown in July 2021.

The magnitude of the swings hasn't changed; what has changed is the "depth" of the market absorbing these swings.

Three structural factors have driven the decline in volatility:

First, the "accumulation" effect of ETFs and institutions. K33 statistics show that ETFs net purchased approximately 160,000 Bitcoin in 2025 (though lower than the 630,000+ in 2024, the scale remains considerable). ETFs and corporate treasuries combined added about 650,000 Bitcoin, accounting for over 3% of the circulating supply. This capital entered the market through "programmatic rebalancing," not driven by retail FOMO sentiment.

K33 specifically notes that even as Bitcoin's price fell about 30%, ETF holdings only decreased by single-digit percentages, with no panic redemptions or forced liquidations.

Second, corporate treasuries and structured issuance. By the end of 2025, corporate treasuries cumulatively held approximately 473,000 Bitcoin (the pace of accumulation slowed in the second half of the year). New demand came more from preferred stock and convertible bond issuance rather than direct cash purchases—because finance teams execute capital structure strategies quarterly, unlike traders chasing short-term market trends.

Third, the reallocation of assets from early holders to a broader base. K33's "asset holding period analysis" shows that since early 2023, Bitcoin dormant for over two years began steadily "activating"; over the past two years, about 1.6 million long-held Bitcoin entered circulation.

2024 and 2025 were the two years with the largest activation of "dormant assets." The report mentions that in July 2025, Galaxy Digital sold 80,000 Bitcoin, and Fidelity sold 20,400 Bitcoin.

These sales恰好 coincided with the "structural demand" from ETFs, corporate treasuries, and regulated custodians—who build their holdings gradually over months.

This reallocation is crucial: early holders accumulated Bitcoin at prices between $100 and $10,000, with assets often in a few concentrated wallets; when they sell, the assets flow to ETF shareholders, corporate balance sheets, and high-net-worth clients buying small amounts through diversified portfolios.

The end result: lower concentration of Bitcoin ownership, thicker order books, and weakened "chain-reaction feedback loops." In early cycles, a sale of 10,000 Bitcoin into a illiquid market could cause a 5% to 10% price crash, triggering stops and liquidations; but in 2025, such a sale attracts buy-side interest from multiple institutional channels, potentially even pushing the price up 2% to 3%. Feedback loops weaken, and daily volatility decreases accordingly.

Portfolio Construction, Leverage Shocks, and the End of "Parabolic Cycles"

The decline in realized volatility changes the calculus for institutions regarding "Bitcoin allocation size."

Modern Portfolio Theory suggests that asset allocation weights should be based on "risk contribution" rather than "return potential." The same 4% allocation to Bitcoin: if daily volatility is 7%, its contribution to portfolio risk is far higher than when volatility is 2.2%.

This mathematical fact forces asset allocators to choose: either increase the allocation to Bitcoin, or utilize options and structured products (assuming the underlying asset's volatility is more stable).

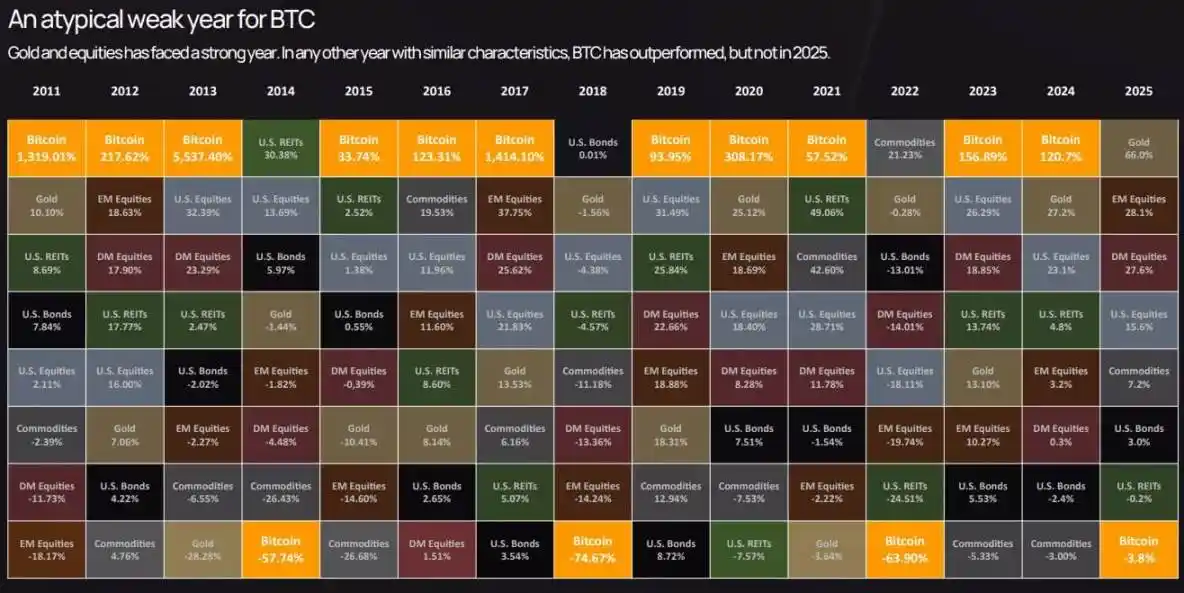

K33's cross-asset performance table shows Bitcoin ranked near the bottom in terms of asset returns in 2025—despite outperforming for multiple years in previous cycles, it lagged behind gold and stocks in 2025.

This "underperformance," combined with low volatility, shifts Bitcoin's定位 from a "speculative satellite asset" to a "core macro asset"—with risk similar to stocks, but return drivers uncorrelated with other assets.

The options market also reflects this shift: recent Bitcoin option implied volatility has declined alongside realized volatility, lowering hedging costs and making synthetic structured products more attractive.

Previously, compliance departments often restricted financial advisors from allocating to Bitcoin due to "excessive volatility"; now, advisors have quantitative grounds: in 2025, Bitcoin's volatility was lower than Nvidia's, lower than many tech stocks, and comparable to high-beta stock sectors.

This opens new investment channels for Bitcoin: inclusion in 401(k) retirement plans, allocations by Registered Investment Advisors (RIAs), and insurance company portfolios with strict volatility limits.

K33's forward-looking data predicts that as these channels open, 2026 ETF net inflows will exceed those of 2025, creating a "self-reinforcing cycle": more institutional inflows → lower volatility → unlocking more institutional mandates → more inflows.

But the market's "calm" is conditional. K33's derivatives analysis shows that throughout 2025, Bitcoin perpetual swap open interest steadily rose in a "low vol, strong uptrend" environment, culminating in the October 10th liquidation event—which wiped out $19 billion in leveraged longs in a single day.

This sell-off was related to President Trump's tariff announcement and broad "risk-off sentiment," but the core mechanism was still a derivatives issue: excessive leveraged longs, thin weekend liquidity, cascading margin calls.

Even with an annual realized volatility of 2.2%, "extreme volatility days triggered by leverage unwinds" can still be hidden. The difference is: such events are now resolved within hours, not weeks; and because现货 demand from ETFs and corporate treasuries provides a "price floor," the market can recover quickly.

The structural backdrop for 2026 supports the view that "volatility will remain low or decline further": K33 expects selling from early holders to decrease as the two-year-old Bitcoin supply stabilizes; additionally, there are positive regulatory signals—the U.S. CLARITY Act, full implementation of Europe's MiCA, and Morgan Stanley and Bank of America opening 401(k) and wealth management channels.

K33's "Golden Opportunity" data predicts Bitcoin will outperform stock indices and gold in 2026—because the impact of regulatory breakthroughs and new capital will outweigh selling pressure from existing holders.

Whether this prediction materializes remains uncertain, but the mechanisms driving it—deepening liquidity, improved institutional infrastructure, regulatory clarity—do provide support for low volatility.

Ultimately, the Bitcoin market is moving away from the "speculative frontier"属性 of 2013 or 2017, closer to a "highly liquid, institutionally-anchored macro asset."

This does not mean Bitcoin becomes "boring" (e.g., low returns or lack of narrative), but rather that the "rules of the game have changed": price paths are smoother, the options market and ETF flows matter more than retail sentiment, and the core market changes are reflected in structure, leverage levels, and the composition of buyers and sellers.

In 2025, despite undergoing its largest-ever regulatory and structural changes, Bitcoin became an "institutionalized,平稳 asset" from a volatility perspective.

The value in understanding this transition is this: low realized volatility is not a signal of an "asset losing its vitality," but a sign that "the market is mature enough to handle institutional-scale capital without crashing."

The cycle hasn't ended; it's just that the "cost" of moving the market has become higher.