Author: Knight Frank

Compiled by: Felix, PANews

Global private real estate advisory firm Knight Frank recently released the "2026 Wealth Report," highlighting the rapid expansion of global private wealth and dynamic changes in its geographical distribution. PANews has summarized the core content of the report.

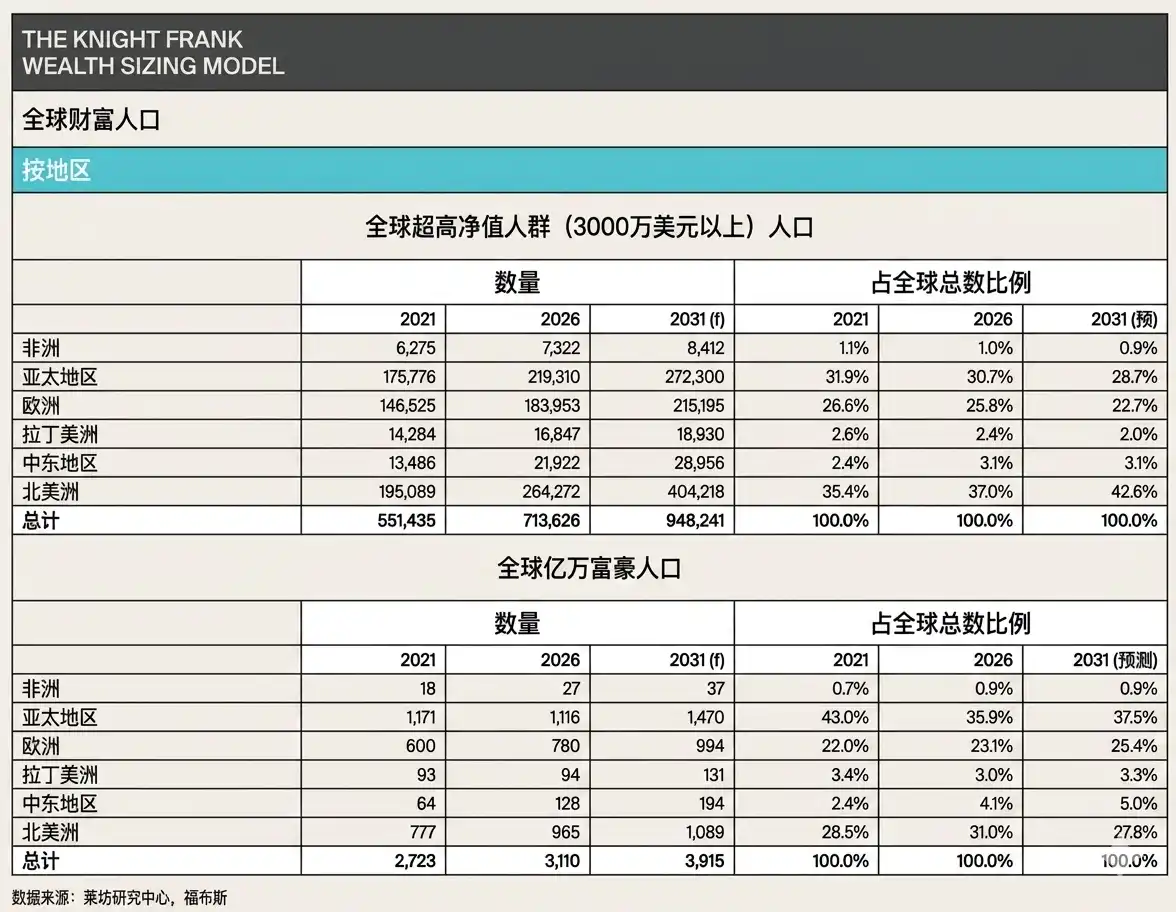

The report shows that between 2021 and 2026, the number of global ultra-high-net-worth individuals (with wealth exceeding $30 million) increased from 551,435 to 713,626, adding 162,191 new ultra-high-net-worth individuals over five years, or an average of 89 people per day breaking through the $30 million wealth threshold.

The United States led this wealth growth. During this period, 41% of all new ultra-high-net-worth individuals came from the U.S. The U.S. share of global ultra-high-net-worth individuals steadily increased from 33% in 2021 to 35% in 2026. By 2031, the U.S. is projected to account for 41% of the world's ultra-high-net-worth individuals.

China remains the world's second-largest wealth creation center, although its relative position is declining. China's share of global ultra-high-net-worth individuals fell from 18% in 2021 to 17% in 2026 and is expected to drop further to 15% by 2031. In fact, almost all countries are losing their global market share to accommodate the continued growth of U.S. wealth.

India is a counterexample. Between 2021 and 2026, its number of ultra-high-net-worth individuals (over $30 million) surged by 63%, from just over 12,000 to nearly 20,000. India's share of global ultra-high-net-worth individuals is only 2.8%, up from just over 2% five years ago. By 2031, the number of ultra-high-net-worth individuals in India is expected to increase from the current 19,877 to 25,217.

Australia holds a position in the global wealth landscape that far exceeds its size. Over the next five years, its number of ultra-high-net-worth individuals is expected to grow by nearly 60%, reaching 26,095, accounting for almost one-thousandth of its total population. Australia has a large number of billionaires, which is projected to grow by 77% between 2026 and 2031.

By region, the global wealth landscape is dominated by three major areas.

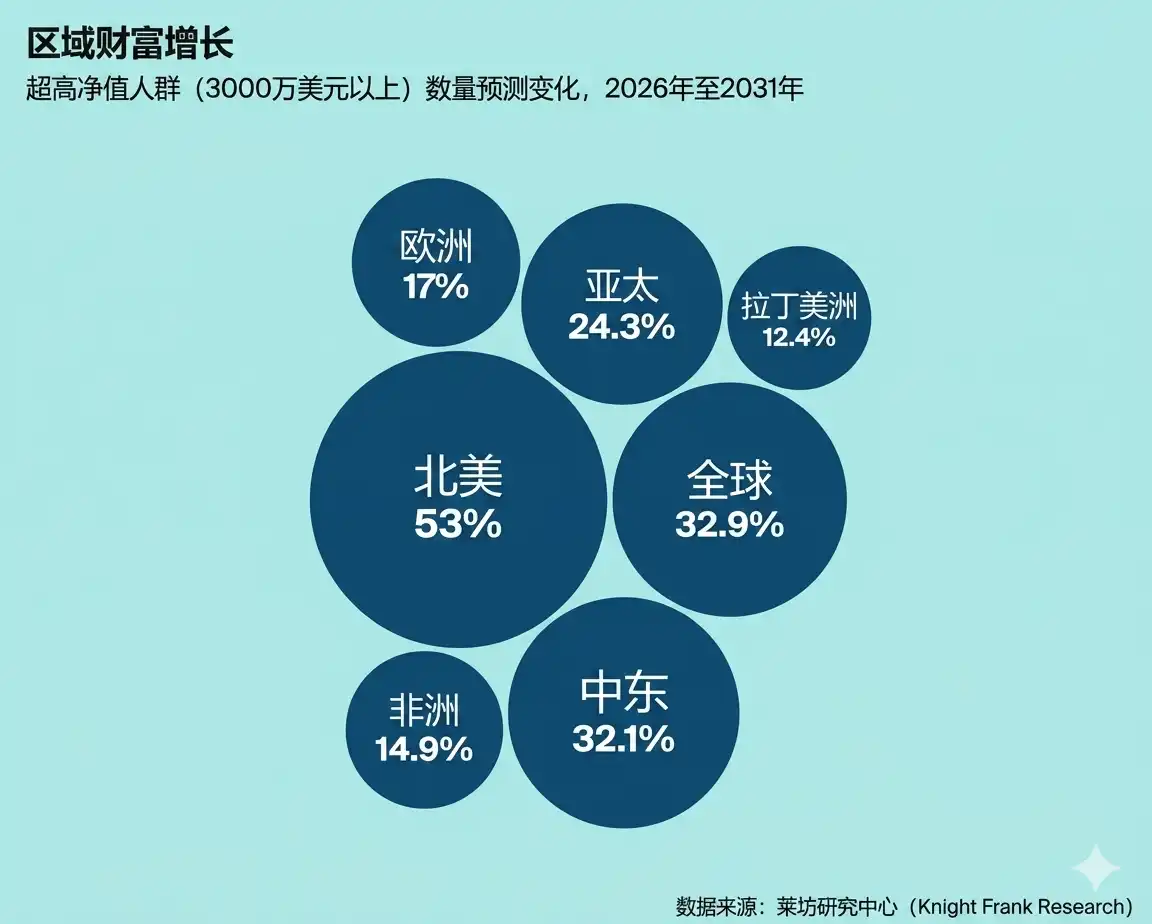

North America leads, accounting for 37% of global ultra-high-net-worth individuals in 2026. The Asia-Pacific region accounts for nearly 31% of ultra-high-net-worth individuals in 2026. Europe follows closely, with 183,953 super-rich, representing about a quarter of the global total. Beyond these regions, the Middle East stands out. Over the past five years, the Middle East's share of global millionaires increased from 2.4% to 3.1%.

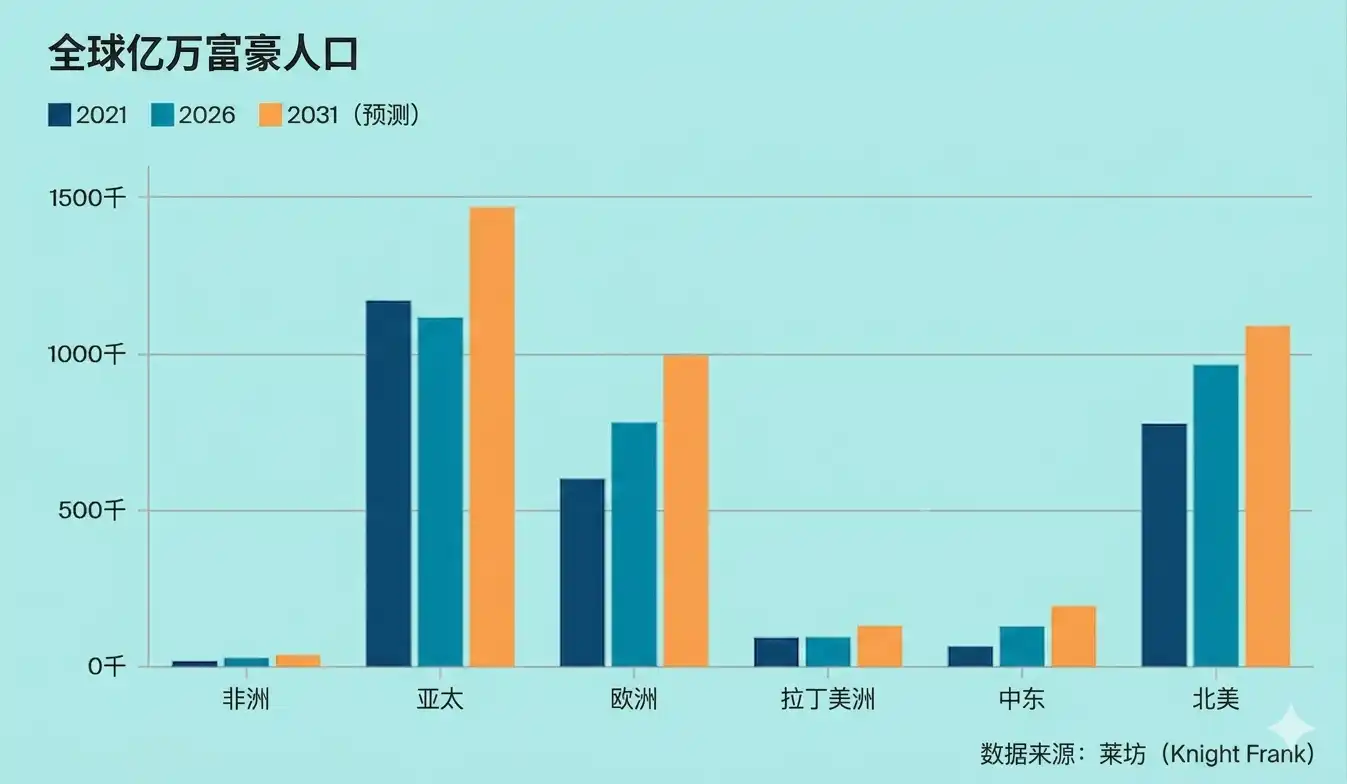

Additionally, the geographical distribution of the world's 3,110 billionaires is more dispersed than the broader ultra-high-net-worth individual group. The Asia-Pacific region has the most billionaires, with 1,116, followed by North America with 965. The Middle East accounts for just over 4% of the world's billionaires, significantly higher than its share of ultra-high-net-worth individuals.

Looking ahead, billionaire growth is expected to be highly geographically diverse. In percentage terms, Saudi Arabia is projected to lead, with its number of billionaires growing by 183%, followed by Poland (123%), Sweden (81%), and Australia (77%). This highlights the increasingly global trend of future billionaire growth.

Over the next five years, the growth of global ultra-high-net-worth individuals will not be led by traditional economies but by some rapidly maturing economies. Indonesia tops the list, with its number of ultra-high-net-worth individuals (over $30 million) expected to surge by 82% by 2031. It is followed by Saudi Arabia and Poland, both with growth rates exceeding 60%. Vietnam's nearly 60% growth highlights the rapid rise of emerging wealth centers in Southeast Asia.

Europe also shows strong performance, with Sweden, Romania, and Greece all achieving significant growth. Although wealth remains concentrated in a few global economic powerhouses, its geographical distribution is expanding.

Related reading: California to 'Harvest' 5% from Billionaires in One Go? Some Are Moving Overnight