Germany’s two largest banking networks are undergoing a major shift by integrating cryptocurrency trading directly into their banking apps. This includes Sparkassen savings banks and the cooperative Volksbanken Raiffeisenbanken.

Through this initiative, the banking network will enable millions of regular retail customers to purchase and sell digital assets without the need for third-party cryptocurrency exchanges.

Good news for Germany’s crypto ecosystem?

These organizations collectively cater to about 80 million clients across Germany, making it one of Europe’s largest integrations of crypto into traditional banking.

For its part, this shift is noteworthy because, only four years ago, both banking groups had written off cryptocurrencies as being too risky. Now, they are creating their own regulated cryptocurrency infrastructure rather than collaborating with outside exchanges.

However, through DZ Bank, the cooperative banks have already introduced the meinKrypto platform. For those unaware, “meinKrypto” is a platform that allows local Volksbanken and Raiffeisenbanken to deliver Bitcoin [BTC] and Ethereum [ETH] directly to millions of retail savers.

Approved by BaFin, Germany’s financial regulator, in December 2025, the platform runs under the European Union’s Markets in Crypto-Assets (MiCA) framework. Following the approval announcement on the 14th of January, ‘meinKrypto’ officially went live.

At the same time, Boerse Stuttgart Digital offers crypto custody, guaranteeing that asset storage and trading continue to be governed by German regulations. Meanwhile, DekaBank is getting ready to launch a comparable service for the nation’s savings banks.

Challenges remain!

Needless to say, the initiative has drawn criticism. This is because only a few percent of Germans who own cryptocurrency trust their main banks far more than independent cryptocurrency platforms.

According to Co-Pierre Georg, professor at the Frankfurt School of Finance & Management, novice clients may underestimate the high volatility and potential for total losses linked to cryptocurrencies due to the legitimacy of well-known banks.

Georg added,

It is concerning that the floodgates to the cryptocurrency market are now being opened by savings and cooperative banks.

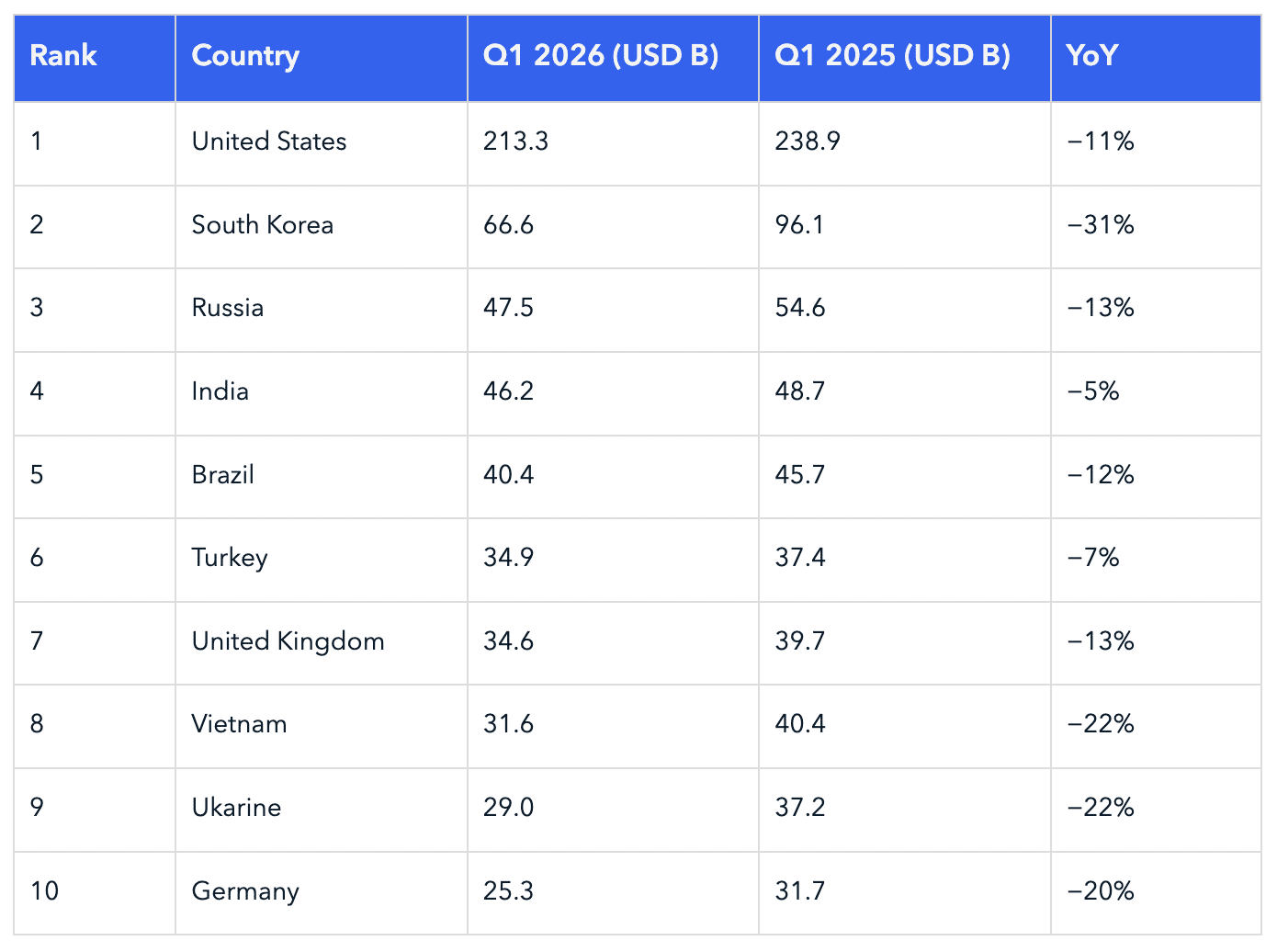

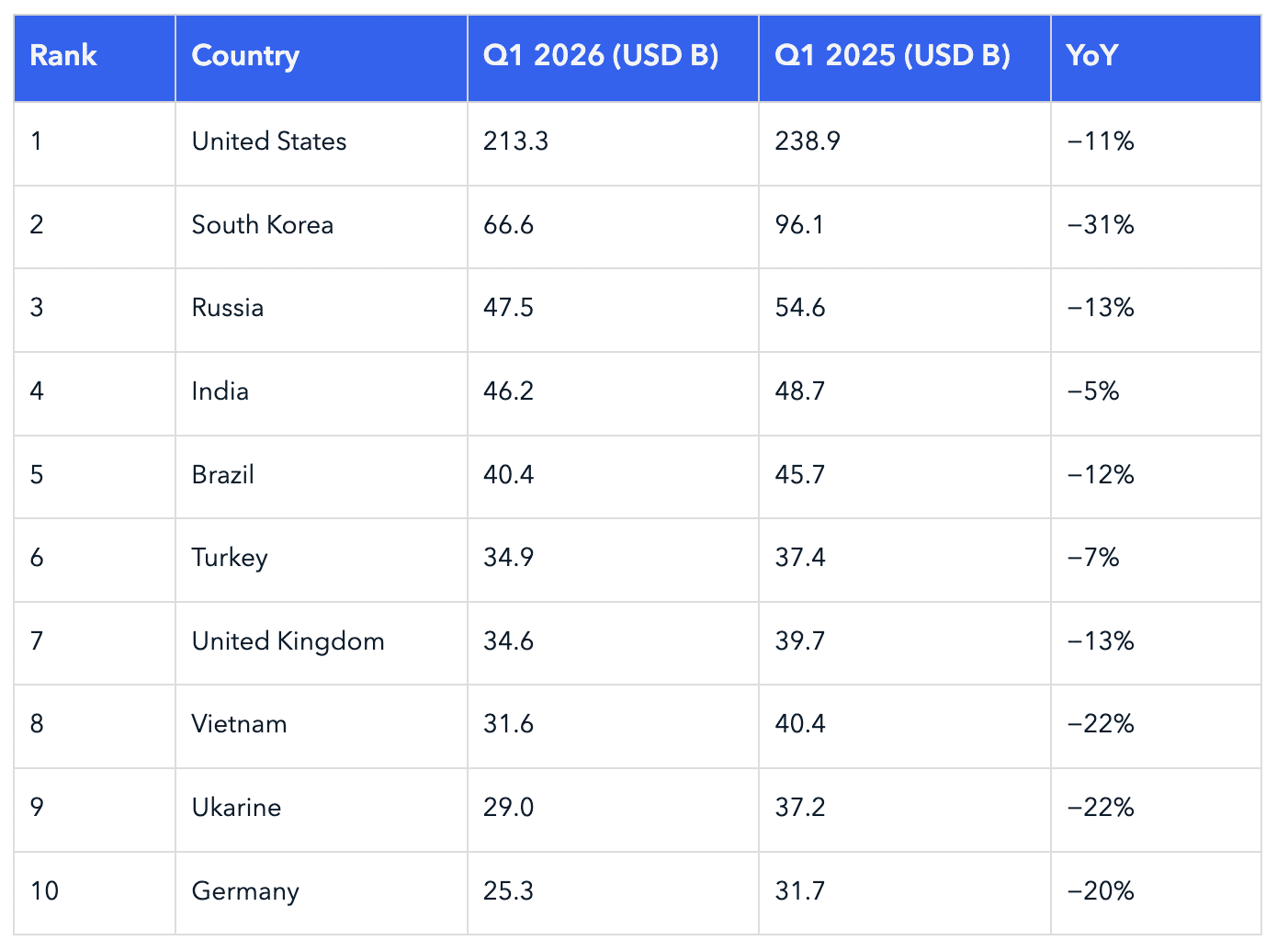

Yet despite this, Germany remains one of the top ten countries in terms of retail volume in Q1 2026. The year-over-year comparison shows a 20% decline from Q1 2025, when it was $31.7 billion, to Q1 2026, when it was $25.3 billion.

Final Summary

- Germany’s two biggest banking networks are integrating cryptocurrency trading directly into their banking apps.

- Roughly 25% of Germans who currently own cryptocurrency trust their main banks more than independent cryptocurrency platforms.