The core driver of the market last week was the sharp escalation of the US-Iran conflict. As the Strait of Hormuz faced a substantial threat, WTI crude oil prices surged nearly 17% during the week, reclaiming the $100 mark. This simultaneously triggered strong inflation expectations, leading to rising US Treasury yields and dealing a heavy blow to high-valuation tech stocks. The US Dollar Index broke through the 100 mark, suppressing gold's gains. Cryptocurrencies, as high-risk assets, experienced significant selling pressure, with weekly declines exceeding 6%. As the US-Iran conflict entered its fifth week with no signs of resolution, the sell-off continued. Last week's volatility and uncertainty indicators reflected the current macroeconomic tone. The VIX index closed at 31.05, its highest level since the outbreak of the war; while CNN's Fear & Greed Index fell to the "Extreme Fear" level, its lowest since last November. The bond market further adjusted its pricing, with the 10-year US Treasury yield rising to 4.44% and the 30-year US Treasury yield briefly breaking through 5% before retreating to just below that level. This movement reflects the market's entrenched expectation of "higher for longer" interest rates. The market widely believes the possibility of a Fed rate cut before autumn is minimal, while the chance of a 25 basis point rate hike this year is about 25%.

2. Liquidity Analysis

2.1 Crypto ETF Net Flows

Crypto ETF flows showed a clear pattern of "outflows first, recovery later" over the past week: sentiment weakened rapidly mid-week, with spot ETFs seeing a combined net outflow of approximately $500 million—BTC outflows were about $296 million and ETH outflows about $207 million. The selling pressure was mainly concentrated on March 26-27, indicating a clear phase of institutional de-risking. Marginal inflows appeared over the weekend, ending the multi-day outflow trend. Overall, institutional funds remain cautiously allocated amid macroeconomic uncertainty.

2.2 TradFi Liquidity

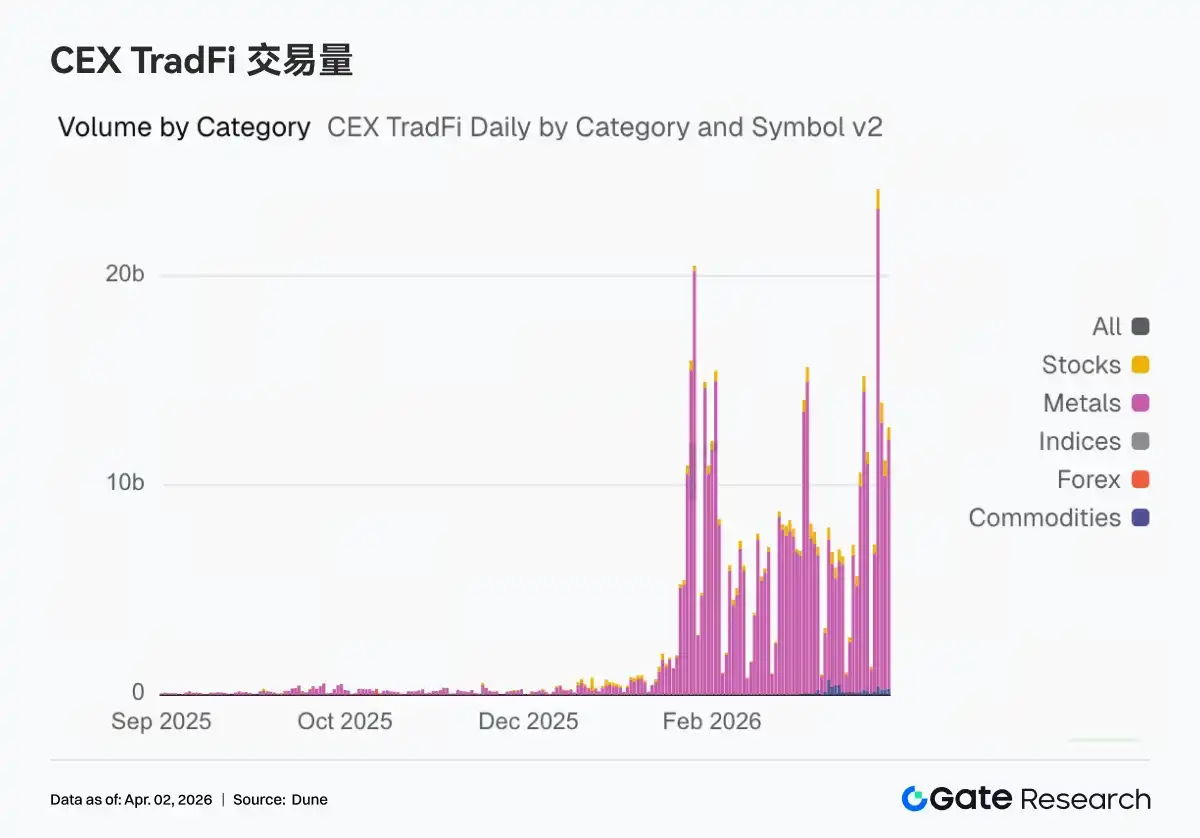

Over the past week, on-chain trading remained centered around macro asset volatility. Perp DEX TradFi trading volume rose to $17 billion; crude oil trading still had the highest weight but declined sequentially, while gold's share increased again. TradFi perpetual trading volume on CEXs surged, with volume on March 23rd hitting a record high. All sub-categories saw significant growth, with commodities and metals showing the highest sequential increases.

PAXG's market depth changes over the past week exhibited a structural feature of "weak first then strong, with tail-end volume expansion." Early in the week, Delta was mostly negative, coupled with price declines from highs, indicating net selling dominated and liquidity tended to withdraw; subsequently, around March 23rd, a round of concentrated selling pressure emerged, corresponding to a rapid price drop and creating a temporary liquidity vacuum. Depth structure improved significantly over the weekend, with Delta turning consistently positive and the scale significantly expanding, indicating funds began to actively absorb selling and push prices higher.

The number of TradFi asset categories expanded further last week. The total number of TradFi asset categories (counting only TradFi and CFD sections, excluding perpetual contracts) on three major CEXs increased from 598 to 619, a sequential growth of 3.5%. Metals saw the most significant growth, increasing from 22 to 31 items, up 40% sequentially; overall, only Gate saw an increase in the number of TradFi asset categories last week.

3. On-Chain Data Insights

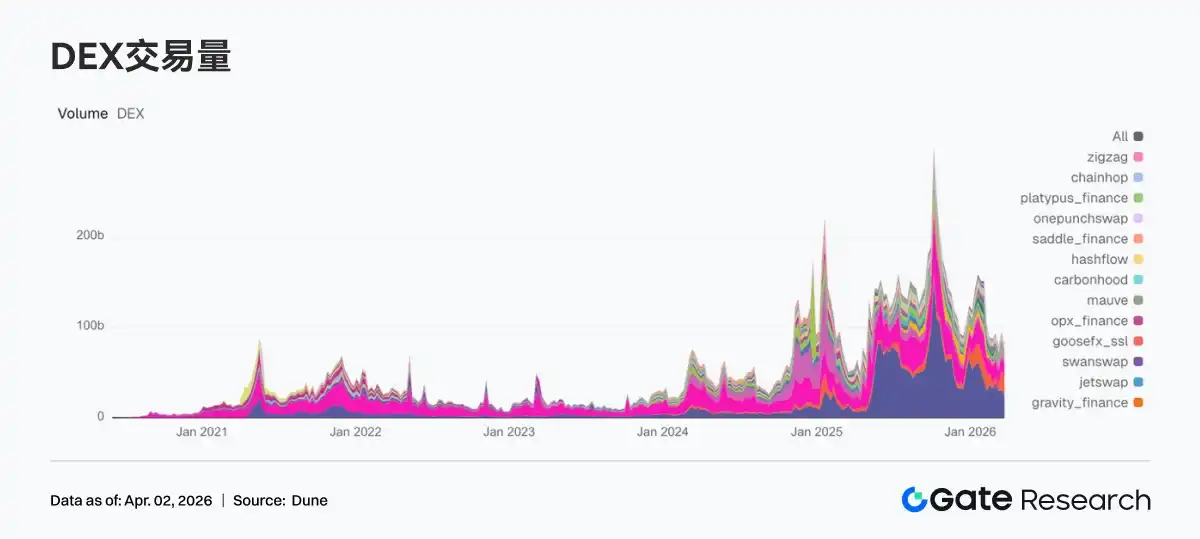

3.1 DEX Trading Cools Down, Meteora Remains High

Trading heat shifted from last week's surge to a cooling phase, with top protocols generally pulling back. Weekly trading volume on both PancakeSwap and Uniswap declined compared to the previous week, indicating a overall convergence of spot trading demand on mainstream chains. The Solana side showed divergence; Meteora remained at a high level slightly above $20 billion in trading volume, but marginal growth has slowed; Raydium's weekly trading volume fell 50% sequentially, the largest drop among top DEXs. Aerodrome, Humidifi, and Bisonfi also saw varying degrees of decline. Looking at the protocol side, PancakeSwap's Infinity architecture and Meteora's DLMM remain the strongest efficiency labels, but the market this week placed more emphasis on确定性 liquidity.

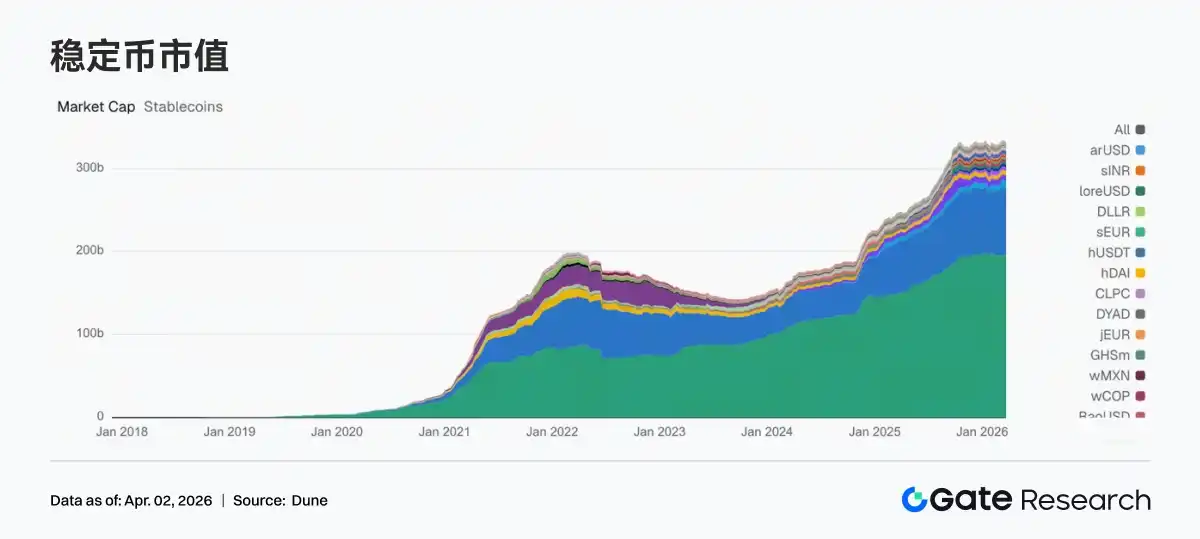

3.2 Stablecoin Supply Consolidates at Highs, DAI Shows Resilience

No new external inflows were seen in the stablecoin sector this week, with overall levels consolidating at highs. USDT remained almost flat compared to the previous week. USDC decreased by about $1.4 billion, and PYUSD also fell by nearly $200 million, indicating demand for payment and settlement-oriented stablecoins slightly declined this week. Protocol-type stablecoins were relatively more stable, with DAI seeing slight growth and USDS maintaining high levels. USD1, USDe, and GHO had minor fluctuations,偏向 structural reallocation. Circle continues to advance the multi-chain expansion of USDC + CCTP, but this week's data reflects a tilt within stablecoins from payment/settlement towards resilience in DeFi scenarios.

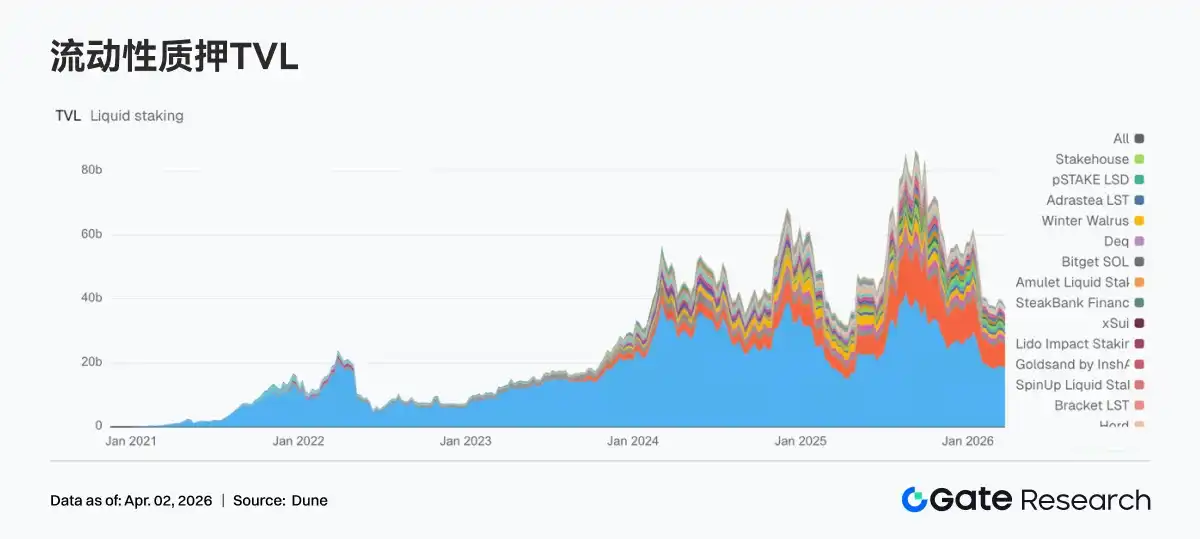

3.3 LST Protocols Pull Back, ETH and SOL Both Decelerate

This week, the liquid staking sector saw both ETH and SOL narratives decelerate. Affected by ETH's poor performance, ETH LST funds began阶段性 reducing positions, with TVL declining for both Lido and Rocket Pool. Lido's V3 and EarnETH / EarnUSD vault expansions have broadened the product boundaries, but short-term TVL is more influenced by market risk appetite and staked asset price volatility. The SOL direction also faced pressure, with Jito and Sanctum Validator LSTs, among others, experiencing pullbacks. Overall, the week saw a downturn in the sector's overall risk appetite.

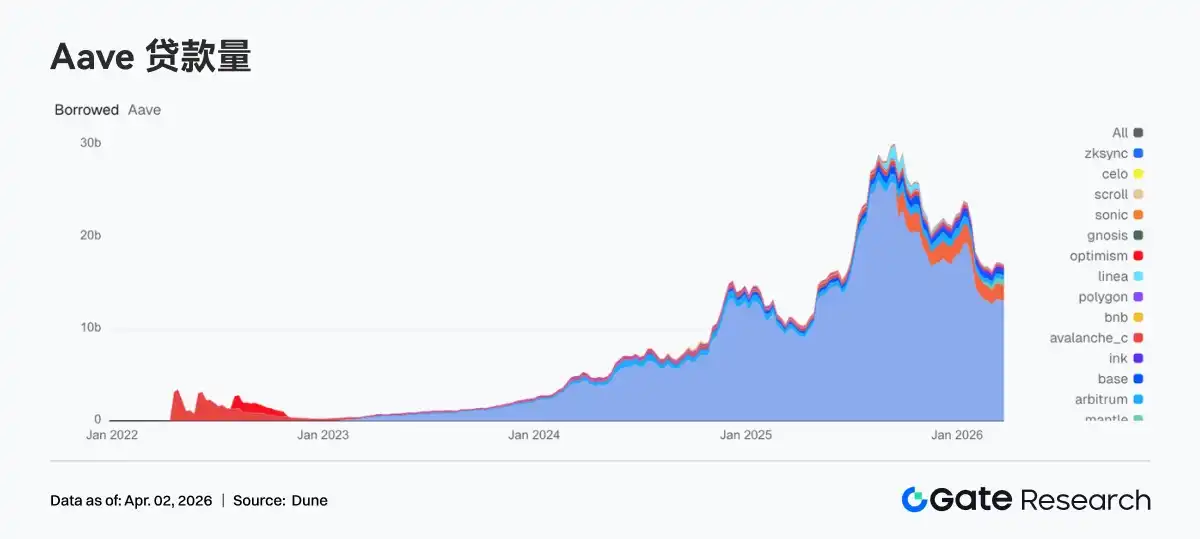

3.4 Aave Loan Volume Pulls Back, Mantle Becomes a Market Absorbing Limited Increment

Aave's total loan balance slightly decreased compared to the previous week. Both the Ethereum main market and Plasma saw declines of about $100 million, indicating deleveraging in mainstream markets. Multi-chain expansion also temporarily slowed this week, with Base and Arbitrum同步 pulling back. Mantle was one of the few markets that grew against the trend, with loan规模 increasing from $555 million to $574 million, becoming the structural highlight of the week. Ink also rose slightly from $289 million to $292 million, but the increase was limited. Aave is recently advancing its V4 Hub-and-Spoke model, and the market is pricing in future cross-market liquidity efficiency, but current funds are prioritizing reducing overall leverage and allocating limited increments to sub-markets with new narratives.

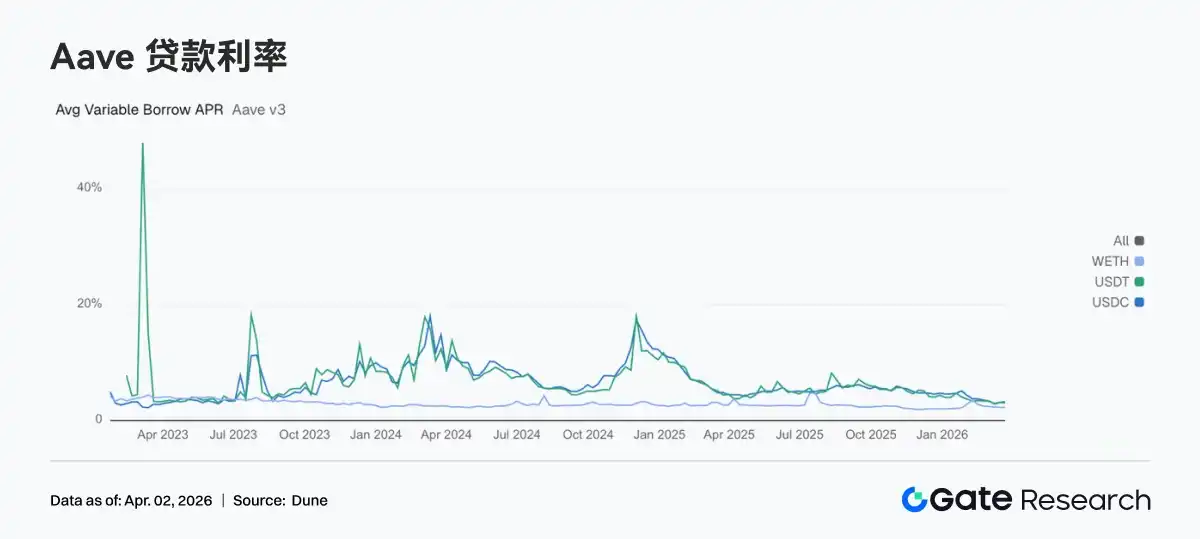

3.5 Divergence in Aave's Three Core Asset Lending Rates Continues

The average floating borrowing APR for USDC rose from 3.10% to 3.23%; demand for USD stablecoins did not weaken同步 with the decline in total loan balance this week. In contrast, USDT fell from 3.10% to 3.02%, and WETH also slightly decreased from 2.25% to 2.23%. While compressing broad risk exposure on-chain this week, lending demand became more concentrated on USDC. From a strategic perspective, this typically corresponds to institutions preferring USDC for liquidity scheduling, collateral management, and neutral strategy turnover. Combined with Aave's latest governance progress, the risk isolation and liquidity routing framework of V4 is gradually becoming clearer. Divergence in interest rates between different assets is likely to become more frequent in the future, better reflecting true capital preferences.

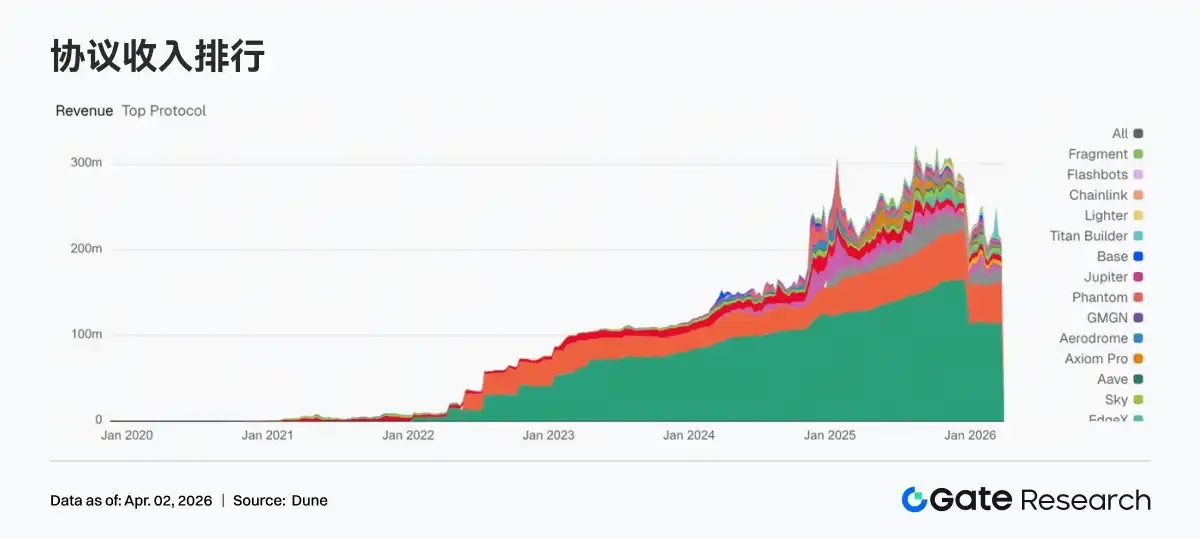

3.6 Protocol Revenue Shifts from Transaction-Driven Back to Stock-Driven

Revenue from trading protocols generally cooled down, while stablecoin issuers remained the most stable profit centers. Weekly revenue for Tether and Circle remained stable at high levels. In contrast, Hyperliquid declined from $14.3025 million to $12.6277 million, Pump fell from $7.1452 million to $6.6905 million, and EdgeX also dropped from $4.5534 million to $3.7969 million; the cooling trading activity has already transmitted to the revenue side. Overall, the main theme of protocol revenue this week was whose revenue is less dependent on short-term trading volatility.

4. Derivatives Tracking

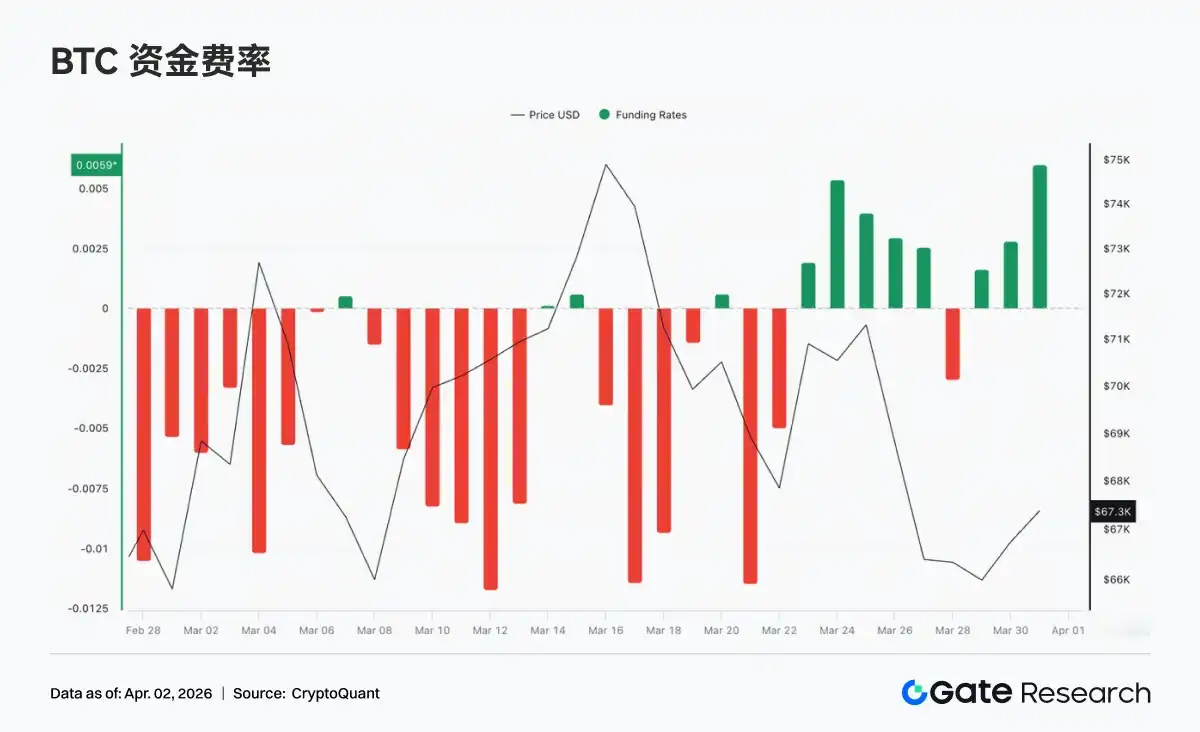

4.1 Funding Rates Shift to Short-Term Bullish, Sentiment Switches to Tentative Longing

BTC funding rates overall showed a structure of shifting from repair to briefly turning positive before fluctuating again. The previously long-standing deep negative, short-dominated pattern has明显 eased. Funding rates turned positive mid-week and remained for several days (peaking near +0.005), indicating the market switched to active long试探, with short-term risk appetite repairing and resonating with the阶段性 price rebound. However, this positive funding rate phase was short-lived and limited in intensity, failing to form a trend-positive premium structure.

4.2 Open Interest Rises Then Falls, Consolidates; Leveraged Funds Turn Watchful

Over the past week, BTC open interest first expanded to a阶段性 high alongside rising prices, but then quickly decreased to around $21B following the price pullback, indicating significant deleveraging in the market. Subsequently, open interest failed to return to previous highs, instead oscillating and repairing within the $21B–$22.5B range, with the overall center of gravity lower. New capital inflow momentum was insufficient, and leverage shifted from expansion to contraction. Overall, the current open interest structure is dominated by存量博弈 (stock game playing), lacking sustained volume配合, and the market remains in a震荡重建阶段 (oscillating rebuilding phase) after deleveraging.

4.3 Option Open Interest Concentrated in Medium-to-Long Term & High Strike Prices, Bullish Structure Prevails

BTC option open interest is mainly concentrated in medium-to-long term contracts like April and June, indicating the market is focused on medium-term positioning; structurally, Calls are significantly higher than Puts, overall still偏向 bullish. Looking at strike prices, Calls are主要集中在 the $80,000–$120,000 range, while Puts are distributed in the $60,000–$80,000 range, forming a typical structure of upside call speculation and downside hedging. It is worth noting that Put open interest in the $60K–$70K range is not low,表明 the market maintains medium-term bullish expectations while also strengthening short-term defensive sentiment.

4.4 Skew in Negative Territory, Short-Term Defensive Sentiment Still Dominates

Over the past week, the BTC 25D Skew overall remained in negative territory (approx. -6 to -10), with Puts still carrying a premium relative to Calls, indicating the market's assessment of downside risk remains relatively high. Shorter cycles (7D, 30D) were more volatile, falling rapidly before briefly repairing, reflecting反复 switching short-term sentiment; medium-to-long term (60D and above) was relatively stable, overall maintaining in the -5 to -7 range, showing little change in medium-term risk expectations. Overall, the Skew did not show a sustained recovery to near neutral or positive values, meaning that although there were repair attempts, defensive positioning still dominates.

4.5 Implied Volatility Stabilizes, Market Expects Limited Short-Term Volatility

Over the past week, the BTC DVol index overall oscillated within the 52%–55% range, first slightly declining then rising again, without a trend increase. The market's pricing of future volatility remains relatively restrained overall. During this period, prices experienced significant declines, but implied volatility only rose温和, without panic amplification, indicating the market did not view the current adjustment as a high-risk event. Overall, IV showed some desensitization from price, reflecting traders' inclination towards range-bound volatility expectations rather than unilateral trend行情 (market moves).

5. Week Ahead Outlook

6. Gate Institutional Dynamics

Refined Operations

1. Advancing data-driven and refined management,精准定位 customer needs, enriching customized solutions.

2. Significant results in dormant user activation.

Capital Business

1. Collateralized lending scale continues to grow, approaching bull market levels.

2. BTC interest rates下调, driving new demand growth.

Product & Technology

1. Websocket contract BBO real-time push achieved full availability in April.

2. AI gradually implemented, institutional services entering the AI-assisted operation phase.

Events & Marketing

1. CrossEx Advanced Trading Incentive Program launched, offering up to -0.01% contract rebate maker fees starting April 9th.

2. April Hong Kong Web3 Festival Side Event即将开启 (coming soon).

Data Sources:

• Investing, https://investing.com/currencies/xau-usd-historical-data

• Gate, https://www.gate.com/trade/BTC_USDT

• CMC, https://coinmarketcap.com/real-world-assets/?type=all-tokens

• Coinglass, https://www.coinglass.com/pro/depth-delta

• Dune, https://dune.com/gateresearch/gate-institutional-weekly-report

• CryptoQuant, https://cryptoquant.com/asset/btc/chart/derivatives

• Amberdata, https://pro.amberdata.io/options/deribit/btc/current/

Gate Research Institute is a comprehensive blockchain and cryptocurrency research platform, providing readers with in-depth content including technical analysis, hot topic insights, market reviews, industry research, trend predictions, and macroeconomic policy analysis.

Disclaimer

Cryptocurrency market investment involves high risks. It is recommended that users conduct independent research and fully understand the nature of the assets and products they purchase before making any investment decisions. Gate is not responsible for any losses or damages resulting from such investment decisions.