Author: Max.S

Original Title: The "Performance Pains" of Traditional Giants: Warnings from Coinbase and Robinhood's Q4 Earnings Reports

When Wall Street analysts digested Robinhood and Coinbase's Q4 earnings reports during the morning meeting on February 13th, a harsh reality emerged: despite both giants desperately trying to escape the gravitational pull of Bitcoin's price cycle through "diversification," in the eyes of the market, they are still Bitcoin's High Beta derivatives.

On one side, Robinhood delivered its strongest revenue performance in history, yet its stock price was halved; on the other, Coinbase turned from profit to loss, posting a massive quarterly loss of $667 million. These two earnings reports are not just health check-ups for the two companies; they are the tombstone for retail sentiment across the entire crypto market.

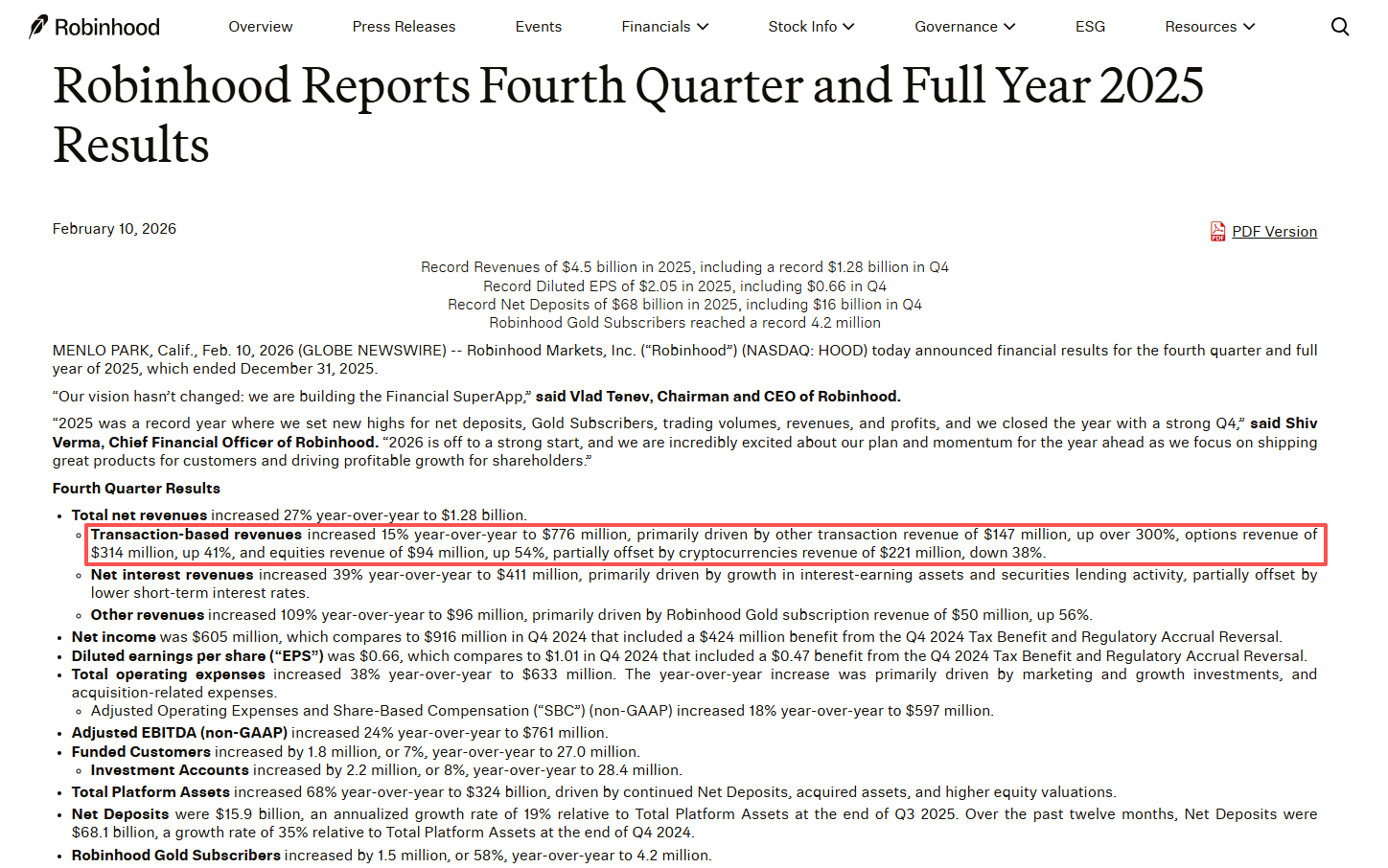

Robinhood: A Luxurious Casino Without Gamblers. Its earnings report is filled with magical realism. If you only read the first half, this is a fintech giant at its peak: full-year 2025 revenue hit a record high of $4.5 billion, net profit was $1.9 billion, and Gold membership surged 58% to 4.2 million. CEO Vlad Tenev confidently declared in the earnings call: "We are building a financial super app."

But the market is only focused on the second half: retail investors have stopped playing.

The most glaring data in the report is the collapse of cryptocurrency trading revenue. In Q4, this revenue was only $221 million, a staggering 38% drop year-over-year. Correspondingly, the nominal cryptocurrency trading volume within the Robinhood app in January 2026 plummeted 57% year-over-year to just $8.7 billion.

Currently, Robinhood's traditional finance (TradFi) business is advancing triumphantly: stock trading revenue rose 54%, options rose 41%, and even prediction markets have become a new growth pole, with the number of contracts traded in the first year exceeding 12 billion. But their crypto business is cooling rapidly: As Bitcoin retreated from last year's high of $126,000 to around $65,000, FOMO turned into fear itself. Retail investors not only stopped trading but even began to exit.

For Wall Street, Robinhood is like a newly renovated, luxuriously equipped casino. The slot machines (options) and poker tables (prediction markets) have the latest upgrades, but the most profitable VIP room (cryptocurrency) is empty.

The market voted brutally with its feet: Despite Robinhood desperately trying to prove it's more than just a "crypto broker," investors still see it as a shadow stock of Bitcoin amid the crypto winter. The stock price has fallen 50% from its peak last October. This valuation drop is not aimed at its performance but at its "crypto content."

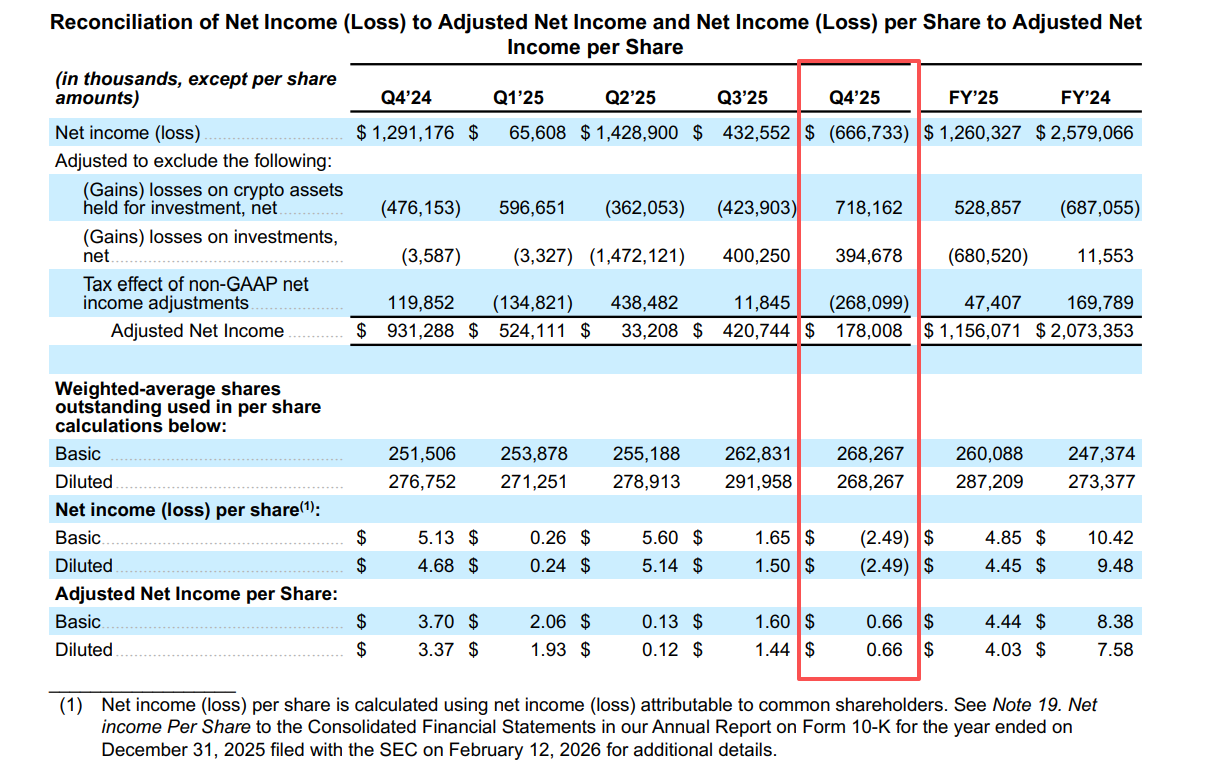

Coinbase: The Naked Swimmer's Winter. If Robinhood could still "hedge" the winter with its stock and options business, Coinbase was completely exposed to the blizzard. Q4 earnings showed Coinbase's revenue fell 21.6% year-over-year to $1.78 billion. More shocking to the market was its net profit turning from positive to a massive loss of $667 million. This huge loss was mainly due to investment losses in its crypto asset portfolio—a classic case of "bull market asset, bear market liability."

(Image Source: Coinbase 2025 Q4 Shareholder Letter)

Coinbase's data reveals a deeper industry crisis than Robinhood's:

-

Retail Investors Have Completely Given Up: Consumer transaction volume was only $59 billion, compared to institutional transaction volume of $237 billion. Retail investors are almost "missing" from Coinbase's ecosystem.

-

A One-Man Show for Institutions and Derivatives: The only bright spot came from institutional business and derivatives (thanks to the integration after acquiring Deribit), but this low-fee flow cannot compensate for the loss of high-fee retail trading.

-

USDC Dependency: Stablecoin revenue reached $364 million, becoming the "steadfast anchor" supporting revenue. With trading volumes drying up, Coinbase is increasingly resembling a bank living off US dollar interest rather than an exchange.

Coinbase's current situation is eerily similar to 2022. Brian Armstrong's vision of an "Everything Exchange" seems pale and powerless in the face of a downward Bitcoin price cycle. When the underlying asset (Crypto) price plummets, the exchange, the "shovel seller," not only can't sell shovels but also sees the shovels in its inventory depreciate significantly.

Putting the two companies' earnings reports together, we can clearly see the underlying logic of the 2026 crypto market: Whether it's Web2's Robinhood or Web3's Coinbase, neither has escaped Bitcoin's Beta. Over the past year, both companies have been trying to build their own Alpha opportunities.

-

Robinhood bet on "de-crypto-fication," trying to dilute the volatility of its crypto business through breadth, by acquiring Bitstamp and even entering the Indonesian brokerage market.

-

Coinbase bet on "deepening," focusing deeply on Layer 2 (Base chain), derivatives, and payment infrastructure, trying to retain institutional funds.

However, the data mercilessly shows that as long as Bitcoin falls, retail investors leave, and trading frequency drops to zero. Robinhood's monthly active users (MAU) decreased by 1.9 million. This is not just a numerical reduction; it's a loss of faith.

MicroStrategy's (MSTR) Q4 earnings report also corroborates this—a single-quarter paper loss of $12.4 billion due to Bitcoin impairment. Whether it's MSTR directly holding Bitcoin or HOOD and COIN providing trading services, the overlap between their stock price charts and Bitcoin's K-line chart remains over 90%. This is a "false diversity." No matter how many business lines you have (Robinhood claims 11 businesses with annual revenue over $100 million), as long as the core narrative—Crypto Adoption—falters, the market's valuation system quickly collapses.

For financial practitioners, these two earnings reports send three clear signals:

-

Excess Infrastructure & Scarce Users: The 2024-2025 bull market催生ed a lot of infrastructure construction (Layer 2, wallets, payments), but Q4 earnings show that real active users (especially high-net-worth retail) are contracting sharply. 2026 will be a year of "supply-side reform"; only the leading platforms will survive the winter.

-

The "Stablecoin Content" of Revenue Structure is Crucial: Coinbase's USDC revenue and Robinhood's Net Interest Income are their oxygen masks for survival. Before the next bull market arrives, whoever's cash flow is more like a bank's will be safer.

-

Valuation Logic Restructuring: The market is punishing those "Betas disguised as tech companies." Unless Robinhood's prediction markets can prove to be an independent growth flywheel, or Coinbase's Base chain can generate large-scale non-transaction revenue, their stock prices will continue to fluctuate with Bitcoin until the market is convinced the bottom has arrived.

Robinhood's Tenev said at the end of the call: "We are building a financial ecosystem for the next generation." But right now, the next generation of investors is staring at screens full of red K-lines and closing the app.

For Coinbase and Robinhood, the "record-breaking" year of 2025 is history. The theme for 2026 is no longer "growth" but "resilience." As Warren Buffett said, "Only when the tide goes out do you discover who's been swimming naked." Now the tide is out. Although these two giants are wearing swim trunks, the wind is bitterly cold. They must prove to the market that they have enough cash flow to survive until the next summer.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush