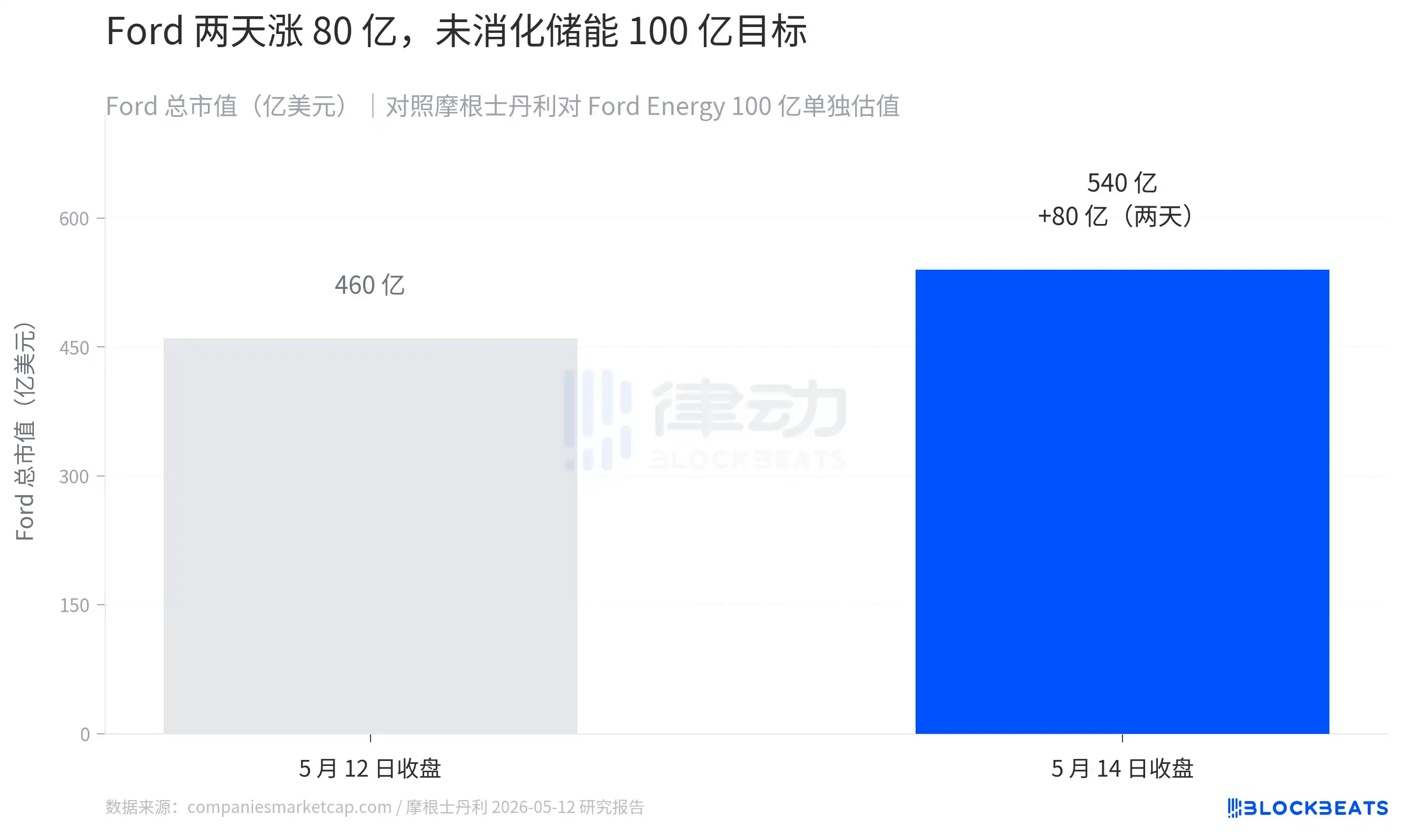

On May 11th, Ford established its wholly-owned subsidiary Ford Energy, investing $2 billion to transform its Glendale factory in Kentucky, targeting an annual production capacity of 20 GWh for energy storage systems. The next day, Morgan Stanley analyst Andrew Percoco valued this standalone business unit at $10 billion. The market reaction was immediate: Ford's stock price rose from $11.99 to $14.48 over two trading days, adding approximately $8 billion to its market cap.

The story up to this point resembles the standard script of another "traditional automaker being repriced by AI." But a look at the supply-side ledger reveals another name: the state of Louisiana.

What is the market revaluing?

Morgan Stanley's $10 billion valuation for Ford Energy was not pulled out of thin air. Percoco's report assumed Ford Energy would achieve a 25% gross margin and $346 million in EBIT by 2028, then applied the price-to-sales multiples of leading energy storage companies to work backwards. Compared to the profit structure of Ford's existing business, this is an entirely different species.

Ford's 2024 financial report shows that its Ford Blue internal combustion engine division generated annual revenue of $145.4 billion with an EBIT of only $5.28 billion, a margin of 3.6%. Industry estimates place the per-vehicle gross margin for selling an F-150 in the 10-13% range. The energy storage industry, meanwhile, operates on a completely different scale. According to various company reports, Tesla's Megapack business boasts a 26.2% gross margin, Sungrow Power's energy storage business exceeded 28% in the first half of 2024, and pure-play system integrator Fluence sits between 12-14%. Morgan Stanley is betting that Ford's cost structure—building its own LFP battery cells and retrofitting existing EV factories—can place it within the leading range, with a per-GWh gross margin at least double that of selling an F-150.

This is the reason the market is willing to pay a premium. But the market has only priced in $8 billion so far. Morgan Stanley's $10 billion target implies an additional $2 billion not yet digested. The revaluation is in its early stages.

To absorb that remaining $2 billion, Ford Energy needs to deliver on capacity, contracts, and pricing. Production capacity is expected only in the second half of 2027, while contracts depend on downstream buyers—those regions scrambling most aggressively for electricity.

The Four Corridors

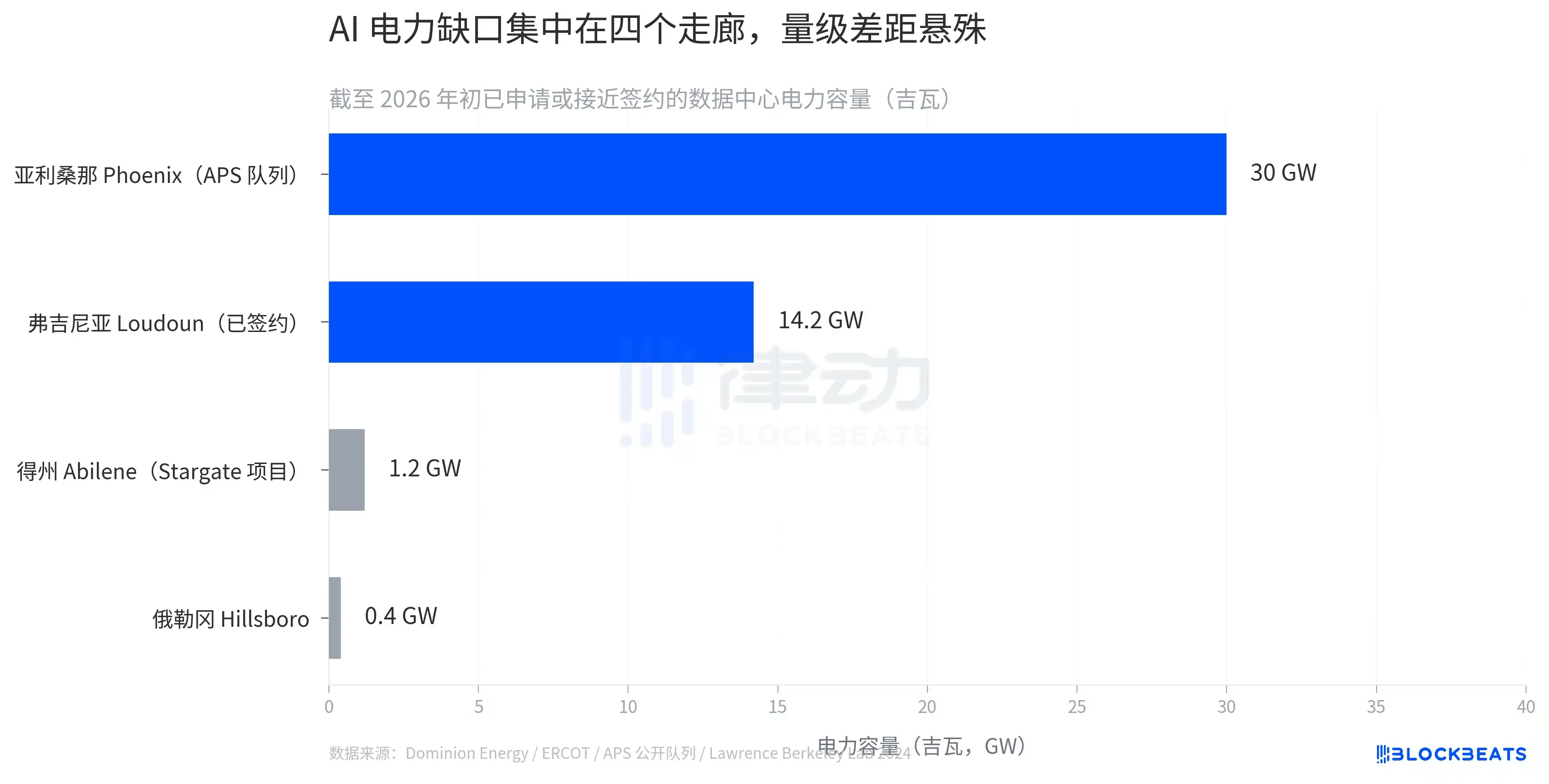

In the same research report, Morgan Stanley provided another figure. U.S. data center installed power capacity was 40 GW in 2024 and is projected to reach 79 GW by 2027. By 2028, a gap of approximately 49 GW is expected between demand and supply, representing a 20% shortfall. This gap will not be evenly distributed across 50 states.

Based on currently public data center power applications, the gap is concentrated in four corridors. The APS service area in Phoenix, Arizona, has a backlog of 30 GW in its queue. Loudoun County, Virginia, has capacity either signed or nearing signature of 14.2 GW. In Abilene, Texas, the OpenAI-led Stargate project alone requires 1.2 GW. Hillsboro, Oregon, has another 0.4 GW. The figures differ in scope: Phoenix's 30 GW includes projects in utility queues yet to be finalized, while Loudoun's 14.2 GW represents actual capacity close to being contracted.

This is the demand-side foundation for Ford Energy's $10 billion valuation. When a region's grid capacity growth can't keep pace with data centers' electricity grab, space for energy storage arbitrage is created. On one side are training loads during peak hours that are almost impossible to cut, and on the other is a supply curve the grid cannot instantly respond to. In the middle lies the deterministic cash flow for energy storage providers.

But grabbing electricity comes at a cost. The question is, who pays?

The Bill Lands in Louisiana

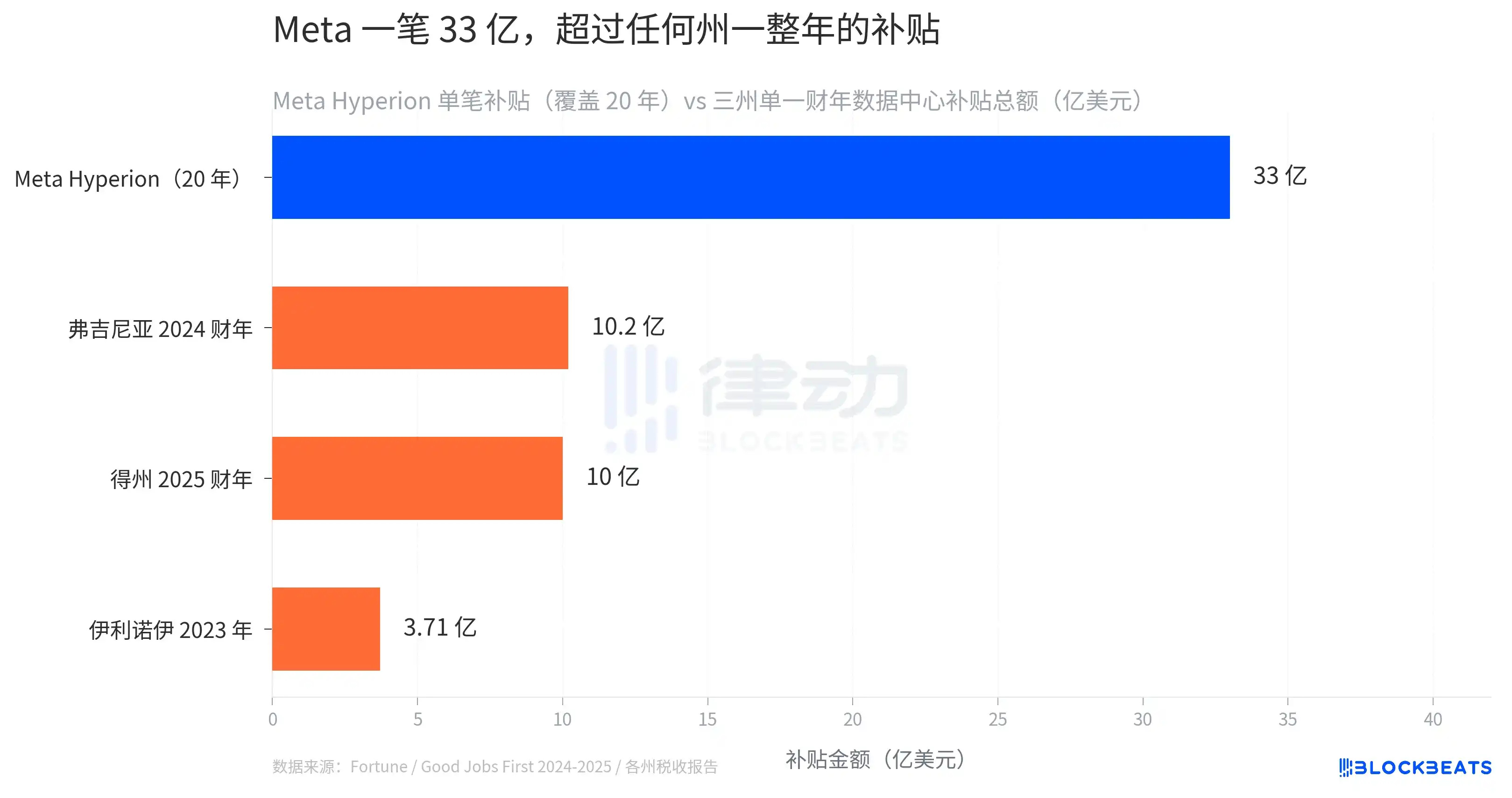

On May 14th, Fortune's front page reported on Meta's Hyperion project in Richland Parish, Louisiana. This flagship data center, Meta's bet on "AI advantage," costs $10 billion. In July 2024, the Richland Parish Commission approved sales and use tax exemptions totaling $3.3 billion, covering 20 years.

This abatement exceeds the combined police budgets of the state of Louisiana for seven years.

Meta also secured a 60% local property tax exemption through a PILOT agreement, conditional on hiring 300 local permanent positions. This project's predicted power consumption could account for 20% of Louisiana's total electricity usage.

A more crucial comparison lies across state lines. Texas's total data center sales tax exemption losses for the 2025 fiscal year amounted to about $1 billion, making it the state's costliest industry subsidy. Virginia's was $1.02 billion in FY2024, and Illinois's was $371 million in 2023. The $3.3 billion subsidy for Meta's single project exceeds any single state's total annual data center subsidies.

This is not an isolated case. According to Good Jobs First, at least 36 states have authorized data center sales tax exemptions through specific legislation, with only 11 publicly disclosing beneficiary company names. Official calculations in some states are more direct: for every dollar given in data center tax breaks, state coffers incur a net loss of 52 to 70 cents. The $8 billion increase in Ford's valuation is built on the implicit assumption that "this subsidy arms race will continue."

The continuation of this subsidy arms race depends on state legislators' ability to explain why an abatement exceeding seven years of police budgets is justified. This is becoming increasingly difficult.

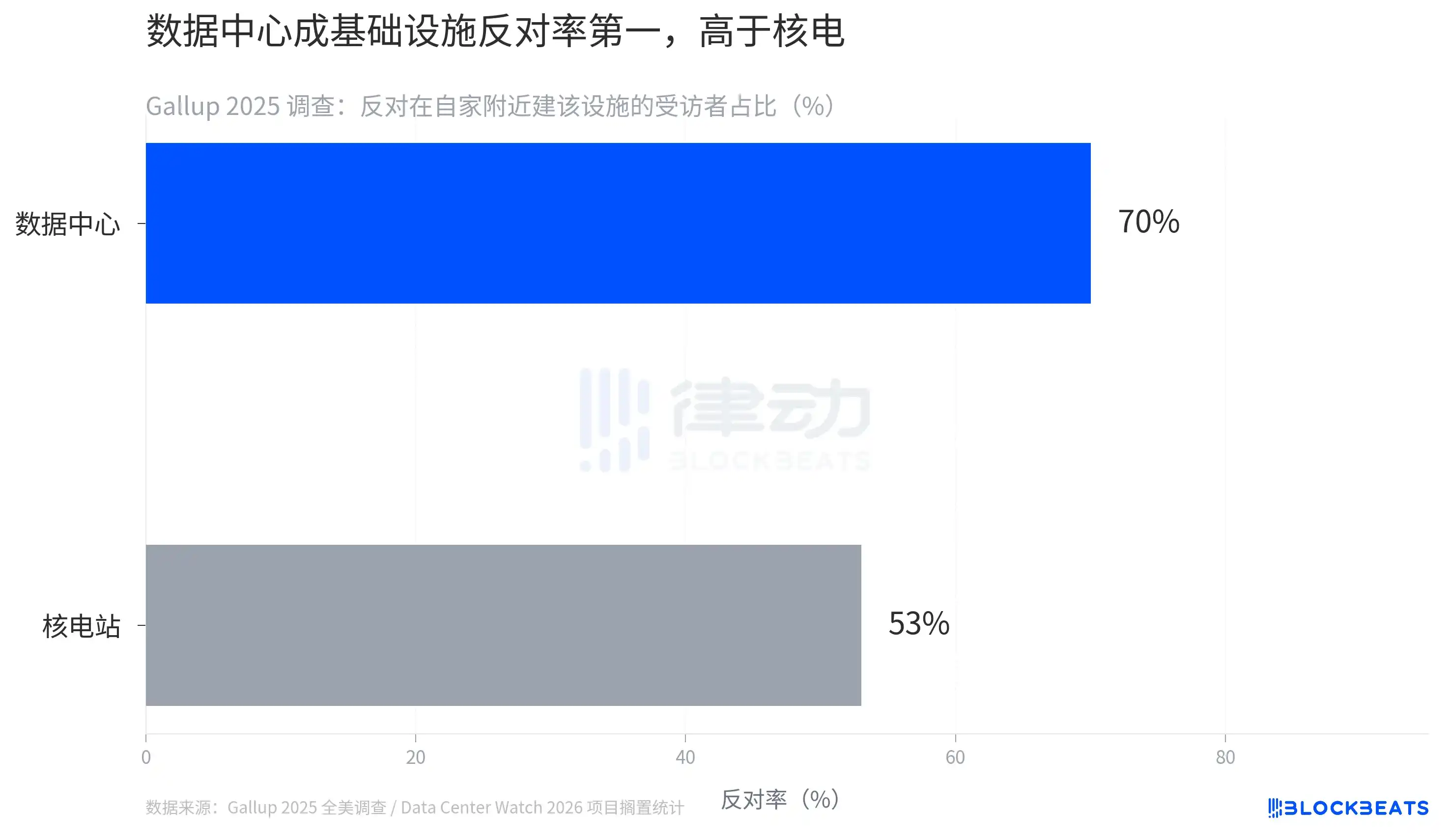

Data Center Opposition Rates Now Exceed Nuclear Power Plants

A 2025 Gallup national survey shows 70% of respondents oppose building a data center near their homes. The opposition rate for nuclear power plants in the same survey is 53%. Data centers are now the most opposed-to infrastructure in the United States.

This is not an abstract number. Data Center Watch's database as of early 2026 shows 69 jurisdictions have halted approvals or rejected data centers through local referendums or moratorium resolutions, stalling $64 billion in planned projects. In Loudoun County, Virginia, data center tax breaks caused a $267 million loss for the public school system in 2024, a fact now entering voters' consciousness.

The reasons data centers are disliked are more complex than those for nuclear plants. Nuclear plants are typically tens of kilometers from residential areas, while data centers hug urban edges. They consume water for cooling, increase grid load, generate low-frequency noise, yet provide local employment mostly in the hundreds, far lower than the job density of steel mills or auto plants. Hyperion's 326 operational jobs for $3.3 billion in abatement equates to a fiscal cost of $10 million per job. The room for explanation by local governments is narrowing.

The path to realizing Ford Energy's $10 billion valuation requires this grid to keep running, subsidies to hold, the electricity grab to proceed as usual, and opposition not to translate into legal mandates. If any link weakens, repricing will follow.

Ford's $8 billion gain, Meta's $3.3 billion subsidy, Phoenix's 30 GW queue, and the 70% opposition rate are readings from four cross-sections of the same grid. They remain disparate data points for now. Once one hard constraint emerges—whether physical power shortage, state fiscal breach, or public vote—the others will be repriced simultaneously.