Author: Lawyer Shao Shiwei

For family members of criminal cases, when a loved one is suddenly investigated for a virtual currency fraud case, they are often at a loss.

On one hand, the case itself involves professional content such as virtual currency, platform trading, and order guidance, making it difficult to understand immediately;

On the other hand, the feedback from the outside world is often very simple—"This is basically fraud."

However, when handling such cases in practice, it becomes clear that this is not a simple individual act but often a chain with clear organization and division of labor:

There is a platform operator responsible for overall setup and fund operations;

There are technical personnel responsible for system development and maintenance;

There are business personnel responsible for external promotion and developing agents;

There are agent teams responsible for attracting and converting clients;

There are also lecturers and order-guiding teachers who provide guidance in live streams or community groups.

From the outside, these roles appear to operate around the same platform,

But for each individual, the specific part they participate in, the information they possess, and their understanding of the overall model are often completely different.

It is precisely because of this that in specific cases, not everyone is evaluated in the same way, and it is even more inappropriate to simply categorize everything as fraud.

However, for the individuals involved, they often only see the part of the work they are responsible for. They neither understand the overall structure nor can they judge how their actions will be legally evaluated, making it difficult to propose targeted defense strategies in the first place.

It is under such circumstances that many cases may appear to be already decided on the surface, but when it comes to individual cases, there are still varying degrees of room for negotiation—including possibilities for exoneration, lesser charges, or even no crime at all.

Based on Lawyer Shao’s experience in handling such cases, the following provides some judgment perspectives from several key dimensions for families encountering virtual currency fraud cases.

1. 5 Critical Questions That Determine the Direction of the Case

From case-handling experience, whether such cases are classified as fraud often depends on a comprehensive judgment of several core issues.

1. Were the Users Deceived by the Platform?

In judging such cases, we must first return to the starting point—was the investment behavior of the users (investors) caused by deception from the platform, agents, or other involved parties?

In practice, we typically assess the true cognitive state of investors from the following aspects:

Investment duration. If an investor has participated in trading for one or two years, or even longer, they usually have a considerable understanding of the platform’s operational model, fund flow, and risk characteristics. It is difficult to say that they were in a "deceived" state for such a long time.

Existence of profit records. If an investor has never made a profit or was unable to withdraw after making a profit, the characteristics of being deceived are more apparent. However, if the investor has made profits and successfully withdrawn them, it indicates that the platform is not "one-way only." Subsequent losses may be the result of continued participation in trading rather than being caused by platform fraud.

Ability to make independent decisions. In many cases, we see in investors’ statements: "Sometimes I don’t follow the order-guiding teacher’s advice; when they suggest buying long, I buy short." This shows that investors do not mechanically execute the teacher’s instructions but have the awareness and ability to make independent judgments and decisions.

If many people have been involved for one or two years, even made profits, but only claim to have been "deceived" after incurring losses, this is a key point that defense lawyers need to emphasize to case handlers in judicial practice.

For example, in a case handled by Lawyer Shao involving a digital collectibles platform accused of fraud, when communicating with the procuratorate, we emphasized one question: Did users participate in trading under misleading circumstances, or did they continue to invest after understanding the rules?围绕这一点, further introducing the analytical perspective of "investor cognitive state." It was at this level that the case handlers were prompted to re-examine the trading model of the case:

—Was the user deceived, or did the user voluntarily participate in trading knowing the risks?

Ultimately, the case was not classified as fraud (➡️Related reading: Successful Case of Innocence Defense for Fraud Crime | From Facing Over Ten Years in Prison to a Case Closed as Innocent!).

2. Were the Platform’s Data Real or Fake?

A critical question in such cases is: Were the platform’s data real or artificially created?

In some cases, technical personnel clearly state: The platform’s K-line trends are connected to real-time market data from an exchange, not generated by the platform itself.

If this can be proven, the profits and losses of investors are more due to market fluctuations rather than the platform "controlling wins and losses" in the background, leading to a significant difference in case evaluation. On the evidence level, we must examine: Can it be proven that the data is connected in real time? Does the functionality exist to modify data in the background? Even if such functionality exists, is there evidence proving it was actually used to manipulate trading results?

This is a crucial dividing line in定性.

Conversely, if it can be proven that the data is generated in the background or that profits and losses can be artificially interfered with, the nature of the case will fundamentally change.

3. How Were the Losses Actually Incurred?

Many family members wonder: Since users incurred losses and reported the case, does it mean the platform was indeed acting as a market maker, taking client losses, or even operating a "Pixiu plate" (a scheme where funds only enter but never leave)?

But in specific cases, we often further investigate: How were the losses actually incurred?

For example:

-

Was there high-frequency trading (frequent buying and selling)?

-

Was high leverage used (borrowing money to trade cryptocurrencies)?

-

Was there frequent entering and exiting, chasing rallies and selling off?

These factors themselves significantly amplify losses. Even without platform manipulation, long-term high-frequency operations have a much higher probability of loss than profit.

Even in the case files, we see victim statements: "I sometimes listened to the teacher, sometimes not, and even did the opposite"—then it is difficult to say that the losses were entirely "controlled" by one party.

This also shows: There may be multiple reasons for user losses, which cannot be simply equated with being defrauded by the platform.

4. What Was the Composition of the Involved Personnel’s Income?

How the involved personnel profited is also a very important question.

In practice, we often distinguish: Where did their income actually come from?

For example, for the platform operator, if their income mainly comes from transaction fees and spreads (the difference between the buying and selling price), this itself is a common profit model for trading platforms, and its nature is closer to providing trading services.

But if the platform’s main revenue comes from sharing client losses (i.e., "client loss") or even directly retaining client principal, then its profit model has changed, making evaluation more inclined towards fraud.

Another example is the role of "lecturers." If their income is limited to fixed lecture fees, course fees, or membership fees, it can generally still be understood as providing information or training services; but if their income is directly linked to client losses, such as receiving a commission based on the loss ratio, or even participating in the distribution of "client loss" after "reverse order calling," then the role of their behavior in the overall chain will be re-evaluated, and the corresponding legal risk increases significantly.

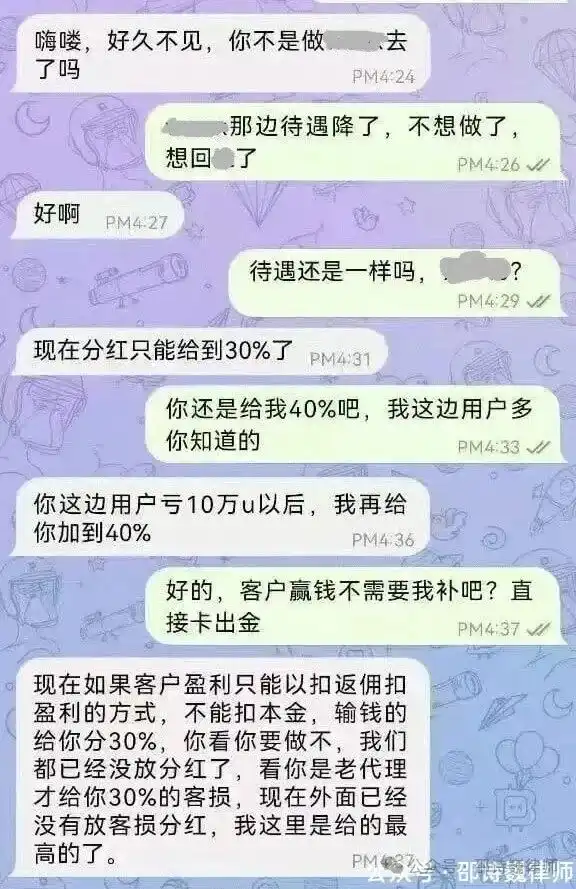

For example, as previously exposed online, a certain exchange openly provided "client loss sharing" to agents, where the mentioned 'dividend' referred to sharing client losses (the platform and agents split client losses 70-30). The more users lost, the higher the agent’s share.

(Image source: Internet)

5. Could Users Withdraw Their Money Normally?

This is an easily overlooked defense point: Could investors withdraw their money normally from the platform?

For example, in the aforementioned chat log, the agent asked: If the client wins money (the platform loses), should the agent bear the loss? The agent suggested the platform "directly block withdrawals," meaning restrict users from withdrawing.

However, in some cases:

-

Investors could freely deposit and withdraw funds

-

Some people even made money and successfully withdrew it

-

Even when the platform changed versions, funds could be transferred accordingly

In this situation, the platform did not substantially restrict fund outflows, and investors still had a certain degree of control over their funds. Because of this, when determining whether there is "intent to illegally possess," significant controversy arises. It is difficult to directly认定 the platform intended to possess user funds.

It is precisely based on this point that in practice, cases with superficially similar models can have significantly different outcomes.

2. How Do Courts Judge in Similar Cases?

In a virtual currency-related case I encountered, although the prosecution charged the platform and related personnel with fraud, the court ultimately did not认定 it.

From the judgment reasoning, the core focus was not on superficial situations like "order guiding" or "losses," but revolved around several key facts:

-

Existing evidence could not prove the platform data was fake

-

It could not be proven that the defendant could manipulate real-time trading results

-

The platform did not restrict withdrawals; users could deposit and withdraw freely, and some victims stated they had profited from trading on the platform

When these facts could not be proven, the key elements of "fabricating facts, concealing the truth" and "intent to illegally possess" in the crime of fraud could not be established.

Of course, each case is different, and specific conclusions cannot be simply applied.

But this type of adjudication思路 at least indicates that the定性 of virtual currency trading cases is not just about the superficial model but must return to the evidence itself.

For specific individual cases, as long as key facts remain uncertain, there is often still room for defense.

3. Conclusion

From a practical perspective, the定性 of such cases is often not a simple question of "guilty" or "not guilty," but depends on a comprehensive judgment of specific circumstances.

Differences between roles often directly affect the outcome of the evaluation. For example, platform operators, technical personnel, business personnel, agents, lecturers, sales staff, and even investors themselves may have significant variations in specific communication content, fund flow, participation methods, and understanding of the overall model.

If these individual differences are not communicated to the case handlers in time and fully explained, they are often lumped together as a whole, leading the case定性 towards a more unfavorable direction.

It is precisely because of this that if a family encounters a similar situation, the more important thing is not to repeatedly纠结 over "whether it is fraud," but to clarify the key facts item by item as early as possible—including what was specifically done, how they participated, how funds flowed, whether they understood the overall model, etc.

In many cases, if these issues are not clarified in the early stages, it often becomes very passive to try to adjust the direction later,甚至 missing out on more favorable handling opportunities.

Special Disclaimer: This article is an original work by Lawyer Shao Shiwei and represents only the personal views of the author. It does not constitute legal advice or opinion on specific matters.