Author: David, Deep Tide TechFlow

Do you still care about Ethereum?

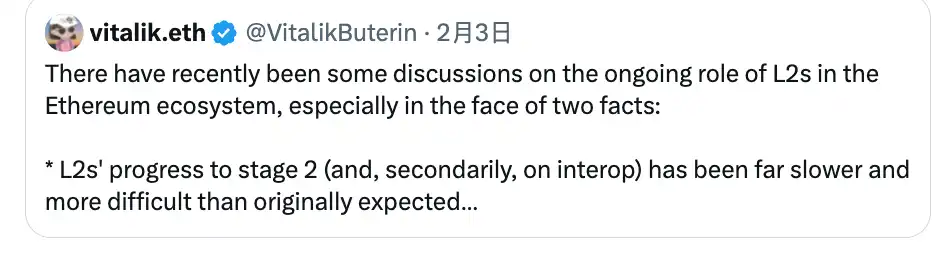

On February 3rd this year, Vitalik posted on X.

No long essay, just one sentence: The original vision of L2 and its role in Ethereum is no longer reasonable. We need a new path.

For the past five years, Ethereum's entire scaling roadmap has been built on L2. The mainnet is responsible for security and settlement, leaving all execution layer work to L2. Rollups, bridges, cross-chain messaging... The entire architecture was designed under the leadership of Vitalik himself.

Now the designer himself says this path is wrong.

Less than two months later, at the EthCC Cannes conference on March 29th, Gnosis co-founder Friederike Ernst and zero-knowledge proof developer Jordi Baylina took the stage to announce something called EEZ:

Full name Ethereum Economic Zone.

Co-funded by the Ethereum Foundation, with protocols like Aave joining as founding members. What EEZ aims to do can be summed up in one sentence: make all L2s no longer isolated islands, but one connected continent.

The direction is certainly correct.

But the problem is, this archipelago has been built for five years... The islands were once prosperous, but surely no one is there now. Is it too late to start building tunnels now?

Closing the Stable Door After the Horse Has Bolted?

From the name EEZ, you can actually see what Ethereum wants to do.

The logic of an economic zone is well understood: unified rules within the zone, free flow of capital, no checkpoints. In the past, Ethereum's twenty-plus L2s were like twenty small economies, each with its own customs, currency, and clearance procedures. Moving money from Arbitrum to Base required finding a middleman to exchange currency and bridge.

What EEZ aims to do is remove tariffs, unify the currency, and dismantle customs. Your operations on any chain can directly interact with contracts on another chain, settling back to the Ethereum mainnet, with Gas uniformly paid in ETH.

Does that sound familiar?

LayerZero and Wormhole told similar stories back in the day. Connect all chains, free flow of assets... all old tricks.

The difference here is that those cross-chain protocols are asynchronous. For example, you initiate an operation on chain A, and chain B executes it after a while; there's a delay in the middle, a risk of failure, and the bridge itself is a favorite target for hackers.

This EEZ is synchronous. Contracts on two chains execute simultaneously within one transaction, either both succeed or both roll back. The technical prerequisite for this is the real-time proving of Ethereum blocks.

This wasn't possible before. For two chains to operate synchronously, they need to be able to verify each other's ledgers in real-time. But Ethereum produces a new block every 12 seconds, and the speed of verifying the previous block couldn't keep up. The accounting wasn't finished before the next block arrived.

This year, this speed was technically achieved. Synchronous operation became an engineering reality for the first time, leading to the EZZ proposal.

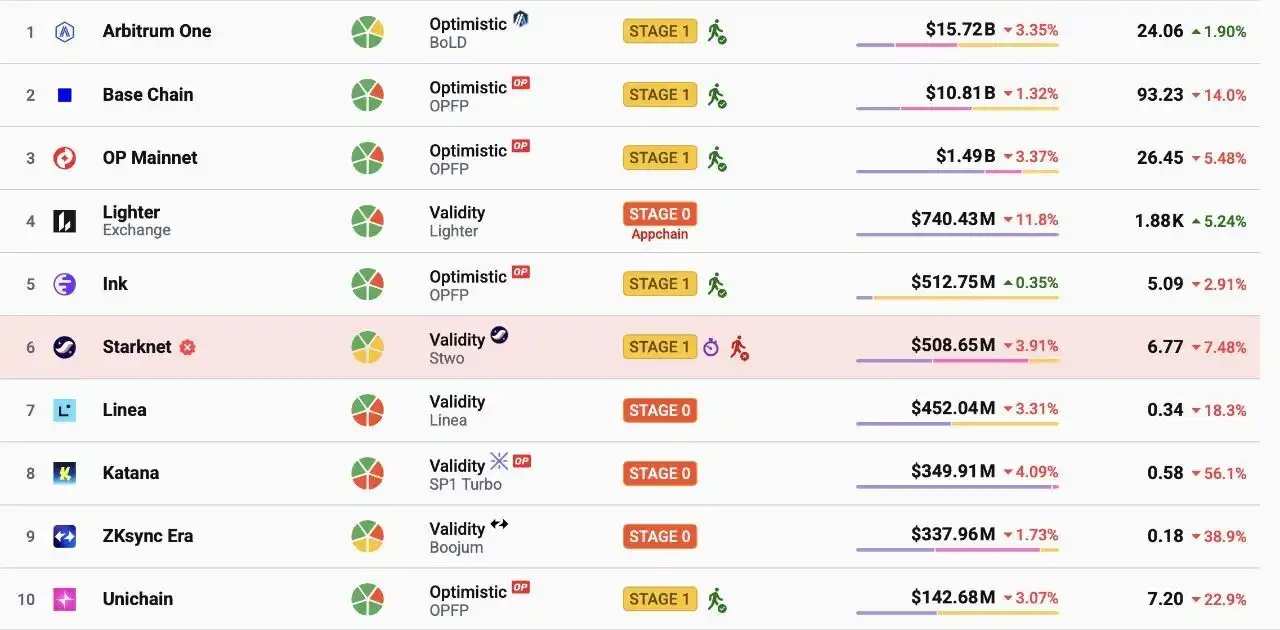

The direction is fine. But if you check Twitter, who is still talking about Ethereum?

It's not just Ethereum that's cold; the whole industry is quiet. Last year there was meme coin frenzy, Solana's comeback, the AI Agent hype. From the start of this year until now, no narrative has taken off.

Ethereum is just colder—ETH dropped from $4800 at the end of 2025 to just over $2000 now, evaporating over 60%. There isn't even much anger in the community, more a kind of weary silence.

From Archipelago to Treasury Era

But if you look at on-chain data, you see a completely different picture.

According to AMBCrypto, the supply of stablecoins on the Ethereum mainnet is still about $163.3 billion. In the $16.5 billion on-chain real-world asset market, Ethereum accounts for 58%. Last year, Ethereum spot ETFs saw a net inflow of $9.9 billion. DeFi TVL is still the highest in the industry, about $53 billion.

The people left, but the money remains. And it's not retail money, it's institutional money.

The Ethereum Foundation's own actions point in the same direction. It paused its public grants program in the middle of last year, reducing its burn rate to below 5% per year. But last week it completed its largest single staking event ever—22,517 ETH, worth about $46.2 million, locked into the Beacon Chain.

Cutting the budget while locking money into the treasury, and simultaneously funding an interoperability solution that's arriving last.

All these actions pieced together point to one judgment: Ethereum's archipelago era is indeed over. But what replaces it is not a bustling continent.

It's a treasury.

Quiet, sturdy, filled with institutional assets. Not many people live there, but it holds the most money in the industry.

Even Treasuries Don't Generate Tax Revenue, Ethereum Doesn't Make Money

Ethereum's economic model has a very simple cycle:

Users transact on the mainnet, transactions generate Gas fees, and a portion of the Gas fees (ETH) is permanently burned. The more users, the more burning, the more the ETH supply decreases.

When this mechanism first started running in 2022, the community gave it a name: ultrasound money. Meaning ETH is not only anti-inflation, but deflationary—harder than Bitcoin.

This narrative held for two years. Then L2 dismantled it.

When a large number of transactions moved from the mainnet to L2, the mainnet's Gas fee income collapsed. According to BitKE, Ethereum mainnet revenue has fallen by about 75% over the past two years. One week, the combined blob fees generated by L2s submitting data to the mainnet were only 3.18 ETH.

3.18 ETH, at the price then, was only about $5000.

A network locking $53 billion in TVL, with weekly blob revenue enough for a decent New Year's Eve dinner table in Shanghai.

If it can't burn, the supply can't be suppressed. In February this year, ETH's supply officially turned to net growth, with an annualized inflation rate of about 0.74%. "Ultrasound money" became an expired marketing slogan.

This is the cost of the L2 roadmap. Users and transactions move to L2, L2s take the fee income, and the mainnet is left with only settlement work. Settlement is important, but settlement doesn't make money.

To use an analogy, Ethereum built an economic special zone, moved the factories and shops inside, and the zone is bustling. But the tax revenue goes to the zone itself, and the central government's fiscal revenue反而 decreases. The EEZ scheme mentioned in the previous chapter wants to reconnect the special zone to the center, but what it connects back is liquidity, not tax revenue.

The institutional money is locked in the treasury, very safe. But the treasury itself, the ETH asset, is becoming increasingly difficult to narrate because it has no income.

The price drop from $4800 to $2000 is not just an emotional issue. When an asset's core narrative shifts from "deflationary" to "actually still inflationary," the market reprices it.

The situation Ethereum faces now is:

The strongest in the industry in terms of infrastructure, the most institutional capital in the industry, but the economic model is leaking. EEZ fixes fragmentation, but it doesn't fix this.

Is an Uninhabited House Valuable?

Back to the opening question: Do you still care about Ethereum?

The honest answer for most people is probably not really. ETH isn't rising, the narrative is outdated, it's troublesome to use,还不如Solana next door.

But ask it another way: Do you care about the water pipes under your building?

No, you just turn on the tap and there's water. You don't research what purification technology the water plant uses, you don't care what material the pipes are made of, and you certainly don't post on social media because of the pipe brand.

Ethereum is becoming that water pipe.

$53 billion TVL, $163.3 billion in stablecoins, 58% of the industry's real-world assets, nearly $10 billion in annual ETF inflows... These numbers indicate one thing: most of the global crypto-financial on-chain clearing is still done on Ethereum.

Not because users like Ethereum, but because institutions can't find a second pipe as thick.

What the economic zone EEZ is doing now is essentially increasing the diameter of this pipe—allowing institutional funds to flow faster between L2s, reducing settlement friction. This is useful, even necessary.

But pipes have one characteristic: no one wants to pay a premium for a pipe.

Water companies are one of the most important infrastructures in a city, but have you ever seen a water company's P/E ratio higher than an internet company's? The global clearing giant DTCC processes over $2000 trillion in transactions annually, but almost no one discusses its stock price.

If Ethereum truly moves towards becoming a treasury, a pipe, it will become extremely important, and simultaneously extremely boring. Important enough that all institutional money passes through it, boring enough that no retail investor wants to hold ETH waiting for it to rise.

But most people holding ETH today are still pricing it according to the logic of a "city." Users will grow, the ecosystem will prosper, L2 will feed back to the mainnet, the coin price will hit new highs? This is the story the Ethereum community has been telling itself for the past five years.

The reality is, Ethereum is becoming SWIFT, not New York.

SWIFT handles over $150 trillion in cross-border payments annually, and the global financial system cannot do without it. But no one speculates on SWIFT's stock because the valuation logic of infrastructure is stability.

ETH's drop from $4800 to $2000 is not just emotion; the market is re-understanding what this asset actually is.

If Ethereum's future is a treasury, then ETH's reasonable pricing shouldn't be based on user numbers and ecosystem heat, but on how much value it can capture annually as a settlement layer. At the current level of $5000 weekly mainnet blob revenue, that answer isn't very pretty.

The archipelago era is over. EEZ is here, the institutional money remains. But for those holding ETH, there's really only one thing to figure out clearly:

Did you buy a house in a city, or the right to use a pipe.